Daily Updates

CAN YOU HANDLE THE TRUTH?

The suggestion that somehow generating 3% real GDP growth a year after a bottom is bullish ignores the deep the hole we are still trying to climb out of. Normally, two years after a recession starts, nominal GDP is up 16% and real GDP is up 7.5%. Currently, nominal GDP is up 1.1% while real GDP is down 1.5% from pre-recession peaks.

According to earlier White House projections, that $800 billion fiscal gorilla unveiled last year was supposed to pull down the unemployment rate to 7% by now. Instead, we are at 9.5%. In fact, it’s really even worse than that, for if the participation rate had stayed constant at the April level, than unemployment rate would be 10.2% today.

What about jobless claims? They lead employment. Below 400k, you can have a bullish stance. Above 500k – the opposite, and recession risks rise materially. Well, that rise in the past week to 464k from 427k was even worse than it appears because the non-idling of auto plants this summer has given a temporary downward skew to the claims data – the underlying number is now closer to 475k. The upcoming seasonal factors that are “looking for” a decline are actually going to end up boosting the adjusted claims data and a test of 500k in the weeks ahead is a good bet.

What would that trigger?

Answer: more talk of a “double dip”. Claims back above 500k would be horrible for the markets (not bonds though).

The earnings news has, on net, been positive but not a slam dunk. The stock market is responding well to the Q2 reports but remember that the quarter was skewed by a strong start – after all, April was when the ISM hit its peak (in other words, it would be reasonable to assume that much of the Q2 earnings growth was “front loaded”). The economic data are interesting because they reveal a serious loss of momentum as the quarter drew to a close and there does not appear to have been a pickup in July at least based on the limited amount of survey data at hand.

Housing is still in disarray – existing home sales are a bit of a lagging indicator but even with the extension of the tax credits to deals signed but not yet closed, turnover still dropped 5.1% last month ( -10% was expected) taking sales back to March levels.

What was more critical was the huge jump in months supply… now at 8.9 months’ versus 8.3 months’ in May – the highest since August 2009, and well above the 5-6 months’ that would typify a well-balanced market.

Of course, we also had the “official” leading indicator come out and verify what the ECRI has been saying – when the financial market components are stripped out, the decline goes to -0.4% (as opposed to -0.2%) which is the second decline in the past three months. And the coincident/lagging ratio, a favourite among some pundits (like a book-to-bill ratio for the entire economy) dipped for the first time since February of this year.

The stock market still seems to be driven largely by technicals and momentum trading. The economy has clearly reached an inflection point and this won’t be ignored indefinitely. The gains yesterday were large and broad-based, but lacked volume again, which calls into question the overall level of conviction.

And the fact that the Treasury market retains such a positive overall tone is a development that is failing to ratify the whippy bounce in the major averages back to their 50-day moving averages.

The summer rally came, we shall see soon enough if it is over, but with all the sturm and drang, let’s face it – we’re exactly where we were one month ago – on June 22nd, the S&P 500 was sitting around 1,095. And with 10 of the 22 trading days producing moves of 1% or more, one usually has to go to Six Flags for rides like this (thanks Josh!).

More: In this issue of Breakfast with Dave

• Just-released soft CPI data out of Canada should help Carney sleep better at night

• What are the bulls looking at?

• Leading economic indicators are now down the past two of three months

• Down 5% is good?

• Bank of Canada trims global GDP forecasts on sovereign debt crisis worries

….read more Breakfast with Dave

Michael Campbell interviews David Coffin of Hard Rock Advisories on Gold, the Metals markets and the companies they search for. Companies “with the potential to at least double over one or two years based on asset growth and development of metals deposits for production or take over by larger companies.”

Michael Campbell: I am very pleased to welcome back to the show one of the coauthors of the Hard Rock Advisory, David Coffin. David, I appreciate you taking the time in the weekend with us.

David Coffin: My pleasure, Michael.

Michael Campbell: I want to start with the kind of action you have seen in the gold market generally, one of the things that you cover in the Hard Rock Advisory. The bigger picture David, looking at the kind of action, the price action, you have seen in gold over the last while.

David Coffin: While the gold prices of course moved up to historic heights and it is consolidating around the $1200 level, I think we are in a market that makes it difficult to try and give precise near-term timing, but what we are seeing is the notion that gold should be part of a portfolio, as insurance value has grown and we think that is going to support the price and move it higher in due course.

Michael Campbell: Random noise out there compared to what you see as the broader trend?

David Coffin: Oh, definitely. Right now, you know, what you are talking about it is the 1% and 1.5% move, but the market in general is volatile. It is that something that you can shake off on a day-to-day basis. You have got to look for trends and we are still very much in an upward trend for the gold price.

Michael Campbell: When you look at individual companies, what is the environment for them out there right now in terms of raising money? Two years ago it really did not matter what quality you had in the ground, it was just difficult to go get money. Has that environment changed significantly? As gold has performed so well, has that also eased the taps of finding available cash?

David Coffin: It has not eased at the level of exploration companies per se. What has happened though is, they came back on with everything else after the credit crunch. So, there is money available if they are properly priced now. It is not as easy as it has been, but for gold and good solid gold companies, there is definitely a market and the money is available. You take the Yukon Gold play for instance to the larger players there, are in the middle of financing after having taken significant upticks since beginning of the summer, so the money is available if you show the goods.

Michael Campbell: What things do you look for in this environment that leads you to make the recommendations in the Hard Rock Advisory that have done so exceptionally well. What are the key components on your checklist?

David Coffin: Management is important, the availability to finance, which we just talked about and the two of them are tied together. The assets themselves are quite important to us. We start by looking at what the people have for holding and within that context, there has to be a geological potential, but there also has to be the right environment so that the project can be taken forward to corrasion, in other words the geopolitics. The geopolitics, some countries we are not very interested in or not interested in at all. With the gold project unlike a base metal property proximity to a coast is not quite so important, but infrastructure is important. One of the things that is aiding the Yukon right now is an infrastructure improvement that is underway there. Both will be the main points.

Michael Campbell: You mentioned the Yukon project, that it helps it is in Canada. Political risk has clearly become involved in certain countries in South America and certain countries in Africa. It tends to color all projects in those areas to some degree because it feels so volatile to us here. Has that been the pivotal component in making a project a disaster if the wrong government comes to power?

David Coffin: Oh, definitely. Conversely, if governments change and the right one comes to power, that can sometimes open up opportunities, but yeah, definitely there are some places that we leave alone that we are not interested in, Venezuela, say. We are interested in Colombia because the politics there have been changing and it has got a strong gold belt. We look at the world that way without question.

Michael Campbell: What timeframe for investors do you look at when you make specific recommendations in the Hard Rock Advisory?

David Coffin: It depends on the situation. We will come into a stock based on management and good general geology, from time to time; in other words, we will come into an area if you will. As often as not we would like to come in on specific targets and the timing that we would like is typically a matter of months away from potentially a discovery or a post discovery if the targeting information indicates that the potential is there for scale and the company has not moved so strongly that they are already priced to its overall potential.

Michael Campbell: Do you worry that this cycle is running out of steam at this point, the general commodity cycle outside of just gold?

David Coffin: No, we are not worried about it running out of steam per se. What is worrying is that there were two components to the extension of this cycle. One is the one I think most people recognize now which is China, but China plus India, China plus Brazil, China plus Indonesia, a whole list of large countries, which are seeing their economies mature and industrialize, that is what is driving it from the demand side, but there was also issues on the supply side. There was a long period when it was difficult to capitalize and make money with the mining project and because of that development of them slowed. So, what we have seen is we have matured through the point where the big upticks in price due to demand from China pushing into a lack of supply because mines are not being developed coalescing, but what you have to do is look back and say the price of gold had been 250 an ounce is now 1200, price of copper had been 60 to 65 cents a pound is now $3, nickel $2 is now $8. That first big price move has happened. What we believe is that as we get through the credit crunch, but more importantly as other large economies, India in particular move into their high growth periods, you are going to see that new increase in demand, again makes it difficult for the sector to keep up with the supply and probably push the price of at least some metals, considerably higher for a while.

Michael Campbell: David, we have been talking a little bit about looking forward here and of course what you do is with your geological background, you go look at these properties, these individual mining situations and you have your set of criterion of what would qualify. Then of course there comes times the baby gets thrown out with the bathwater, as when the overall market dropped 260 points yesterday in the Dow and Toronto was down. Sometimes that presents opportunity because people are forced to sell. Maybe they get a margin call, maybe they just want a raise cash, maybe they are just nervous. Can you give us maybe a couple of situations that we could put on our radar screens, a couple of things through all of your work that you think are of interest to pick up on selling?

XAU Seasonality Chart below provided by Don Vialoux’s EquityClock.com

David Coffin: Sure, your listeners should keep in mind that what I will be talking about are speculations on higher risk stories, but I will go into each of them a little bit and explain the risks. I have mentioned the Yukon a few times. In the Central Yukon by way of background, the current push in that territory results from a company named Underworld, being taken over by Ken Ross. That was just finalized a few weeks ago. The takeover had started a few months ago. Underworld made their discovery about 2 years ago. So, this has been a fairly quick moving story. In the Yukon, there is a couple of other companies and both as I mentioned that are doing placements and both of which have had strong upticks. So, bearing that in mind, Kaminak (KAM.V) has been the one that we have followed fairly closely. The other is a company named, ATAC (ATC.V) who made the discovery last year in the Yukon.

What Kaminak has done was last year, in a project near Underworld’s, they picked it up, they did the soil sampling, they did the basic targeting. They got some strong surface results from trenching. This year they have been drilling it, they put from 2 zones that have been tested so far, quite strong results, still early in the process. Our comment now to subscribers is they have put a potentially viable result on the table. They will be in the process of moving a long trend and testing other targets and we think they have lots of room in this summer to expand in terms of evaluation potential beyond the correct pricing and they are picking up a $10 million at $1.50 in a BOT deal financing, there may be an opportunity during that financing, since it is not likely to report any results to pick up some stock at this level on bad speculation basis.

A couple of other companies that are coming along, but still to report results, in other words still more pure speculation, a company called Silvercrest (SVL.V), we had mentioned them a few months back. We just recently told subscribers that we are moving them to an accumulate status, they have in the past week since we mentioned, that they can have a significant uptick, so look for a little bit of weakness in that market if you can, another that we are following who is drilling a little further away, but still in that play and who have a series of targets coming is Northern Tiger (NTR.V). We told subscribers to start picking that up a while ago. They are a little lower in price. They are still earlier because none of their projects have shown discovery potential yet. So they are more of a pure speculation, but certainly worth a look at.

East Asia Minerals (EAS.V) has put a large discovery on the table in Indonesia. It has had a pullback along with a lot of other stocks beginning a few months ago. We feel it is trading in a good range. We don’t feel it is undervalued, but we do feel that the project still has a lot of upside potential. We looked at it on that basis.

One that may interest a different group of people, Silvercrest (SVL.V), they are in the midst of building a mine in Mexico. It is a gold silver mine. They are to be in output by year’s end and we feel that their current pricing is below what they should be trading at cash, below by a significant amount. From there, the growth will come from further expansion on this project and looking at other projects primarily in Mexico in the gold silver space.

In West Africa, Burkina Faso is another area that has had a very rapid expansion of gold output over the last 6 years. It has grown from having no commercial gold mines about 4 years ago, to having by the end of this year, if unless one of the two newer developments get side tracked somehow, it will have 6 mines in production with 750,000 ounces total, very substantial for the country. The company we are talking about there is called Riverstone Resources (RVS.V). They have been working in country for quite a while. They have established a resource of over a million ounces. They recently found several new zones. They did significant financing. So they are well cashed up and they are in the process of determining how much expansion may come from those zones as they drill them off. The company we like quite a bit. West Africa, has been important to the gold space, Ghana is well known to everybody I think who knows the gold mining sector. Burkina Faso is the next country inland and it is proven to be an excellent place to go, discover, and put into production Gold Deposits. We think Riverstone is trading at a little below now because they have had to pullback with everybody else. It is a matter of how much more the drill depth is going to add to their valuation over the next 6 to 18 months.

Michael Campbell: One of the questions I always get from people is when to buy into and when to sell, positions like this.

David Coffin: Sure and it is important thing in terms of both selling and take profit to reduce your risk. One basic time to buy is, as the saying goes, when the blood is running in the street, best buying opportunity most of us will ever see happened early last year. Now that we are into somewhat more of a normal market, but one that is highly volatile and which will certainly have lower periods, it is worth keeping that in mind. You don’t really want to go in and buy much of anything after the market has taken a strong uptick. Typically, you wait for that to settle down and to pullback and use that as a buying opportunity.

At a more specific level, there are a couple of different ways to look at this. One is to come in before a stock has made a discovery. I mentioned a couple like that, but have put out good solid property information that suggests the target of the right type and as importantly of the right scale potential and a company that has been run by management who understands how to deal with those results, then you are taking a speculation. In that case, the company should have enough financial backing and enough other ideas on the table to give you some comfort that they can continue, but you do have to view that for what it is, that is a company that has not yet demonstrated an asset liability, therefore, it will shift down in a weak market.

The other time is post discovery, I mentioned a couple, Kaminak, in particular this year have put discovery level results on the table. The nature of the risk changes, it does not go away, that has to be kept in mind. Kaminak have demonstrated that they have a project in the Yukon, as have others on the list that I mentioned and a number of others, of course, in the world. They have demonstrated that they have the right type of geology. They are showing metal grades and thicknesses, which can be viable if the ongoing drill program expands that deposit to a scale that allows you to capitalize the development, and the development of course itself would be depending on where you are, a minimum of 5 to in some areas with some deposit takes 10 years away; so that also has to be kept in mind. Now having looked and seen that potentially viable results are put on the table, in another words, a drill has cut through a deposit and located good grades at appropriate thicknesses, you then have to think in terms of what will be required as a minimum to make a viable situation in a place like the Yukon or most others, where typically looking for targets that have a scale of certainly of a million ounces, but ideally of several million ounces or more as a potential. Usually that is what is needed in order to put the pieces together to bring a mine to production.

Ideally, we would like to see much bigger, as in the case of East Asia and in that case where you are looking at a country that has a mature mining industry, but in that particular part of the country has not had recent development or a lot of recent foreign investment you want to see a somewhat better situation, a larger deposit with good grades.In the case of a company like Riverstone, where the country has been developing mines for the past few years and has the demonstrated capacity to do that you have a got a little more comfort, there you are back into the somewhere between a million and two million ounces depending on deposit type and viability it is going to be a your threshold for mine development.

Now, the next point where you might want to come in is after that exploration process has been done, the evidence of a viable scale, and then more importantly the evidence of other requirements, the right metallurgy, etc., those studies have been completed, that is another point when you can come in. This is very market dependent. In a strong market companies can get priced up and through their actual cash flow potential. So you do have to be cognizant of that. The period such as we are in there are a number of companies around, who are priced below their cash flow potential, the market is risk averse, that can be a buying opportunity and typically you are looking for a situation in this market potentially a stock that can double. You do again have development risk. Even though all of the studies have been done, the details have been put on the table, there will be circumstances in which conditions are actually different than expected and results are not as strong as hoped for, so you do have to keep that in mind, which brings us to the fourth period.

Post development when a company has demonstrated that the mine is viable, then you are buying into a growth company. If you are looking for that type of situation, what you need to see is that the initial project is large enough to give the company sustainable cash flow for long enough that they can then make their decision on the next point, the next way to grow the company. That in the mining space is typically for a startup company, a development with a 7 to 10-year mine life in that range, ideally something bigger, but that is ample to get full valuation. The company with a strong project is going to run 4, 5 to 6 years is certainly viable and the company will give them price, but you want to look for a little quicker capital repayment in that situation, that is something more along the lines what Silvercrest looks like to us right now.

Michael Campbell: As you say, it is just such a fascinating area and I think there is going to be some massive opportunities that will come in the next few years and it is most helpful to hear that the people can also go to www.hraadvisory.com. David, thank you so much for taking the time in the weekend, always great to talk with you.

David Coffin: My pleasure.

Who are these guys and how do they keep finding winner after winner before other analysts do?

The “secret” to their success is simple. It’s hard work. A LOT of it. The other key to the success of HRA publications is the background of the editors, David Coffin and Eric Coffin. They are brothers, born in a mining town and raised in the industry. They have both spent decades in the resource business. This gives them a background of real practical experience that no other editors can match. That’s why they can spot winners before anyone else. They have “been there and done that” on both the geology and the market fronts. They’ve run exploration programs, helped form and structure companies and they know what works and what doesn’t. They know everyone in the sector and can quickly check the facts and the management on new opportunities. HRA readers profit from their special insight into metals and exploration gained from over 50 years of combined experience in the resource sector. It’s an unbeatable combination that delivers unbeatable returns for HRA readers. Not politics, not rumors, not regurgitated broker research – just hard work, real insight and real gains.

Subscribe HERE

Recent economic data is pointing toward a second wave of recession … and maybe even outright deflation. One key consequence: Long-term interest rates are low and getting lower.

Today I’m going to tell you about some exchange traded funds (ETFs) that I think can thrive in this short-term, falling-rate environment. First, let’s take a look at some evidence the economy is entering the dreaded “double-dip” part of the cycle …

Inflation is staying low. The Consumer Price Index (CPI) — the key gauge of price inflation in the U.S. — is growing at an annualized rate of only about 1 percent. Some of the component prices, like energy, are actually falling.

Moreover, the monthly changes show the deflationary trend is accelerating. June was the third consecutive month that the CPI for All Urban Consumers (CPI-U) actually fell when seasonally adjusted.

When the price of our everyday purchases is flat or falling, it’s very hard for the price of money — which is what “interest rates” are — to rise.

Consumers are losing confidence. The days of carefree trips to the mall and splurging on useless stuff are gone for most Americans. People are overloaded with debt, worried about their jobs, and afraid their savings (if they have any) will evaporate in volatile markets.

This is no doubt a big reason why the University of Michigan Consumer Sentiment Index plunged last month at a rate we haven’t seen since the October 2008 Lehman Brothers collapse, and before that in September 2001.

I’m all for frugality and simple living, but this presents a problem for the retailing industry. They need people to buy things. Increasingly, the only way to motivate consumers is to cut prices to unheard-of levels. This points toward deflation, not inflation.

The housing market is going nowhere. Right now we are in the time of year that has historically been the peak selling season for residential real estate. If they must move, people with children try to do it in the summer.

So when the Mortgage Bankers Association reported that the number of new mortgage applications in the second week of July dropped to its lowest level since December 1996, realtors must have shuddered. People just aren’t buying.

What happened?

Part of the reason is that the special homebuyer tax credit that recently expired moved a lot of demand forward from summer into spring. Now we have a hangover effect with a humongous supply of homes for sale. This creates serious downward pressure on housing prices.

The Federal Reserve, the banks and the Treasury are well aware of all this. But there isn’t much they can do about it that they haven’t done already; so look for the trends to continue. If anything, we’ll see them try to push mortgage rates even lower to help out the builders and mortgage lenders.

As you can see the big-picture outlook points toward falling interest rates … for the short-term anyway. In fact, it’s already happening.

Since the beginning of April, the ten-year Treasury bond yield plunged from almost 4 percent down to below 3 percent. That’s a huge move in only three-and-a-half months.

Will this trend continue? Hardly …

Runaway government spending is bound to push interest rates higher and bond prices lower as Washington scrambles to cover all the new debt. And when you pile on the commitments made to fund Social Security and Medicare, it’s easy to see why interest rates are almost guaranteed to go up soon.

But what we’re experiencing right now with rates falling could still be a great short-term opportunity. But where?

ETFs for Falling Rates

Individual bond trading is tough to do in small amounts, and most bond mutual funds are designed for income, not speculation.

However, bond ETFs could be the ideal vehicle if you just want to bet on a short-term price trend like this one. Bond prices rise as interest rates fall, and the impact is magnified in long-term bonds.

Here are three bond ETFs that are well-known, easily tradable and sensitive to changes in long-term interest rates. Therefore, they give you the flexibility to get out quickly when yields start to shoot back up and bond prices plummet, which they indeed will. And once bonds have sold off, you can jump back in again:

- iShares Barclays 20+ Year Treasury Bond ETF (TLT). This one is about as simple as they get. It’s a plain-vanilla bond fund that holds U.S. Treasury securities with a maturity of 20 years or longer.

- Vanguard Extended Duration Treasury ETF (EDV). This is a “zero coupon” bond fund, which means there are no interest payments. With no coupon, the moves in the underlying bond prices are more exaggerated than with traditional coupon-paying Treasury bonds. EDV is a pure bet on falling Treasury rates.

- Direxion Daily 30 Year Treasury Bull 3X Shares (TMF). Hold on to your hat! This ETF tries to triple the daily change in the price of 30-year Treasury bonds. Needless to say, you should expect a wild ride and your timing has to be near-perfect. But if you can handle the risk, TMF is a way to maximize your exposure to falling Treasury yields.

Treasury rates have fallen a long way in the last few months, and a correction could unfold at any time. Even so, I think this is a case for making the trend your friend.

Best wishes,

Ron

P.S. I just put the finishing touches on my ETF Field Guide. See why this is the one report Wall Street’s fund managers don’t want you to read.

This investment news is brought to you by Money and Markets. Money and Markets is a free daily investment newsletter from Martin D. Weiss and Weiss Research analysts offering the latest investing news and financial insights for the stock market, including tips and advice on investing in gold, energy and oil. Dr. Weiss is a leader in the fields of investing, interest rates, financial safety and economic forecasting. To view archives or subscribe, visit http://www.moneyandmarkets.com.

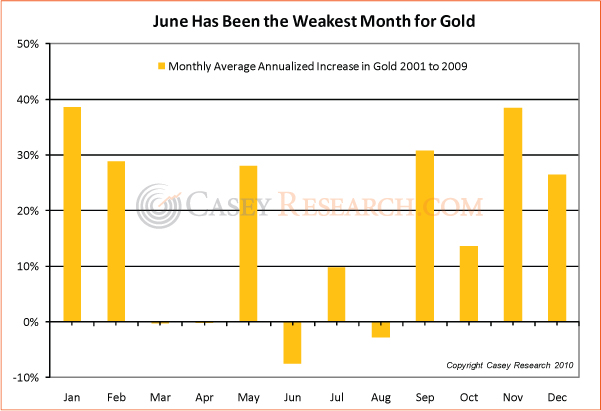

While we’re convinced gold and gold stocks are destined for much higher levels, buying when prices are low can mean the difference between a double or triple and a ten-bagger… a week in Malibu vs. a week in Milan.

There’s no secret formula to buying low, and we aren’t holding the right hand of Midas, but there are periods when prices tend to be lower than others. And if those tendencies play out, it can give us the opportunity to snag a high-quality asset at a bargain price.

So, how do you get a bargain price? You cheat.

I think the secret to getting a low-cost basis on all your gold and gold stocks is this: only buy on significant price pullbacks.

And this can be done without trading or using technical analysis.

I think there’s a good chance we can cheat this summer. For example, here are the average monthly increases in gold since our bull market began in 2001.

….read more and view 4 more timing charts HERE

“UNUSUALLY UNCERTAIN”

Those were the words Ben Bernanke used to describe the macro outlook. He refrained from discussing double-dip risks, but in contrast to the market’s desire for more policy juice, he actually spent more time talking about the how, “at some point, the Committee will need to begin to remove monetary policy accommodation to prevent the buildup of inflationary pressures”.

Amazing – the Fed is still pre-occupied with inflation at this juncture – David Rosenberg To register for David’s Market Musings and Data Deciphering go HERE

Bernanke Says Economic Outlook is “Unusually Uncertain”, Fed Prepared for “Actions as Needed”

Be prepared for Quantitative Easing Round 2 (QE2) and/or other misguided Fed policy decisions because Bernanke Says Fed Ready to Take Action.

Treasuries rose, pushing two-year yields to the fourth record low in five days, as Federal Reserve Chairman Ben S. Bernanke said the economic outlook is “unusually uncertain” and policy makers are prepared “to take further policy actions as needed.”

Ten-year note yields touched a three-week low as Bernanke said central bankers are ready to act to aid growth even as they prepare to eventually raise interest rates from almost zero and shrink a record balance sheet.

“An unusual outlook may call for unusual measures, and that means the Fed may take more action as needed, which would lead to lower rates,” said Suvrat Prakash, an interest-rate strategist in New York at BNP Paribas, one of the 18 primary dealers that trade with the central bank.

The Fed chief didn’t elaborate on steps the Fed might take as he affirmed the Fed’s policy of keeping rates low for an “extended period.” Economic data over the past month that were weaker than analysts projected have prompted investor speculation the Fed may increase monetary stimulus in a bid to keep the economy growing and reduce a jobless rate from close to a 26-year high.

“Bernanke acknowledged that things weren’t very strong economically and left action on the table without going into details, and that’s sending investors from stocks into bonds,” said James Combias, New York-based head of Treasury trading at primary dealer Mizuho Financial Group Inc.

Bernanke Has Met His Match

Hyperinflationists will be coming out of the woodwork on the Fed’s statements today. However, I calmly note that Bernanke has met his match: consumer attitudes.

We have reached a Consumption Inflection Point – No One Wants Credit and consumer spending plans have plunged. There is nothing Bernanke can do to “fix” that.

Besides, there is nothing to “fix” anyway. Boomers headed towards retirement better be saving more and spending less. The same applies to kids out of college without a job.

Finally, I note that Bernanke thinks consumer spending is on the rise. It’s not. Bernanke needs to get out in the real world and see what’s happening. He can start by reading Rockefeller Institute Confirms Rising Retail Sales a Mirage.

Mike “Mish” Shedlock

http://globaleconomicanalysis.blogspot.com

Click Here To Scroll Thru My Recent Post List

Mike “Mish” Shedlock is a registered investment advisor representative for SitkaPacific Capital Management. Sitka Pacific is an asset management firm whose goal is strong performance and low volatility, regardless of market direction. Visit http://www.sitkapacific.com/account_management.html to learn more about wealth management and capital preservation strategies of Sitka Pacific.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair