Gold & Precious Metals

I received the following from reader Bill Teter:

The CNBC “Fast Money” program, airs Monday through Thursday for one-hour nightly, often features Dennis Gartman as a guest commentator. He’s intelligent, a ‘fun’ guest who always responds to the question “Good to see you, Dennis” with “Always good to be seen!” Fast Money often refers to Dennis as “The commodity king” for his opinions on all things so related, from coal to cotton to platinum. I perk up every time Dennis appears as a guest, because usually the subject of the price trend in gold will be discussed. Dennis always appears as a kindly and gentlemanly person, and is one of the favorite Guests and some-times Panelist on “Fast” (as they often refer to their show). After all, “Fast Money” first-and-foremost, is a SHOW!

But here’s what I learned long ago about Dennis through my personal experience, and now it is revealed in a graph: Dennis is more likely to serve as a good contrarian indicator! I wasn’t aware that there was a fund that would prove that point until Peter Degraaf ran this chart and commentary today

Featured is the Horizons Gartman Fund since its inception, with the price of gold at the top.

In my January 6, 2013 post, I said this about Dennis the Menace:

“…We also once again had to endure Dennis Gartman throwing so-called Goldbugs under the bus for the umpteen time (which if history is any indication shall once again prove to actually be a buy signal)….”

While I believe Bill Teter’s assessment is accurate, no one has come close to being so badly wrong on gold for more than a decade (while being so arrogant) as Jon “Tokyo Rose” Nadler, Dennis Gartman is a shrewed marketer and a very good public speaker. He has masterfully played the media to a point where his actual performance takes a back seat to how well he comes across in their minds. He can and is for the most part, entertaining.

Once you appreciate this, Dennis the Menace will become little more than a fly and rather than swatting him to his death, just appreciate that he’s a goldbug who can’t bring himself to “come out of the closet” as in his mind it would throw a monkey wrench into the superb (and masterfully developed) propaganda machine he knows the media has bought into when it comes to his actual gold forecasting record among his overall performance. Have pity as down deep he knows GATA is right but he also knows supporting GATA’s argument would cast him as a kook, conspiracy nut, and tin-foil hat wearer. His ego and his business couldn’t afford such a label.

Me?

The call for this week: Last week saw the highest flows into stock funds in six years. Those flows, over the past two weeks, have lifted the broadest-based index, the Wilshire 5000, by $500 billion! That rally has caused the Wilshire to make a much clearer upside breakout than the SPX; it is closer to its all-time 2007 high than the SPX (see chart on page 3). I think the Wilshire is eventually pointing the way higher, despite the current near-term overbought condition. This week should tell if it is a true upside breakout, or if we will need to spend some more time consolidating before trading higher…

The call for this week: Last week saw the highest flows into stock funds in six years. Those flows, over the past two weeks, have lifted the broadest-based index, the Wilshire 5000, by $500 billion! That rally has caused the Wilshire to make a much clearer upside breakout than the SPX; it is closer to its all-time 2007 high than the SPX (see chart on page 3). I think the Wilshire is eventually pointing the way higher, despite the current near-term overbought condition. This week should tell if it is a true upside breakout, or if we will need to spend some more time consolidating before trading higher…

Believe it or not, mutual funds were once exciting. If you remember the days before the internet – when investors got their information from newspapers and magazines – mutual funds were the biggest advertisers and the focus of nearly every article.

They were sexy.

The industry sold them well. It told us someone smarter than you and me would invest our money for us and make us boatloads of profits.

I remember nervously and excitedly making my first investment. Despite working an entry-level job for no money and living in Manhattan, I had saved up a few hundred dollars that I was ready to put to work.

I chose the Fidelity Select Health Care Fund (Nasdaq: FSPHX), figuring there’ll always be demand for health care, no matter what the economy was doing. I was right. The mutual fund turned my few hundred dollars into a few hundred more.

But the more I investigated these funds, the more I got turned off. The lessons I learned 20 years ago are still valid today.

In October I told you that 65% of mutual fund managers underperform the S&P 500. It was proof you should take your investments into your own hands.

And now, the numbers for all of 2012 are out. It looks like fund managers improved their performance.

This time, “only” 61% of fund managers did worse than the market.

In other words, if you invested in a stock mutual fund (not a focused fund like precious metals, health care or technology), you still had a nearly two out of three chance of underperforming the market.

Heck, you could do that yourself by throwing darts at The Wall Street Journal, without having to pay expenses to the mutual fund company.

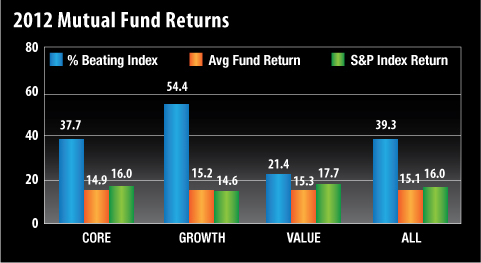

Here’s a graph courtesy of Abnormal Returns…

With a quick glance at the bars on the right, we can see just 39.3% of all mutual funds beat the S&P 500. The average fund returned 15.1% versus the S&P’s 16% gain.

With growth funds, just over half beat their benchmark indices (which performed worse than the S&P). And although 54% of growth-fund managers beat their index, the average return was 15.2% – still below the S&P 500’s gains.

Finally, value managers had a horrible year, with only 21% beating their benchmark.

The bottom line is, the majority of mutual funds will never make you rich. Which is why I present you…

THE THREE REASONS WHY YOU CAN MANAGE YOUR MONEY BETTER THAN A MUTUAL FUND MANAGER

-

Expenses – someone has to pay for that Ivy League manager’s paycheck, as well as the salaries of his analysts, traders and administrative assistants. And the company Christmas party doesn’t pay for itself. Neither do the electric bill, cleaning staff and all of the other costs associated with running a business.

While many managers do have their investors’ best interests in mind, they are still running a business. Bills have to be paid and profits have to be made. And the only way that happens is if they charge you for the privilege of letting them invest your money.

In 2011, equity fund investors paid an average of 0.79% worth of their positions in expenses to mutual funds. Note that figure is quite close to the difference between the average return for an equity mutual fund and the return of the S&P 500.

That 0.79% figure might not sound like much, but if you have a portfolio worth $200,000, you’re paying $1,580 per year in expenses. Over 10 years, that’s $15,800 worth of fees. (If the portfolio grows, you’ll pay even more.)

And that’s just an average fund. If you’re paying over 1% in expenses, you’re flushing even more money down the toilet.

Don’t forget some funds charge “loads,” or upfront fees. Often, if you’re using an investment advisor, you’ll pay an upfront fee of as much as 4.75%. That means if you give the advisor or fund $1,000, only $995.25 is invested on your behalf.

It’s going to be very tough to beat the averages starting nearly five percentage points down.

-

You can buy whatever you want. They can’t.

If you find a small stock that has big potential, you can buy a few thousand shares and see what happens. When you’re done, you can sell your shares with no problem.

A mutual fund manager doesn’t have that luxury.

With millions of dollars that need to be put to work, buying a small stock doesn’t make sense unless he can buy a ton of it.

But that fund manager can’t load up on a stock that only trades 100,000 shares a day without moving the price. It’s the same thing when he goes to sell it.

The individual investor has a lot more flexibility to acquire stocks that have the ability to outperform, while the fund manager is often stuck buying familiar names because they have the liquidity he needs.

-

No one cares more about your money than you. The fund manager’s goal is to make as much money as possible for you by December 31, because that’s when his performance is evaluated.

If he beats his benchmark, he gets a nice bonus. If he misses, there may be no big payout.

But you’re not concerned with December 31. Your focus is probably on April 5, 2015, September 21, 2027, or any other date you plan on retiring. Or perhaps you are already retired and you need consistent income or growth.

December 31 is meaningless to you except for deciding which friends to ring in the New Year with.

While the fund managers are trying to make money for their investors, you’re the one that knows your tolerance for risk, your goals and how to best handle your money. Don’t let someone else make those decisions for you.

GET SMART

With those ideas in mind, I beg you to learn as much as you can about investing so that you can handle your own money. After obtaining more knowledge, you may decide to use a portion of your money to try to beat the market and leave the rest in index funds.

Or maybe you’ll do as I consistently recommend and invest in Perpetual Dividend Raisers – stocks that raise their dividend every year. These stocks have an excellent track record of beating the market over the long term. And if you hold them for several years, the yield on your original investment will likely be substantial.

For example, let’s look at Middlesex Water Co. (Nasdaq: MSEX), a small water company that services New Jersey, Pennsylvania and Delaware. It’s a tiny stock, with a market cap of just $305 million and average daily trading volume of less than 30,000 shares. No fund manager could touch it without sending the price rocketing higher.

But the company has raised its dividend every year since President Nixon was in office.

Today it yields a respectable 3.9%. But if you had bought it 10 years ago, you’d be enjoying a yield of 6.4% due to the annual dividend hikes.

A mutual fund manager is probably not going to hold that stock for 10 years. Remember, he’s trying to post great numbers this year. The average tenure for a mutual fund manager is only four to five years. He knows he likely won’t be managing the same fund in 2023… when you’re looking to retire.

Your best chance at a wealthy retirement is to manage your investments yourself. You’ll save money, you’ll have more flexibility, and your money will be in good hands.

Click here to post a comment on WealthyRetirement.com.

© 2013 Wealthy Retirement. All Rights Reserved.

105 West Monument Street

Baltimore, MD 21201

North America: 1.800.992.0205; Fax: 1.410.223.2650

International: +1.410.223.2643; Fax: +1 410 223 2650

E-mail: WealthyRetirement@WealthyRetirement.com

Website: www.wealthyretirement.com

Keep the e-mails you value from falling into your spam folder. Whitelist Wealthy Retirement.

China’s New “Little Car”

This is not a joke and they do sell for $600.00. They won’t be able to make them fast enough–good just to run around town. Here’s a car that will get you back and forth to work on the cheap…$600 for the car.

Only a one seater however – Talk about cheap transportation…. Volkswagen’s $600 car gets 258 mpg. It looks like Ford, Chrysler and GM missed the boat again!

This $600.00 car is no toy and is ready to be released in China next year. The single seater aero car totes VW (Volkswagen) branding too. Volkswagen did a lot of very highly protected testing of this car in Germany, but it was not announced until now where the car would make its first appearance.

Volkswageb did a lot of very highly protected testing of this car in Germany, but it was not announced until now where the care would make its first appearance. The car was introduced at the VW stockholders meeting as the most economical car in the world. The initial objective of the prototype was to prove that 1 liter of fuel could deliver 100 kilometers of travel. And the Spartan interior doesn’t sacrifice safety.

The areo design prived essential to getting the desired result. The body is 3.37 meters long, just 1.25 meters wide and a little over a meter high. The prototype was made completely of carbon fiber and is not painted to save weight.

The power plant is a one cylinder diesel, positioned ahead of the rear axle and combined with an automatic shift controlled by a knob in the interior. Further Safety was not compromised as the impact and roll-over protection is comparable GT racing cars.The Most Economic Car in the World will be on sale next year: Better than Electric Car at 258 miles/gallon, this is a single-seat car. From conception to production took 3 years and the company is headquartered in Hamburg , Germany .

- The will be selling the car for 4000 Yaun, the equivalent of US $600.00.

- Gas Tank capacity is 1.7 gallons

- Top Speed is 74.6 Miles an hour

- Fuel efficiency is 258 miles per gallon

- Travel distance with a full tank is 404 miles

– Keith

Master Limited Partnerships Defined

Master Limited Partnerships Defined

By and large, master limited partnerships are just that – limited partnerships that happen to be highly liquid, and tradable on U.S. stock exchanges, just like traditional stocks.

Instead of shares, MLP’s offer investors “units,” and payouts aren’t called dividends, they’re called “distributions.” In essence, MLPs offer the tax advantages of limited partnerships with the asset growth benefit associated with common stocks.

Tax-wise, MLPs are treated differently from stocks and bonds, and are generally treated more favorably by the Internal Revenue Service. Taxes are paid by MLP unit-holders, on a pass-through basis.

That means MLPs, unlike common stocks, don’t face double taxation on distribution payouts to investors. However, non Americans (like Canadians, eh) do face double taxation—there is a withholding tax by Uncle Sam and they are not part of the Canada US tax treaty. All MLP investors should check with their tax accountants.

Master Limited Partnerships are often referred to as an “investor’s dream.” Why? Because some MLPs really do make that true – at least from a historical sense. Statistically, MLPs offer…

There’s no sure thing on Wall Street, but MLPs may be as close as a “sure thing” as possible. Since MLPs generally invest in relatively stable midstream energy companies – think pipelines, storage tanks, and oil and gas terminals – investors benefit from high demand for the services those midstream oil and gas companies provide. In other words, it doesn’t matter where the price of oil stands – $150 or $75 – as long as global consumers use oil and gas, MLPs benefit from that steady demand.

Master limited partnerships have proven resilient against down stock market cycles. In the immediate aftermath of the economic collapse of 2008, 39 of 50 MLPs actually raised their distributions to investors to, on average, 10%. In addition, as MLP’s invest in “high demand” midstream oil and gas companies, MLP’s provide investors with stable, reliable.

While MLP’s do offer stable, dependable yield growth, significant tax advantages, the tax situation is complicated, and you may need to bring in a tax advisor to handle the MLP portion of your investment/tax portfolio. In addition, exposure to small-cap oil and gas stocks – a common investment for MLPs – can lead to higher-than-normal volatility.

Some master limited partnerships are riskier than others. For example, larger pipeline MLPs are relatively stable – they generate a steady cash flow, as they’re not significantly impacted by oil and gas prices. Larger pipelines are also difficult to replace, making them more valuable for MLP investors.

That’s not the case for smaller pipelines that move natural gas from processing plants to suppliers. Since natural gas is more vulnerable to commodity price fluctuations, MLP investors should proceed with caution when it comes to evaluating various MLP investments.

According to the Interstate Natural Gas Association of America both the U.Ss and Canada will shell out an estimated $84 billion to build new midstream oil and gas platforms, pipelines, storage tanks, and other necessary infrastructure that meets the needs of skyrocketing domestic energy production.

That demand will generate big revenues to MLPs, who are expected to provide that entire infrastructure. In turn, those revenues should fatten up distributions, and boost MLP performance for years – and maybe even decades to come.

MLPs are exactly the product of the Wild, Wild West. In fact, the U.S. Security and Exchange Commission regulates MLPs, just like it regulates stocks. As a result, MLPs must file annual and quarterly reports, and keep investors apprised of any changes to its business model, and any developments that may impact the MLP. In addition, MLPs must also comply with the accounting requirements mandated by Sarbanes-Oxley.

What are the top reasons why regular, everyday investors are so attracted to MLP’s? Here are four big reasons why:

– Brian O’Connell, guest editor

Publisher’s Note: My top yield play for 2013 stems from a very simple premise: a sector that I strongly believe is best positioned to benefit from North America’s surging energy production. Click here to find out how I’m playing it for profit, and how you can as well.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair