Winning the Rare Earth Economic War

China’s sudden cuts to rare earth export quotas and domestic production marked the beginning of a Rare Earth Economic War, proposes Jacob Securities’ Senior Mining and Metals Analyst Luisa Moreno. The good news is that partnerships between end-users and mining companies may just be the secret weapon to level the playing field for critical metals producers operating beyond China’s borders. In this exclusive interview with The Critical Metals Report, Moreno points to the companies that are closest to delivering high-quality goods for the benefit of manufacturers and investors alike.

COMPANIES MENTIONED: AVALON RARE METALS INC. – FRONTIER RARE EARTHS LTD. – LYNAS CORP. –MATAMEC EXPLORATIONS INC. – MEDALLION RESOURCES LTD. – MOLYCORP INC. – MONTERO MINING AND EXPLORATION LTD. – NEO MATERIAL TECHNOLOGIES – RARE ELEMENT RESOURCES LTD. –TASMAN METALS LTD. – UCORE RARE METALS INC.

The Critical Metals Report: Last year you published a research report called the Rare Earth Economic War. When we talked last time, you said that China was on one side and industrialized nations were on the other, with China winning. Does China’s new five-year plan with an emphasis on consumer consumption change that balance?

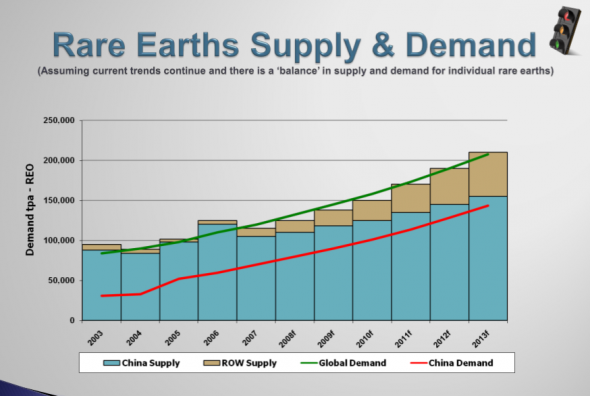

Luisa Moreno: China’s new five-year plan as it concerns raw materials suggests that China wants to better utilize its resources primarily for its own economic development, which in part supports the concept of a raw materials economic war. China, just as most nations, would like to be self-sufficient in key mineral resources. The country has about one-third of all the total rare earth element (REE) resources, but it supplies the world with more than 95% of its rare earth needs. I believe China is in a resource-preservation mode. However, what is not so fair are the differences between China’s domestic rare earths prices and international prices, which are usually much higher, and China’s dramatic decrease in production and export quotas in such a short period of time. China is well aware of the critical uses of some of the rare earths and it seems that it is determined to allocate a limited amount to the world and increasingly consume most of it by attracting REE-dependent manufacturing into China. The leaders plan to manage sustainable growth of the Chinese REE sector by attracting companies that utilize these resources. That would bring jobs while developing advanced rare earth-based technologies. It is no different from what other nations would like to do. Of course, China is at an advantage because it has the largest capacity in the world for the production of these elements and the know-how to refine them. The rest of the world is left with the option of moving manufacturing to China for better access to these materials.

TCMR: So you are saying that China is still winning?

LM: I believe so. Actually, the recent move by the U.S., EU and Japan to file a law suit against China may end up supporting that conclusion, if they are unable to persuade it to change its rare earth policies. It seems that China is increasingly consuming most of these elements and it is trying to control supply and prices.

TCMR: Can lawsuits and political pressure really make China change its export habits?

LM: Potentially. I think a negative ruling could make leaders think twice before deciding on export quotas or other related trading policies. But China will put Chinese interests first, obviously. I don’t think that the rest of the world has much leverage with what is now the second-largest world economy. I think the lawsuits bring attention to how other nations may feel, but might not necessarily be sufficient to change China’s policies regarding rare earths or other critical materials.

TCMR: China’s Ministry of Commerce recently announced that the export quotas would remain essentially the same—30,184 tons (t) in 2012—but only 50% of the quota was used last year. Is that quota meaningful?

LM: 2011 was an exceptionally bad year, the tsunami in Japan, the second-largest REE consumer, having caused a slowdown in demand, not to mention the global economic slowdown in the second half of the year, which was marked by poor economic conditions in Europe and negative economic politics in the U.S. The second half of 2011 was clearly not a favorable one for rare earths and many other commodities. Now that the rare earth element export quotas are separated into lights, mediums and heavies, I think it will become more evident where the real demand is and how tight the export quotas really are, assuming that we see some economic recovery.

I think the new invoicing system that China is implementing to better control production and exports may decrease illegal exports of rare earths as well. Right now, official export numbers are not the total picture because so much is illegally produced and exported. I’m not sure China will be able to control all of the illegal exports, but at least reining it in a little bit will impact the supply-demand equation.

If Lynas Corp. (LYC:ASX) comes into production and Molycorp Inc. (MCP:NYSE) ramps up production, we should see an increase in production of light rare earth elements (LREEs). That may make export quotas for LREEs less meaningful. However, China will probably maintain export quotas for some of the most critical REEs, including the light element neodymium and some of the heavy rare earths (HREEs) like dysprosium and yttrium. For the next five to 10 years, as long as there is a risk that some of these elements might be in shortfall, we may still see an REE export quota of some sort.

TCMR: You called 2011 an exceptional year in terms of bad economic news, but could the drop in rare earths prices indicate that it had been in a bubble? Have companies’ efforts to re-engineer products and eliminate their needs for rare earths been successful? Or was it just the economy in general that accounted for the price drops?

LM: Likely it was a combination of all those things. I think the current and future demand for materials such as dysprosium should be healthy, but I’m not sure if $3,000/kilogram (kg) was justifiable. Similarly, the prices of lanthanum and cerium, which are fairly common elements historically below $10/kg , were above $100/kg back in August, a level we now know is not really sustainable. Prices seem to have been in a bubble and when demand decreased, REE prices also fell significantly. Chinese officials may have wanted prices to stay high and some Chinese refiners even suspended production for a few months when prices were falling and demand was weak.

TCMR: Considering that not all REEs are created equal in terms of market value, what are some of the most in-demand elements, and could those prices break out this year?

LM: I think the critical elements identified by the U.S. Department of Energy—neodymium, praseodymium, terbium, dysprosium and yttrium—could experience a significant increase in demand; some may even be in shortfall right now. It is possible that the prices of these elements may rise, but in the short term, we might see continued decreasing prices until they stabilize. I have already seen signs that they are starting to stabilize. If there is stability, or better yet growth in the global economy, the prices for some of these elements could potentially increase this year.

TCMR: You mentioned Molycorp and Lynas. Molycorp just announced the start-up of its manufacturing facility in Mountain Pass, California. Will that produce mostly LREEs? Could those two companies make a difference in global supply in the next couple of years?

LM: Absolutely. Light rare earths are the most sold or consumed elements—particularly lanthanum and cerium. They are the cheapest, but they are the ones that are sold in the highest volume. Lynas and Molycorp could also produce significant amounts of neodymium, which is very important for the production of super magnets used in hybrid cars, computers and wind turbines. Molycorp really does not have much of the heavies like dysprosium and terbium at Mountain Pass. Lynas might be able to produce some of the most critical heavies from its plant in Malaysia, but it would be rather expensive given that it only has small percentages of heavy lanthanides. In any case, even if both companies ramp up production, it won’t completely close the gap in demand that exists for some of these critical elements outside China.

TCMR: When do you see each of those companies going into production?

LM: There have been delays with the Lynas project because of permitting issues, but I think it hopes to start production in Malaysia before the end of the year. Molycorp expects to reach its phase one annualized production of 19,050t of mixed rare earth oxides by Q312 and separated products perhaps before the end of the year. It’s hard to say exactly when these companies will be able to reach their target production. As you know, with mining projects delays are not unusual, but both companies are working very hard to deliver on their promises.

TCMR: What are your top picks for non-Chinese companies that could supply some of the heavy elements in the future?

LM: My top picks include Matamec Explorations Inc. (MAT:TSX.V; MRHEF:OTCQX) and Ucore Rare Metals Inc. (UCU:TSX.V; UURAF:OTCQX). I cover both companies and they both have a favorable REE distribution with high percentages of the critical elements. I think Matamec has made significant progress with its metallurgy and its partnerships. The company just announced that Toyota Tsusho Corp. (TYHOF:OTC; 8015:JP) has signed a binding memo of understanding with Matamec, which means it has priority over the development of the Kipawa. That is very good for Matamec.

Ucore should come out with a preliminary economic assessment (PEA) in the next few weeks, and we should be able to better assess if it is an economically viable project. The project is in Alaska and we believe it is the most significant HREE deposit in the U.S. It’s very interesting.

TCMR: Could either of these companies be takeover targets for a Molycorp looking to cover the HREE space?

LM: If Molycorp wants to become the leading rare earths company, it will have to find a solution for the heavy rare earths. I think Matamec could have filled that role, but because Toyota has now the binding agreement, it will be difficult for Molycorp to approach Matamec. Besides, it seems that Toyota is interested in a 100% offtake deal with Matamec. Ucore, on the other hand, continues to be another good option for Molycorp, although the company is still working on its metallurgy and may be seen as too early stage. When the PEA comes out, hopefully we’ll have a much better idea of the progress of the project.

Another company that would also be of interest is Tasman Metals Ltd. (TSM:TSX.V; TAS:NYSE.A; TASXF:OTCPK; T61:FSE), which has the Norra Karr deposit in Sweden. It is close to Molycorp’s Silmet refinery in Europe. Tasman has one of the highest percentages of heavies. Contrary to Ucore and Matamec, it actually has a very large resource. My understanding is that in terms of the metallurgy, it made significant progress but it is not as advanced as Matamec or Rare Element Resources Ltd. (RES:TSX; REE:NYSE.A). Hopefully, it will file a PEA this year as well.

TCMR: Matamec is trading at $0.32 today and Ucore at $0.41. Could the recent news be catalysts for both of those companies?

LM: I think so. As the market looks around for HREE alternatives to Molycorp, I think there is great potential for Ucore and Tasman to be recognized by the market as potential targets. Matamec is currently working on the details of a definitive agreement with Toyota Tsusho, to be completed by July.

TCMR: You have commented on the importance of metallurgy and the refining process for extracting and efficiently delivering high-quality oxides for each individual mineral source because each one is very different. What companies are well on their way to doing this?

LM: Like I said, Matamec is well underway in doing this. Now, it has a fantastic partner, which is Toyota Tsusho and all the associated companies and likely universities that will be involved in developing that project.

I think another company that has made significant progress is Montero Mining and Exploration Ltd. (MON:TSX.V). It has a deposit in Tanzania and it just announced that it has produced an oxide concentrate. That’s really good.

Rare Element Resources Ltd. is another. I visited its pilot plant last year. It has also made significant progress. The resource is mainly comprised of bastnasite mineral, which, relative to other deposits, might mean that it will have fewer processing challenges. It has been able to produce a mixed oxide concentrate and is moving towards separating the elements and producing individual elements oxides. As I said, it’s already at the pilot level and completed a prefeasibility study. Rare Element is one of the most advanced projects; we believe however that the company needs to secure offtake agreements and a JV partner capable of co-financing the $375 million project.

Another one that I like is Frontier Rare Earths Ltd. (FRO:TSX). It just published a comprehensive PEA, which included a separation plant. No other company has done that yet. Frontier has a partnership and partial offtake agreement with Korea Resource Corporation and the support of a consortium of Korean companies.

TCMR: Could other REE companies that you’re following break out in the next few years, either because of agreements with partners or as takeout candidates or because they might actually start producing?

LM: I think we should perhaps pay more attention to what is going on in Brazil. We believe that Neo Material Technologies (NEM:TSX) spent some time there before being acquired by Molycorp. It seems that the company may have been looking at recovering xenotime from tailings at the Pitinga mine in Brazil.

Another private project is owned by Mining Ventures Brasil. It seems to have a colluvial deposit with high percentages of xenotime and monazite. The distribution for the heavies may be quite favorable. It’s an early-stage project; the company is moving forward with the metallurgy now. There is a possibility that things could work out pretty fast for them.

Another private project still in Brazil is the one that it is ongoing at Companhia Brasileira de Metalurgia e Mineração (CBMM). It is the largest producer of niobium but it also has rare earths in its deposit.

Medallion Resources Ltd. (MDL:TSX.V; MLLOF:OTCQX; MRD:FSE) is a public company targeting monazite deposits around the world. Monazite, just like xenotime, has been used in the past to recover rare earths. The model is to find these monazite deposits because they represent a far easier metallurgic process than other sources. That could allow Medallion to fast-track its project.

A lot of folks are trying to find solutions for these metals.

TCMR: The sheer number of early-stage projects presents a challenge for potential investors. How can investors pick which companies might be successful? What should they focus on when there are so many moving parts—the management, the location, the metallurgy and the different elements themselves?

LM: To start, investors should be looking at the same factors they usually use to assess mining companies. Beyond that, the most important factors for REE projects specifically are metallurgy and industry partnerships. However, it depends what investors are looking for. Essentially, there are some names in the rare earths space that are well known and respected. Examples of that are Avalon Rare Metals Inc. (AVL:TSX; AVL:NYSE; AVARF:OTCQX) and Rare Element Resources Ltd. They were the first ones to publish PEAs and are still perceived by some as the frontrunners. There are, however, lesser-known companies that have received far less love from the market, despite having made significant advances. That includes Matamec and Frontier, which I still feel are somewhat under the radar.

If investors are anticipating a bounce in rare earths stocks and would like to hold rare earths companies that have made major progress in metallurgy, with solid industry partnerships and have great potential for significant long-term upside, I think names like Matamec and Frontier might be good. They’re relatively more advanced, particularly in metallurgy, which is very important because you can have 100 million tons at high grades, but if the metallurgy is complex and you are five years away from solving the processing to a level where it’s economic to recover these elements, that might not be so competitive in this market. Those that are more advanced will be better positioned to secure development partners. That’s very important because the PEAs coming out show that projects are capital expenditure intensive and industry partners can help finance these projects.

Rare earths are not commodities; end users, usually through joint ventures, guide companies toward production of appropriate materials. It’s a very complex space. As I said, although Matamec and Frontier have made significant progress, they consistently have underperformed some of their peers. So investors who are interested in those names will have to be really patient. We believe, however, that Molycorp is the undisputable leading non-Chinese rare earth listed company at the moment and investor interest in this space should follow and analyze this company to determine a good entry point.

TCMR: You’re going to be speaking at the International Rare Earths Summit in San Francisco in May. What message will you be delivering?

LM: Seeing as a significant part of the audience is expected to be end users who are extremely concerned about the long-term availability of these elements, I’ll be talking about the challenges that rare earth miners and future producers face, focusing on how end-users may better participate in the development of a global rare earths supply industry. They could surely help fast track the development of the rare earths industry outside China.

TCMR: Thank you very much for your time, Luisa.

Luisa Moreno is a senior mining and metals analyst at Jacob Securities Inc. in Toronto. She covers industrial materials with a major focus on technology and energy metal companies. She has been a guest speaker on television and at international conferences. Moreno has published reports on rare earths and other critical materials and has been quoted in newspapers and industry blogs. She holds a bachelor’s and master’s in physics engineering as well as a Ph.D. in materials and mechanics from Imperial College, London.

Want to read more exclusive Critical Metals Report articles like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators and learn more about critical metals companies, visit our Critical Metals Report page.

DISCLOSURE:

1) JT Long conducted this interview. She personally and/or her family own shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of The Critical Metals Report: Rare Element Resources Ltd., Medallion Resources Ltd., Frontier Rare Earths Ltd., Tasman Metals Ltd., Matamec Explorations Inc. and Ucore Rare MetalsInc. Streetwise Reports does not accept stock in exchange for services.

3) Luisa Moreno: I personally and/or my family own shares of the following companies mentioned in this interview: None. I was not paid to do this interview.