Bonds & Interest Rates

FULL BLOWN JAPAN CRISIS

FULL BLOWN JAPAN CRISIS

Kyle Bass became well-known after successfully predicting and benefitting from the subprime mortgage crisis and his prediction of the European sovereign-debt crisis.

You can pay attention to how this man is positioning himself in this thorough article HERE

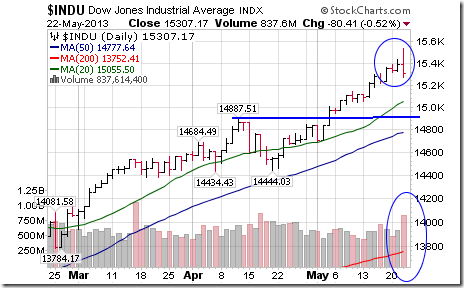

U.S. equity indices recorded a classic key reversal sell patterns yesterday. A classic key reversal sell pattern includes opening above the previous day’s close, moving higher than the previous day’s trading range, closing lower than the previous day’s close and moving lower than the previous day’s trading range. Higher volume is a confirming indicator.

Key reversal sell signals for equity indices are rare. When they happen, they usually are a reliable indicator that equity markets are about to move lower in the short term. U.S. equity indices could easily fall back to break out levels that occurred on May 3rd when the last monthly employment report was released.

Trigger for the key reversals was news that the Federal Reserve is considering the possibility of reducing the size of its Quantitative Easing program as early as June. That means the Federal Reserve will purchase fewer Treasuries and Mortgage Backed Securities. As expected bond prices also responded strongly to the downside on the news.

The VIX Index spiked on the news.

The U.S. Dollar move higher and the Canadian Dollar virtually collapsed on the news.

Economic sensitive sectors were notably under pressure. Their performance relative to the S&P 500 Index has started to deteriorate, a typical seasonal pattern at this time of year. Note that all charts below also recorded negative key reversal patterns.

Not all markets and sectors moved lower yesterday. Notable strength was recorded by the Russian ETF and the Grain ETN. The latter is being influenced by problems with planting the grain crop on a timely basis due to weather (cold spring, tornado season)

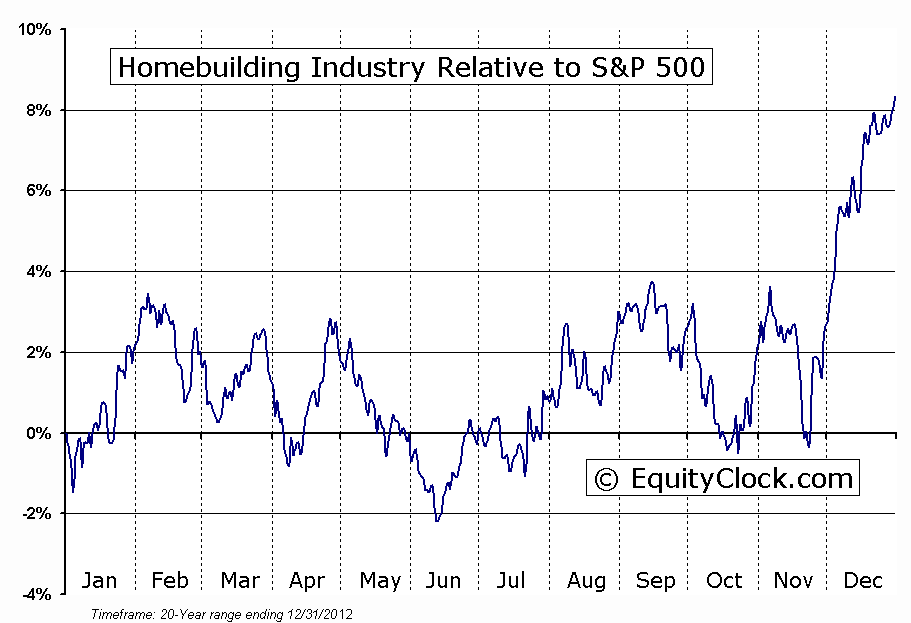

Special Free Services available through www.equityclock.com

Equityclock.com is offering free access to a data base showing seasonal studies on individual stocks and sectors. The data base holds seasonality studies on over 1000 big and moderate cap securities and indices. Notice that most of the seasonality charts have been updated recently.

To login, simply go to http://www.equityclock.com/charts/

Following is an example:

S5HOME INDEX Relative to the S&P 500

As anyone knows who has tried in whatever way to opine on the financial markets, sometimes three of the most important words in the English language are the following, “I was wrong.” The second most important three words are “I don’t know.” There are several reasons why I say this, but the most important one is that having lived through the 2008 financial crisis I can absolutely tell you that everyone from investment bank heads, CEOs of major corporations, to popular TV financial prognosticators, on down to private speculators and broker dealers in general did not see the crisis coming and took a bath on investments. Even the brightest minds get things wrong. And don’t get me started on central planners, who often never seem to be able to see asset bubbles coming, or to even know how to safely deflate said bubbles if they could see them coming.

As anyone knows who has tried in whatever way to opine on the financial markets, sometimes three of the most important words in the English language are the following, “I was wrong.” The second most important three words are “I don’t know.” There are several reasons why I say this, but the most important one is that having lived through the 2008 financial crisis I can absolutely tell you that everyone from investment bank heads, CEOs of major corporations, to popular TV financial prognosticators, on down to private speculators and broker dealers in general did not see the crisis coming and took a bath on investments. Even the brightest minds get things wrong. And don’t get me started on central planners, who often never seem to be able to see asset bubbles coming, or to even know how to safely deflate said bubbles if they could see them coming.

In short, the most important lesson of the financial crisis may have been that oftentimes there are no experts, and that sometimes no one is in charge. I don’t mean to be negative in saying this- quite the opposite. It is meant to be empowering.

Oftentimes the big boys and gals get themselves in trouble with their 8 or 9 figure accounts, they are forced to liquidate, and do so without regard to fundamentals. Or put differently, these people are human beings after all who are caught up in the cycles of greed and fear– they are not superhuman, they are not above panicking. These “professionals” seem to act just as unprofessionally as retail investors– sometimes even more so. Its just that the consequences of their actions are felt more powerfully, look larger, and seem more ominous than when John Q. Public gets in trouble with his more meager holdings. But don’t let the carnage brought about by professional liquidation lead you to believe that a sector is permanently done for. Just ask investors at the bottom in March 2009 regarding many financial service industry stocks, for example. Although bottoming is a process, we are clearly at this kind of professional liquidation stage in the precious metal miners, and regardless of the price of metals, you can do quite well with these stocks in the years ahead.

We hear many valid objections to owning mining stocks. Those who only buy gold and silver bullion don’t want the risk involved in a mere paper asset. Others who have followed the cost management (or lack thereof) in the mining industry over these past five years believe that the miners will never get their act together and will never provide meaningful profits for investors. They believe that the mining companies are incapable of learning lessons about cost overruns, or from unrealistic expectations concerning mine acquisitions. Investors think that the miners can’t adapt the way other business owners can.

Couple this with the apparent belief that the bull market for precious metals prices is over, that a new era of nationalizations is upon us and can’t be avoided globally, and you get sentiment readings like the one we see today (and also saw last month). The percent bulls for the Gold Miners ($BPGDM) is at zero. Yes, you read that correctly— zero.

We have been here before, in late 2008. And I hope you know where the miners went from there. I also hope you understand that markets always look broken at the bottom, and that, as Alexander the Great is supposed to have said, “fortune belongs to the bold.”

…more comments from Ryan HERE

Ed Note: With metal mining stocks grinding around at the bottom, names are what you need for investing/speculating. Gregory Weldon’s trend tracker is brilliant. You can get a FREE trial HERE

Stocks, bonds – everything – at risk

Stocks, bonds – everything – at risk

As the global equity and bond markets grind ever higher, abundant signs exist that we are once again living through an asset bubble – or rather a whole series of bubbles in a variety of markets. This makes this period quite interesting, but also quite dangerous.

With equity and bond markets at or near all-time record highs, with all financial assets consistently shrugging off bad – or worse – news as the riskiest of assets continue to find consistent upward bids, we find ourselves in familiar and bubbly territory.

I can summarize my thoughts in one sentence: How could this be happening again so soon?

In times past, it took one or more generations between bubbles for people to financially recover and forget the painful lessons before they would consider doing it all again. Yet here we are, working our way through our third set of bubbles in less than two decades, which must be some sort of world record.

I will confess to my biases right up front: I have always been deeply skeptical of both the practice of running up debts at a faster pace than income (the common practice of the entire developed world over the past several decades) and the idea that the solution to too much debt is more debt, enabled by cheaper money courtesy of thin-air money printing.

In short, instead of seeing central banks as sophisticated stewards of intricate monetary policies, I view them as serial bubble-blowers and reckless debt-enablers whose only response, when confronted with the inevitable consequences of their actions, is to serve up more thin-air money at an even cheaper rate. And when that doesn’t work, then they simply try even more of the same, but in larger quantities.

While I think central banks are populated by earnest people with impressive credentials who have rationalized their actions as being necessary and in service of the greater good, I also think that the biggest ones hold an entrenched set of institutional views that are dogmatic, fail to incorporate the idea of economic and resource limits, and are seemingly immune to healthy introspection.

Somewhere along the way, I would have hoped they might have noted that each new crisis is larger than the one before – necessitating an even larger response that begets an even larger crisis next time, etc., and so on. A corporate bond hiccup in 1994 led to monetary loosening that enabled the development of the Long Term Capital Management (LTCM) fiasco of 1998, which was followed by the tech bubble, and then the housing bubble, and here we are with a now global equity and bond bubble that is larger than all the prior bubbles combined. Much larger.

It was famously said that the market can remain irrational longer than you can remain solvent. And if the trading maxim, don’t fight the Fed, is worth heeding, then surely one should absolutely not take on all of the central banks at once, either. So, the risk I run here in seeing things through my ‘common sense’ filter is that perhaps this time the Fed, et al., have got it right, and a true and lasting recovery is at hand.

With that caveat, in this report I lay out the five most worrisome signs that horrific market losses await the unwary, the careless, the reckless – and those who possess all three characteristics (i.e., your average central bank).

These are not normal times. The degree of separation between reality and today’s financial markets is extreme, which means they have a tremendous degree of potential energy stored up that could erupt in a downward cascade at any time.

While we can’t predict the exact time or trigger of a market avalanche back down to reasonable levels, I can definitely advise that you do not want to be standing in the valley when it happens.

Four Signs That We’re Bubbling

HERE are the four things including charts that convince me that we are in truly bubbly territory:

With S&P 500 is hitting new highs, and gold and silver are sitting roughly at two-year lows, it’s ususally good to listen to what these two old guy’s have to say:

Richard Russell on May 17, 2013:

Richard Russell on May 17, 2013:

“The CPI is manipulated, and I believe gold is being manipulated as well. The Fed’s QE4ever is inflating everything — school tuition, haircuts, food, gas, insurance, medicine. They’ve already “rearranged” the CPI, so what’s left for them to do to keep us from knowing about inflation? Oh yes, it’s gold, so c’mon, Bernanke, keep the lid on gold. Slam it in after-market trading in the thin paper-gold markets of the night.

I promise you, when the true forces of inflation finally break loose, the Fed won’t be able to disguise what they’ve wrought. When the true forces break out — it will be a national disgrace and an emergency. ‘Then you will know the truth, and the truth will set you free.’ The rest of this year should be something to behold.”

Jim Rogers to MoneyNews on May 19, 2013:

Jim Rogers to MoneyNews on May 19, 2013:

“Right now, we have a very artificial situation. You have the central bank in America printing staggering amounts of money,” he tells Newsmax TV in an exclusive interview.

“There’s this gigantic artificial flow of money floating into our economy, and this is going to end badly because it is artificial.”

“It seems that Mr. Bernanke may be leaving in a few months,” Rogers says. “I guess he wants to get out before he has to deal with the hangover or the aftermath.” Bernanke’s term ends Jan. 31, 2014, and the consensus opinion is that he doesn’t want to serve another.

But as far as the Fed’s easing tactics are concerned, Rogers doesn’t see a smooth conclusion on the horizon.

“I don’t know how long it will last,” Rogers says. “I don’t see how it can last much more beyond this year.”

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair