Stocks & Equities

“Instead of looking for opportunities to invest in real products, Wall Street awaits the minutes of each Federal Open Market Committee meeting with bated breath, hoping that QE3 and QE4 are just around the corner.”

– Ron Paul

There have been bouts of risk aversion over the last few years – some sustained, most not; but all unquestionably due.

We understand that the final arbiter is price, regardless of what the fundamentals suggest about an investment or underlying economy. But it’s hard to maintain such necessary agnosticism when the news is so consistently bad.

And therein lays the problem – consistency.

One might instead use the term “mindless recitation,” but the steady — consistent — dose of ‘bad’ has rarely spooked investors (those still playing, anyway). Sure, a confluence of ‘bad’ has served to ruffle feathers periodically, but, ultimately, the markets continue chugging along because we always know ‘just how bad’ or ‘just how good.’ For as long as everyone knows what’s going on, the cause for worry is diminished. Why? Because investors rationalize their above average, selective stock-picking ability and fabricate a false sense of security (trading bias) which, in a self-reinforcing sort of way, creates the apparent absence of uncertainty.

Bringing the black swan concept into this, analysts have sought to uncover potential risks that would bring on massive shocks to the markets; it’s become a well-tred path to popularity and influence in the investment world since 2008. But, by definition, predicting a black swan event is impossible.

As we move further and further away from the credit crisis of 2008, and as we are further desensitized to the words ‘bad’ and ‘worse’ by government and central bank officials’ action, investors seek out risky investments because they have not found a black swan (and, because of the low interest rate background, nothing else pays.)

To Read More CLICK HERE

Dear Readers,

We are just back from the Recovery Reality Check Summit, which was very informative as well as thought-provoking. We took some time while there to chat with a few of our speakers after their presentations and will be sharing them here over the next few weeks.

Our first conversation is with Rick Rule, the legendary resource speculator. He gives us a powerful primer on being a contrarian speculator, which may help bolster some discipline in the current market climate. We hope you enjoy this presentation.

Sincerely,

Louis James, Senior Metals Investment Strategist

Casey Research

[Rick was one of 31 esteemed financial experts featured at the Casey Research Recovery Reality Check Summit, where attendees heard three days’ worth of illuminating takes on the economy, spirited debate over where it’s headed, and a wealth of actionable investment advice. Even if you couldn’t make it, you can still hear every recorded session with our soon-to-be released Summit Audio Collection.]

(Interviewed by Louis James, Editor, Casey International Speculator)

Louis James: Ladies and gentlemen, welcome. Thank you very much for tuning in. We are at the Casey Research Summit – the reality check on the recovery of the economy. One of our luminary speakers who is always at our events, Rick Rule, is with us here now. We’d like you to give us the quick tour of your talk today and we’ll go from there.

Rick Rule: Sure. My role here wasn’t to do economics; that’s not what I am. I am a speculator, and so I talked about where we are in the context of where people are with their own portfolios – in particular portfolios that are junior-resource centric – which is what I think most of your audience was interested in.

Louis: Right.

Rick: And my point was that there were some good forces in the market: lots of cash on the sidelines; some good work being done; and basically a good market for resources as a consequence both of population growth and demographic growth at the bottom of the economic pyramid, and in terms of historical supply constraints. And there were some bad factors in the market: excessive debt in the system; way too much government interference; very large social takes on a global basis, beginning to impact extractive industries. And there were some truly ugly factors – the ugly factors in particular being poor corporate as opposed to share market performance, and the unfortunate truth that probably 80% of the junior resource stocks on a global basis are valueless. So the sector itself is in perma-decline. Although the performance – as you know from being affiliated with Casey – of the top 10% of the sector can be extraordinary. It often serves merely to focus attention on the worst companies in the sector. And then I went on to say: “This is the set of circumstances that exists, now what can we do with this?”

The fact that the market has fallen, by some estimates, by half suggests by other estimates that the market is approximately half as risky as it used to be. Price has taken care of some of the risk that existed in the market before.

The second factor that we need to take into account on a going-forward basis is the fact that the industry itself didn’t finance as aggressively last year as they did the year before, but although they didn’t raise new capital, they didn’t stop spending. I call this financial roulette. The issuers are engaged in this rather circular exercise, which is very risky: They’re spending money to attempt to get results, to generate excitement, to raise their share price, to raise money. So they’re spending money to raise money, which is a very, very risky strategy.

Most of the issuers will need to come back to market this year, and they’re coming into a market that’s in total disarray. The buyers that existed for the last 10 years – the small hedge funds and the open-ended hedge funds – are facing massive redemptions as we speak, so rather than being a source of new capital, they’re a source of the selling that you see weighing down the market. We are going to have to, as investors, invest with a view to a different buyer on a going-forward basis, and the companies who are issuing equity are going to have to find a different class of buyer for the new financing. So we’re in a time of real change and real turmoil – and hence a time of real opportunity.

My suspicion is that with so many issuers having to access the market and so few market participants that have the capability of differentiating between good and bad issuers, that just as the bad issuers were swept up with the good issuers in 2010, the good issuers are being swept out with the bad issuers in 2012. It’s my supposition that for investors who are willing to work hard, take advice, and segregate viciously in terms of allocation of capital, that this will be the best private-placement investment period that we have enjoyed since 2002.

To Read More or Watch the Video CLICK HERE

What I like most about Gary Shilling’s economic analysis is that it’s thorough. In the piece that follows – an excerpt from Gary’s monthly INSIGHT – he ranges from the importance of US consumer spending and the unemployment rate, to the actions of the Fed, to business cost cutting and productivity, to the housing crisis and household debt, to state and local government fiscal issues, to US exports – Etc.! So by time he gets ready to deliver conclusions, you know they’re well-supported. And Gary’s overall conclusion here, regarding the rest of 2012, is a strong one and maybe not quite what you’d expect.

As part of the deal with Gary to send you his material, he has asked me to offer you the chance to subscribe to his letter. If you like his work as much as I do, I suggest you consider it. Outside the Box readers can subscribe to INSIGHT for the special rate of $275, and you’ll receive 13 reports instead of the normal 12, plus a free 10-page Special Report outlining Gary Shilling’s investment strategies for 2012. (This offer is available to NEW subscribers only.) To subscribe, call them at 1-888-346-7444 or 973-467-0070, and be sure to mention Outside the Box to receive your special rate and free report.

Your home at last but not for long analyst,

John Mauldin, Editor

Outside the Box

JohnMauldin@2000wave.com

U.S. Consumers: Still Key to the Outlook

(Excerpted from the April 2012 edition of A. Gary Shilling’s INSIGHT)

In the Dec. 2011 issue of my Insight newsletter, I wrote: “In the U.S., major new fiscal stimulus is on hold, and monetary policy is impotent. State and local spending, housing, inventory investment, capital equipment investment and commercial construction are likely to remain subdued. U.S. exports are curtailed by sluggish foreign economies. So U.S. growth in 2012 will be decided by consumer spending, 71% of GDP. With declining real wages and incomes and low confidence, continuing strength in outlays is unlikely. A 2012 U.S. recession is probable, but milder than the 2007-2009 nosedive, unless another financial crisis unfolds.”

Four Months Later

Well, here we are, four months later. Do the economy and financial markets in the ensuing times substantiate our forecast? The chorus of bullish investors bellows, “No!” as they point to the 29% rise in the S&P 500 index from its October 2011 low (Chart 1). They even believe that a continued sluggish economy is good news.

To Read More CLICK HERE

I love earnings season. Don’t you? Sure, it can feel like trying to stand in front of an open fire hydrant, but so many opportunities can arise for both short-term traders as well as long-term investors due to the volatility among individual stocks. Time is scarce – institutional investors react swiftly, often buying or selling before they have time to fully digest the news.

Earnings season is particularly busy for me, as I try to keep up with the 100 stocks on my watchlist as well as pay attention to important ones that aren’t. This past week, for instance, 30 of the 100 reported, many hosting conference calls at the same time. One morning, I caught four straight live calls, but I tend to end up reading the transcripts for many of them. For those not aware, Seeking Alpha provides free transcripts, which are available on many companies.

When a company reports, there are many possible reactions. The report can can be viewed as “Good”, “Neutral” or “Bad”, but it’s not that easy. To me, it’s almost always about the future rather than the recent past. Ultimately, my key question that I want to answer is this: How does the news impact the future earnings? Presumably, if the future is brighter, the stock goes up. If it is dimmer, it goes down. If only it were that easy!

So, when I am judging the quarter, I am looking ahead, but I certainly recognize that many others focus on the short-term. For example, one of the stocks I will address below, Mattel (MAT), missed earnings by 50%. OH MY GOD! The reality is that this was their smallest quarter in terms of earnings typically, and the “huge miss” was rather inconsequential relative to the full year.

The real opportunities that stand out to me are the following combos:

* Good news, mild reaction

* Bad news, terrible reaction

While I am not addressing it today, often a company will report what I view as very favorable news, but the market, for whatever reason, doesn’t fully appreciate it. These situations can be tricky, requiring a judgment about why the stock isn’t moving. The flip-side, though, seems to happen more frequently: A company “misses” and the stock is pounded silly.

To Read More CLICK HERE

Jordan Roy-Byrne

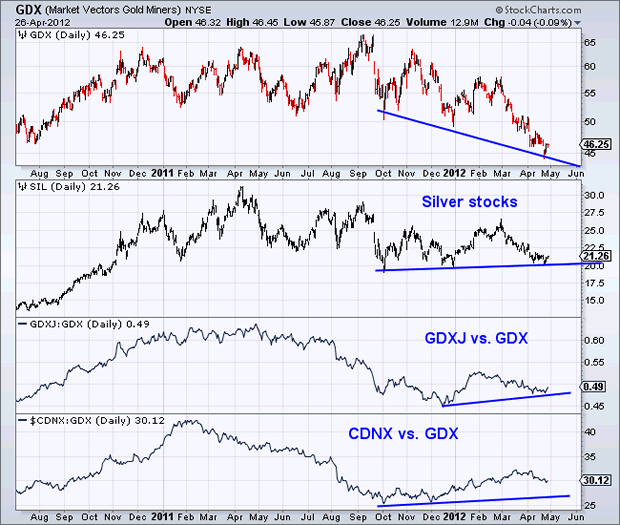

While the precious metals sector has consolidated and struggled to find a bottom, an important development has taken place. First, lets harken back to 2007-2008. Large cap mining stocks peaked in March 2008, yet the speculative sides of the sector “gave out” far earlier. The juniors and silver stocks actually peaked in April 2007. That was about a full year ahead of the large gold stocks. As the 2007-2008 crisis unfolded, juniors and silver stocks led the way down and displayed extreme relative weakness even as metals prices were firm.

Today, we have an entirely different and bullish development. As you can see in the chart below, the speculative areas of the sector have been outperforming the large gold producers (GDX). If this were really an end to the bull market or another collapse, the juniors and silver stocks would not be showing this kind of relative strength. In fact, the silver stocks have actually managed to hold near their 2010-2011 lows even as gold stocks have broken to new lows. We also see that the CDNX has been outperforming GDX since October while GDXJ has been outperforming since December.

GDX (Market Vectors Gold Miners) NYSE

Given the recovery of the past few days, we are likely witnessing the start of the next cyclical bull market for the gold and silver stocks which have essentially been in a cyclical bear or correction since December 2010. The above analysis implies that the more speculative areas of the sector, the juniors and silver stocks will be the leaders.

To Read More CLICK HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair