Personal Finance

How to Protect Your Money When the U.S. Debt Bill Comes Due

Ever heard of a wedding crasher? You know — that distant “cousin” who shows up uninvited, hangs around the open bar all night, chugs down double-everythings and falls on his butt on the dance floor — all before mysteriously vanishing and leaving his night of indulgence on the father of the bride’s tab.

You don’t want to be around when that bill comes due!

Well, as a quasi-government organization with the authority to suck down your hard-earned money through the act of inflation, the U.S. Federal Reserve is “that guy,” and you could be the responsible one left with its bill.

Did you know that the Fed has been inflating the supply of dollars at a stunning 33% annual rate over the past five years? Or that it plans to continue inflating the supply of dollars at least into 2014 and has kept open the possibility that it will do so indefinitely?

When the Fed’s party is over, who do you think will be left with the bill?

Not the Wall Street bankers! We’ve learned that lesson already.

It’s Main Street investors like you who get the bill.

But you can protect yourself — though your window of safety is closing rapidly.

Robert Prechter, market forecaster and leading opponent of the Federal Reserve, has just released a report that that will help you understand the risks of deflation that most mainstream sources cannot see because they are blinded by decades of inflationary Fed policy.

At just 8 pages, “How to Protect Your Money When the U.S. Debt Bill Comes Due” is a quick read — well worth any independent investor’s time.

Report Excerpt:

The Federal Reserve’s efforts to rescue the economy have been historically aggressive, starting with the initial round of quantitative easing in 2008 and continuing through 2013.

The central bank’s assets have skyrocketed due to the Fed’s bond purchases, which you can see clearly in this eye-opening report that Robert Prechter presented to the Market Technicians Association and his Elliott Wave Theorist subscribers.

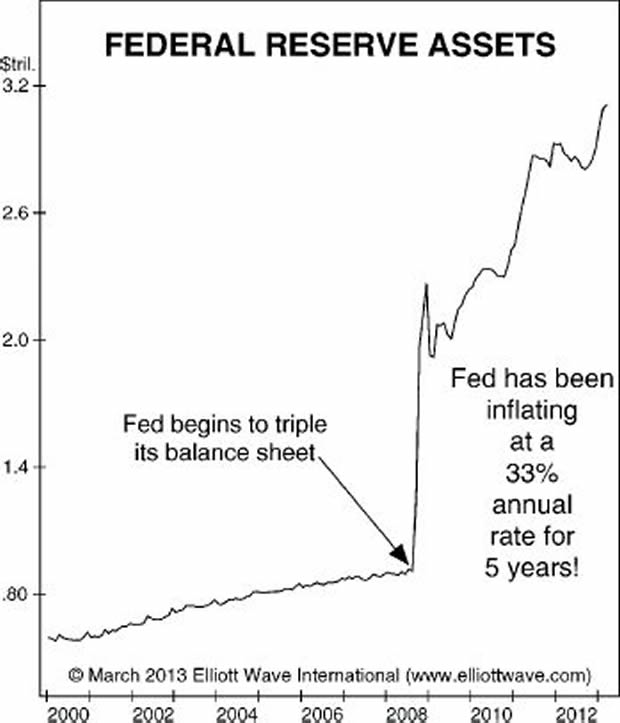

The main reason investors are expecting runaway inflation is illustrated in , which shows the value of assets held at the Federal Reserve. The Fed has been inflating the supply of dollars at a stunning 33% annual rate over the past five years. … o wonder investors expect inflation and have aggressively positioned for it.

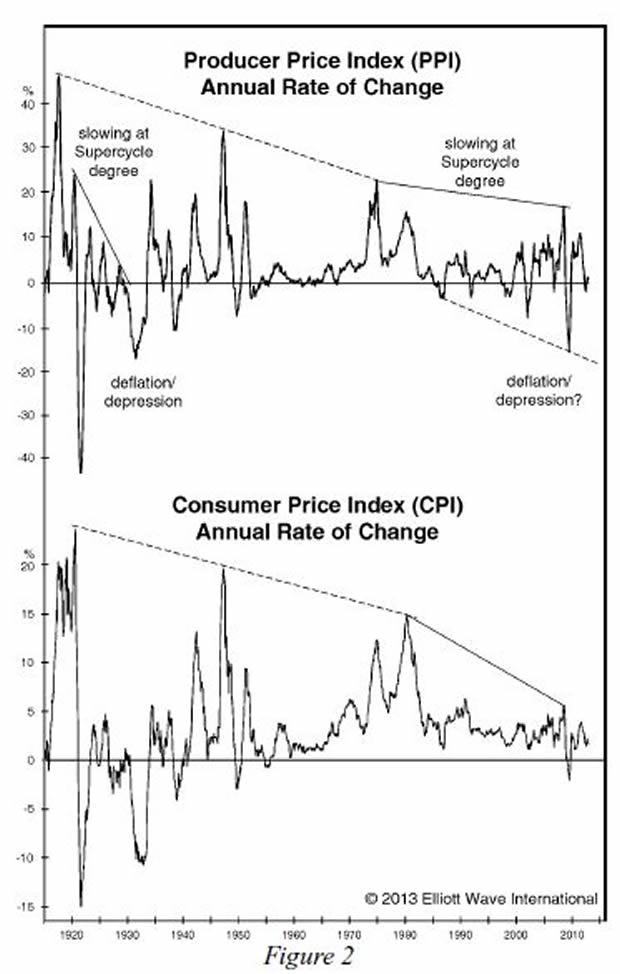

Look just about anywhere else, however, and you will see subtle evidence of deflationary pressures. Given knowledge only of the Fed’s inflating, many people would expect the Producer and Consumer Price Indexes to be rising at a rate of 33% annually. But, as you can see in Figure 2, the PPI’s annual rate of change is stuck at zero and the CPI has been rising at only a 2% rate.

In an interview at the recent San Francisco Money Show with financial author Jim Mosquera, EWI’s Chief Market Analyst Steven Hochberg explains why the Fed has gotten so little in return from its stimulus programs. Here’s a brief excerpt from the interview published on Aug. 18 on the Examiner.com website.

Question: The Fed wizards have been pushing buttons and pulling levers rather furiously since 2008. The discount rate is rock bottom, and the Fed balance sheet has swelled to the tune of trillions. What button is left for them to push?

Steve Hochberg: That is a really interesting question the way you phrased it because the fact that they have been pushing buttons and have gotten very little in return tells us … that the Fed is not in control. The Fed does not control the markets, and it doesn’t control the economy. Both are bigger than the Fed.

You say they have been doing this furiously. They have been doing this historically! Yet if you look at inflationary measures, such as the Personal Consumption Expenditures, which is the Fed’s favorite way of measuring inflation, it’s bumping along at 1%.

We have had historic fiscal and monetary stimulus and yet no inflation. Why? The forces of deflation are overwhelming the forces of inflation. The Fed dropped interest rates in 2000 to 2002 and that did not stop the Nasdaq from dropping 78%. The Fed dropped rates from 2007 to 2009 and it did not stop the Dow from going down 59%. There is historical evidence that the Fed does not control the markets but that the markets control the Fed.

As the next leg of the bear market starts unfolding, they are going to do more unconventional things. Things will accelerate to the downside when the public realizes the central banks aren’t in control.

For a limited time, you can read Robert Prechter’s 6-page report to prepare for what EWI sees ahead. In this report you’ll learn why the risk of deflation is mounting and how you can see it coming in the prices of gold, gas, real estate, crude oil and other markets. See below for full details.

Follow this link to download your free deflation-protection report now >>

About the Publisher, Elliott Wave International

Founded in 1979 by Robert R. Prechter Jr., Elliott Wave International (EWI) is the world’s largest market forecasting firm. Its staff of full-time analysts provides 24-hour-a-day market analysis to institutional and private investors around the world.

I can think of no better asset to own during any kind of financial crisis than farmland or investing in agriculture stocks.

I can think of no better asset to own during any kind of financial crisis than farmland or investing in agriculture stocks.

In some ways, farmland is even better than gold or silver. At least farmland is an intrinsically useful thing. It provides a tangible yield in the form of good things from the earth. We all have to eat. As consumers trim their sails, they ‘ll give up a lot before they give up their calorie intake. In fact, worldwide, the per capita calorie intake is likely to rise, while quality soil will become a scarce commodity. Altogether, I see five big reasons why agriculture investments are as good as green gold…

Invest In Agriculture: Reason #1

Grain inventories are falling to their lowest levels in more than 40 years

Obviously, we can’t continue to dip into inventories. The natural response you would expect to see is rising prices for grains and for the farmland that produces them. Global grain inventories, drought pending, are expected to rise this year, but will still remain well below historical level.

The big thing to keep your eye on here is stocks-to-use ratio. That compares the amount we have on hand to the amount we’re using. The higher the number, the closer we are to having fully stocked granaries. In the case of big commodities like corn, wheat and soybeans, the cupboard’s pretty bare. Based on USDA numbers, the stocks-to-use ratio for 2008-2009 looks to be the second lowest in history.

U.S. ending stocks are projected to nearly double, going from 7 million metric tons to nearly 14 million metric tons. Many countries, even grain powerhouse Argentina, are still holding onto local supply by restricting exports.

Mark McLornan made this comparison in the May issue of Marc Faber’s Gloom Boom & Doom Report: Investing in agriculture today will be like investing in the oil sector in 2001-2002. (If you’ll remember, that’s when oil raced up to $143 a barrel from its $30 low.) Right now, this sector remains locked in underinvestment, so there’s opportunity here, considering the case of future demand.

Invest In Agriculture: Reason #2

Grain consumption is on the rise

The world consumes, on average, 2,600 bushels of grain crop per second. That’s almost twice what we ate back in 1974. And that amount could easily double to 5,200 bushels per second over the next 20 years. The amount of pressure on the global food supply network is enormous. You can see the steep downward trend in wheat supply in the chart below.

Why are we eating so much more grain? The big factor here is meat. Hundreds of millions of people in China and India are joining the middle class. As people get wealthier they eat more meat. And more meat requires more grains to feed cattle and hogs. It takes 10 pounds of grain to produce one pound of meat. Because of that, most of the demand growth for coarse grain and oilseed meal will come from livestock in developing economies or the countries feeding them. So long as the middle class expands, you can be sure meat and grain consumption will follow.

Invest In Agriculture: Reason #3

Biofuels are driving ag demand up to new levels

Most every oil-consuming country has biofuel targets in place that will kick in over the next five years. These places include the U.S., the EU, Canada, Japan, Brazil, India and China. To meet their targets, according to work by Agcapita, we‘ll have to commit some 240 million acres to biofuel production. That represents about 50% of the arable land in North America and about 6% of all the arable land in the world.

Let’s consider ethanol alone for a moment, courtesy of some World Bank stats. From 2004-2007, U.S. biofuel use increased by 50 million tons, while world production increased only 51 million tons. That leaves only 1 million tons left over to cover a 33 million ton increase in the rest of corn demand the world over. Meaning we didn’t cover usage and caused the price to rise. By 2008, U.S. farmers were already planting every available acre with corn, the second biggest planting in 60 years, and producing one of the largest corn crops in history.

This helped push U.S. farmland values up to new record highs. Massachusetts farmland fetched the highest price at $12,200 per acre. As you can see, the biofuel craze puts more pressure on farmland demand. And, there are other pressures as well…

Invest In Agriculture: Reason #4

Arable land per person is falling

We are losing quality topsoil faster than we are replacing it. Quality soil is loose, clumpy, filled with air pockets and teeming with life. It’s a complex microecosystem all its own. On average, the planet has little more than three feet of topsoil spread over its surface. The Seattle Post-Intelligencer calls it the shallow skin of nutrient-rich matter that sustains most of our food. Replacing it isn’t easy. It grows back an inch or two over hundreds of years.

This is not lost on certain farseeing investors. Jeremy Grantham, the curmudgeonly head of the money manager GMO, recently told his clients: Our farmers are in the mining business! Yes, the soil is incredibly deep, but it is still finite. For every bushel of wheat produced, we lose two bushels of topsoil.

We lose topsoil to development, erosion and desertification. Globally, it’s clear we are eroding soils at a rate much faster than they can form, notes John Reganold, a soils scientist at Washington State University. Estimates vary, but in the U.S., the National Academy of Sciences says we’re losing soil 10 times faster than it’s being replaced. The U.N. says that on a global basis, the rate of loss is 10-100 times faster than that of replacement.

In any case, it seems safe to say that good dirt is in short supply. This ensures a growing scarcity of good farmland, and plenty of countries including Saudi Arabia, China, and South Korea, that will pay for it at any price.

For the first time ever we’re in danger of slipping below one acre per person. Of course we don‘t need 2.8 acres per person anymore, because of advances in agriculture over time. But gains in yield per acre are slowing. Over the last 40 years, we’ve increased the yield per acre by 2.1% per year. But the pace of those gains is slowing. Since 2000, the increase in yields per acre has averaged less than 1% per year.

We may see new innovations in seeds or other technology that we can scarcely imagine now. But any solution will take time and money to implement. Meanwhile, the world’s agriculture markets just get tighter and tighter…

Invest In Agriculture: Reason #5

Low water supplies cut down farm productivity

China is a biggie to watch when it comes to food supply dynamics. It feeds 20% of the world’s population on only 10% of the world’s arable land and with only 6% of its water. China’s water tables are falling too. In parts of its traditional breadbasket in the north production of wheat and corn is in jeopardy. Chinese officials are well aware of this urgent need.

As the Financial Times reports: The country is investing heavily in agriculture. Its agriculture budget increased 27% in 2007, 38% in 2008, and about 20% in 2009. No other big country, barring India, has increased spending on farming so much, says the FT. Still, increasing output will be a challenge.

One British study suggests that if China imports to meet just 5% more of its grain demand, it could swallow all the world’s exported grain. In 2007 and 2008, China imported practically zero wheat. However, today imports are on the rise, sometimes increasing over 100% from month to month. Part of that’s due to drought, which we can expect a lot more of in China as the years roll on and the water table decreases even more.

It also means that any way to secure better water supplies will be worth its weight in gold. Growing crops and keeping livestock hydrated uses three-quarters of the world’s water. That’s a lot of water, and China already doesn’t have enough.

A United Nations report puts it in stark terms: The population of China, India, Pakistan, and other big Asian countries will grow 1.5 billion by 2050, doubling the continent’s food demand. Some of the best returns this decade will come from agriculture investing, and the kinds of companies that keep us supplied with water, food, and energy. Position your portfolio accordingly.

Thank you for reading,

Chris Mayer for The Daily Reckoning

More Reading: 2014: The Year the Chickens Come Home to Roost

Although the Fed may realize (though I doubt it) that the current asset purchases have minimal impact on the real economy of the majority of American people, they probably think that continuous monetary stimulus is the lesser of two evils. This is a wrong assumption, in my opinion, because prices are rising far more than wages and salaries.

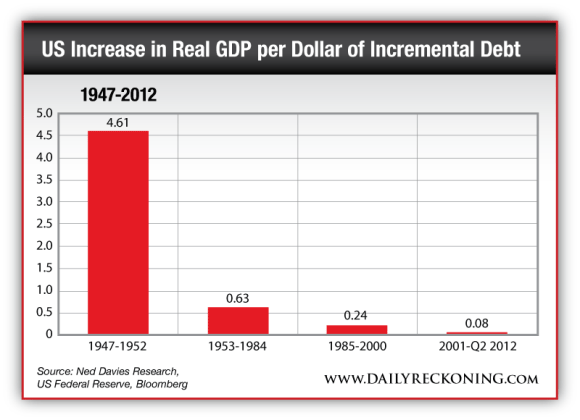

Moreover, the Fed wants to stimulate credit growth with its artificially low interest rates. But again, credit growth has largely lost its impact on the real economy. The multiplier on GDP of an additional dollar of debt is now negligible.

I suppose that the conclusion we can draw from it is that the larger the debt as a percentage of the economy becomes, the less will be the impact of an additional dollar of debt. I actually think that there is a tipping point where additional debt has a “contractionary” effect on the economy, because at this tipping point, the debt becomes so large that interest rates will increase no matter how much a central bank monetizes the debt. (Subsequently, inflation accelerates and the currency collapses, which leads, contrary to Mr. Bernanke’s view, to a general impoverishment of the population.)

But as I contended before, the probability that we have embarked on permanent asset purchases by the Fed is very high (until QE99 — or at least until the system breaks down, as just outlined).

Given my negative outlook for the global economy, I believe that 10-year Treasury note yields could decline once again to between 2.2-2.5%.

To Mr. Bernanke’s credit, and to be fair to him, I need to point out that his economic sophism is shared by most central bankers around the world. We can see that the global monetary base has exploded more than fourfold since 2003. These universally common monetary policies are, of course, applauded by fund managers, bankers and the investment community, all of which benefit (including myself) from rising asset prices. (Within 24 hours of the Fed’s announcement that there would be no “tapering,” the value of my assets increased by about 3%.)

But what is good for me as an asset holder doesn’t imply that it is the right monetary policy for the economy and for society as a whole. (Bill de Blasio’s policy of increasing taxes on high-income earners is a direct consequence of the growing wealth and income inequality brought about by expansionary monetary policies.)

For investors, the challenge is the following. Despite record buying of Treasuries and mortgage-backed securities, since September 2012, interest rates are up, not down. This proves clearly that the Fed is not all powerful.

Similarly, commodities and precious metals are still well below their peaks. The majority of stock markets around the world are well below their peaks, as are the majority of stocks in the U.S. In other words, it is not likely that the Fed and other central banks can boost further all asset prices, since this would require them to accelerate the expansion of the balance sheets ad infinitum.

The global monetary base expanded at 35% in 2009. Thereafter, its growth slowed to an annual rate of 10% in early 2012. The global monetary base expansion then re-accelerated to an annual rate of over 20% in late 2012. However, it has since slowed to an annual growth rate of around 5%. Simply put, even without tapering, there is a relative tightening of the turbocharged monetary expansion.

Above, I mentioned that the Fed has lost control of the bond market. Now let us consider two extreme cases of monetary policies: The Fed announces an immediate stop of its asset purchases (policy A), or it announces an immediate increase in its asset purchases to $200 billion monthly (policy B). How would the bond market react to these announcements, and what would the subsequent performance be? I suspect that on the announcement of policy A, the bond market would sell off for a day or two.

But then the bond buyers would figure out that no asset purchases by the Fed would likely be somewhat deflationary and, therefore, beneficial for bonds. The announcement of policy B would likely lead to an immediate bounce in bond prices (though likely not a new high) and likely not to a new low in interest rates. In fact, I would assume that if the Fed’s and other central banks’ balance sheets were to expand forever at a rapid pace, the bond market would tank.

…even without tapering, there is a relative tightening of the turbocharged monetary expansion.

For what it’s worth, when yields on the 10-year U.S Treasury note rose toward 3% I bought some of the notes. Sentiment was extremely bearish (small traders were heavily short the bond market) and I thought that “tapering” (I expected $10-15 per month) would be favorable for the bond market. I was wrong in my assumption, but right about buying the notes, since they rallied subsequently. That’s the confusing world of investments we live in. Given my negative outlook for the global economy, I believe that 10-year Treasury note yields could decline once again to between 2.2-2.5%.

However, longer term, I remain bearish about bonds. Yet there is one point we need to consider. Is it wise to sell U.S. bonds of America? Its “Bank of America, Merrill Lynch (BofAML) private client flow data” shows a complete aversion to bonds and a strong appetite for equities.

According to BofAML’s chief investment strategist, in the week ended Sept. 11, 2013, private investors put $14.3 billion into equity mutual funds and withdrew $3.5 billion out of bonds. (It was the largest weekly move out of bonds in the last three years.) I am raising this question because, based on current U.S. stock valuations, the future returns will be relatively small.

According to Robert Shiller’s current P/E ratio, the five-year expected return will be 4% and the 10-year return just 1%. In the near term, I was also concerned that stocks had become extremely overbought following the strong rebound from their late August low, and that the current advance had not been confirmed by numerous technical indicators. From the Aug. 28 low at 1,627, the S&P 500 rose in a straight line to 1,729 on Sept. 29 (by 6.3% in three weeks, or by more than 100% when annualized).

As a reminder, the S&P 500 is also up 61% from its Oct. 7, 2011, low at 1,074 (two years). So I can understand why the phones are ringing at BofAML’s retail offices from clients who want to switch their funds out of bonds into equities. But this doesn’t imply that equities are a good value at present.

I want readers to perfectly understand that when I recently bought my Treasury notes yielding over 2.9%, I didn’t think they were of particularly good value either. But within my asset allocation of 25% of total assets in emerging market bonds and cash, I held a lot of dollar cash, which was in the banking system and yielding next to zero. So by moving some cash into 10-year Treasury notes, I gained some additional income and a higher level of security (at least for now) as compared with holding bank deposits.

I should also mention that according to Shiller’s current P/E ratio, the five-year expected return for emerging market equities will be 19% and the 10-year return 13.8%. I have to say that I consider these emerging market return expectations to be completely unrealistic. Given my negative outlook about the Chinese economy, which I have outlined in earlier reports, I think that emerging markets’ returns could be as low as zero (or even less) for the next few years.

As James Burgh, a British Whig politician who stood up for “free speech” (1714-75), observed: “In prosperity, prepare for a change; in adversity, hope for one.”

Faber: The Feds Next Move To $1 Trillion

Marc Faber, publisher of The Gloom, Boom & Doom Report, told CNBC on Monday that investors are asking the wrong question about when the Federal Reserve will taper its massive bond-buying program. They should be asking when the central bank will be increasing it, he argued.

“The question is not tapering. The question is at what point will they increase the asset purchases to say $150 [billion] , $200 [billion], a trillion dollars a month,” Faber said in a “ Squawk Box ” interview.

The Fed-which is currently buying $85 billion worth of bonds every month-will hold its October meeting next week to deliberate the future of its asset purchases known as quantitative easing .

(Read more: Treasury yields will still spike to 5%: Societe Generale )

Faber has been predicting so-called “QE infinity” because “every government programthat is introduced under urgency and as a temporary measure is always permanent.” He also said, “The Fed has boxed itself into a position where there is no exit strategy.”

The continuation of Fed bond-buying has helped support stocks, and the Dow Jones Industrial Average (Dow Jones Global Indexes: .DJI) and S&P 500 Index (^GSPC) are coming off two straight weeks of gains, highlighted by record highs for the S&P.

While there may be little inflation in the U.S., Faber said there’s been incredible asset inflation. “We are the bubble. We have a colossal asset bubble in the world [and] a leverage or a debt bubble.”

Back in April 2012, Faber said the world will face “massive wealth destruction” in which “well to-do people will lose up to 50 percent of their total wealth.”

In Monday’s “Squawk” appearance, he said that could still happen but possibly from higher levels because of the “asset bubble” caused by the Fed.

“One day this asset inflation will lead to a deflationary collapse one way or the other. We don’t know yet what will cause it,” he said.

More from Marc: Bond Burglars to Bring Bears Out of Hibernation

The United States of America are in a terrible, terrible situation. We are saddled with a government comprised of anti-American Marxists who hate our freedom and everything America used to stand for. This cadre of traitors seeks nothing less than to “fundamentally transform” America from a free nation of citizens into a slave nation of serfs. To do this, their every move since the Obama administration took office has been calculated to destroy the middle class backbone of our nation. A strong, vital middle class is a bulwark for any free nation, and therefore is an obstacle and impediment to the communistic goals of Obama and his gang of governmental thugs.

The United States of America are in a terrible, terrible situation. We are saddled with a government comprised of anti-American Marxists who hate our freedom and everything America used to stand for. This cadre of traitors seeks nothing less than to “fundamentally transform” America from a free nation of citizens into a slave nation of serfs. To do this, their every move since the Obama administration took office has been calculated to destroy the middle class backbone of our nation. A strong, vital middle class is a bulwark for any free nation, and therefore is an obstacle and impediment to the communistic goals of Obama and his gang of governmental thugs.

A good example of this is the ObamaCare debacle. The whole point to this program is to impoverish the middle clases by requiring them to spend onerous amounts of their money buying more expensive health insurance, while simultaneously subsidizing the “Free Stuff Army” half of the country that voted for Obama. Meanwhile, the calculated effort of the Left is toward the failure of ObamaCare, so that it can be replaced by something even worse—single payer socialized medicine in which the government completely controls health care access for most people and the only folks who can obtain “gold star” private health care are the very rich (i.e., like the “elite” in Washington and their buddies in the news media and Hollywood). Just look at the current issues with the Healthcare.gov website rollout, which has been an absolute disaster. I strongly suspect that this has been purposeful, intended to frighten people into demanding that ObamaCare be scrapped…to be replaced with the single-payer system the left-wingers have wanted all along. If the middle classes can be forced into a single-payer system, then they will be fleeced to pay for it, seeing their wealth frittered away, while the health care sword of Damocles is held over their heads lest they get out of line (“You’re a member of the Tea Party? I’m sorry, the doctor won’t be able to see you…”)

Yet, for American left-wingers, the relatively slow process of bilking the middle classes out of their aggregated wealth is not quick enough to solve the various “revenue deficit” problems that keep them from spending even more on expanded government projects to take away even more freedom. What would work much more quickly would simply be to directly confiscate the wealth of the middle classes by taking over their savings and investment. And that, while unthinkable for most of American history, appears like it may be on the horizon.

An astute reader sent me a link to an article that appeared last week in Natural News, in which the author warns us about impending changes to banking capital controls (i.e. how you can move your money around and where) are being put into place that appear calculated to allow the U.S. government to more easily nationalize private funds contained within our banking system,

“This is the beginning of the capital controls we’ve been warning about for years. Throughout history, when governments are on the brink of financial default, they begin limiting capital controls in exactly the way we are seeing here.

“Following that, governments typically seize government pension funds, meaning the outright theft of pensions for cops, government workers, etc., is probably just around the corner.

“Finally, the last act of desperation by governments facing financial default is to seize private funds from banks, Cyprus-style. The precedent for this has already been set in Cyprus, and when that happened, I was among many who openly predicted it would spread to the United States.

“This is happening, folks! The capital controls begin on November 17th. The bank runs may follow soon thereafter. Chase Bank is now admitting that you cannot use your own money that you’ve deposited there.”

The author of this piece, Mike Adams, is absolutely right in his warnings. As he pointed out, what is being proposed here is not some pie-in-the-sky, far out wacko conspiracy theory. Instead, it has already happened elsewhere, with Cyprus being the most recent and well-known example. Cypriots , who thought their money was safe in the banks, woke up to find one day that they could no longer access their own money, it was locked in the banks, and the reason for this was so that their government could grab it without worrying about people withdrawing it ahead of time.

…..continue article at Canada Free Press HERE

The US Share Market has a turning point in November so we could get a temporary high with a retest of support followed by a breakout to new highs thereafter again. The Jan/Feb period is showing already and the debt ceiling issue will come up once again. Our computer is starting to show a bit more chaos in many markets forming for the first quarter of 2014.

We are still within the uptrend channels and this shows resistance at 16950 level with support at the 13748 area, A closing above 13700 for year-end will leave this index in a positive position for next year.

Today, a closing 15438 will keep the index positive but some resistance stands at 15679. A weekly closing above that should signal new highs into as late as the 2nd week of November.

Capital will have no choice but to flee to equities. The minimum target objectives remain 17000 and 21000 by 2015.

More from Martin Armstrong:

Hyperinflation Question

Gold Questions:

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair