Daily Updates

7/28/10 Paris, France – Yesterday, the rally on Wall Street slowed down a bit. The Dow rose 12 points.

Gold had a bad day – down $25. We had guessed that gold would be going down. But it is still too early to detect a real trend. For the moment, the financial markets and the economy are going in different directions. The stock market is signaling a boom. The economy and gold are signaling a bust. We’ll have to wait and see which direction prevails…

In the meantime, had a seer come to us a couple of years ago with a tale of back-to-back US deficits totaling $3 trillion over two years, his credibility would have been in doubt. Had he also foreseen US Treasury debt at record low yields – at the same time – he would have had no credibility at all.

One of the surest things we thought we thought we knew back then was that the government could not simultaneously run huge deficits and borrow cheaply. It was one or the other; that was all there was to it.

It turns out that Dick Cheney was right all along. Deficits don’t matter. At least, they don’t matter until they do matter.

And they don’t matter right now. Bloomberg:

For all the criticism of record budget deficits, President Barack Obama can take comfort knowing that for the first time in half a century, government bond yields are declining during an economic expansion and Treasury Secretary Timothy F. Geithner is selling two-year notes with the lowest interest rates ever.

The combination of record-low yields on two-year notes, 10-year rates below 3 percent and a deficit projected to surpass $1.4 trillion for a second consecutive year is a signal that the bond market is less concerned with government spending than with getting the economy back on track.

The last time yields were this low as the economy expanded was in 1955, when Ray Kroc founded McDonald’s Corp. and Bill Haley’s ‘Rock Around The Clock’ topped the music charts. The 10-year note yield averaged 2.65 percent that year, according to monthly data compiled by the Fed, while the economy grew 6.4 percent, consumer prices for the year declined 0.4 percent and the government ran a fourth consecutive budget deficit.

Why have yields fallen so much? Because the economy is not recovering. Investors look for a safe place to put their money. Bloomberg continues:

“Expectations of growth over the next couple of years have indeed come down,” Alan Blinder, former Fed vice chairman, and economics professor at Princeton University, said in a telephone interview. “There is still plenty of fear out there in the world financial markets, which has investors all over the world scurrying into Treasuries, even though they get paid very little.”

We opined – without doing any research on the subject – that Harley Davidson had probably peaked out. Only old men ride Harleys. The young prefer a different style of bike. We guessed that it was time to sell the stock.

Naturally, the company’s earnings have soared since then. But not because of increased sales. Instead, like the rest of corporate America, Harley is learning to earn more money without selling more merchandise.

The New York Times has the story:

Motorcycle sales are falling in 2010, as they have for each of the last three years. The company does not expect a turnaround anytime soon.

But despite that drought, Harley’s profits are rising – soaring, in fact. Last week, Harley reported a $71 million profit in the second quarter, more than triple what it earned a year ago.

This seeming contradiction – falling sales and rising profits – is one reason the mood on Wall Street is so much more buoyant than in households, where pessimism runs deep and joblessness shows few signs of easing.

Many companies are focusing on cost-cutting to keep profits growing, but the benefits are mostly going to shareholders instead of the broader economy, as management conserves cash rather than bolstering hiring and production. Harley, for example, has announced plans to cut 1,400 to 1,600 more jobs by the end of next year. That is on top of 2,000 job cuts last year – more than a fifth of its work force.

Everyone is doing the right thing. Households are reducing spending. Business is reducing its costs. GDP growth is falling and investors are taking shelter in Treasury debt.

So what’s the problem? Well, the feds can’t bear to see people doing the right thing. They want them to do the wrong thing – that is, they want them to spend money they don’t have on things they don’t need. Why? Because it makes the economy look good…and makes them look like they know what they are doing.

It’s all hokum and folderol, dear reader…all hokum and folderol…

Bill Bonner

for The Daily Reckoning

A very well-known and internationally respected forecasting firm believes the price of oil is headed “unimaginably higher” in the next few years. To somewhere north of $300 a barrel.

I couldn’t agree more.

What will drive the price of oil so much higher, when most of the western world is either in a deep recession, or worse, a depression?

We can talk about peak oil, or supply and demand forces, global warming, and so forth. But in reality, oil ultimately heading to $300 comes down to two very simple forces …

First, the inevitable demise of the U.S. dollar. I’ve written many times about this in the past, and I’ve been one of the only analysts in the world who has accurately predicted the now almost 11-year long bear market in the dollar.

Make no mistake about it: Despite an occasional rally in the dollar, the greenback is utterly destined to lose at least half its current purchasing power in the next two to three years, if not more.

And then even lose its status as the world’s reserve currency.

The reasons are varied, and inevitably bearish for the dollar. All you have to do is understand that the Federal Reserve stands ready, willing, and able to print unlimited amounts of paper money to pump up the U.S. and global economy, and that it will not hesitate to do so.

Federal Reserve Chairman Ben Bernanke confirmed it last week at his testimony on Capitol Hill when he stated emphatically that the central bank stood ready to act if the economy slows, and will take additional measures to support the economy.

That’s why, despite all the hullabaloo about the dollar’s recent rally in forex markets, the dollar has shed 7.33% since June 7, a whopping decline by any measure.

Second, the inevitable rise of China. At its current rate of economic growth, which is NOT going to slow substantially anytime soon, China’s economy will overtake the U.S. economy in less than 10 years.

And one of the ways China’s growth is showing up is, naturally, in energy demand.

In fact, according to the International Energy Agency (IEA), in 2009 China officially overtook the U.S. as the world’s top energy user, far faster than expected, and in spite of the global financial crisis.

China used up 2,252 million tons of oil equivalents last year, about 4% more than the U.S., which burned through 2,170 million tons, according to data from the IEA.

But energy consumption in China is still in the early stages of its growth.

In terms of total energy usage on a per capita basis, U.S. consumes 11.4 kW per person per day, while China consumes only 1.6 kW.

In other words, China consumes one-seventh of the amount of energy the U.S. consumes on a per capita basis — and China is already the world’s biggest consumer of energy.

As China’s economic growth continues and hundreds of millions more people are lifted out of poverty, it’s not too hard to see how the country’s need for all forms of energy is going to explode higher.

Or how that demand could easily push the price of oil “unimaginably higher” in the years ahead.

My view: Oil is one of the very best investments you can make in your portfolio for the long haul.

No matter what the economy or stock markets do shorter-term.

That’s why, in just the last 12 days, energy shares have been exploding to the upside, with the typical oil and energy share gaining more than 11%.

And all of this is also why I expect a huge wave of mergers and acquisitions in the energy sector in the months and years ahead.

Huge, burgeoning Asian demand for energy and energy services, generating surging revenues … plus the sliding value of the U.S. dollar will mean loads of companies will also want to put their money to work in the energy sector.

Which is why you should consider investments for the long haul

in my …

Short List of Prime Investment

Candidates in the Oil and Energy Industry

These are oil and energy companies I believe every investor should own a piece of for the long haul. They represent the top players in their particular niches in the industry … or have huge undervalued oil and gas reserves … and could eventually be prime takeover candidates by larger companies.

They are certainly not the only ones. But they are companies I would consider buying now and putting away for a few years.

Each and every one of them could easily double … triple … or even quadruple in the next couple of years. I suggest you buy them and sock them away.

Not at the expense of any of your gold investments, mind you.

Lastly, stay out of the broad stock markets, except for the above investments and any others recommended in my Real Wealth Report.

Short term, yes, the Dow could rally back to the 11,000 level. But the risk is to the downside, down to Dow 9,000, and probably lower, to Dow 8,700.

You can see the cycles forecast in this updated cycle chart that my colleague, Richard Mogey at the Foundation for the Study of Cycles, and I just put together. While we do expect a rally into late August/ early September — thereafter we should see one doozy of a decline, a nasty sell off that will catch most investors way off guard.

The way I suggest to play it: With an inverse ETF on the broad markets, such as the ProShares Short S&P 500, symbol SH, or the ProShares Short Dow 30, symbol DOG.

But don’t buy them yet. Consider buying them as soon as you see the Dow hit 10,800.

Finally, don’t listen to all those pundits out there who are telling you to get out of Asian, and especially Chinese-based investments. They’ve been wrong time after time about Asia and China, and they are going to be dead wrong again.

Instead, Asia and China, in addition to gold and oil, represent your keys to wealth in the months and years ahead. So be sure to also follow our Asian expert, and my good friend, Tony Sagami’s column, published every Wednesday.

Best wishes, as always, for your health and wealth!

Larry

P.S. For just $99 a year you can get ALL of my timing signals, recommendations, risk reduction strategies, insights into the markets, including how I expose how the powers-that-be that are destroying our dollar — and more. It’s a freaking bargain. Join now by clicking here.

This investment news is brought to you by Uncommon Wisdom. Uncommon Wisdom is a free daily investment newsletter from Weiss Research analysts offering the latest investing news and financial insights for the stock market, precious metals, natural resources, Asian and South American markets. From time to time, the authors of Uncommon Wisdom also cover other topics they feel can contribute to making you healthy, wealthy and wise. To view archives or subscribe, visit http://www.uncommonwisdomdaily.com.

Editor’s Note: Toby Connor is the author of Gold Scents, a financial blog with a special emphasis on the gold secular bull market.

Last week I was told that we were going to see more gold weakness in the days ahead because big money had to sell their positions. Folks, smart big-money traders don’t sell into weakness. These kinds of investors don’t think like the typical retail investor who’s forever trying to avoid drawdowns. Big-money investors take positions based on fundamentals and then continually buy dips until the fundamentals reverse. The fundamentals haven’t reversed for gold so I’m confident in saying that smart money isn’t selling its gold, it’s using this dip to accumulate.

With that being said, there are times when big money will sell into the market and it’s why technical analysis, as used by retail traders, often doesn’t work. They sell into the market to accumulate positions. Let me explain.

….read more and view 3 charts @ Gold Bears Are Wrong, Smart Money Isn’t Selling

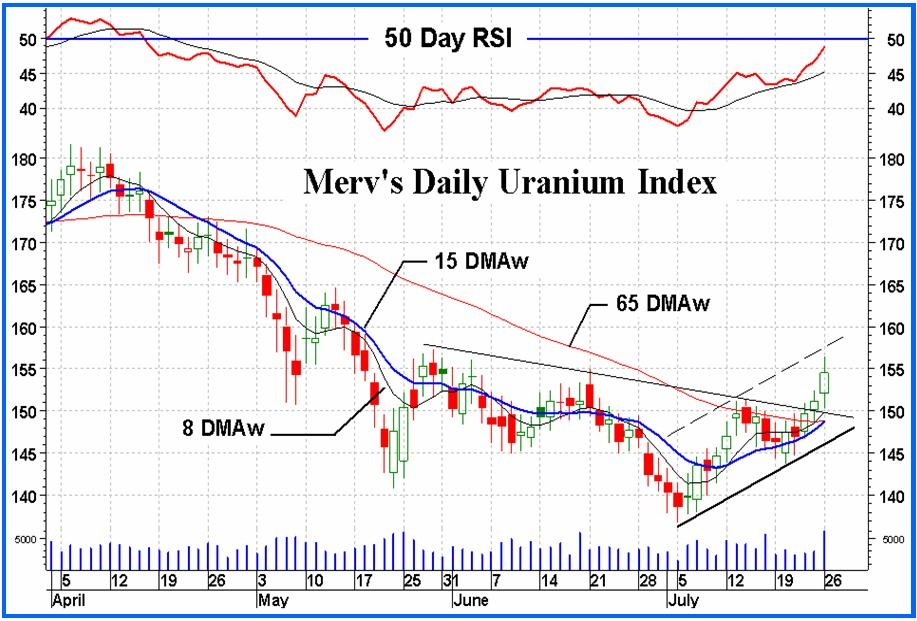

Uranium stocks were notably stronger yesterday (see 4 stocks lower below) on news that the spot price of uranium oxide rose $2 U.S. per lb. last week to $43.50. Nice breakout! – Don Vialoux

It was a great day yesterday with a 2.28% rise in the Daily Index but a 5.31% rise by the average component stock. The cheepies are on the move. Many double digit movers yesterday. Let’s see what happens today. – Technically Uranium with Merv

Blast Off! – 4 Uranium Stocks

All Charts by Don Vialoux – BNN Clip on Denison Mines “Highest Grades in the World”

For an update on Denison Mines’ Wheeler River uranium project, BNN interviews Marin Katusa, Chief Investment Strategist say’s drill results “Highest Grades in the World” – Click HERE

Glowing Reviews for Uranium Plays + The Scoop on Major Discoveries

You don’t hear a lot of talk about uranium these days. It’s just not as sexy as gold or silver. But with a host of reactors slated for construction, the sector is rife with opportunities. Haywood Securities Analyst Geordie Mark visits numerous uranium projects each year, researching plays at all levels. In this exclusive interview with The Energy Report, Geordie tells us why he’s given “sector outperform” ratings to no less than 11 companies. It could be the most comprehensive global roundup of uranium plays anywhere.

The Energy Report: The spot price for uranium was $40.75 a pound on June 21, when the long-term price for uranium was $58—a spread of $17.25, or 42%. What’s poised to support a 42% price increase?

Geordie Mark: The spot price actually moved up to $41.75 that night, the first move to the upside in quite a number of months. It’s a positive response to demand coming onstream. The long-term contract market is very different from the spot market; and, historically, it’s significantly bigger in terms of the volumes that are traded. We’re seeing the spot price moving to meet those contract prices going forward. We also think there’s a backdrop of significant demand increase due to a delay in the development-stage projects resulting from financial crisis issues and general market conditions.

TER: How far out do you see the spot price and the futures price meeting?

GM: We’re looking at a marriage maybe even by the end of 2011, with a spot price of $65 and a long-term move out to $70. We certainly expect to narrow the current gap by that point.

TER: And you said part of that is due to the number of projects coming onstream?

GM: That’s right. A few development-stage companies will go into production but, certainly compared to 2007, there have been delays due to equity raising. The number of new projects going forward has been stymied when those projects needed significant capex for development.

TER: At the same time we have a number of new reactors being built.

GM: That’s true. Over the last two years, we’ve seen some significant growth in the number of reactors going into construction. I think something like a 58% increase in the number of reactors are on the planning board; that’s a very good size in terms of a steady increase in future demand.

TER: Given the number of reactors being built or scheduled, why haven’t uranium stocks performed better of late?

GM: There’s a relationship between share prices and general market conditions. Over the last two years, both spot and long-term prices have come off somewhat in response to global financial conditions. I believe spot has come down from about $59 and long-term prices from $80. Company valuations are quite closely linked to commodity prices, so you’re basically seeing the relationship to a softening in the commodity price over that two-year period.

TER: So with demand slated to rise significantly, we should see a corresponding rise in share prices of uranium miners and explorers?

GM: That’s our target forecast for our covered companies and where we see the commodity price going in response to increasing demand. I think the interesting thing is that increasing demand not only corresponds to the number of new reactors coming onstream but also policies echoing out of Europe regarding extending the life of existing reactor fleets. You’re seeing a number of different avenues in which nearer-term demand could increase, which only adds to the longer-term demand of new reactors. There are incremental policy changes toward nuclear power, too, certainly across Europe and coming across through North America. Obviously it’s happening in Asia, with China and South Korea furnishing fairly large reactor-unit increases for their countries.

TER: Some of the most promising uranium projects are in Australia. Although the country is considering a new tax on miners, the Mineral Resources Rent Tax (MRRT), a recent change in leadership in the governing party could be a favorable development. Could you update us on the political climate in Australia as it pertains to the uranium players there?

GM: Well, Australia is interesting. It has the world’s largest accumulated known uranium resources and the largest uranium deposit—Olympic Dam. At the moment, Australia’s federal government allows uranium mining, and other regulations basically filter down state by state. Western Australia is now open to uranium mining. South Australia has an active uranium mining history, as does the Northern Territory. The more recent super-tax proposal, which the Labour Party put forward, created an uncertainty in terms of the value of both current and future mining projects. Julia Gillard, the new Prime Minister, has made motions toward the industry in terms of coming forward and talking about possible modifications to the mining taxation rules. For the time being, it’s hard telling how ultimately this will break down.

TER: Your research talks about some sector outperformers among the conventional explorers. You’ve mentioned Energy Fuels Inc. (TSX:EFR), Mega Uranium Ltd. (TSX:MGA) and Strateco Resources Inc. (TSX.V:RSC). Please update us on those companies.

GM: They provide investors with exposure to uranium in different jurisdictions. For example, Mega has the Lake Maitland project in Western Australia, which is opening up for uranium mining and where a significant proportion of Mega’s assets are located. The company has good partners in a Japanese consortium, which owns about 35% of the asset at Lake Maitland. Mega provides people with exposure to a near-term uranium producer that has a significant support base in terms of these partners. I think that’s one of the more favorable new projects in Australia. We anticipate production maybe in 2013. It would be a lower-cost producer, probably in the high $20s in terms of USD per pound of production.

TER: How much would Mega produce annually at Lake Maitland?

GM: We’re looking at about 1.65 million pounds; it’s small-scale production. It’s basically a thin layer at surface that doesn’t require conventional mining. It’s unconsolidated mud effectively, so 1.65 million pounds a year for the life of the project.

TER: Does Mega have any other projects in Australia?

GM: Lake Maitland is their primary project. Their second main asset in Australia is Ben Lomond, up in far northern Queensland, just outside the city of Townsville. It’s a modest-grade deposit; it’s got potential. They’ve got a bunch of other exploration plays around the world, particularly in Canada.

TER: What’s your target price on Mega?

GM: $0.80.

TER: Before we go further, could you give us an overview of cash costs—low, medium and high—in terms of uranium production?

GM: Sure. Certainly low cash costs now would be below around $25 a pound. Medium would be upper $20s and $30s. High costs are $40s and above.

TER: Okay. What can you tell us about Strateco?

GM: Matoush is a very nice deposit in Québec; very handsome grades, close to 0.6% U3O8. It has a resource of about 20 million pounds of uranium U3O8—small, but higher grade. Our interpretation is that Matoush is the most advanced project for a development-stage company in Canada. Strateco has a big program going at the moment —another 60,000 meters of drilling this year to look for extensions of mineralization, and another 60,000 meters planned for 2011. The orebody is still open. Guy Hébert, the president and CEO, is also working out permitting. We’re looking at permits for the project to start underground development for bulk sampling.

TER: How long would it take for them to get the assay results from that bulk sample?

GM: We’re looking at a couple of years, probably 2012. They have to develop the underground workings first. The main thing in the interim is the underground development itself, and also the exploration drilling they’re doing. It takes time. That’s why we think Strateco is ahead of its peers in terms of submitting proposals to the Canadian Nuclear Safety Commission (CNSC) for licensing and permitting approval. Canada is highly regulated, which is a good thing. It’s mandated, and these things take time.

TER: Alright, what about the others?

GM: Energy Fuels, that’s a uranium-, vanadium-oriented company in Utah and western Colorado. We like them because of the duality of the commodities. In addition to uranium, they have the vanadium, which is an integral component in steel manufacturing. That gives them a bit of a boost. Energy Fuels would be a moderate to higher-cost producer and shares many similarities with Denison Mines Corp. (TSX:DML; NYSE.A:DNN) and its mining and processing operations in the United States.

TER: What are some of their assets?

GM: They have the Piñon Ridge Mill project, permits for which are under review. That process should be complete by early next year. They have a couple of mines that are fully permitted and will be underground mining on the Colorado Plateau. Energy Fuels has the potential to go into production at their Whirlwind Mine, but they don’t have a mill there yet.

TER: A recent edition of Haywood Securities’ Uranium Weekly gives sector outperform ratings to Paladin Energy Ltd. (ASX:PDN; TSX:PDN) and Denison. What upsides do you see there?

GM: I favor Paladin simply because they have two conventional open-pit mines in Africa where they’re ramping up production. There’s one in Namibia, which is the world’s fourth largest uranium-producing country. The new mine that they commissioned last year in Malawi is Kayelekera. Paladin’s a conventional player with production costs of around $30 a pound; it’s a Tier-2 producer at the moment and is looking to expand from there. The company also has development plans in Australia and elsewhere in Africa. They’ve done quite well—they’ve proven themselves to be the new player in terms of conventional mining and milling in the uranium sector.

TER: Are they approaching Cameco Corp. (NYSE:CCJ; TSX:CCO) status?

GM: No, not yet. Cameco is fairly substantial, quite diverse; but Paladin is a Tier 2. There are not many Tier 2 producers out there; they include Uranium One Inc. (TSX:UUU), Paladin and Denison in that fold.

TER: Tell us about Denison.

GM: Denison is basically a North American uranium producer and also produces vanadium from its Utah operations. It’s a higher-cost producer, and certainly the leveraged play in the space. Denison has basically reconstituted itself over the last year and a half in terms of raising equity to minimize long-term debt. They’ve also brought in KEPCO as a partner—Korea Electric Power Company (NYSE:KEP). Basically, Denison is slowly ramping up its production in the U.S. They’ve cut down a few of the higher-cost producing mines to be more prudent in their mining and producing operations. For example, they have a partnership with AREVA (PAR:CEI) at the McClean Lake facility in Canada, which is probably going on care and maintenance in July.

TER: Why is that?

GM: AREVA operates that, so it’s largely their decision. . .probably looking toward future prices to see when it comes back onstream. Denison also produces vanadium, and they have a very exciting discovery in the Athabasca Basin—the Phoenix Zone in the Wheeler River joint venture. Phoenix has had some outstanding drill results over the last year. They’re aiming to get a resource estimate out on that by the end of 2010. Quite an exceptional discovery, I think.

TER: In that same issue of Uranium Weekly, you talk about some in-situ miners. Among your sector outperformers are Uranium Energy Corp. (NYSE.A:UEC), Ur-Energy (NYSE:URG; TSX:URE) and Uranerz Energy Corporation (TSX:URZ; NYSE.A:URZ). Tell us about those.

GM: Uranium Energy, Ur-Energy and Uranerz are all in the U.S., all looking at in-situ uranium recovery—so no physical mining, all sandstone-hosted. We see near-term production out of all three of the companies. That’s this year for Uranium Energy, probably next year for Ur-Energy and late 2011, early 2012 for Uranerz.

TER: This year for Uranium Energy?

GM: Yes. We’re looking at Uranium Energy entering production in October from their Hobson plant and mining from their well fields at Palangana—both in Texas; so, with this timeline, it will effectively be the world’s next uranium producing company. It’s quite an exciting development for the space and the company. They have another project, Goliad, which could potentially add to their production and should get its final permitting by the end of this year. We like Uranium Energy’s lower-cost production base. They’re not large but their cash costs are probably around $22, so quite good there. Production scale potentially 1M–2M pounds annually.

TER: Has the share price moved in anticipation of production?

GM: No, not as yet.

TER: Given that its pending production profile hasn’t been taken into account, might it be a good buying opportunity?

GM: We certainly like them. Our target there is $3.90. They’re trading at around $2.40, so we think that offers a good opportunity. They have a number of catalysts going forward and a big exploration plan around their existing resources. They will update their resource estimate in September; production in October. We’re looking at getting a second well field project ‘Goliad’ permitted by the end of the year. A third project called, Seager-Salvo, could have an initial resource estimate by year-end, as well.

TER: What about Ur-Energy?

GM: Ur-Energy and Uranerz are good peer companies. They’re both in Wyoming, and both submitted applications to go into mining around the end of 2007, beginning of 2008. We’re looking at production next year for Ur-Energy and early 2012 for Uranerz. Let’s go through Ur-Energy. They’ve got a very good cash position and have the Lost Creek and Lost Soldier deposits. They’ve been operating from Lost Creek first—they’re looking at development there. We’re looking at the Nuclear Regulatory Commission (NRC) ultimately providing final permits and licenses to go into production in the second half of this year. It’s the same for Uranerz. We’re looking at probably starting to build at the end of this year, beginning of next year. Lower-cost producer, small scale.

TER: Let’s go back to what’s happening in Africa. Haywood’s research would seem to agree that Africa has a number of promising uranium explorers and developers. Could you talk about some of the juniors Haywood thinks are poised for significant share appreciation?

GM: Africa is blossoming as a region for uranium discovery. Mantra Resources Ltd. (TSX:MRL; ASX:MRU) and Extract Resources Ltd. (TSX:EXT; ASX:EXT) have made some genuine new discoveries there over the last year or two. I think the best thing about Africa is the probability of making discoveries that are more easily exploitable in terms of being at or near surface, so they’re amenable to open-pit mining. Mantra has an exceptional deposit, the Mkuju River Project in Tanzania. I think the company published its first resource estimate at the beginning of last year. . .more than doubled it within a year and still has the potential to increase that resource. They’re looking at production in the second half of 2012. That’s a very quick timeline to production. They’re still looking at increasing the capacity from their plant and milling operation. We’re looking at a modest cash cost of about $25 a pound. Mantra has a lot of positives going forward.

Extract made an outstanding discovery at Rossing South in Namibia. This is 6 km. south of the existing Rossing Mine that Rio Tinto Ltd. (LSE:RIO; NYSE:TP; ASX:RIO) operates. They have close to 300 million pounds of defined resources, which they identified in rapid time. Their resources are significantly higher grade than the existing Rossing operation and they’re looking at expanding on that. It’s a world-class discovery, a fact that their share price has reflected over the last 18 months.

TER: That’s great. Any others?

GM: Bannerman Resources Ltd. (TSX:BAN; ASX:BMN) has done a lot of work in terms of defining the Etango deposit, which has about 160+ million pounds of uranium. It’s tens of kilometers away from Extract’s Rossing South. They’re all very close together, and all alaskite-hosted. That means the mining and processing techniques are well known and understood given the long history of mining at the Rossing Mine.

The Etango deposit is defined over 6 km. of strike length. It crops out—it’s at surface and shallow. Bannerman doesn’t have the grade that Extract has, so they’re a more leveraged play in the space; but we still like Bannerman in terms of a large strategic resource. We’re looking at cost of production in the high $30s or maybe $40 a pound.

The big thing there is that they should get their ultimate mining license over the next few months, so they’ll be one of only three operations to have licenses to go into production. The big players are looking for resources with potential for large-scale production in areas that allow uranium mining. And that’s where Bannerman, Extract and Mantra all come out quite well.

TER: Thank you, Geordie, for updating us on all of these exciting developments.

Dr. Geordie Mark, a research analyst with Haywood Securities, focuses principally on uranium companies involved in exploration, development and production. He joined Haywood Securities from the junior exploration sector, where he was vice president of exploration for Cash Minerals, which concentrated on uranium and iron oxide-copper-gold targets across Canada. Immediately prior to joining the exploration industry full-time, Dr. Mark lectured in economic geology at Monash University, Australia and served as an industry consultant. He completed his Ph.D. in geology in 1998 at James Cook University’s Economic Geology Research Unit in Australia, specializing in aqueous geochemistry and igneous petrology applied to ore-forming systems.

Want to read more exclusive Energy Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Expert Insights page.

In Search of a Good Basin

By Dave Forest – Pierce Points July 20, 2010

Yesterday, we went through the basics of unconformity-hosted uranium deposits. And why these are the big prize for the uranium industry.

And yet, despite decades of study, we’ve still only found unconformity-type mineralization in a handful of basins worldwide. Athabasca, Thelon, Kombolgie, Kintyre, Hornby Bay, Otish, Karku.

This is largely a function of exploration. There is no shortage of potential targets. Uranium gurus Kurt Kyser and Michel Cuney note in a recent paper there are over 200 sedimentary basins globally that fit the general bill for unconformity mineralization. That being (as we discussed yesterday), the presence of old Archean rocks overlain by younger Proterozoic rocks.

Something happened around the Archean/Proterozoic transition. Almost certainly related to the first appearance of large amounts of oxygen in Earth’s atmosphere.

The formation of uranium deposits is controlled by “oxidation state” (generally, the presence or absence of oxygen) to a much greater degree than other metals. And Archean/Proterozoic basins appear to have been the setting where oxidation conditions were optimal for the formation of large, high-grade uranium deposits.

But it’s highly unlikely that all 200 of the world’s Proterozoic basins will be significantly mineralized. We know that a number of special geological and geochemical conditions blessed places like Athabasca. Playing a critical role in uranium ore formation.

The trick to finding the next major uranium discovery is to survey the world’s basins. And figure out which ones might also have these special ore-enhancing features.

Here’s a checklist of things to look for in a good basin.

1) Uranium source. As we discussed yesterday, unconformity deposits form when older uranium is dissolved in oxygen-rich waters, concentrated, and then re-deposited. This means a basin must have an identifiable source of old uranium.

There’s debate in uranium circles about sources for unconformity mineralization. Some workers believe U is sourced from granites in the Archean rocks that underlie Proterozoic basins. Some believe the overlying sediments are the source, with uranium coming from minerals like zircon and monazite. It’s also possible both these sources come into play.

…..read pages 2-3 of The Scoop…. on the Next Big Uranium Discovery

As stocks have slipped lower over the last three months, copper has bucked the broad trend and broken the pattern of lower highs and lower lows it set in the spring.

After bottoming on June 7, the iPath Dow Jones-UBS Copper Subindex Total Return ETN – which closely tracks copper futures – has gained more than 12.2%. In the same span, the Russell 2000 small cap stock index has lost 0.6%.

The red metal is nicknamed Dr. Copper for its ability to peer around the corner and act as a leading indicator for the global economy. And right now, the commodity with a Ph.D. in economics seems to be saying the future looks bright. Is the trend set to continue?

On a technical basis, looking just at price, analysts at Standard Chartered Bank believe copper will continue to move higher. They point to the formation of an “inverse head-and-shoulders” pattern. This pattern reflects the psychology of traders: The rebound from the initial low is quickly reversed, sending sentiment into a tailspin. The retouch of the “neckline” encourages short sellers to press their luck, but buyers are found lying in wait.

A break up and out of the pattern is a very positive signal that the selling pressure has been exhausted, clearing the way for bargain hunters to send prices skyward. Analysts at Merrill Lynch are looking for copper prices to increase another 18% through 2011 as the economic recovery rolls on.

Fundamentally, copper still faces tightening supply and growing demand. Credit Suisse Group AG (NYSE ADR: CS) analysts have reinforced their view that copper is their top base metal pick with “falling ore quality grades and tight supplies causing long-term prices to rise again.”

After looking at the rate of copper imports into China, it looks like the Chinese are drawing down their stockpiles of the metal – a sign that demand from the Middle Kingdom is set to rise as these inventories are replenished.

Copper’ s relative strength is a sign that some positive sentiment is creeping back into the psyche of global traders. Mining stocks will benefit from its advance, and so will the iShares MSCI Chile Investable Market Index fund (NYSE: ECH), as copper mining makes up a large part of the Chilean economy. ECH hit an all-time high last week.

[Editor’s Note: Money Morning Contributing Writer Jon D. Markman has a unique view of both the world economy and the global financial markets. With uncertainty the watchword and volatility the norm in today’s markets, low-risk/high-profit investments will be tougher than ever to find.

It will take a seasoned guide to uncover those opportunities.

Markman is that guide.

In the face of what’s been the toughest market for investors since the Great Depression, it’s time to sweep away the uncertainty and eradicate the worry. That’s why investors subscribe to Markman’s Strategic Advantage newsletter

Subscribe to Strategic Advantage and hire Markman to be your guide. For more information, please click here.] every week: He can see opportunity when other investors are blinded by worry.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair