Stocks & Equities

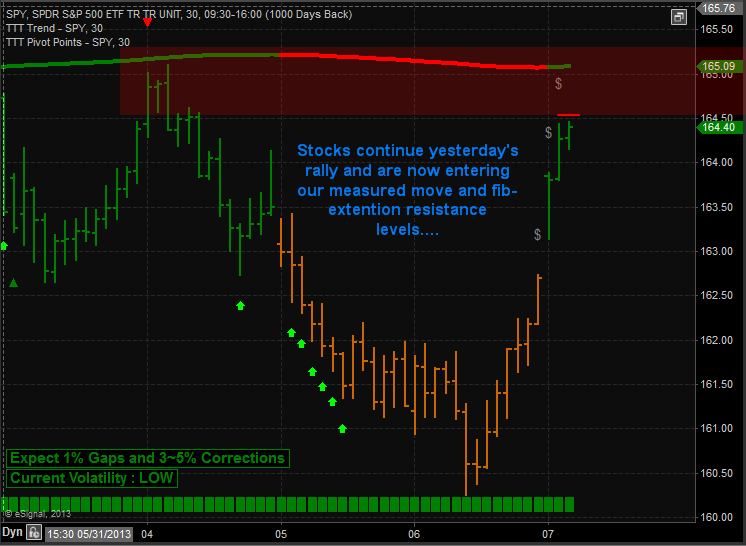

This week has played out perfectly thus far. The expected volatility of intraday price swings and lower prices for stocks has happened. The Vix has collapsed the 15% which I mentioned would happen just 2 days ago and money is flowing out of precious metals and miners today in a big way as that risk off money is now moving into Risk-On Stocks.

My partner who focuses exclusively on Small Cap Stocks and 3X Leveraged ETF’s have been cleaning up this week also. Take a look at how he How We Nailed The Market Low for 4.6% in 24 hours

I just want to mention that all markets are connected (intermarket analysis) We are long the SP500 which is how I want to play this move because it carries the least amount of risk and volatility then other investments. That being said a trade could instead short gold or short the vix. Many ways to play moves like this in the market. One thing to remember though is that each of these moves are the same trade. so buying a position in each is just multiplying your exposure and if this bottom in stocks didn’t take place you would get your head handed to you on a silver platter. Again I am here for market guidance and to share low risk setups as I see fit. You can trade all you want around analysis as many of you do on your own.

Charts Show it all in Detail below:

WATCH TODAY’S VIDEO FOR FULL EXPLANATION: HTTP://YOUTU.BE/PRLXPTFDWXI

GET THIS TYPE OF ANALYSIS MULTIPLE TIMER EACH TRADING DAY DELIVERED TO YOUR INBOX!

Chris Vermeulen

“The eurozone is already in a Japan-trap … What we are seeing in the money supply data and falling monetary velocity is exactly what happened in Japan in the 1990s, yet the ECB seems to think everything is fine.”

-Lars Christensen, Danske Bank

Wait for it … wait for it … Draghi will “save the day” eventually …

Greetings!

The driver of the euro has changed a bit in recent months. Certainly expectations have.

Traders now expect the European Central Bank’s new efforts to support its economies with ultra-easy monetary policy will drive yields lower. And this narrowing yield differential between the US and Europe will weigh on the common currency.

Remember, before, action from the ECB to support economies was seen as alleviating a Sovereign debt problem, reducing pressure on economies and leading the way to growth; and that was bullish for the euro.

Not anymore …

Currency Currents 7 June 2013

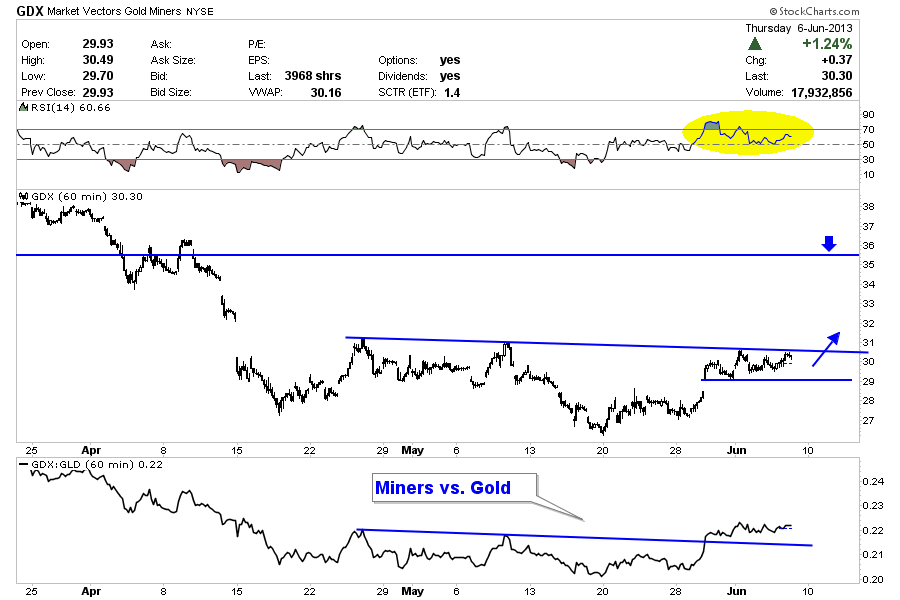

Though we’ve anticipated this rebound since late spring (albeit way too early), it is just about here and will pay big rewards to those who are long. A few weeks ago we wrote 6 Reasons why Gold Stocks will Begin a Big Rally. Since then, the action has been increasingly positive. In four of the past seven days, GDX closed near the high of the day and formed a strong white candle. In the other three days GDX closed well off the lows of the day. The action of the past seven sessions is a sign of accumulation. During these days the sector has performed well in the last 30 minutes of trading (which is when the smart money is most active). We will explain why we are even more confident that a big rally is days away from beginning and why it could continue until late September.

GDX’s price action appears to show a developing reverse head and shoulders bottom. If GDX closes above $31 then it brings a potential target of $35.50 into play. Aside from the bullish price action there are two other important points. Note that the hourly RSI is acting bullish for the first time in many months (yellow). The RSI pierced 70 to the upside and is holding in bullish territory while the market consolidates. Also, the miners have been outperforming Gold. The stocks lead the commodity at key turning points. Gold has struggled to break free but the fact that miners are showing more strength is encouraging for the entire sector.

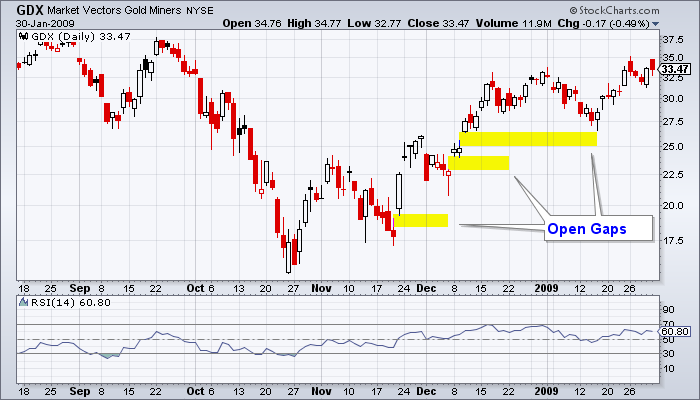

Six days ago the miners gapped up and the majority of the sector (as well as GDX, GDXJ, SIL continues to hold the gap. Checking back to 2008, (chart below) we find that GDX gapped up many times and left three open gaps that were never filled. Two of these gaps occurred immediately after higher lows. The gap from six days ago occurred less than 48 hours following a higher low.

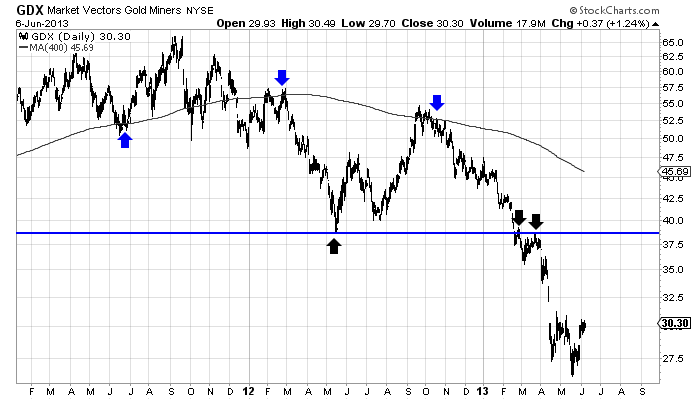

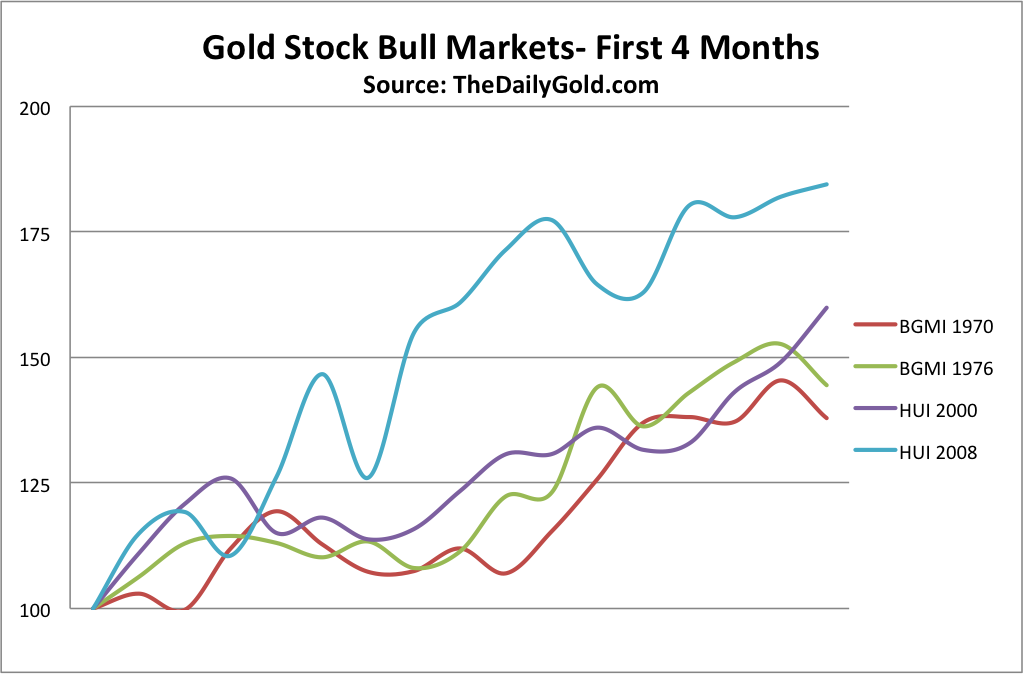

In studying history, we found that following four major bottoms (1969-1970, 1976, 2000, 2008) gold stocks rallied back to the 400-day moving average in an average time of roughly 4.25 months. Currently, GDX has strong resistance at $39, its 38% retracement of the 2011-2013 bear is at $41 and the 400-day moving average is at $45.70 and falling. Four months from now the 400-day moving average should be below $42. In any event, the $39-$41 region is setting up as a potential strong target following the aforementioned $35.50.

If GDX reaches $39 by October then that is a 50% rebound in less than five months. History suggests this is not extreme. In the chart below (which uses weekly data) we show the performance of the gold stocks following their most oversold points within the two secular bull markets. The biggest rebounds followed the 2000 and 2008 lows. Note that the rebounds accelerated in earnest about five weeks after the bottom.

Traders should use the low in late May (on GDX & GDXJ) as a stop.

Some may decry our analysis because Gold has yet to break $1420 and Silver has yet to break $23. At market extremes and turning points its best to focus on the stocks as they are the “tell” for the sector and the commodity. We are aware that there are huge short positions in Gold and the unwinding of those positions will add further fuel to the rebound in both the metals and the shares.

Furthermore, a fall in the S&P 500 will not affect this rebound. It will actually help. Since September 6, 2011 the S&P 500 is up 40.6% while GDX is down 53.3%, Silver is down 45.7% and Gold is down 24.0%. There is a clear long-term negative correlation between equities and precious metals. This was also the case from 1972 to 1977 before Gold accelerated into its bubble phase and from 2001-2002. Precious metals can and will perform well when the S&P corrects or goes sideways.

It’s been a tough road for precious metals but the path ahead has strong potential of being significantly profitable and in a short period of time. The buying opportunity that we’ve spoken of for months is now here. When precious metals equities rebound, they rebound violently. If you’d be interested in our analysis on the companies poised to recover now and lead the next bull market, we invite you to learn more about our service.

Good Luck!

Jordan Roy-Byrne, CMT

“This is the end of a 30-year rally”

In a speech to Toronto reporters tuesday, Federal Reserve Bank of Dallas President Richard Fisher did something surprising when he actually declared a market rally over!

In a speech to Toronto reporters tuesday, Federal Reserve Bank of Dallas President Richard Fisher did something surprising when he actually declared a market rally over!

His agressive warnings continued when he stated that the current Fed’s $85-billion-a-month bond buying program risks:

“debasement” of the dollar

high inflation

“the ruination of our economy and lifestyle”

As for describing the effectiveness of the Fed’s program, Fisher pulled no punches:

“the Fed is at best pushing on a string and at worst building up kindling for speculation and eventually, a massive shipboard fire of inflation”

Fisher has repeatedly said the Fed’s current QE3 quantitative easing has done little to boost the economy and could do it harm. Fisher is not alone in his opposition to the Fed’s QE3 bond-buying program either. It is gaining some other opponents recently within the Fed:

Last week the very highly regarded Paul Volcker, former Fed chairman from 1979 to 1987, sounded a warning on QE3, saying that central banks are often too late in removing stimulus.

San Francisco Fed President John Williams said he is open to cutting the central bank’s bond-buying program over coming months. He joined two other regional Fed presidents – the Philadelphia Fed’s Charles Plosser and the Richmond Fed’s Jeffrey Lacker – who have also called for phasing out the Fed’s monthly purchases of mortgage-backed securities .

While Fed chairman Ben Bernanke has said he’s open to the idea of reducing bond purchases, he first needs to see additional signs of a stronger economy. One indicator of that health will come out this Friday when the federal government releases its May employment and unemployment data.

Ed Note: Fisher is not a voting member of the Fed’s policy-making committee this year.

“At some point secular markets change” was the statement made by Federal Reserve Bank of Dallas President Richard Fisher in Toronto on Tuesday. “This is the end of a 30-year rally” in bonds he emphasized, making it doubly clear he didn’t see just this as a short-term top.

With a Federal Reserve Official broadcasting point blank that interest rates are going up, and that the BIG BOND RALLY that has been raging for 30 years is now over, institutional investors world wide are probably taking that as a signal to agressively review and make moves in holdings they have in fixed income instruments.

One person who tracks Institutional Investors is Sasha Cekerevac. Here is what he had to say:

Institutions Already Shifting Their Investments; Should Investors Follow Suit?

by Sasha Cekerevac for Investment Contrarians

Recently, I’ve issued several warnings in these pages for investors who are heavily involved in fixed-income assets. As I’ve mentioned over the past couple of months, I think the worst investment for investors to make is to put a lot of money into long-term Treasury bonds and notes.

This is because the unprecedented level of quantitative easing by the Federal Reserve will not go on forever. Once this shift occurs—the Federal Reserve beginning to reduce its aggressive quantitative easing program by decreasing monthly asset purchases—I believe it will hit the bond market quite hard.

I am not alone in this analysis, as recently the Federal Reserve Bank of Dallas President, Richard Fisher, stated that he too believes the multi-decade bull run in the bond market is over. (Source: Ito, A., et al., “Fed’s Fisher Urges QE Reduction Seeing End to Bond Rally,” Bloomberg, June 5, 2013.)

As Fisher stated, “The one thing the market has begun to discount is that this will not go on forever.” (Source: Ibid.) Large institutions are beginning to shift their investments ahead of adjustments in the quantitative easing program by the Federal Reserve, and you should consider this too.

Featured below is the chart for the 10-Year U.S. Treasury Yield Index:

Even before the Federal Reserve has officially stated it will begin reducing quantitative easing, investors have already begun shifting assets out of the fixed-income market, as I thought they would. The 10-year Treasury note has moved up in yield from 1.63% in May to 2.14% currently.

While this is a substantial move upward over a short period of time, when one looks back over the past few years, there is still a lot of room for yields to move up and for fixed-income asset prices to go down.

While I don’t see the Federal Reserve reducing quantitative easing over the next month, as some are forecasting, I do see the Federal Reserve reducing its asset purchase program by the end of the year.

So, what does all of this mean?

Many parts of the economy that have benefited from the low interest rate policy enacted by the Federal Reserve through quantitative easing will now see headwinds.

Both the housing market and vehicle sales have performed extremely well over the past year, but as interest rates begin to move up, this will cause a slight drag in these sectors.

When interest rates move up, it creates an affordability issue. It’s a fine balancing act for the Federal Reserve to adjust quantitative easing to help the economy without giving it too much gas. Historically, the Federal Reserve has erred on the side of too much quantitative easing rather than too little.

Considering that many of the stocks that have benefited from the current quantitative easing policy by the Federal Reserve have gone up a huge amount—homebuilding stocks included—I would certainly look to take profits.

Homebuilding stocks have gone up a huge amount over the past few years. For them to sustain their current valuations, the growth rate needs to remain at extremely high levels. I think with higher interest rates moving upward, this will cause investors to pause when calculating their forecast for future sales and revenues.

Obviously, with the Federal Reserve beginning to reduce quantitative easing by tapering and eventually eliminating its asset purchase program, this will be a negative for the fixed-income market. As I’ve written over the past couple months, owning long-term Treasury notes and bonds is a huge mistake. It appears we are now witnessing just the beginning of what will happen when the Federal Reserve begins to shift its quantitative easing program.

We believe the stock market and the economy have been propped up since 2009 by artificially low interest rates, never-ending government borrowing and an unprecedented expansion of our money supply. The “official” unemployment numbers do not reflect people who have given up looking for work. The “official” inflation numbers are way off reality. After a 25-year down cycle in interest rates, we believe rapid inflation caused by huge government debt and money printing will start us on a new cycle of rising interest rates.

Investment Contrarians is our daily financial e-letter dedicated to helping investors make money by going against the “herd mentality.”

When everyone was getting out of gold bullion in 2002 at $300 an ounce, we recommended getting in.

When the housing market peaked in 2006, we were telling our readers to get out.

When the Dow Jones Industrial Average hit 14,000 in 2007, we told our readers stocks were at a top.

And when the Dow Jones Industrial Average fell to 6,400 in March of 2009, and the majority of investors were bailing from stocks, we told our readers to jump in with both feet!

Investment Contrarians provides independent and unbiased research. We are independent analysts that love to research and comment on the economy and the stock market. We make money when a reader of Investment Contrarians purchases one of our many paid-for financial advisories. Our parent company, Lombardi Publishing Corporation, has been in business since 1986.

You can learn more about the editors of Investment Contrarians, here.

JOIN US TODAY! You’ll quickly see why thousands of investors look to Investment Contrarians daily to help them with their investment decisions.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair