Stocks & Equities

The fraud that has been the US government and its effects on the Potemkin economy should be obvious by now. Yet our politicians continue to pretend the economy is growing and recovering. It is not. It is in a death spiral that their interventions caused and continue to feed.

The fraud that has been the US government and its effects on the Potemkin economy should be obvious by now. Yet our politicians continue to pretend the economy is growing and recovering. It is not. It is in a death spiral that their interventions caused and continue to feed.

The presentation below is another one from Gordon T. Long. This one includes Charles Hugh Smith as his guest. Both are worthwhile listening to, especially in this presentation.

What is discussed is expectations for 2014. The problems that may surface this coming year have their roots decades before. Each problem results from prior government attempts to stop normal economic corrections. Each was designed to stimulate the economy to avoid the necessary adjustments. Their effectiveness short-term was politically acceptable and was achieved by distorting prices, interest rates and lending standards. The intent was to send false signals to economic actors, to encourage them to behave in ways that helped short-term results but were harmful long-term.

….continue reading HERE

Over the past few weeks, I have been trying to push back against the usual contingent of bears. In particular, I have argued that this bull cycle is not yet over, markets are not in bubble and that people have been sitting for too long in way too much cash.

Over the past few weeks, I have been trying to push back against the usual contingent of bears. In particular, I have argued that this bull cycle is not yet over, markets are not in bubble and that people have been sitting for too long in way too much cash.

John Coumarianos of the Institutional Imperative is a prudent value guy. He wonders aloud in a recent blog post if I am too bullish?. He raises a number of interesting points via (mostly) valid criticisms.

I am not a rampaging bull, but if I come across that way to a reasonable guy such as John, then I am probably miscommunicating my thoughts. I am going to use his critique as a jumping off point to clarify some ideas and positions. I know that nuance and subtly are not necessarily my strong suits — nor the Internet’s, for that matter — but I will avoid all hyperbole in this discussion, click-throughs be damned.

Continued here

Wall Street was pointing to a higher start on Monday, with U.S. stock futures rising after better-than-expected euro-zone manufacturing data, although manufacturing conditions in the New York region didn’t pick up as much as expected.

Traders were also gearing up for this week’s all-important Federal Open Market Committee meeting, as well as watching for an industrial-production report just before the opening bell.

The New York Federal Reserve said itsEmpire State general business conditions index edged up to 1.0 in December from negative 2.2 in November. A MarketWatch survey of economists called for a reading of 5.0 in

Don Vialoux spoke in detail to Michael Campbell on Money Talks this Saturday about the rally about to take off and the different sectors, including the TSE: 300 that are highly likely to outperform. You can listen to the entire interview here beginning at the 3:56 mark: {mp3}mtdec14hourfp2{/mp3} in which Don talks about a Key Juncture occuring in Mining Stocks.

Don’s Monday Report complete with 45 Charts & commentary below:

The Bottom Line:

Barring an unexpected event coming from the FOMC meeting, the stage is set for a typical year end Christmas rally trade. Economic sectors respond strongest during this period, (Industrials, Consumer Discretionary, Materials, Financials). Preferred strategy is to continue to hold markets and sectors that benefit from seasonal strength at this time of year.

Equity Trends

The TSX Composite Index dropped 155.02 points (1.17%) last week. Trend remains neutral (Score: 0.5). The Index remains below its 20 day moving average (Score: 0.0) and fell below their 50 day moving average. Strength relative to the S&P 500 Index remains negative (Score: 0.0), but note early signs of turning positive. ‘Tis the season from the second week in December to the second week in March for the TSX Composite to outperform the S&P 500 Index! Technical score remains at 0.5 out of 3.0. Short term momentum indicators are trending down.

The S&P 500 Index fell 29.77 points (1.65%) last week. Intermediate trend remains up. However, short term trend changed to down on a break below 1,779.09. The Index fell below its 20 day moving average. Short term momentum indicators are trending down.

….continue reading Don’s analysis of sectors and stocks HERE

Economic News This Week

December Empire Index to be released at 8:30 AM EST on Monday is expected to improve to 5.0 from -2.2 in November.

November Industrial Production to be released at 9:15 AM EST on Monday is expected to increase 0.4% versus a decline of 0.1% in October. November Capacity Utilization is expected to increase to 78.4% from 78.1% in October.

November Consumer Prices to be released at 8:30 AM EST on Tuesday are expected to increase 0.1% versus a gain of 0.1% in October. Excluding food and energy, November Consumer Prices are expected to increase 0.1% versus a gain of 0.1% in October.

Housing Starts to be released at 8:30 AM EST on Wednesday are expected to increase from 891,000 in August to 900,000 in September to 920,000 in October and 950,000 in November.

Decision from the FOMC meeting is expected to be released at 2:00 PM EST on Wednesday.

Weekly Initial Jobless Claims to be released at 8:30 AM EST on Thursday are expected to fall to 333,000 from 368,000 last week.

November Existing Home Sales to be released at 10:00 AM EST on Thursday are expected to slip to 5,000,000 units from 5.120,000 units in October.

December Philadelphia Fed to be released at 10:00 AM EST on Thursday is expected to slip to 5.0 from 6.5 in November.

November Leading Economic Indicators to be released at 10:00 AM EST on Thursday are expected to increase 0.6% versus a gain of 0.2% in October

Third estimate of third quarter real GDP to be released at 8:30 AM EST on Friday is expected to remain unchanged from the second quarter estimate of 3.6%.

Canadian November Consumer Prices to be released at 8:30 AM EST on Friday is expected to increase 0.1% versus a loss of 0.1% in October.

Canadian October Retail Sales to be released at 8:30 AM EST on Friday are expected to increase 0.2% versus a gain of 1.0% in September.

….continue reading Don’s analysis of sectors and stocks HERE

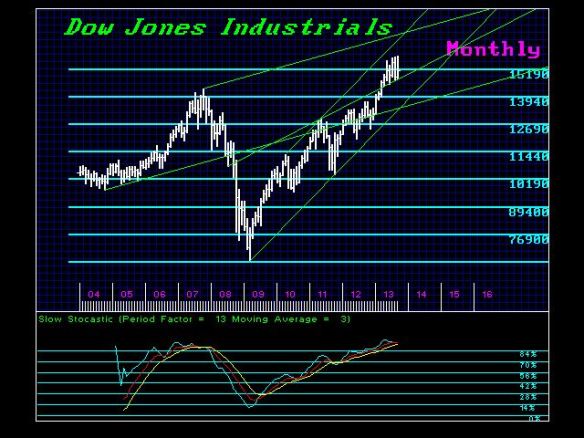

The Amazing thing is people are already talking about this is aBUBBLE that is unsustainable. They are now claiming household income is down 4% yet the S&P 500 is up 70%. They are incapable of any real analysis. The RETAIL investor is NOT involved in this market. There is no wild speculative fever. They are obsessed with this being a bubble purely based on new highs with no regard for the pattern.

There has to be a Phase Transition for a Bubble. That requires a near doubling in the value within often the last year. We have new highs in the DAX as well. Why? Is the European economy doing well? No way!

Capital is fleeing from PUBLIC to PRIVATE. This is capital preservation – not wild speculation. Pension funds are moving into equities. Central banks are even putting out their reserves to be privately managed. The IMF is proposing taking 10% of all accounts in a bank in Europe. They are arguing for a SuperBank in Europe that will have the power to directly tax people in Europe and no nation can stop them.

HELLO! Just where is the wild speculation these people are yelling about that make up a bubble?

Ed Note: More articles from Martin Armstrong:

Greece To Default in 2014 – Cycles of War – Presidential Elections 2016

Understanding 2014

Seeing the Light

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair