Stocks & Equities

What a difference a few weeks can make.

All eyes were anxiously watching the Federal Reserve in mid-September. The key question on every investor’s mind: Would they or wouldn’t they? (Taper quantitative easing, that is.)

The S&P 500 Index had recorded its largest monthly drop in 15 months in August. But the Fed surprised investors by keeping the current pace of $85 billion in monthly bond purchases.

Today the benchmark index is at a record, having jumped 24 percent this year, the best performance since 2003. Yes, investor sentiment has shifted dramatically.

[Editor’s note: For more detail on where Mike sees potential outperformance, Click HERE for an audio extra.]

Not only is tapering no longer the worry of the day, but apparently it’s not even on the horizon. Most commentary and analysis I’m reading has pushed the start of reducing the stimulus program well into 2014.

The government shutdown and prospect for continuing budget battles early next year has a lot to do with the shift in consensus. And the jobless rate, a key indicator for the Fed, is still too high. (The government finally got around to releasing it – 7.2 percent in September compared with 7.3 percent in August.)

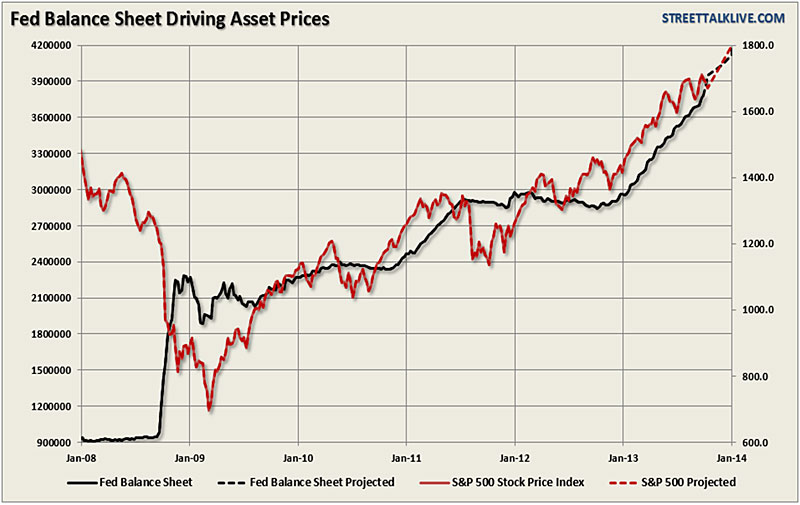

(Click image or HERE for larger view)

As the graph above shows, there’s a strong tie between the size of the Fed’s balance sheet and the stock market’s rise. Ever since the Fed’s first round of QE in 2009, and with each successive expansion, the S&P 500 has responded almost in lock-step.

Shift in Stock-Market Leadership

The no-taper relief rally has been accompanied by a shift in stock-market leadership, which I pointed out several weeks ago. Specifically, the risk-on trade is back, featuring outperformance by economically sensitive assets that are considered riskier, including:

1. Cyclical stocks and sectors, such as basic materials, technology and industrials.

The good news: You don’t have to invest in foreign stocks or international ETFs to tap into this potential. Instead, you can “go global” by investing locally by focusing on sectors or stocks that earn a substantial share of sales from abroad.

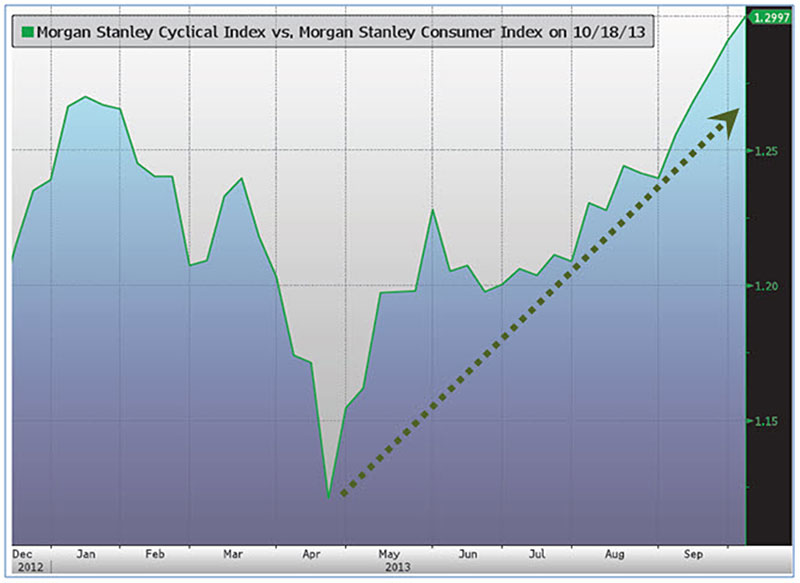

Here’s why cyclical sectors should keep outperforming. In the chart above, the dotted line plots the Morgan Stanley Cyclical Index relative to the Morgan Stanley Consumer Index.

When the line is rising from the lower left to the upper right, it means cyclical stocks (materials, energy, technology, industrials, consumer discretionary and financials) have the upper hand over defensive stocks (consumer staples, health care, telecommunications and utilities).

The reason: A downshift in global growth is stabilizing, and there are signs of improvement overseas. Over the past three months, global manufacturing expanded in 27 of the 33 largest economies. That’s a bullish sign for cyclical stocks.

The table above lists the performance by sector since the end of June. It’s no surprise that nearly all of the top-performing stocks and industries also have the highest percentage of foreign sales — they stand to benefit most as global growth re-accelerates.

– Technology, for instance, generates 40 percent of sales from overseas markets. It’s the second-best-performing sector since June, up 14 percent.

– Energy and industrials earn 20 percent and 21 percent of sales abroad. They’re beating the benchmark Russell 2000 Index too.

– Materials is trailing, yet with 30 percent of sales from overseas, the sector has been playing catch-up, with a gain of 14.7 percent since July 1.

In the third quarter, materials and technology companies have reported the biggest upside earnings surprises compared with estimates (26.8 percent and 12.3 percent, respectively), according to FactSet Research.

I’ll be keeping an eye on these trends as earnings season progresses, and you should too. The shift in market leadership toward cyclical stocks, if it’s sustainable, may have a long way to go. And there are plenty of attractive technology, energy and materials stocks to choose from today.

Make sure to go to our Money and Markets’ Facebook page for a review of two undervalued cyclical stocks I’m looking at.

Good investing,

Mike Burnick

The Other Precious Metal Can Double Your Money Now

At times like this, gold and silver typically grab all the attention… and attract all the “safe” money. But there’s another metal that could blast past both of these, virtually overnight.

That’s because it has unique physical properties for which there is just no substitute – something its biggest consumers lose quite a bit of sleep over.

It’s 15 times more rare than platinum… and 30 times more rare than gold.

And, as you’ll see in the chart below, it hasn’t been this attractive in 13 years.

We’re looking at a 70% gain on this one – perhaps more – no matter how far Washington kicks the “debt can” down the road.

At current prices, it could even double…

Palladium: The Double-Your-Money Metal

Even when the government isn’t on the brink of financial suicide, palladium is in heavy – and growing – demand.

It’s found in everything from jewelry to dental equipment, including a wide range of electronics.

Tablets, flat screen TVs, iPhones, iPods, iPads, iEverythings…

They all require palladium.

Electronics represent 12% of gross palladium demand.

For perspective, there were 5.4 billion cell phones on the planet in 2009. By the end of this year, estimates are that there will be 8 billion. It’s going to take a lot of palladium for the world to keep talking, texting, and tweeting.

But its most significant use is in the automotive industry, where fully two-thirds, or 67%, of all palladium is consumed each and every year.

That’s because palladium is found in virtually every single gas-powered vehicle’s pollution-controlling catalytic converter.

And global light vehicle production has been on a tear in the last couple of years, with no signs of abating. 2011 saw 77 million light vehicles produced, and 2012 saw 81 million. This year, it’s expected there will be 85 million units produced, and by 2017, IHS Automotive forecasts 102 million units.

By 2018, China alone will likely be manufacturing and buying about 31 million vehicles annually.

Developed and developing economies alike have adopted increasingly stringent emission control standards, boosting the need for palladium.

There’s little doubt, we’re going to need a whole lot more of this specialized metal.

But it’s not going to be easy…

Global Supply Is Dwindling

What’s crucial to understand about palladium supply is where the metal is actually sourced.

Only about 6.5 million ounces of palladium are produced annually. Recycling, plus sales from a Russian stockpile, supplies the rest, to reach a total 9.8 million ounces each year.

Russia is responsible for fully 44% of the 6.5 million produced ounces and South Africa for 36%. But both of these suppliers face serious output challenges. Norilsk Nickel is responsible for all of Russia’s mined production as a byproduct of nickel production. But Russia’s mined supply has been dwindling, and active mines have seen declining ore grades.

What’s more, only two years ago 775,000 ounces came to market from Russia’s state repository, Gokhran. That was about 8% of world supply. Last year, that number had dropped by 68% to 250,000 ounces. Industry insiders figure those stockpiles may now be totally exhausted, but officially no one can say for sure; Gokhran’s contents are a state secret.

What we do know is that 2012 saw the lowest level of global palladium supply since 2002, suffering a deficit of 1.07 million ounces.

For its part, South African supply is even more challenged. Palladium is produced there as a byproduct of platinum. Numerous South African platinum producers are facing such high costs that they no longer turn a profit. Mines are deeper, power and water are sparse, labor costs are rising, political risks are growing, and work strikes and other stoppages all add up to declining output.

That leaves 14% of mined palladium supply contributed by North America and 6% from a few small players sprinkled across Africa, Australia, China, and the former Yugoslavia.

The ever-dwindling supply of palladium isn’t going entirely unnoticed, of course…

Industry Insiders Are Hyper Aware of the Supply Squeeze

I recently interviewed a mining executive whose company is a primary palladium producer.

He concurred that the fundamentals for palladium demand – thanks to pressure from pollution control and car sales – are very supportive. He also confirmed that Russian and South African supplies face real headwinds.

Morgan Stanley (NYSE: MS) has recently said, “We expect an ongoing and sizable structural deficit in palladium supported by an increase in net auto catalytic converter demand as gross demand from strong vehicle growth and tightening emission standards outpaces recycled palladium supply, especially in China.”

After accounting for investment demand, Morgan Stanley is forecasting a 2013 palladium deficit on the order of 1.013 million ounces.

Besides the deteriorating supply and expanding demand factors I’ve outlined, there are two other catalysts that are primed to ignite palladium prices ahead.

“Double Demand” from ETFs and Short-Sellers

The first is physical, or investment, demand. Since 2007 physically backed palladium ETFs have grown to include 11 such investment vehicles, absorbing nearly 2.2 million ounces from global supply, up from 1.9 million at the outset of 2013. Johnson Matthey PLC (LON:JMAT) has indicated that so far this year palladium ETFs have acquired 339,000 ounces of palladium, on pace to surpass 2012’s 385,000 ounces. And this trend is in motion.

Now a 12th palladium ETF is in the offing, which could be trading on South Africa’s Johannesburg Stock Exchange by year’s end. A wildly successful platinum ETF that began trading there earlier this year has already soaked up 685,000 ounces, representing fully 30% of worldwide ETF holdings. The new palladium offering could well be Act II, further exacerbating the market’s persistent shortfall.

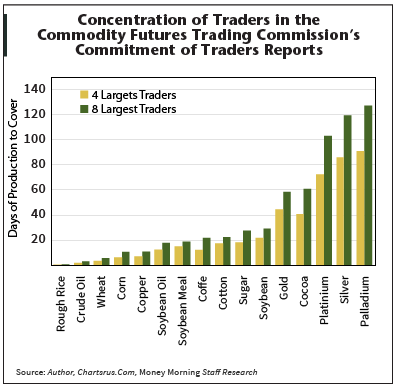

Yet another bullish factor for palladium prices is something intriguing that’s happening in the futures market. As you can see in the chart at right, the eight largest futures traders are short 127 days of world palladium production. That’s at a 13-year high, and it’s more than any precious metal, and more than all other major commodities.

Yet another bullish factor for palladium prices is something intriguing that’s happening in the futures market. As you can see in the chart at right, the eight largest futures traders are short 127 days of world palladium production. That’s at a 13-year high, and it’s more than any precious metal, and more than all other major commodities.

If the palladium price should suddenly rise significantly, those traders would likely be forced to quickly cover their massive short positions.

That could lead to a violent rally in the price of palladium, as they would have to buy long contracts to offset their shorts.

And get this…

Norilsk, the world’s largest palladium producer, also expects a 1 million ounce deficit this year and has repeated their stance that Gokhran is drained of its palladium stockpile, unable to contribute to the market going forward.

The pricing estimates reflect that shortfall, too.

Palladium is currently trading around $710 per ounce. The average of analysts’ forecasts pegs this year’s price at $751, next year’s at $829, and $909 two years out. The most optimistic of these projections sees palladium averaging $1,200 in 2015.

Extremely bullish supply and demand fundamentals, impending growth in investment demand – and the futures “wild card” all point to palladium prices heading up fast, a lot faster than most analysts expect.

U.S. Stock Market – My growling bear suit was hung up in my closet back in March 2009. Since that time the U.S. stock market has enjoyed an incredible rise during a period of rather pathetic economic growth. Not that many days pass without a reader asking how come I’m not shorting the stock market.

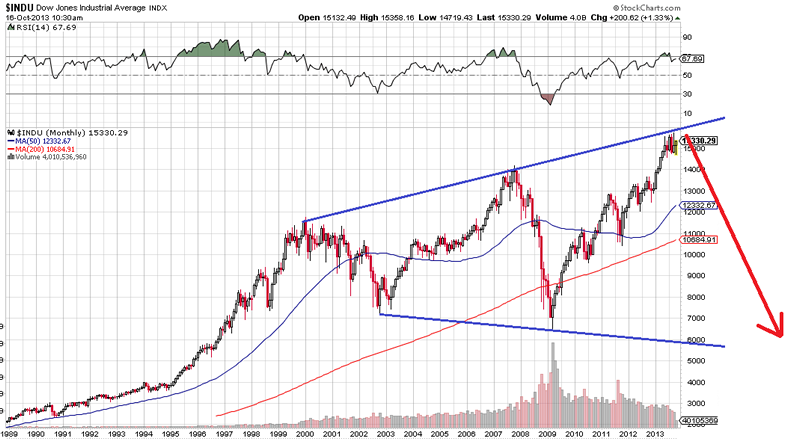

It’s been my opinion for quite some time that the U.S. stock market was tracing out a “megaphone” pattern and that the ultimate top appears to be somewhere over DJIA 16,000. I continue to act on that belief and feel with all other factors impacting the market it would be an ideal place to get short.

For now, the “Don’t Worry, Be Happy” crowd are dusting off their Santa Claus rally propaganda scripts and starting to calculate their year-end bonuses. If defaulting on our debt didn’t sway them, I can almost assure you they’re home free through at least year-end

U.S. Bonds – the high yield for the year was 3% on the 10-year and the rally anticipated from there is running its course. For those who didn’t like the taste of losses holding bonds, it was just a trial run to what’s going to happen in 2014 and beyond. Don’t be part of the fool me once shame on you, fool me twice shame on me group in the coming economic, political and social upheaval forming in America as we speak.

Gold – Funny thing about its many critics. Throughout most of the year, they and the media who love to follow them said with “tapering” to come and a rising U.S. dollar, it will spell doom for gold. Yet, with the opposite, not one of them have showed class and said this.

A very significant bottoming process in near complete and a move back sbove $1,400 appears in the cards. The $1,500 – $1,550 area is critical resistance and a place you can be assured the gold haters will make a stand

U.S. Dollar – It’s terminally ill. End of story.

Good morning! Here’s what you need to know.

Good morning! Here’s what you need to know.

- Markets were mostly higher. Korea’s Kospi led in Asia at 0.54%. In Europe, Germany’s DAX was up 0.45%. U.S. futures were up about 0.30%.

- China’s purchasing managers index for Octobe rprinted a seven-month high 0f 50.9, beating expectations of 50.4. “This implies that China’s growth recovery is becoming consolidated into 4Q following the bottoming out in 3Q. This momentum is likely to continue in the coming months, creating favorable conditions for speeding up structural reforms,” HSBC chief China economist Hongbin Qu said.

- Europe is still growing, but it’s slowed down a bit. The Eurozone’s composite PMI declined to 51.5 from 52.2. “Although modest, the expansion is reassuringly broad-based across the region, reflecting signs of economic recoveries becoming more entrenched in the periphery as well as ongoing expansion in Germany and stabilisation in France,” Markit’s Chris Williamson said.

- India is now expected to see its GDP decline to the lowest level in more than a decade. Reuters polled 24 economists, who now see growth slowing to 4.7% — the same figure the World Bank recently came up with. “India’s ailing economy is likely to remain under pressure from weak domestic and foreign demand for some time, while uncertainty ahead of elections next year is expected to keep investors and businesses at bay,” Reuters’ Rahul Karunakar and Ashrith Rao Doddi write

- Institutional investors accounted for 14% of all sales in September according to RealtyTrac, up from 9% of all sales last month. “The housing market continues to skew in favor of investors, particularly deep-pocketed institutional investors, and other buyers paying with cash,” Daren Blomquist, vice president at RealtyTrac said in a press release.

- This is the busiest earnings day of the year, with 358 different firms releasing their Q3 figures. Ford is already in: they beat earnings, missed sales estimates, and its shares are up 3.6% pre-market. Also before the bell we get, among others, 3M ($1.75/share expected), Altria ($0.64/share expected), Colgate ($0.73/share expected), Dunkin Donuts ($0.43/share expected), Southwest Airlines ($0.33/share expected), and Xerox ($0.25/share expected). Amazon ($-0.09/share expected) and Microsoft ($0.54/share expected) also report, after the bell.

- We also get a raft of new economic data this morning. At 8:30, weekly jobless claims print, with 335,000 expected versus 358,000 prior; and August international trade data, with a decline of -$900 million expected. Just before 9 am, October flash PMI prints, with a decline of 0.01 to 52.7 expected. Finally at 10 am, we get the Job Openings and Labor Turnover Survey (JOLTS).

- The Obama Administration appears ready to extend the open enrollment period to sign up for health insurance at least through March, Reuters’ David Morgan and Mark Felsenthal report. And pressure is now mounting from Democrats to make additional reforms to the Affordable Care Act’s centerpiece, the health insurance exchanges. “Representative James Clyburn of South Carolina, the third-ranking House Democrat, criticized the website for forcing consumers to provide private information before deciding what kind of health insurance plan they want to buy. ‘I’ve talked to too many people who tell me before they ever get around to figuring out what it is they want to buy, they’re having to answer questions that they don’t feel they should be answering,’ Clyburn said.

- The CEO of British-based WPP, the world’s largest ad firm by revenue, told the Wall Street Journal that allegations the U.S. was spying on its own allies would damage both “brand America” as well as the ad industry, since it could lead to commercial data collection becoming more restrictive. “If Germany’s Chancellor is bugged—true or not—the bare suggestion of this is bad,” Mr. Sorrell said. “Imagine [CEO of rival Publicis Groupe SA Maurice Levy ] calling me to assure me that he wasn’t tapping my phone, or the other way round…It’s pretty serious stuff.”

- Bitcoin prices briefly hit $230 overnight and remain above $200 this morning on the Mt. Gox exchange, recalling the insane surge that occurred this spring and reflecting the resiliency of the digital currency.

Yesterday, the Labor Department reported that nonfarm payrolls (jobs) increased by 148,000 in September. Today’s chart provides some perspective in regards to the US job market. Note how the number of jobs steadily increased from 1961 to 2001 (top chart). During the last economic recovery (i.e. the end of 2001 to the end of 2007), job growth was unable to get back up to its long-term trend (first time since 1961). More recently, the number of nonfarm payrolls has been working its way higher but at a pace that is not fast enough to close the gap on its 1961 to 2001 trend. It is interesting to note that the current number of US jobs recently surpassed its 2001 peak. However, the job market has yet to reach the peak levels obtained back in early 2008.

Notes:

Where should you invest? The answer may surprise you. Find out right now with the exclusive & Barron’s recommended charts of Chart of the Day Plus.

Quote of the Day

“People who work sitting down get paid more than people who work standing up.” – Ogden Nash

Events of the Day

October 24, 2013 – United Nations Day

October 31, 2013 – Halloween

November 02, 2013 – Breeders’ Cup

November 03, 2013 – Daylight Saving Time ends (US) – New York Marathon

Stocks of the Day

— Find out which stocks investors are focused on with the most active stocks today.

— Which stocks are making big money? Find out with the biggest stock gainers today.

— What are the largest companies? Find out with the largest companies by market cap.

— Which stocks are the biggest dividend payers? Find out with the highest dividend paying stocks.

— You can also quickly review the performance, dividend yield and market capitalization for each of the Dow Jones Industrial Average Companies as well as for each of the S&P 500 Companies.

Mailing List Info

Chart of the Day is FREE to anyone who subscribes. Click HERE to subscribe

To ensure email delivery of Chart of the Day, add mailinglist@chartoftheday.com to your whitelist

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair