Energy & Commodities

Nuclear power accounts for 5.7% of the world’s energy and 13% of the world’s electricity. Uranium, used in nuclear power, is a relatively clean source of energy that does not produce greenhouse emissions. Uranium is extremely dense – it is nearly as heavy as gold. It is, however, about 500 times more common than gold in the earth’s crust. This infographic covers the history of uranium, its properties, the supply and demand forecasts, the advantages and disadvantages of nuclear power, uranium as an energy source, and military applications.

Are You Prepared For a Market Meltdown?

The markets are skating on very thin ice.

Stocks have hit new all time highs, but the ugly realities beneath this move in the markets have got many of the world’s most elite investors scared stiff.

Consider the following.

- Warren Buffett, arguably the greatest investing legend of the last 100 years has dumped many of his consumer discretionary holdings and is sitting on the single largest cash hoard of his entre career (he definitely doesn’t think it’s time to buy).

- Stanley Druckenmiller, investing legend, and former partner of George Soros has closed his hedge fund stating “…I see a storm coming. Maybe bigger than the storm we had in 2008 to 2010…”

- Jim Rogers, famed investor who made so much money that he retired at the ripe age o has warned that 2013 will be a disaster “… if you are not worried about 2013, please, get worried”

These guys have collectively made billions from investing. And they’re all terrified by what’s happening in the economy and the markets today.

It’s not difficult to see why.

Japan’s bond market is on the verge of imploding. Remember the impact Greece had on the markets? Well Greece’s bond market was just $450 billion. Japan in contrast has a bond market is over $7 TRILLION in size.

Europe is facing the single longest recession in its history. Youth unemployment is over 50% in some EU nations and total unemployment is nearly 20%.

And then there’s the US where 76% of Americans are living paycheck to paycheck with little to no emergency savings. And nearly 30% had NO SAVINGS AT ALL.

More on Japan: The Smart Money Is Leaving the Building

Japan continues to dominate the economic news. The latest move concerns Prime Minister Abe’s new economic policies to cut corporate taxes. He also announced plans to run a shakeup at Japan’s political ministries.

This is “Plan B” for Abe who has found that his policy of “Abenomics” or pushing the Bank of Japan to print even moremoney has failed to stimulate Japan’s economy.

Abe won in a landslide last September on his platform of urging the Bank of Japan to do more. This platform ignored the failure of QE to stimulate growth in Japan in the previous 20 years (Japan had already engaged in QE programs equal to 25% of the country’s GDP). It also ignored the risks of unfettered money printing, namely higher inflation.

Sadly, Abe has discovered that ignoring both of these key issues, while good politically, has been disastrous economically. Abe won the election and the Bank of Japan announced a record $1.4 trillion QE effort in April 2013. To put this number into perspective, this would be the equivalent of Ben Bernanke announcing a $3.75 trillion QE plan in the US. Suffice to say it was a “shock and awe” move.

Unfortunately, it hasn’t worked. Japan’s industrial production fell3.3% month over month in June. At the same time, Japan’s consumer price index registered its first increase in 14 months in June. The pace of increase was the fastest since 2008 when commodity prices were at record highs.

In plain terms, the Japanese economy is failing to respond to Abenomics. This is the single most important issue for the global financial system today.

The economy and financial markets have been moving in a zig-zag pattern ever since 2008 with drops in asset prices and GDP being met by intervention and stimulus by the world’s Central Banks.

However, thus far no Central Bank has gone “all in” with QE. The larger efforts have been focused on specific timelines (six months to a year) and the ongoing efforts have been tied to economic developments (the Fed claims it will taper QE when US employment falls to an acceptable level).

Never before has a Central Bank stated point blank that it’s firing a bazooka at the economy. Japan has done this. It has failed. And this failure has effectively been the “Emperor has no clothes” moment for Central Bank interventions.

And the markets are taking note.

Traders and investors do not respond to sea changes instantly. The smart ones take note and begin adjusting their portfolios and hedging their bets. This doesn’t result in massive market moves as these investors are sophisticated enough to move out of old positions and into new ones without drawing too much attention

It’s only when the investment herd en masse realizes that something has changed that you begin to see market Crashes.

This process has begun in the world. The smart money is leaving the market. And the market rally is being driven by fewer and fewer companies. This is classic Bubble Topping signals.

This is not to say that the market will crash tomorrow. But the sea change has hit and it’s now a matter of time. The likelihood of a full-scale market Crash similar to 1987 occurring in the coming months has increased dramatically.

If you have not taken steps to prepare for a market collapse, we have a FREE Special Report that outlines how to prepare your portfolio. To pick up a copy, swing by:

http://gainspainscapital.com/protect-your-portfolio/

Best Regards

Graham Summers

Chief Market Strategist

Phoenix Capital Research

All aboard and back up the truck. The recovery train is soon to leave the station for higher prices!

Obviously, the ideal time for that would have been at the exact bottom. Hours before that bottom we penned an article titled, Epic Opportunity in Gold Stocks. A number of factors came together making a near bulletproof case for a major bottom. Bulletproof is a dangerous word to use and especially for someone (cough, me!) who had anticipated a huge rebound as early as the spring. Last week we used that term again because the gold stocks were only correcting and consolidating which is a typical of a post-bottom rebound. The precious metals complex looked weak to start last week but reversed course to form not only a bullish weekly reversal but the first higher low since the major bottom. Our technical work and historical analysis strongly argue that it’s only a matter of time before this sector begins the next move higher.

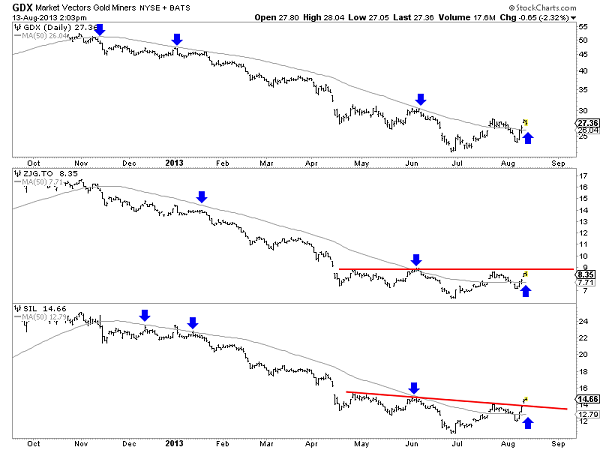

The daily chart below shows GDX (large miners), ZJG.to (mid-tiers and juniors) and SIL (silver stocks). All markets have not only put in a higher low but are now trading above their now upward sloping 50-day moving averages. In studying the 1970, 1976, 2000 and 2008 bottoms in gold stocks I found that the recoveries accelerated after the market moved above a flat or upward sloping 50-day moving average. That is currently quite visible in ZJG and SIL. GDX contains the large and most depressed companies so its not a surprise that its lagging. These markets should soon break out from their multi-month bottoming patterns.

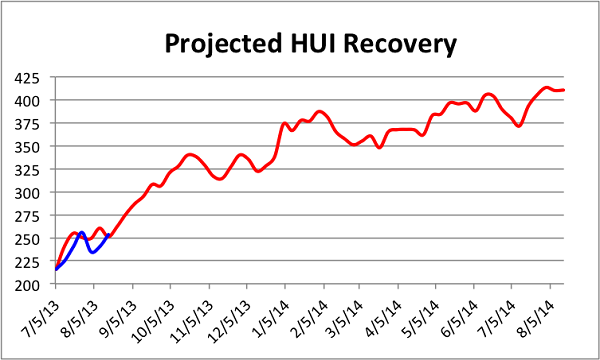

The next chart shows the current recovery (blue) overlaid with the average recovery which I constructed by amalgamating the 1970, 1976, 2000 and 2008 recoveries. We shouldn’t expect the current recovery to mirror the average exactly. The projection (average) serves only as a guide but that guide is telling us that big gains could be directly ahead.

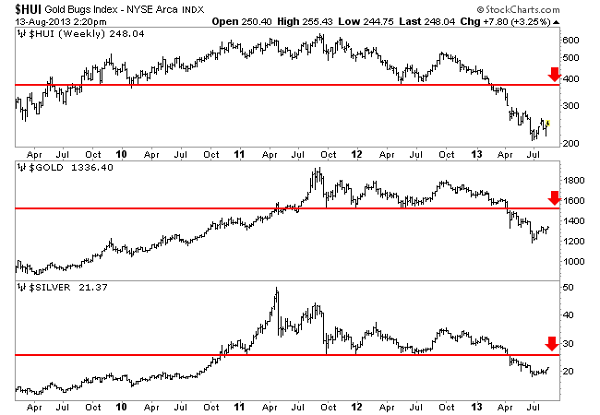

The projection above shows the HUI reaching 340 quickly and then 385 a few months later. The weekly chart below shows the next major resistance for the HUI, Gold and Silver. The HUI won’t face major resistance until 365 to 375. Thus, there is ample room for the market to recover as shown in the above projection. The same can be said of Gold and Silver. If and when Gold breaks $1350 it should have little in its way until $1525. Meanwhile, Silver should be able to rally back to $26.

It’s true of any market but even more so for the precious metals complex. The biggest gains come immediately following major bottoms. The recovery template shows that the recovery and gains really accelerate after the first correction or consolidation. Last week this sector put in a higher low on the weekly chart. That is significant. Look for this sector to gain momentum in the coming days and weeks. More instructive is the fact that many quality and leading companies are already trading at three or four month highs. Most traders will go with GDX and GDXJ, thereby neglecting the fact that there are huge gains to be had in this sector if you can identify the leading companies. For those who missed the initial rebound, now could be your final chance to initiate or add to positions before the acceleration begins. If you’d be interested in our analysis on the companies poised to lead the next bull market, we invite you to learn more about our service.

Good Luck!

Jordan Roy-Byrne, CMT

(Just Kidding!)

(Just Kidding!)

What is interesting is that during Japan’s lost decade [from 1991-2001] it outperformed the Eurozone in all categories: growth was faster, debt growth was slower, manufacturing productivity was higher, and labor costs grew more slowly.

Obviously there are several takeaways here, and we haven’t even broached the disastrous social impact of towering unemployment rates [specific country brain drain, birth rates, fall in scientific research, family strife, suicides, etc.]:

- If growth doesn’t resume soon, debt/gdp ratios across the Eurozone will mirror Japan’s; but in many ways because of such poor relative productivity and size of the Eurozone banking system the rise in debt will likely be that much more dangerous.

- As a hub for future industry in a globalized world where multi-nationals have so many choices, it looks bleak for countries inside the euro straight jacket. In short, foreign direct investment will go elsewhere.

- Instead of bringing cultures together, the single currency is helping bring old animosities to the surface, which are numerous thanks to two recent civil wars (WWI and WWII).

It seems unless something very big happens fairly soon, politicos across the Eurozone will be responsible for marginalizing the future of their people simply because they have invested so much political capital in this bold, but seemingly failed, experiment called the single currency despite passing by all the signs that read, “Turn back now!”

So, what is the endgame here?

…Into Cash?

With the Federal Reserve’s bond buying, liquidity injecting, market inflating, volatility suppressing, confidence inspirng, economic supporting, media headline generating, program currently in full swing; one would assume that the daily pushes to new market highs are driven by massive inflows of cash into the equity markets. Well, that assumption would be partially correct.

According to Trim Tabs:

“Fund flows in the past two months were by far the most volatile we have evermeasured. After ignoring equities and dumping bonds at a record pace in June,fund investors poured record sums into U.S. equities and continued to sell bonds in July.“

Of course, this is clear evidence that the “Great Rotation” by investors, from bonds into equities, is upon us which will cause yields to rise as investors bet on a recovering U.S. economy. Right? Maybe not.

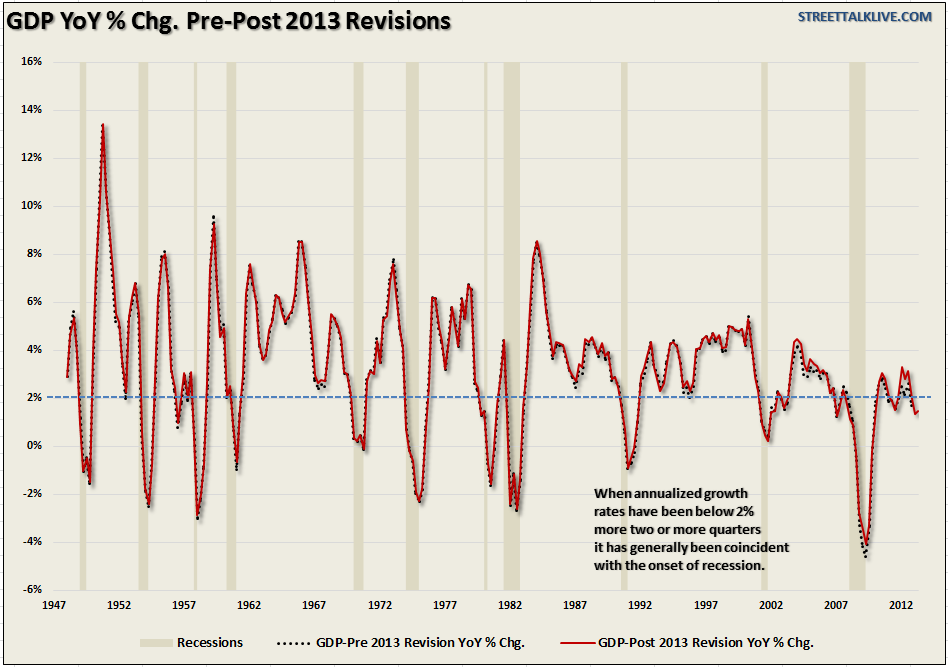

First of all there is scant evidence that the economy is entering into a growth mode. Even after the recent data manipulations by the Bureau of Economic Analysis (BEA) to artificially inflate the economic data by $500 billion through the addition of pension deficits and R&D expenses; the annual growth rate of the economy remained below 2% for the third straight quarter. Historically, such events have only been witnessed prior to the onset of economic recessions – not expansions.

Yet, the markets have continued to rise setting daily records with each minor uptick. This incredible advance….

…..read & view more HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair