Energy & Commodities

Wealth Maintenance and Creation in the “New” World. The coming Turn of the Tides will occur in the next 5 to 10 years as the dollar demise increases. You will have to learn how to handle investments in an entirely different way if you plan to create and maintian your wealth.

The Confluence of 4 Factors Dictates a MAJOR, NEAR-TERM TURN of the Tide

1. Demise of the U.S. Dollar, at least in its current role.

2. Government polarization and intrusion in the economy.

3. The post war evolution of American consumerism.

4. The digitally connected world driving lifestyle convergence.

…….read it all HERE

A cooling trend that has hovered over the real estate market for more than a year as the Teranet-National Bank index of Canadian housing prices continues to show.

….read more HERE

IMF says Canada’s housing market still overvalued, warns more intervention may be needed

“Our analysis suggests an overvaluation in real terms of about 10% at a national level, although with significant variations across provinces,” said Roberto Cardarelli, IMF mission chief for Canada, in comments provided as a complement to the technical report.

….read more HERE

Home costs take slightly smaller bite of household budget, but Vancouver still least affordable market

A new report says the cost of home ownership in most major Canadian markets was down slightly in the last three months of 2012 but notes that pressure on household budgets remains somewhat above the historical average.

“Home ownership costs came down for a second consecutive quarter as a share of household income thanks primarily to small declines in mortgage rates and home prices in several markets across the country,” the RBC report says.

…..read more HERE

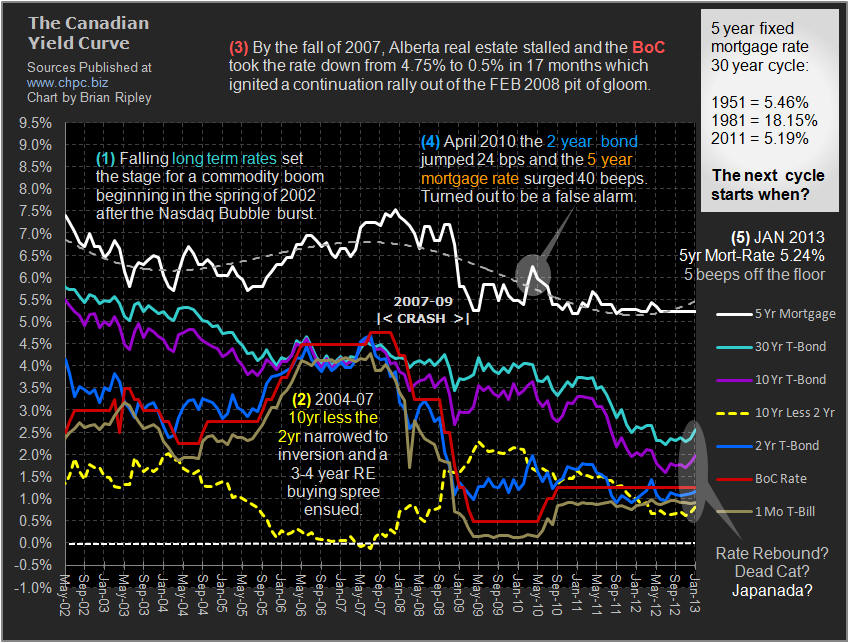

Interest Rates & Mortgage Rates at Lows

The chart above shows that in Janaury 2013 the spread between the Bank of Canada rate and the residential 5 year fixed mortgage remained unchanged as banks advertised the 5 year fixed mortgage rate at 5.24% and the BoC held its rate at 1.25% continuing to fix the cost of money and distorting market prices. The December CPI print remained at 0.8% so the short real rate also remained at 0.5%. Penny pinching ‘conservative‘ Canadian martyrs have been watching their savings evaporate while their fearless brethren have been all in for the big capital gain real estate flip. The Government policy of urging Canadians to borrow at low rates and spend at high cost (rather than promoting skill acquisition to become productive) has been a tax on savers and a short sighted policy; globally everyone is doing it, and it is not ending well. Look at Ireland, Spain and California (the list goes on). “ZIRP” could be the new normal and there is really no rush or panic to take on debt when asset prices are falling and rates remain boot suppressed. Notice how the TSX RE Index is correlating with the spread between the BoC and the 5 Year retail mortgage rate. If the spread between the BoC Rate and the 5 yr Mort-Rate widens as it did from April 2007 to Dec 2008, will the TSX Real Estate Index drop? Tension is mounting in the coiled spring as “real” rates continue to rise.

…..11 more Read Estate Charts HERE

How Close to the Final Bottom in Gold Are We?

Gold roller coaster seems to go on and on without an end. But what we saw last week was more of a bungee jumping. However, at this time there seems to be no more room for further declines, as major support lines have been reached already or are about to be reached. Does this mean that we are close to the final bottom and that a strong rally will emerge soon? Let us jump straight into the technical part of today’s essay to find out – we’ll start with the yellow metal’s long-term chart:

(click on chart for larger image)

The most interesting point in this chart is not that prices moved to the long-term support line and reversed but rather the current RSI level, based on weekly closing prices. It is the most oversold since the beginning of the bull market and is now more oversold than after the 2008 plunge.

This is a huge deal. Even based on the above alone, the bottom could be in for gold prices. Since the long-term support line has been reached, the medium-term bottom is probably in, and prices are likely to rally in the months ahead. It seems that perhaps a major top will be seen close to mid-2013.

Let’s see how the situation looks like from the non-USD perspective.

We continue to see a somewhat bullish picture here. Extensive consolidation has been seen after the 2012 breakout. Gold moved below the declining support line this week and while the situation looks a bit discouraging, we expect the recent breakdown to be invalidated – likely today. The support line currently in play has held declines for several months now with only one previous quick dip below it which was invalidated towards the end of 2012.

Now, let’s take the Canadian Dollar perspective which yields yet another encouraging analogy with 2008.

In this chart, we see that prices are now below the trading channel, much the same as was seen in 2008. That move was followed by a strong move to the upside, and with the situation heavily oversold here today, we expect prices to move back into the trading channel and rally sharply as we saw in 2008. Note the extremely oversold RSI levels – see the red arrows in our chart.

Finally, we would like to address one of our subscriber’s questions regarding a death cross technical formation on the gold market. Supposedly, it is a herald of doom for gold investors, but we would like to confront this belief with cold facts.

Q: Could you please address whether we need to be concerned about the recent golden death cross technical formation. Thanks.

Thanks for the daily market alerts! They are very helpful, especially during these trying times!

A: We discussed the death cross in gold in April, 2012 and here’s a quote:

Yes, we do have something to say about the death cross in the precious metals market. Something quite to-the-point:

It doesn’t work.

To be precise, in our opinion, it doesn’t work as signaling a good moment to sell gold or silver. Actually, in most cases it was a very reliable buy (!) signal. Here are the moments where the death cross was seen in gold during this bull market:

End of Q2 2004 – right after a major bottom and before a big rally (lower prices were never seen after that bottom); Mid-2005 – right before a major bottom and before a huge rally (lower prices were never seen after that bottom); Beginning of Q4 2006 – right after a major bottom (lower prices were never seen after that bottom); Q3 2008 – in the middle of the 2008 plunge.

Which of these four scenarios is the odd one? The last one marked neither a good buying point nor a good exit point – it was right in the middle of the extraordinary decline. In all other cases the death cross was a bullish development.

Summing up, 3 out of 4 cases where the death cross was seen were great moments to buy and the 4th one was neither a good nor bad moment to buy.

Therefore, the implications of a death cross are actually bullish.

In reality, gold did move lower in the weeks following the above comment despite the bullish impact of the death cross (it sounds weird, but that’s how it used to work), so we now have 3 out of 5 moments that were great times to buy gold, one average moment and one before a not-so-deep decline. It’s still not bearish.

By the way, please keep in mind that we have a search function on our website (top right part of the page) that works very well — it breaks the results into sections and can you can also filter them by dates. We will happily reply to questions in this section of updates and the Q&A Panel, but we are naturally not able to provide answers 24/7, and our search engine can do it instantly. You can try searching for “death cross” and you will find, for instance, similar comments for the silver market.

Summing up, support lines are in play for two out of three of this article’s gold charts and it’s likely that a local bottom has indeed formed. Additionally, RSI levels indicate an oversold situation. The outlook for gold from here is bullish.

Thank you for reading. Have a great and profitable week!

The stock market has been rising steadily since the Japanese inspired Key Turn Date of November 16…but doing so with a growing sense that a correction, at least, was due. We may have had another KTD this week (it’s too early to tell) when a number of markets reversed course on Wednesday triggered by the release of the Fed minutes.

Gold: dropped nearly $120 in 2 weeks, Silver was down $3. Base metals were down sharply this week. Precious Metals may have made a short term low this week. I covered a short gold position I have held for over a year.

Stocks: all major US stock indices moved higher early this week then reversed on Wednesday/Thursday. As of mid-morning Friday all indices look to have made Key Weekly Reversals.

Energy: Brent and WTI both made multi-month highs last week…faded…then broke more than $5BBL starting Wednesday.

Currency: The US$ rallied Vs. all major currencies (save the Yen) on the Fed minutes. The 18% drop in the Yen Vs. the USD since mid-November appears to have stalled. PM Abe is meeting Obama and is expected to announce the new head of BOJ next week. The Yen could move on the announcement. Last week I established option positions looking for an end to Yen weakness as well as a drop in Yen option VOL.

Interest rates: Bonds rallied to their best levels in a month following the release of the Fed minutes…even though a change in Fed policy would likely see the Fed buying fewer bonds.

I’ve asked a number of times, “What are we trading?” and my best answer has been, “Central Bank policies.” David Rosenberg notes the correlation between the S+P and the Fed balance sheet is 85%. Currency markets have been responding to relative central bank policies with talk of currency wars all over the media….so…the hint of a slight change in Fed policy within the minutes released Wednesday was significant.

Market Psychology has been increasingly “What Me?….Worry?” kind of bullishness since mid-November. Witness the 5 year plus lows in VIX, new all-time highs in the mid-cap Russell 2000, the NZD trading at an 8 year high Vs. CAD. It seems as though market relationships had left “risk on / risk off” behind and were reacting to individual market fundamentals…then suddenly, on Wednesday, correlations went to ONE in a “risk off” mode with the USD and Yen higher, all other currencies lower, stocks and commodities down and bonds up. If we did indeed have a Key Turn Date then Market Psychology may return to a binary “risk on / risk off” world.

Futures markets provide an efficient and effective way to trade a wide range of financial markets. If you would like to speak to a broker to discuss the aforementioned markets or about trading in the futures market please call 604-664-2842.

Victor

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair