Timing & trends

The speculative community has crushed the gold and silver price in the second quarter of this year. From a short term price perspective, the outlook for gold and silver is not too bright. On the other hand, investors who own the metal in PHYSICAL form (acting as their own central bank) have an ideal hedge against the increasing counterparty risk.

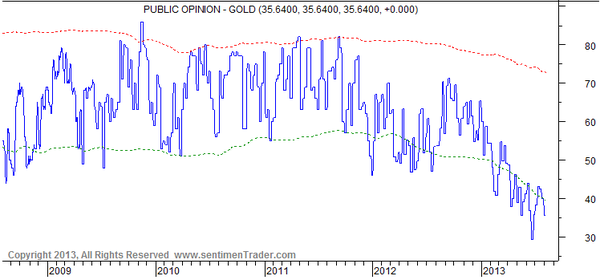

This week’s COT report (first chart gold’s report) provides an insight in the outlook of the precious metals. The COT report shows the futures positions of commercials and speculators. Their positions are important because those “paper markets” (COMEX and LBMA as the most significant ones) continue to dominate the price setting. Speculators include hedge funds in the “managed money” category in the reports.

The chart shows that large speculators keep on increasing their net short position in gold while the commercials keep extending their net long position. Commercials are known for seducing speculators in one direction while simultaneously changing their own positions. Nevertheless, speculators have been in control over the past months with aggressive short bets. Besides, some analysts argue that the rise in long positions of commercials is due to hedging of gold miners, a common practice during gold’s bear market in the 90’s. It would imply that sentiment among speculators will be an important driver of precious metals prices going forward.

According to the latest Sentimentrader data, the sentiment vis-à-vis the metals remains at extreme levels. From a contrarian point of view, it could be interpreted as positive. But given the recent correlation between sentiment and prices, it is likely a bearish factor short and mid-term.

What is at the basis of this sentiment? In order to understand the arguments of the bears, it suffices to turn on a mainstream media channel. A recent commentary from a Wall Street pro on CNBC, Mr. Scaramucci, showed four reasons why hedge funds could continue to push the gold (and silver) price lower.

When analyzing the bearish arguments, we figured that every argument can basically be reversed to become a valid counter-argument. Why? In our opinion, it all depends on the time horizon and the fundamental difference between investing and trading. The following high level analysis makes our point clear.

Please note that our point is not to criticize trading. We just point to the fundamental difference between trading and investing. Traders do not necessarily take decisions based on fundamental grounds. Also, traders have a benefit in the fractional and leveraged system, which is the reason why they will never mention the monetary benefits of physical precious metals.

Bearish argument 1: Central bankers are exercising caution

The first point is related to inflation. It touches the most known benefit of gold, which is a hedge against inflation. The following quote comes from the CNBC interview:

“There’s a lot of very wealthy people that are going to own gold as a defensive hedge for what they’re fearing is that whole Weimar Republic thing, where either the Europeans or the United States aggressively prints money, where the multiplier effect kicks in on the banking side, and you get this out-of-control inflation,” Scaramucci said, referring to hyperinflation that occurred under the German democratic system in place between 1919 and 1933.

But Scaramucci says these gold bugs just aren’t doing their research. “If you read the minutes from the Federal Reserve, or if you look at the essays that Ben Bernanke just recently published, you will discover that your central bankers, particularly in the United States, understand this issue very well. And that’s one of the main reasons that gold has not worked in this environment.” The Fed minutes make clear that the Fed is keeping a close eye on inflation, and is keeping risk factors in mind. For instance, the latest Fed meeting minutes, from the July 18-19 meeting, note: “Although the staff saw the outlook for inflation as uncertain, the risks were viewed as balance and not particularly high.”

The obvious counter-argument?

The underlying assumption in the above statement is that the US central bank is kind of omnipotent. But what if that is not true and their policy will not bring the desired results? After all, they cannot justify their policy based on empirical results as the current money experiment is unprecedented in its scope and scale.

The fact is that the US is currently exporting their (monetary) inflation. Lots of the newly created dollars end up at foreign central banks rendering abroad currencies weaker. That is why the dollar is increasingly bypassed through trading agreement particularly by the BRICS (as we reported here, here, and here). Going forward, one should not exclude a scenario in which inflation stays within the US and price inflation picks up fast.

True, it is not visible on the horizon yet. But it is a looming risk which can materialize rather fast. History learns that inflation remains invisible longer than most expect but picks up faster than expected.

Bearish argument 2: Deflation has become a risk

The second point is related to disinflationary signs from the global economy which could, ultimately, lead to deflation. From the interview:

“What’s happening now is the specter of deflation is way, way, way more fearful to the central banking community than inflation,” Scaramucci said, “and gold typically works when there’s a devaluation of currency, or inflation.” As the Federal Open Market Committee noted in its July 31 statement: “inflation persistently below its 2 percent objective could pose risks to economic performance.” “In a deflation economy,” Scaramucci said, “gold is not going to work.”

The obvious counter-argument?

Central banks are scared to death about deflation. Japan’s fear for deflation resulted in the biggest monetary stimulus in history, beating helicopter Ben. What if central bank’s policies get out of control in their attempt to defeat deflation?

From another point of view, let’s assume that Western central banks will allow deflation. In such a scenario, gold will go down, but history has shown that it goes down to a LESSER extent than other assets (see Exeter’s pyramid). In such an environment, physical gold offers protection in a decline of purchasing power.

Bearish argument 3: The Fed won’t sell its bonds

The third point is related to the risk that the bond bubble will burst. From the interview:

“People are buying gold because they predict there’s a bond bubble,” he said. “And they predict that, at some point, the Fed is going to shed their $3.9 trillion balance sheet. But that’s not going to happen either.” He believes this incentive for the Fed to sell its bonds simply isn’t there. “The Fed’s duration on its balance sheet is only about seven years,” Scaramucci said. But “they’re a 100-year-old institution, they live inside a 237-year-old country, and there’s no reason to shed that portfolio. They’ll just let their portfolio unwind. And so the prediction here will be that gold prices will languish.”

The obvious counter-argument?

The US Fed is the most important buyer of domestic bonds. What if the market loses trust and pushes yields much higher, to such an extent that the Fed cannot control their own interventions? Higher bond yields (and hence lower bond prices) started to “spiral out of control” since May of this year. The US Fed’s chairman reaction on that was: “it got us puzzled.”

Longer term, our belief is that distorted markets because of central bank intervention will react violently. The precious metals selloff this year was due to the investing community’s perception of relative asset performance. Precious metals were simply the first shot across the board. With looming inflation and dollar debasement, precious metals will be back in favor longer term. That’s when a major price rise will be likely, at a comparable pace as the recent decline. Likewise, we expect other assets to be sold off hard as soon as they will fall out of grace.

Bearish argument 4: Economic growth would hurt gold

The fourth point is related to additional monetary easing as a response on economic growth.

To Scaramucci, holding gold has become a lose-lose proposition. “If the economy picks up, rates pick up, that’s bad for gold. If the economy doesn’t pick up, the Fed is going to be in exactly the position that it’s in now, which is effectively QE but no real money creation.” Simply put, while people thought quantitative easing would create gold-boosting mega-inflation, that simply hasn’t happened. So now, the risk remains to the downside—because rising rates make gold, which does not produce yield, even less attractive in comparison to bonds.

The obvious counter-argument?

On one hand, the gold price has risen between 2001 and 2008 without quantitative easing and with much higher interest rates as today. On the other hand, quantitative easing is about currency debasement, which is happening all around the world right now. The epicenter is in Japan and the US. The dollar is the best of all bad currencies.

The rationale for investing in (physical) gold is related to the monetary protection against the debasement of money.

Also, every marginal unit of economic growth needs an increasing number of units of debt. The effectiveness of debt is at all time lows. So more debt is needed to keep the economy going, not growing. That points to a continuation of the dilution of the value of money.

Conclusion

While the bearish arguments do make sense from a trader’s point of view in the short to mid-term, they do not take into account the fundamental monetary benefits of gold and the violent message of heavily distorted markets. The monetary crisis and financial turmoil in a centrally managed economy are starting to show their ugly head. Jim Rickards describes in Currency Wars how the previous two currency wars took 10 to 15 years to play out. If history is any guidance, the monetary crisis will be the most important fundamental driver for gold. But that’s not what is top of mind of traders, at least not yet.

About GoldSilverWorlds.com

A couple of years ago, we discovered something was fundamentally wrong in our economy. Between the spring of 2000 and 2009, we noticed a series of extreme but also conflicting events. For example, the two decade bull market in the global stock markets which should have ended in 2000, should have been replaced by a new wealth cycle. Instead, in 2007 a new peak was reached in the stock market, but in a non-natural way. The type of implosion that followed in 2008/2009, wasn’t a natural type of event. At the same time, while the price of several commodities have been increasing in a steady way, others showed literally price explosions. One of those commodities, gold, revealed such a steady and robust long term price chart, that it raised a very natural question: ”What is such a robust price chart signaling?”

Our personal and extended research showed that we were experiencing a new wealth cycle. In the last two decades of the 20th century, paper financial assets were the main source of wealth creation. But as it goes with all cycles in this world, the death of one cycle goes hand in hand with the birth of a new one. So we discovered that the first years of the 21st century brought about the birth of a wealth cycle that was centered around hard assets: gold, silver, grains, sugar, potash, rare earths, etc.

Interestingly, the paper financial world was still rising at the same time. In the light of the theory of wealth cycles, we thought that was not really possible …. until we understood the role of the governments. They were apparently not very happy with the ongoing evolution. A paradigm based on financial paper assets is the kind of world they like because they can control it. The real assets based paradigm by contrast, implies a less significant role for governments and Central Banks. It’s all about power and control, even if it means they need to fight a natural ongoing trend. That insight marked a milestone in our view on the world. We weren’t aware it was THAT bad.

By researching the different types of commodities, we discovered that gold and silver had some special values. The most striking one, is integrity! Gold cannot lie, is what we wrote about it. Furthermore, it’s the only asset that can store wealth in a universal way, outside the financial system. During the exceptional implosion of the financial world in 2008 / 2009, we understood that gold was the ultimate store of value: despite it’s price decrease, it was still protecting wealth. The safe haven characteristic of precious metals is historically an important one, although it seems that the world forgot it over the past few decades.

By talking to ordinary people like friends and families, we discovered that most of us consider holding gold or silver as something “exotic”, something “mythical”. That was the final trigger for the birth of GoldSilverWorlds. As we became convinced that gold and silver were decisively going to continue their uptrend and that most people were not aware of the values of the precious metals, we wanted to contribute in a positive way to our society. The ultimate message of gold and silver being “safe havens” which protect our wealth, is a fundamental one for everyone of us to understand. It becomes even more important in a world where governments, central planners and banks will do everything they can to maintain their power. Their extremely dangerous monetary policies result in immense amounts of debts, that sooner rather than later will result in wealth destruction. The longer we wait, the worse the effects. Ordinary and hard working people will pay part of the bill as well. This attitude is simply immoral.

GoldSilverWorlds has the intention to spread the message about the real benefits of gold and silver in a simple way that everyone of us can understand. GoldSilverWorlds helps people understand how to invest their personal or professional wealth, where they can do so and what to avoid when doing so. Those are messages that are not told by mainstream media, sadly enough. Because of the internet, we can help each other as indidivuals, so let’s make use of it !

What is going on in America at least in 2013, is the following summary: of the 953K jobs “created” so far in 2013, only 23%, or 222K, were full-time. Part-time jobs? 731K of the 953K total.

For 2 more disquieting charts & commentary click on this link ZeroHedge

(Source Bureau of Labor Statistics)

Is China Doomed?

Between 1978, the year Deng Xiaoping’s sweeping economic reforms were launched, and 2011, China’s GDP increased by an average of 10 percent annually, three times that of the global economy. Now the boom times may be over.

By mid-2013, economic growth had slowed to 7.7 percent. That’s still a roaring pace compared to the rest of the world. Europeans, Americans and even Japanese might say about China’s slippage, “We should all have such problems.” Still, in thirty-five years, the Chinese polity hasn’t had to handle a prolonged economic slowdown and one may be in the offing. Hence the debate on what the deceleration could portend should it get worse and linger.

Is China headed for upheaval? The argument that it is seems plausible. Eye-popping growth rates and the accompanying increase in living standards—and of course the state’s massive machinery of repression—have been critical to maintaining political stability and public support for the Communist Party. Or is Beijing so skillful, so flush with foreign-exchange reserves—and hence with the capital needed for priming the economy and managing financial crises—that slower economic growth is no big deal? Don’t look to the experts for enlightenment on which take is true: they see the same data but draw different conclusions.

We’ll get to those incongruous assessments soon, but first, some context on China’s remarkable achievements since 1978. (While some China watchers think Beijing cooks the books, they do concur that the country’s economic transformation has been breathtaking.) China’s GDP, measured in purchasing-power parity using current dollars, was $248 billion in 1980; by 2012 it had soared to $12.3 trillion. Per-capita GDP—a useful measure of prosperity, even though it doesn’t reveal income distribution, the inequality of which has soared in China—has likewise surged, from $205 (at purchasing-power parity) in 1980 to $11,316 in 2011. Together, massive investment, breakneck economic growth, sharp declines in population growth, the advent of universal literacy and big increases in the number of people with a higher education have helped pulled six hundred million Chinese out of poverty.

Other numbers illustrate China’s economic makeover. In 1978 China accounted for about 2 percent of the value of global exports. By 2010 its share had risen to 10 percent, and the total value was $1.5 trillion. This success in the global marketplace was achieved to no small extent at the expense of the world’s other economic behemoths, Japan and the United States, whose shares declined. What makes this particularly noteworthy is that China’s GDP, though it recently surpassed Japan’s, is still smaller America’s, which was $15.7 trillion in 2012. Yet the value of China’s tradelast year was $3.87 trillion, eclipsing America’s total of $3.82 trillion. Even allowing for differences in the two economies’ relative dependence on trade this was headline-grabbing news. And it’s not just the value of what China sells the world but the difference that’s emerged in what it sells. Staples such as apparel, toys, shoes and basic electronics have been replaced by machinery and equipment, which account for over 50 percent of China’s exports, compared to just over 25 percent in 1995. Whether it’s energy, banking or telecommunications, Chinese companies have a global presence and are competing with American, European, South Korean and Japanese multinational corporations.

Okay, so what’s the problem then? It’s on this question that informed opinion is split. Paul Krugman is sure that the decrease in China’s economic-growth rate portends “big trouble” and that the signs are “unmistakable.” He and others pessimists chalk up China’s economic success to a combination of a vast rural population that has been available for induction into the industrial sector; low wages for workers, a function of an abundant supply of labor from the countryside; massive investment at the expense of consumption; and an exchange-rate policy that keeps the value of China’s currency low and its export earnings high.

The old paradigm, effective though it was, is starting to crumble. We’ve seen this before. The Soviet economy started slowing in the 1960s once it became harder—because of falling population-growth rates and the drying of the rural labor reservoir—to rack up big growth rates by pumping more people and money into manufacturing. The big difference is that while total-factor productivity (output per composite unit of labor and capital) didn’t pick up the slack in the USSR, in China it has increased significantly over the past two decades. Still, with Europe mired in recession, America posting anemic economic-growth rates and adding few jobs, and India’s and Brazil’s economies slowing down, it’s going to be harder for China to continue banking on big sales abroad to sustain rapid growth. So a lot hinges on whether Beijing finds a new way to sustain high growth, one that goes beyond basic industrialization and catching up to the West and sets trends in innovation.

….read page 2 HERE

Just over a week ago, the probability of a September ‘Taper’ were a mere 14% with the majority of the ‘smart’ money betting on a ‘December 2013 at the earliest’ start to the Fed’s removal of the punchbowl. September 2013 is now the front-runner at a 36% probability, based onPaddyPower’s latest odds. September has surgede from a 7/1 outsider to a 7/4 favorite in that brief time (and October also improved from 11/1 to 7/1). It seems that JPY-carry is well aware of this shift (having surged over 4% in the same period). Between Merkel’s election and the FOMC, the 3rd week of September (which just happens to perfectly correspond to an option expiration) looks set for some fireworks one way or another.

While bonds may well have repriced for this slowing of liquidity delivery, and credit and FX moves signal an awareness that a disturbance in the force is forthcoming, we suspect stocks remain sanguinely oblivious still.

I have been conducting extensive evaluations of all fundamental and technical aspects of this market, and almost everything points to an eventual crash. They key word here is eventual, but I think that sentiment resides with almost everyone I talk to as well.

Most investors believe the market will eventually pull back aggressively again, most investors have a very cautious tone, and over the past two trading sessions, it also seems that institutions have been taking profits.

The interesting part of this recent drawdown is that it happened for the same reason as the last drawdown, concern over tapering. However, the last drawdown was followed by one of the most aggressive increases we have seen all year, and this has been an aggressive year, so that means it was very significant. The last time concern over tapering faded, the market surged, so some traders are expecting the same thing again.

That past pattern of drawdown-then-surge has many traders interested in buying the market after the recent pullback, so the eventual correction that may eventually turn into a crash may not happen imminently. We are still in the middle of summer, the market can still easily be manipulated by a handful of aggressive traders and hedge funds because volume levels are light, and it has been easier to manipulate the market higher than lower this entire summer, so I do not expect them to turn sides easily.

More likely, they may try to push this higher yet again, they may try to let the market surge again, and at Stock Traders Daily we are taking advantage of that, but in the back of our minds is that eventual crash-concern, and therefore we are not holding our breath.

We are in the market for a trade on the long side off of the recent lows on Wednesday, this is a market-based play, but we did not relinquish our prior short-sector plays. We recommended ProShares UltraShort Real Estate (SRS -1.81%) and ProShares UltraShort Financials (SKF +0.34%) about two weeks ago, each of those are up handsomely, and those were directly tied to interest rates, so the increase in rates plus the market pullback helped us realize paper gains of about 7% thus far. We are not recommending these for new buys at this time, but we are not selling the positions either.

Instead, as a market-based play we are taking advantage of the recent drawdown with a strong focus on large-cap tech, and we expect to go all in on the short side soon. This transition will be governed by market forces, but it will be directly in line with our fundamental earnings analysis, macroeconomic work, and of course the technicals. Right now we are holding two sector-short plays and a long-market play focused on large-cap tech.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair