Personal Finance

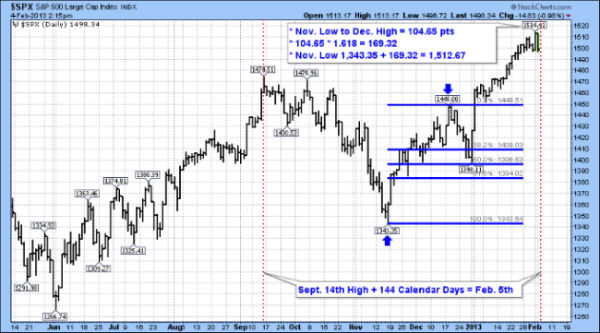

Back on November 19 we wrote a piece in our “Portfolio Manager’s Journal” that we felt the market was putting in an important low. Several technical indicators we were following at the time suggested that the post U.S. election sell-off had run it’s course. In particular, the NYSE Summation Index was at levels associated with previous market bottoms so the odds were stacking in favor of a significant rally. In hindsight our call was correct with the market trading higher and recording new recovery highs on Friday February 1st.

The rally has lasted more than two months, gaining almost 13% as measured by the performance of the S&P 500 Index. Now that the rally has unfolded as we anticipated we want to provide an update on the near-term outlook.

This week we are at an important juncture in terms of time and price with the odds now in favor of a short-term market top at current levels. We employ several different techniques in our market analysis, providing us with some interesting observations.

We like to use the Fibonacci number sequence to help us identify support and resistance price levels as well as projecting future time zones where we would be on the lookout for potential trend reversals. If we use the September 14th high and project out 144 calendar days the date for a potential turning point is Tuesday February 5th as indicated by the red dotted vertical dotted line on the chart.

The method for projecting the price target level involves taking the range between the November low and the December high. The range was 104.65 points. Next we multiply this value by the Fibonacci ratio of 1.618 which gives us a value of 169.32. If we then add this value to the November low of 1,343.35 we arrive at a price target of 1,512.67.

On Friday the market recorded an intraday high of 1,514.41 which is less than 2 points above out target!

Therefore with time and price at an important juncture we feel that the current rally is likely over for now and that we should expect a market correction to begin. Some other factors that support a price high is seasonality and sentiment. In post-election years the U.S. market tends to peak in the first week of February and decline into late March. In the past couple of weeks the bullish sentiment numbers indicate above average optimism and the bearish sentiment is also relatively low. From a contrarian perspective we interpret these numbers as another sign of a top.

Our current strategy is to hold off on any more buying until the market declines to an oversold level. We will be reviewing all our individual stock positions to identify stop loss levels in the event that the decline begins to accelerate on the downside.

The next six weeks should be choppy and volatile as those that came late to this rally become nervous and think twice about their recent purchases. We will provide another update when we feel that it’s safe to go back in the water!

- As Canadian consumers have increased their mortgage debt and bid up housing prices, the potential for a disorderly unwinding of these imbalances rightly concerns the Bank of Canada.

- PIMCO believes that the bank’s next policy move will be to raise interest rates, but with the traditional aim of fighting inflation rather than reducing home prices and consumer debt.

- We expect the Bank of Canada to continue tightening mortgage credit and using moral suasion to damp the housing boom and discourage consumers from taking on more debt.

What is the correct policy response to a prospective asset bubble? This question has been the focus of considerable academic research, especially since the financial crisis of 2008. Recent communication from the Bank of Canada (BoC) suggests it is considering hiking policy rates in response to the recent surge in household debt and home prices. If it does, this could represent a decisive change in its inflation-targeting strategy for monetary policy. At a minimum, it would get the attention of public policymakers worldwide owing to Bank of Canada Governor Mark Carney’s position as chair of the G20 Financial Stability Board (FSB).

……much more & 6 Charts HERE

- After a year cowering in the corner, are investors going all-in?

- Small-caps take a leadership role…

- Plus: a reader talks politics and Dow 40,000…

2012 featured more of the same from skittish investors.

They shunned risk. Instead, anyone interested in equities stuck to blue chips. Stocks paying a decent dividend received plenty of attention, while smaller companies were virtually ignored. Hesitant, fearful buying defined the collective attitude toward equities.

But something changed after the market began moving higher three months ago…

For most of 2012, small-caps and large stocks slogged through the ups and downs within spitting distance of each other. But since the market began to move off its November bottom, the Russell 2000 small-cap index has outpaced the Dow Jones Industrial Average by a wide margin…

Appetite for risk has abruptly changed. The Russell is up an impressive 18% since its November lows, while the Dow has risen about 11.5% during the same timeframe. Even as stocks consolidate this week, smaller names have not given up much ground to the big kids.

The last time we saw similar small-cap outperformance was in September 2010. In that case, a strong Russell helped propel a broad market rally lasting more than 10 months.

When investors show they are willing to take chances on some of the smaller, more volatile names on the market, stocks will continue higher.

Pay close attention to the Russell as stocks consolidate this week. If it fails to hold its ground, you’ll have an early signal to take profits…

Best,

Greg

Quotable

“I am suspicious of the idea of a new paradigm, to use that word, an entirely new structure of the economy.”

Paul A. Volcker

The US Dollar Reserve Status is in Jeopardy? Oh really!

Winston Churchill once quipped, “It has been said that democracy is the worst form of government except all the others that have been tried.” Granted, it would be a stretch to say the current global monetary regime is better than any that have been tried. But given the state of the global economy and dearth of global cooperation on matters large and small it seems a system that will be with us for quite a while…likely too long.

Many analysts wax nostalgic for the days of a gold-based monetary standard. Lamenting that if we had such a system today, all else good would follow. Granted, in its heyday, the gold standard served the globe quite well. But whether gold or wooden shoes or Coconut trees are used as a standard, the reason it succeeded was because central banks at the time, led by the Bank of England, took their jobs seriously.

By seriously, I mean central banks did not waver in their commitment to maintain a stable currency in reference to gold. If a recession was needed to bring currency balance back in line, a recession it was. And there was a major self-reinforcing benefit based on this seriousness. When there was a slight misalignment of values, i.e. gold was moving out of the country in the standard gold-specie regime, the market would actually bet on the central bank expecting them to bring the currency back in line, i.e. when central banks were serious the flows became positively self-reinforcing, thereby reducing volatility. Today, it seems the exactly the opposite.

Thus, the current environment helps to maximize volatility in currencies. No one out there expects central banks to be proper stewards of the currency—they have become bag men for irresponsible federal governments. It is all about this very nebulous and dangerous word called “stimulus.” So instead of forcing the market to clear by means of a sharp swift recession, setting the stage for fresh vibrant growth, our central bankers and their government handlers do all they can to prolong the crisis precisely because their primary goal is “full employment;” full employment of legacy assets owned by government cronies, fully employment of K-street, and full employment of voters beholden to big government. Is it any wonder the current monetary regime isn’t producing growth?

This doesn’t mean by virtue of the dollar as reserve currency it is bad. It does mean that irresponsibility by those in charge would likely destroy even the most elegantly designed system. But keep in mind that monetary systems in history were more evolutionary than revolutionary. It will likely be so in the future.

Maybe China’s growth remains on track. Maybe China’s political environment remains stable. Maybe the experiment with Dim Sum bonds in Hong Kong and other yuan-based derivatives usher in much more sophistication within the Chinese financial system. Maybe China opens its capital account and allows foreigners to hold the vast amounts of Chinese assets; a requirement part and parcel to a global reserve currency. If so, then expect the next evolution in global reserve status to be the yuan.

Granted, China is moving in the right direction to establish itself as global currency hegemon, but two things you shouldn’t expect: 1) for the Chinese currency to be the global reserve currency anytime soon; and 2) to ever return to a gold-based monetary system unless there is a 180-degree paradigm shift in government responsibility. Fat chance!

Euro: Is the top in? I think maybe could be it is.

We are likely now on to the next phase in the ongoing saga of the currency that was destined to supplant the US dollar as a reserve currency—the euro. Not saying there is no possibility of that happening, but not seeing a high probability.

The new phase will likely be characterized by more political bickering during a vital German election year, rising social unrest, the end of the big run in periphery bond prices (falling yields) and some major jawboning from European pols that shows indeed they are worried about the euro’s impact on growth (now that the ECB has “solved” the financial crisis).

Dateline: Wednesday, 6 February 2013

Source: Front page of the Financial Times

Headline: Hollande call for managed euro exchange rate draws German fire

“The euro should not fluctuate according to the mood of the markets,” the French president told the European parliament. A monetary zone must have and exchange rate policy. If not, it will be subjected to an exchange rate that does not reflect the real state of the economy.”

Translation from French to English (American version): The damn currency is too high! EUR/USD Daily: Correction complete? Maybe! I think you can guess which way we are playing this in our forex service.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair