Currency

INSTITUTIONAL ADVISORS

THURSDAY, DECEMBER 20, 2012

BOB HOYE

PUBLISHED BY INSTITUTIONAL ADVISORS

The following is part of Pivotal Events that was

published for our subscribers December 13, 2012.

SIGNS OF THE TIMES

“Italian new car sales plunged in November…Decline of 20.1% Y/Y.”

– Dow Jones, December 4

“The European debt crisis has given way to a new wave of corruption as some of the most hard-hit countries have tumbled in an annual graft-ranking study.”

– Bloomberg, December 5

This is from a watchdog group called Transparency International. Greece fell to 94th place from 80th, ranking worse than Colombia and Liberia. Greece’s “Golden Age of Democracy” was founded not so much on intellectual inspiration, but more upon Athens sitting on one of the richest silver camps in history. Athenians could afford democracy, Spartans could not. The problem recently is that Greece, like any other country, cannot afford interventionist government.

“German industrial production unexpectedly dropped in October.”

– Bloomberg, December 7

The number was down 2.6% from September, which was down 1.3% from August.

“U.K. Manufacturing production fell more than economists forecast in October. Food and alcohol slumped.”

– Bloomberg, December 7

Progress on this great reformation is being made. The legislature in Michigan passed a “Right to Work” bill. This brings the count to 24 states where people can work without being forced to join a union. They can work without being forced to contribute their money to union leaders with an agenda they may find offensive.

PERSPECTIVE

Global business conditions continue to deteriorate. Normally, we don’t follow these types of numbers too closely but they have been interesting since the summer. The ability to service debt is diminishing as federales around the world create huge amounts of paper as their lap-dog central banks buy it.

At some time the spell breaks, but skepticism is better than faith that another government scheme will work. It has been frustrating that our technical overboughts on various bond sectors last summer were not followed by substantial price declines. The long bond dropped 9 points when about 15 were possible. Corporates and Munis eased their overbought conditions and then firmed.

What prevented a significant setback? Central bank bids and the knee-jerk about buying bonds as the economy weakens. Into corporates? Then there was the flight-to-risk bid as stocks and commodities weakened into early November.

The bond future rallied to resistance at the 151 level in the middle of November. The action was only moderately overbought, which makes this week’s decline interesting. Yesterday clocked an outside reversal to the downside. Perhaps the one-way-street is beginning to wander.

However, as Fat Jack famously observed “There is nothing too good that it can’t be screwed up.”

STOCK MARKETS

Due to the oversold in early November and seasonal influences a rally has been possible into December. The next phase includes small caps outperforming the big ones from around now until early January. The “Turn-of-the-Year” model.

If the rally was moderate it would be within the Secular Bear Market model.

So far it has been moderate.

CURRENCIES

The USD was likely to decline into January. Last week, it almost reached support at the 79 level. The low was 79.7 on a weakness that could run into January.

The Canadian dollar has been expected to be firm into January. The low was 99.5 in early November and so far the high has been 101.8.

If commodities stall out over the next few weeks, so will the C$.

COMMODITIES

After all of the drought excitement in July, wheat continues its “stair-step” down. The high was 947 and today its at 806, a new low for the move. Last week’s view that firming then could continue into January seems not to be working.

Other agricultural prices have been sympathetic, with the index (GKX) stair-stepping down from 533 to this morning’s 462, a new low for the move.

However, wheat and the index are approaching an oversold condition.

Going the other way, base metal prices have rallied nicely with copper making it to 372 yesterday. The action is close to an overbought condition and close to resistance. Copper is vulnerable.

The index of base metals (GYX) is recording a similar pattern and at 397 seems close to a setback. On the bigger picture, base metals set an important high at 502 in April 2011. We took that as a cyclical high and the subsequent low was 346 in July – during that concern about European insolvencies. The difference between then and now is that the European economy has suffered further deterioration but there is no panic. Not even a little one.

Metals were likely to rally into January, but the action is approaching overbought. Who cares if it continues over the next few weeks. Let’s declare a victory and enjoy a “Christmas bowl of smoking” punch. It would help to restore alcohol consumption numbers in England.

Link to December 14 ‘Bob and Phil Show’ on TalkDigitalNetwork.com: http://talkdigitalnetwork.com/2012/12/fed-checks-into-hotel-california/” http://talkdigitalnetwork.com/2012/12/fed-checks-into-hotel-california/

BOB HOYE, INSTITUTIONAL ADVISORS

E-MAIL HYPERLINK “mailto:bhoye.institutionaladvisors@telus.net” bhoye.institutionaladvisors@telus.net

WEBSITE: HYPERLINK “http://www.institutionaladvisors.com” www.institutionaladvisors.com

Prognostication on the future can be a mug’s game. You look like a goat if you’re wrong and some kind of wizard if you’re right. But I learned early on in my career at Richardson Greenshields, and then RBC Dominion Securities, working with the influence of some great people like Don Vialoux or Ray Hansen that true investment success comes from understanding probabilities. It’s a stark, uneventful way to assess opportunity, and act, but the most relevant now. With the contemporary twin investor objectives of performance and asset preservation having one’s cake and eating too, or at least a bit of both, is the portfolio manager’s job these days.

From today’s standpoint – that is post-QEternity, post-US presidential election, pre & post the Euro mess, and as we (especially the non- American “we”), march along with the US on their lemming saunter (it is like a slow motion train wreck isn’t it?) towards the fiscal cliff – here’s what changes are occurring in asset classes, sectors, TSX stocks and countries. They lay out an investment map for 2013.

Asset Classes

Our regular weekly work on asset classes is a study in inter-market analysis, something crucial to delivering absolute return. This tells us which broad asset classes are strong and which are weak. Within the large group the biggest movers on an intermediate or investment term basis (vs. short term or trading) since mid-September were US government bonds, the US dollar and silver bullion. Bonds jumped from 11th to 4th; the US dollar moved from 14th to 9th; and silver bullion from 1st to 13th. While we expect markets to favour pro-risk assets through to the New Year big money appears to be placing its markers in more risk adverse classes.

TSX Sectors

Drilling down into TSX sectors the top ranked are the cons. staples, cons. discretionary, telecom and trusts. Industrials and financials moved down out of the upper ranks to mid-tier. Rogers Comm. (shown) as a presentation of the teleco sector (we have preferred to own BCE) continues to show strength against the TSX. The recent up mofavveofuorr pthroe-risk moved down oowners of the trade-hot Blue Jays too shows a longer term commitment to industries with more stable revenue, cost-certainty and a good yield. Consumer discretionary in Canada is not as much about consumer consumption pace as it is in the US. Besides take-out-candidate Astral Media, it also has Shaw and Cogeco. Go figure.

TSE Stocks

On an individual stock basis the strongest stocks within the TSX 60 tables are appropriately Rogers, Shaw, BCE Inc., TransCanada, Enbridge, Weston and Fortis Inc. Collectively all the stocks passed the TSX – we include the TSX itself in the TSX 60 company component table for a total of 61 in the list – over the last month, again reasserting investor compulsion towards securities and sectors showing reliability. We recently purchased George Weston (shown) as it has more upside potential and a good risk-to-reward equation. The company just announced decent earnings and a dividend increase. Success lies at the hands of Loblaws management. The baking is doing well. (Ed Note: I know they bought George Weston before the run-up in December shown below )

Countries

It’s no surprise to see Switzerland make a jump, going from 17th to 6th in the country rankings. When you peer inside the components of the ETF (shown), which presents a cross-section of Swiss industry, you see names like Nestle (cons. staples), Novartis (pharma), and Roche (pharma). For investors, Switzerland and all things Swiss represent performance, reliability and efficiency. They are expecting the same attributes of their capital today. Other stand outs include Turkey, Thailand and Mexico. The common theme amongst the latter group is a young population, smaller government liabilities and pro-commerce policies and reasonable resources.

S&P Sectors

In the US, biotech, healthcare, financials consumer staples and consumer discretionary lead the pack. The biggest losers on the month? The NASDAQ, info tech, and the S&P. Like in our TSX 60 rankings we include broad indices to understand when shifts are occurring. Healthcare and biotech are the long term standouts, and most healthcare companies have significant biotech divisions now. On the shorter term I expect that we will see trading investments made in tech (Apple), materials (Freeport), industrials (Cat) or beaten up financials (Bank of America) into December but on the whole they have displayed material changes since mid-September.

Conclusion

With corporate earnings rolling over from weakening top-line revenue growth and decreasing effectiveness of central bank stimulus programs, investors are preferring to allocate to those securities, sectors or countries displaying predictability in profit and income (dividends) As alluded to above, there will be one more kick at the “risk-on” can at the end of 2012 here and briefly into 2013, a trading timeframe. Granted there will be particular or individual cases of strong growth, but these will be the exception not the rule. When scanning those areas showing good price action there is very favourable return potential.

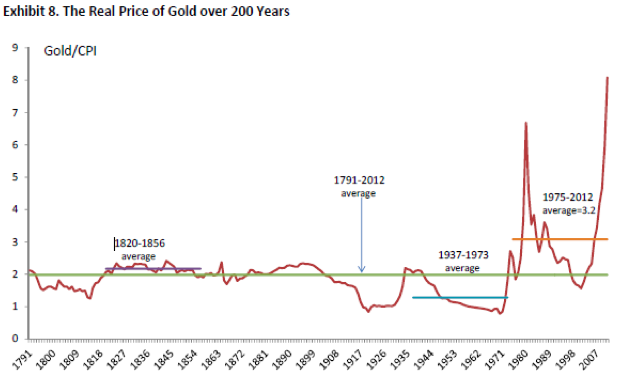

Bitten By the Gold Bug

Time to Buy, or Sell?

Gold in Ancient Rome and Today Is Gold A Currency Hedge?

Then Why Buy Gold?

Central Bank Insurance

How to Buy Gold

Scandinavia, Europe, and Toronto Oh, and the Mayan Calendar

By John Mauldin | December 17, 2012

“For every complex problem there is an answer that is clear, simple and wrong.” – H. L. Mencken

Possibly, the question I am asked the most is, “What do you think about gold?” While I have written brief bits about the yellow metal, I cannot remember the last time I devoted a full e- letter to the subject of gold. Long-time readers know that I am a steady buyer of gold, but to my mind that is different from being bullish on gold. In this week’s letter we will look at some recent research on gold and try to separate some of the myths surrounding gold from the rationale as to why you might want to own some of the “barbarous relic,” as Keynes called it. My personal reasons for owning gold have evolved over the years. I will tell you the story of my own journey, and you can decide for yourself whether to think about coming along.

I cannot start this letter, however, without a brief but sad note about the tragic events at Newton. As a parent I cannot imagine the anguish and horror at learning that my child was murdered while sitting in her first-grade classroom. The senseless wasting of so many young lives leaves me profoundly saddened for our country and culture. There is not much that I can say other than to extend my deepest sympathies to the families and friends of the victims – and perhaps to wonder about the wisdom of relegating violence to the level of an arcade game in the movies and games our kids watch and play.

Bitten By the Gold Bug

I wandered as an innocent bystander into the world of investment newsletter publishing in 1981-82. Back then it was a world inhabited to a great extent by “gold bugs” of one variety or another. The investment newsletter world was in its infancy, and I was something of a direct- mail wizard, brought in to weave my magic with mailing lists and fluid copy. You can’t write……

…..read the rest of this exhaustive analysis HERE (13 pages). At least read “Time to Buy or Sell” on page 3.

Ooops! Just when everyone said gold must go higher – immediately…!

Ooops! Just when everyone said gold must go higher – immediately…!

Markets are made of opinions, some better than others.

There are always plenty of opinions about gold. And right now they’re clearly making the market. Just not in the way you would think.

“There are too many bulls, including me,” warned hedge-fund and commodities legend Jim Rogers toCNBC overnight. He advises caution if you’re buying gold on this drop. Unlike most everyone else.

Swiss bank UBS last week kept its 2013 forecast for gold to average $1900 per ounce – a rise of 14% from the 2012 average so far – while fellow London market-maker Barclays now sees gold averaging $1815 next year, a snip off its previous 2013 forecast.

Investment bank Morgan Stanley takes “a bullish view”, as does Bank of America. It thinks gold will average $2,000 next year, rising to $2,400 in 2014. Whereas Capital Economics (who have an opinion on pretty much anything and everything) predict a peak of $2,200 in late-2013, some 10% above their previous guesstimate.

Never mind that 2013 used to mean $2,500 per ounce for the London-based consultancy. That was back in 2011. And like many a gold bull right now, Capital Economics reckons the treatment of gold under the world’s banking rules – aka, Basel III – could “provide an important psychological lift to the market.”

How come? “European regulators appear increasingly willing to recognise gold as a high quality liquid asset,” explains today’s note from Julian Jessop, head of commodities research, pointing to a much-discussed – but little understand – change in banking regulation.

“Others are likely to follow. Increased demand for gold to meet the tougher liquidity requirements could then go some way towards mitigating what might otherwise have been a large downside risk when the authorities do eventually take away the exceptional liquidity they have provided to the banking system.”

You can find the same opinion – only with less understanding, subtlety or caveating – pretty muchacross the internet. Beware any “analyst” who says gold is about to become a “Tier 1” asset (that refers to capital reserves, not liquidity). Also beware if they claim it’s about to happen, like immediately, starting on New Year’s Day!

Because most of the developed world struggled to implementing Basel II – the last set of agreed principles. Putting Basel III into place by 2013 is now an “ambition” most national regulators have delayed and deferred well into the never-never. And gold’s new status under those rules is still very far from certain. It may perhaps be valued at 50% of its price when regulators count up the liquid reserves a bank holds. Or it might yet get carried at 100% of market-price, causing a headache for the beancounters as the price moves up (or down – shhhh!) minute by minute.

Still, the possible re-assessment of gold as “a high quality liquid asset” would mark a significant step after 12 years of annual price gains. It would mark gold’s “growing use as collateral”, as Capital Economics say. That would mark a new stage in gold’s return to the banking system from hated, under-priced and un-holdable relic. Not dissimilar, perhaps to gold’s return as an investable asset for US citizens on New Year’s Day 1975.

For more than three decades gold bullion had been illegal to own in the United States. Gerald Ford’s executive order to remove that block clearly helped the long 1970s’ bull market run on towards its big 1980 top. US savers had already missed out on a five-fold gain. Now the wealthiest savings market in the world could participate in the inflation-fuelled gold bull market at last!

But ooops…

“Gold rose 600% in the 1970s,” said Jim Rogers back in 2007. “Then gold went down nearly every month for two years. Most people gave up.”

You can’t blame investors who quit the gold market between 1975 and 1977. The gold price fell very nearly in half after all. But that is simply “what happens in bull markets,” said Rogers. And between 1977 and 1980, “gold went up another 850%.”

Fast forward to end-2012, and “Gold is having a correction,” said Jim Rogers last night. “It’s been correcting for 15-16 months now, which is normal in my view, and it’s possible that [the] correction is going to continue for a while longer.”

And just in time for the much-hyped entry of new commercial bank buyers, too. Or so says this opinion.

Looking to Buy Gold or physical Silver Bullion today…?

Adrian Ash runs the research desk at BullionVault, the physical gold and silver market for private investors online. Formerly head of editorial at London’s top publisher of private-investment advice, he was City correspondent for The Daily Reckoning from 2003 to 2008, and is now a regular contributor to many leading analysis sites including Forbes and a regular guest on BBC national and international radio and television news. Adrian’s views on the gold market have been sought by the Financial Times and Economistmagazine in London; CNBC, Bloomberg and TheStreet.com in New York; Germany’sDer Stern and FT Deutschland; Italy’s Il Sole 24 Ore, and many other respected finance publications.

Where Has Objectivity Gone?

It was the best of times; it was the worst of times for the American public over the past month, as it was treated to two high-profile, but deeply conflicting, economic forecasts.

Despite declaring in 2008 that the age of cheap oil was over, the International Energy Agency (IEA) surprisingly announced last week that the United States would become the largest oil producer in the world by 2020. Hooray! This superlative declaration titillated US media organizations, who understand quite well that Americans love to secure a #1 ranking in just about any category (save for prison incarceration, divorce rates and obesity). As I explained to the Keiser Report, however, the IEA has done little more than produce an attention grabbing headline here. Simply ranking the “top oil producer” in 2020 may mean much less than the public currently understands.

This announcement has since led to the magical thinking that we can somehow take ownership of this future “extra oil” not eight years from now, but rather…. today. In other words, the additional 3 mbpd (million barrels per day) of crude oil and the 1 mbpd of NGL (natural gas liquids) that the IEA forecasts for 2020 have suddenly been booked into the “readily-available” column and are already being factored into US growth projections. That is premature, to say the very least.

In contrast to the IEA’s report was the grim outlook recently offered up by legendary investor Jeremy Grantham, of GMO in Boston. Mr. Grantham has been increasingly sounding the alarm on a future of significantly lower growth rates for some years now. It is rather obvious, as well, that Grantham has been methodically making his way through the reading list of resource scarcity scholarship over the past five years, taking in the views of everyone from Joseph Tainter to Jared Diamond. Combined with the available data, Mr. Grantham has come up with the rather unsurprising conclusion that the rate of future growth is set to be much lower than most anticipate. In Grantham’s view, there will be no return to normal growth as was enjoyed in the US in the post-war period (after 1945).

Reactions to Grantham were predictable. Has he lost his mind? And of course: Grantham goes Malthusian was another common refrain. Many of the media outlets covering Grantham’s letter, On the Road to Zero Growth (link to PDF here; free registration required at GMO website), also engaged in predictable reductio ad absurdum, claiming incorrectly that he was calling for the end of the world. Indeed, no such call by Grantham was made.

It leaves the rational observer wondering: Why is the media so breathless in its exultation of any optimistic forecast, no matter how poorly supported? And why does it vilify those who attempt to argue the other side?

Where has our objectivity gone?

Grantham’s Actual Message

It’s clear that very few understood what Grantham was really saying.

Moreover, many were mistaken that Grantham has adopted an ethos of negativity or that he has become ideological in his views. Quite the contrary. He is working with the same data observed by many hedge funds, international organizations, and academic research that shows that, as we entered the past decade, the extraction and production rates of many critical resources began to slow – and slow significantly.

Just to kick off this discussion, let’s start with the master commodity, oil:

In the ten years leading up to 2004, global crude oil supply grew at a compound annual growth rate (CAGR) of 1.71%. This rate of supply growth started during the strong economic phase during the 1990s, and only strengthened after the recession of 2000-2002 when countries like Russia came online with fresh oil supply.

…..read more HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair