Timing & trends

People say that selling in the Paper Gold market has hurt the Bullion market…perhaps it has but it reminds me of an old story from the New Orleans Seafood Exchange…which I think might provide a little perspective on today’s gold market.

People say that selling in the Paper Gold market has hurt the Bullion market…perhaps it has but it reminds me of an old story from the New Orleans Seafood Exchange…which I think might provide a little perspective on today’s gold market.

A long time ago, way before people had color TV, there was a small town doctor who had a real passion for trading commodities. He had a tough old La Salle Street broker who tried to keep Doc on the straight and narrow. Over the years Doc had traded most of the grain markets, without much success. He’d tried cotton, but that didn’t seem to work for him, and he never could get the rhythm of the coffee and sugar market…but then…he discovered the Seafood Market and that seemed to fit him to a “T.”

Employment is one of the most important factors impacting the value of real estate investments in B.C., so it is worth a closer look at some of the recent news.

It was reported this morning that B.C. gained 6,200 jobs in August versus a loss of 11,700 in July. So, that equates to a net loss of 5,500 jobs over the summer. B.C.’s unemployment rate for August was at 6.6%, the same level it was at in August 2012. (It should also be pointed out that the jump in jobs in August was driven primarily by part-time employment which is not overly encouraging).

This is in contrast to the media coverage over the last couple of days about the growing demand for “trade” jobs in the province. These stories focused on the demand for trades people in the middle part of B.C. and how this has led to an overflow of applicants for trades training both at the high school and post-high school levels. BCIT is even considering “round-the-clock” classes to meet the influx!

Anecdotally, I have also witnessed the increased number of trades people, primarily construction, gathering for work in the downtown core as I walk to the office everyday around 6:00am.

So, employment in B.C. looks hot anecdotally, but looks rather anemic statistically. Why is that the case?

Well, I have a theory.

The visible growth in jobs – in the trades – is the result of increased investment spending. This is driven by historically low interest rates which are the result of global economic policies and forces. Also, for an economy, high-paying trades jobs are trophy jobs. They are going to get attention from local politicians and media.

The less visible area of the job market – part-time and lower-paid service sector employment – is waning because of a lack of growth in the underlying economy. Hiring costs, taxes, fees, tolls, cost of living, and real estate prices that have increased in B.C. over the last decade have burdened the economy. Additionally, over the last decade, growth in public-sector employment was dramatic, but that is no longer a growth engine because the province’s public sector payroll had become disproportionately large relative to the size of the provincial economy.

Overall, the province is treading water with respect to employment. Additionally, and somewhat concerning, the high-profile growth in the trades has been dependent on easy global monetary policies that have kept a lid on interest rates and have spurred visible investment spending. However, despite those policies, longer term market-determined interest rates have begun to move higher, increasing about 1.5% over the last year. As a result, there is a risk that it may only be a matter of time until investment spending falls which will make the employment situation in the trades look more like the employment situation elsewhere in B.C.

The opinions expressed in this report are the opinions of the author and readers should not assume they reflect the opinions or recommendations of Richardson GMP Limited or its affiliates. Assumptions, opinions and estimates constitute the author’s judgment as of the date of this material and are subject to change without notice. We do not warrant the completeness or accuracy of this material, and it should not be relied upon as such. Before acting on any recommendation, you should consider whether it is suitable for your particular circumstances and, if necessary, seek professional advice. Past performance is not indicative of future results.

Richardson GMP Limited, Member Canadian Investor Protection Fund.

Richardson is a trade-mark of James Richardson & Sons, Limited. GMP is a registered trade-mark of GMP Securities L.P. Both used under license by Richardson GMP Limited.

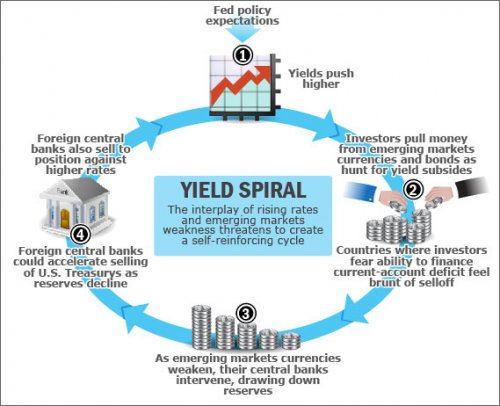

In my experience, markets don’t deal well with several crises emerging at the one time. Give them just QE tapering and they may be able to adapt, but throw Syria and an Asian currency mess into the mix, and it can make for a wild ride. Underlying all of the recent volatility though is the first sign that investors are starting to doubt the omnipresent powers of central bankers. Ben Bernanke says there can be QE tapering without rising interest rates and bond markets revolt against that idea. Similarly, the new Bank of England chief Mark Carney says interest rates will remain low for the next three years and bond yields jump given better economic data and rising inflation.

In my experience, markets don’t deal well with several crises emerging at the one time. Give them just QE tapering and they may be able to adapt, but throw Syria and an Asian currency mess into the mix, and it can make for a wild ride. Underlying all of the recent volatility though is the first sign that investors are starting to doubt the omnipresent powers of central bankers. Ben Bernanke says there can be QE tapering without rising interest rates and bond markets revolt against that idea. Similarly, the new Bank of England chief Mark Carney says interest rates will remain low for the next three years and bond yields jump given better economic data and rising inflation.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair