Uncategorized

Feb. 15 (Bloomberg) — The Democratic Republic of Congo’s government should “respect its commitments” concerning Freeport McMoRan Copper & Gold Inc.’s $1.8 billion Tenke copper and cobalt project, according to a parliamentary report.

The Tenke project is the last question mark after a two- and-a-half year government review of all Congo’s mining contracts. The main point of contention between the two sides was over state-owned Gecamines’ stake, which was reduced from 45 to 17.5 percent in 2005.

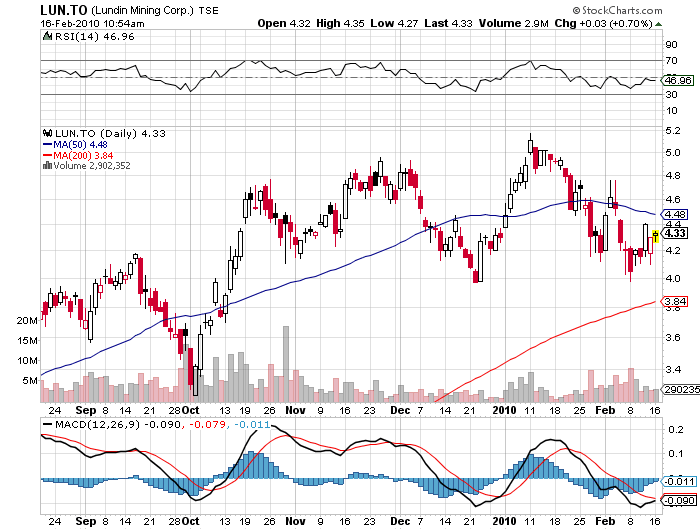

Though the renegotiation was legal, the contract was “badly negotiated” by the government, the commission said. Tenke is now 57.75 per cent controlled by Freeport. Canada’s Lundin Mining Corp. has a 24.75 per cent share.

The Tenke mine, which opened in March 2009, is currently producing 250 million pounds (113.4 million kilograms) of copper and 18 million pounds of cobalt a year. Its second phase of investment will allow it to produce 400,000 metric tons of the metals, according to the report. Cash-strapped Congo could receive as much as $50 million in payments from the project this year, the commission said.

Bemba Arrested

The 2005 reduction of Gecamines’ stake was negotiated by then-vice president in charge of mines, Jean Pierre Bemba. Bemba was arrested in 2008 and is awaiting trial at the International Criminal Court for leading militias that raped and murdered civilians in the Central African Republic in 2002 and 2003.

The commission’s report was spearheaded by Modeste Bahati Lukwebo, a deputy in the National Assembly, and was sent to the government in late January.

Congo produces about half the world’s cobalt, a metal used in jet engines and rechargeable batteries, and holds 4 percent of global copper reserves.

My view has been that the key macro trend is one where China will gradually become a major, self-sufficient global economic power whose development of a middle class will nourish the OECD sunset economies as the Chinese standard of living catches up to that of OCED members. In the even longer run as China begins to grapple with its own demographic problem India with its youthful demographics will pick up the slack and become the driver of global economic growth. In a globalized economy where significant imbalances in living standards between relatively large and smaller population bases exist, and where capital is free to seek out the place with the lowest cost structure, mobilize local resources, and transport goods and services into regions with higher cost structures, the OECD has a 20-30 year window during which its objective should be to prevent the crash of its own living standard and sustain itself on the rising living standard of the have-nots. If the United States has any rival outside of China it has to be Europe and not Japan. During the past few weeks China has been put off balance by stories such as Google’s threatened withdrawal due to Internet censorship, a US decision to ship $6.4 billion in weapons to Taiwan, and an escalation of public anxiety about Iran’s nuclear ambitions which has isolated China as the sole nation unwilling to sacrifice its security of supply interests for a common good.

China, in turn, has retaliated by tightening its banks’ lending requirements in a move ostensibly designed to cool internal inflation, but which is also intended as a warning to the OECD that in so far that it hopes to pull itself out of recession on the coattails of China, it should perhaps not count too heavily on a China portrayed as “Big Bad China”. With China checking out for a little siesta it is a good time for the United States to deal with Europe through its proxies, the transnational mercenaries which have no geopolitical allegiance but do owe some gratitude to the Obama administration for not playing hardball during the 2008 meltdown. The relevant question for the medium term future is, who suffers less as China rises, the United States or Europe? The trouble with this question is that it posits a false dichotomy, for nationalism is a sop for the saps who cast their votes for politicians already bought and paid for by interests who are neither Europeans, Brits nor Americans. The proper question should be how is the disparity between the standard of living of population bases whose economies are de-industrializing and those which are industrializing to be managed so as to avoid chaotic eruptions of the pitchfork or “sieg heil” variety? This risk is for the moment acute because the United States and Europe are both in a state of denial about the course history is taking, which is that the significantly larger Asian population bases will drive the world’s economic future, and in doing so determine the power landscape of the future.

Gold is bound to be a natural beneficiary of this transition period because we cannot predict the political structure of this future, and gold is the ideal long term hedge against this uncertainty. That is why I believe we have entered a period of real increases in the price of gold which may not be very dramatic in nominal terms for speculators hoping to profit from higher prices (oddly, they unanimously seem determined to calculate those profits in dollars!), but which real gains have a profound leveraged impact on the value of resource juniors with ounces in the ground that can be developed as mines. But more importantly, this “optimistic” view in which the world’s average standard of living grows at an accelerated pace implies a steady growth in total demand for all raw materials, with particularly high growth for those raw materials which play critical and incremental roles in new technologies. This puts me into the secular bull camp for raw materials where Eric Sprott used to belong, but from which he has distanced himself after committing the sin of wishing this trend to accelerate faster than it could. During the past year I have spent an increasing amount of time on “minor metals”, that oddball group of metals often referred to as “strategic”, “critical”, “specialty” and ever more frequently as “technology” or “rare metals”. The specific group on which I focused last year was the “rare earth” metals, a group of metals in whose supply China completely dominates and which have a broad set of properties which have helped them become key inputs for many new technologies, including those related to “clean” or “renewable” energy.

Kaiser Bottom-Fish Online is a fee based research portal owned and operated by John Kaiser from his base in Moraga, a suburb in the San Francisco area of California. It specializes in high risk Canadian listed securities and seeks to provide investors with a framework for intelligent speculation. The resource sector is the primary focus for an investment approach developed by Mr. Kaiser which combines his “bottom-fishing strategy” with his “rational speculation model”. A full membership costs $800 annually or $250 quarterly. It provides access to online information resources, commentaries and recomendations.

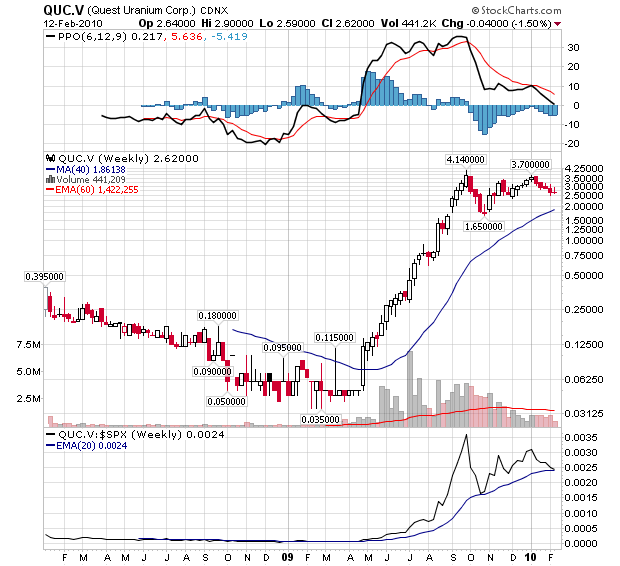

Quest Uranium Corp was created as a spinoff from Freewest Resources Canada Inc to hold the uranium exploration assets Freewest had staked in eastern Canada, including the Strange Lake in Quebec. Freewest shareholders received 1 Quest for 25 Freewest and the opportunity to participate in a rights offering before Quest started trading on Jan 11, 2008. The Strange Lake group, which includes the Quebec portion of the 52 million tonne Strange Lake rare earth deposit discovered by IOC during the eighties, became the company focus in April 2009 when a new target yielded high grade rare earth numbers with a distribution similar to Strange Lake and the junior decided to re-assess Strange Lake and the surrounding area in light of a high distribution of heavy rare earth elements. Sampling and drilling during the summer of 2009 led to the discovery of the BZone, a large near-surface deposit on the Quebec side which appears to be similar to the Main Zone. Metallurgical studies and 43-101 resource estimates are planned before Quest resumes work in Q2 of 2010 to delineate the higher grade pegmatite layers.

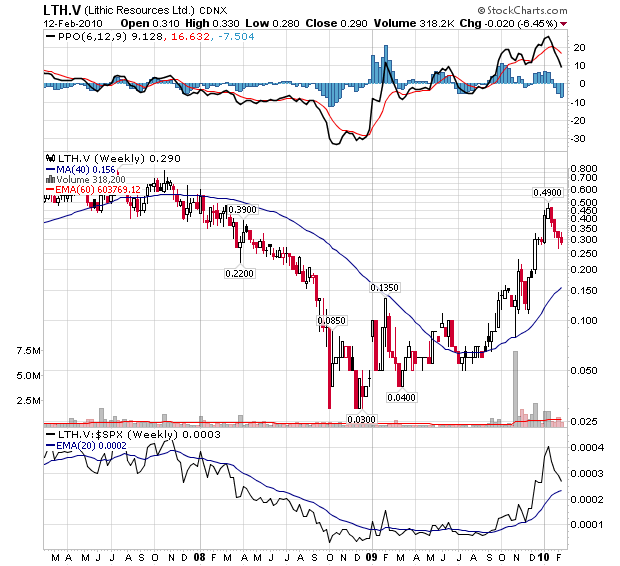

Lithic Resources Ltd is headed by Chris Staargaard who ended up completely in charge in late October 2009 when RCF sold its control to an investor group. The flagship project is the Crypto carbonate replacement zinc deposit in Utah where a 43-101 resource estimate in November 2009 confirmed the presence of a 2.5 billion lb zinc resource with significant copper and indium credits. The smaller oxide portion is amenable to open pit mining, while the richer and larger sulphide resource, which has higher indium grades, will require underground mining. For 2010 Lithic is planning a scoping study and a new round of drilling with an estimated US $6-8 million cost whose purpose will be to collect additional material from the main CRypto zone for metallurgical studies, test the eastern strike extension for addtional zinc-indium skarn mineralization, test the high grade silver potential beneath the old Utah silver mine workings, establish the nature of the high grade moly mineralization previously encountered beneath the main skarn zone, and set the stage for a $20 million plus feasibility study in 2011 which will require an underground drilling program so that an optimized mining plan can be developed which targets high grade zinc-indium ore early in order to achieve rapid payback.

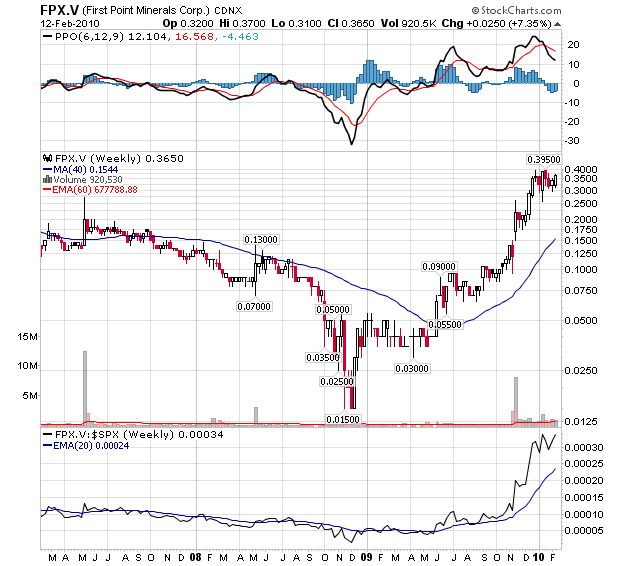

First Point, led by President and CEO Peter Bradshaw, is focused on the Americas where it has both base and precious metals projects in Canada, the United States, and Mexico. First Point’s primary focus is on two nickel projects, Decar in British Columbia and Joe in Oregon, that host disseminated nickel-iron alloy mineralization in intensely altered ultramafic rocks. These properties represent large scale targets in the order of 300 million tonnes plus of open pittable sulpher-free nickel mineralization than could potentially be sent directly to steel mills after magnetic and gravity based concentration without smelting and refining, with obvious potential economic implications relative to sulphide nickel projects. On November 13, 2009 First Point announced it had optioned its flagship Decar project to a subsidary Cliffs Natural Resources where Cliffs can earn up to 70% by taking the project through to a bankable feasibility study. As part of the deal Cliffs is purchasing a 19.9% equity stake in First Point, which will use the funds to mount a global search for additional ultramafic bodies with a significant nickel-iron alloy content using a proprietory geochemical testing method developed by Bradshaw’s team during the past couple years.

Kaiser Bottom-Fish Online is a fee based research portal owned and operated by John Kaiser from his base in Moraga, a suburb in the San Francisco area of California. It specializes in high risk Canadian listed securities and seeks to provide investors with a framework for intelligent speculation. The resource sector is the primary focus for an investment approach developed by Mr. Kaiser which combines his “bottom-fishing strategy” with his “rational speculation model”. A full membership costs $800 annually or $250 quarterly. It provides access to online information resources, commentaries and recomendations.

John Kaiser was born and raised in Vancouver, Canada. He graduated from the University of British Columbia in 1982 with a BA in philosophy and German. He began work in January 1983 as a research assistant with Continental Carlisle Douglas, a Vancouver brokerage firm that specialized in Vancouver Stock Exchange listed securities. In 1989 he moved to Pacific International Securities Inc where he was research director until April 1994 when he moved to the United States with his family. From 1989 until 1994 he was also a registered investment advisor. He worked six months as a researcher for Bob Bishop’s Gold Mining Stock Report before branching out on his own with the publication of the first issue of the Kaiser Bottom-Fishing Report in October 1994. He has written extensively about speculative Canadian issues, is frequently quoted by the media, and is a regular speaker at investment conferences. He specializes in high risk speculative Canadian securities with an emphasis on the resource sector. He is one of the few independent analysts with an in-depth knowledge of diamond exploration.

India is reportedly to follow China’s lead in using government entities to tie up strategic mineral supplies from around the world to help enable it to maintain economic growth.

Some say that the British invented bureaucracy and the Indians perfected it! Certainly dealings with Indian government departments seem to take forever amidst mounds of paperwork.

But now the Indian government recognises that its usually slow movement in completing deals potentially sets it at a disadvantage to countries like China where state organisations have learnt to move quickly and decisively. This has been seen particularly in tieing up access to global mineral resources which the China sees as vital for the years ahead with its rapidly growing internal development.

India is a country which faces many of the same problems as China, but is a few years behind in terms of internal growth but, like China, its GDP is growing at an enormous rate in comparison with the West, where economies are, at best, static for the moment. To fuel this growth India too needs access to major mineral resources – metals, minerals, oil and gas – but has been much slower than China in doing the deals which can guarantee future supplies in a competitive environment, and at a time when there are doubts about the medium to long term availability of many strategically important metals and minerals.

Thus the Indian government is reportedly moving to fast track deals to secure future supplies for its ever-growing industrial base. According to a report in today’s Hindustan Times The Prime Minister’s Office (PMO) has decided that the country’s state-owned corporations need to be supported in aggressively pursuing the acquisition of strategic mineral resources through a dedicated fund – and it has set a 30-day deadline for such plans to be in place. According to Hindustan Times, an unnamed senior government official told it “The PMO has asked the Finance Ministry and the Planning Commission to work out the size and structure of the dedicated fund in 30 days.”

One of the key elements in the proposal too, is that the country’s normally slow procedures will be circumvented by setting up the centralised body with rapid strategic and decision making powers.

The Indian government seems to be taking China’s CIC as its model and is very conscious the Chinese fund is using a significant part of its US$200 billion of government money to acquire stakes in natural resources overseas. Oil and gas has been the prime target, but metals and minerals, have also figured high on the list among other strategic investments. Whether it will follow CIC’s example in investing also in U.S. property and stocks including in the SPDR Gold Trust gold ETF is uncertain, although gold might be of interest given the country’s populace’s propensity to own the yellow metal. Certainly India has already followed China’s lead in this respect with even the state-run Post Office and state-owned banks selling gold bars and coins to the people.

The significance of the Indian move should not be underestimated. Indian growth is currently matching that of China and with the two Asian potential megapowers with enormous populations taking ever increasing volumes of raw materials from the global supply, the pressure on resources can only increase dramatically.

According to the report, India is also beginning to try and use diplomatic pressures to help secure supplies with the External Affairs Ministry tasked with a strategy to help acquire them, particularly in Africa which is seen as key area of potential supply with resources frequently directly controlled by government.

Via MineWeb. Go HERE to subscribe to their NewsLetter

It’s a small chunk of land, about half the size of Rhode Island, located in a part of the world most people know nothing about.

The heads of Toyota, Honda, and the Pentagon all share a common interest.

But they’re not the only ones watching. Venture capitalists, hedge fund managers, and resource companies from all over the globe are also watching and waiting. . . ready to pour billions into Greenland once they get the green light.

Why?

This coming January, when the Kingdom of Denmark relinquishes sovereign control over Greenland’s natural resources, the world’s biggest deposit of Rare Earth Metals (or REEs), will fall into private hands. . . for the first time ever.

This single site boasts deposits valued at an estimated $1.3 trillion. . . and yet, REEs are worth more than just money.

Which is why the world’s leading manufacturers of hybrid cars, wind turbines, batteries, and yes — even the guidance systems to our most sophisticated air and ground defense missiles systems, are watching the events in Greenland unfold with baited breath.

The elements that fall into the category of Rare Earths include:

- Lanthanum – essential in the production of electric car batteries;

- Terbium – without this element, high-strength magnets would not exist;

- Erbium – makes possible a wide range of light-weight, high-strength metal alloys;

- Thulium – makes high-frequency lasers a reality.

- And once Greenland takes control of its mineral wealth, this land — totaling barely 800 square miles — is projected to supply 25% of the world’s entire REE market. . . for half a century.

To companies like Toyota and Honda, that have virtually staked their futures on the rapidly expanding hybrid/plug-in car market, and to our own defense industry, which cannot perform even the simplest task without highly-involved electronic assistance, this news could not have come at a better time.

Because for the last decade and a half, our greatest and most populous modern rival has been hard at work to corner the market on these vital elements.

And on April 17 of this year, with the signing of a single contract, the Chinese reached a record 96.7% global market share.

China’s “Dragon Metals”

That’s why we’ve dubbed these commodities “Dragon Metals,” because China literally owns that market.

This is the kind of monopoly that has caused emergency Congressional meetings in the past. . .

Meetings that have ended in government-mandated intervention.

But there is nothing Congress can do to stop the Chinese government from closing its global stranglehold on materials without which the modern world cannot function.

It’s part of a plan that Deng Xioping claimed almost two decades ago would: “Do for China what oil did for Saudi Arabia.”

Evidently, the People’s Republic is wasting no time in putting this advantage to strategic use.

Plans to limit exports and systematically inflate prices have already trickled down from the party leaders, and progressive decline in production has been standard operating procedure for the past several years.

According to Wired Magazine, “China’s Ministry of Industry is weighing a total ban on exports of terbium, dysprosium, yttrium, thulium, and lutetium — and may restrict foreign sales of other rare earth metals.”

This news is a potential death knell for hybrid manufacturers that have forecast 500% growth in the next 6 years alone. . . alongside a wide spectrum of other cleantech companies whose products depend on magnets, motors, and batteries to create and store energy.

Not to mention a political and economic nightmare for our Department of Defense. . .

However, as Greenland prepares to open its resources to the open market, this Chinese monopoly has finally met a foe it cannot easily topple.

Come January, a single company will control this massive deposit, turning it into the world’s second biggest single producer of REEs.

With a stock price just under 60 cents today, this company has already gained close to 30% since the start of September. . .

But the big spike is still just around the corner, with a vast majority of the gains still in the future.

In the next few weeks, we’ll be publishing specific approaches to squeezing the most mileage out of this historic stock, as well as more information on an approaching commodities boom that may be the biggest we’ve seen in decades.

Profitably yours,

Brian

P.S. Rare Earth Metals and other commodities vital to the developing electric car and battery markets and Uncle Sam’s own defense industry should be on every investor’s radar. And as current energy prices continue to rise, we find ourselves in the early stages of the greatest commodities bull market in history. . .

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair