Mike's Content

Michael goes after the huge trend that is eliminating one of the great barriers to new business success.

Michael goes after the huge trend that is eliminating one of the great barriers to new business success.

{mp3}mcbuscomnov8fp{/mp3}

Four reasons to waste your time with the deeply historic, deeply human value ascribed to gold.

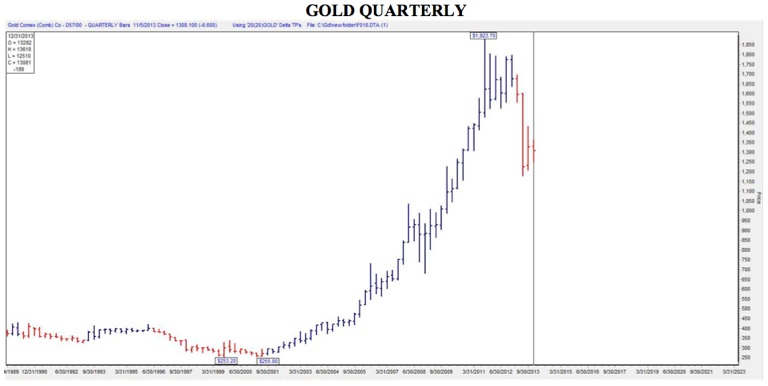

People love to debate, but sadly sometimes it crosses a line and turns argumentative. That’s what is happening right now with the debate over gold.

There have been several high-profile articles, most recently in the Wall Street Journal, saying you should eliminate gold as a worthwhile part of your portfolio, primarily because of this year’s lower price.

Against that idea, many bloggers and private investors, wondering why gold priceshave fallen, say that it shouldn’t have dropped, that there must be some conspiracy driving down prices when money-printing and our still-weak economy should be driving gold higher. But that still puts current price performance front and center in the debate over whether it should or shouldn’t feature in your portfolio. So it misses several key points about why gold is uniquely valuable as an investable asset.

We’d like to look here at some of the common arguments now offered for why gold should not figure in your investment strategy. Yes, working at BullionVault, the physical gold and silver exchange, we’re biased. But there are also people who always say gold doesn’t warrant your investment dollars.

To have any intelligent understanding of your own position, you need to welcome debate. That way you can challenge your own opinions and, if you find they’re correct, improve your arguments, too, such as whether gold investing continues to warrant attention.

1. Gold Does Not Yield Anything

When you buy any commodity outright. you can no longer deposit it with a bank or investment company to earn interest. If you are looking to yield a dividend or interest, then physical gold ownership will not yield anything. Yet that is only half the story.

Gold ownership yields security for the investor, the type of security a person seeks from insurance. It is the only physical form of insurance that exists to counterweight your investments in bonds and stocks, and that is also a liquid, easily traded asset. Gold is also noncorrelated with those more “mainstream” markets, meaning that its price moves independently of where other investment prices are heading. So the goal for most investors in holding gold is first as a safety net for their other assets. This metal has held value for thousands of years, and will hold value for thousands more.

2. Gold Is Worth Only What the Next Investor Will Pay for It

This statement is weak from the onset. There are no stocks, bonds, commodities or goods that are worth more than the next person will pay. That being said, gold has something that the others do not. Gold is 100% transparent, in that, unlike other easily traded investments, it is only one thing: a pure and precious rare commodity that requires little space for storing great value.

This commodity has acted as money for thousands of years. In fact, after World War II, the Bretton Woods agreement used gold to bring stability and sanity to the world’s currency markets once more. If that history of human use doesn’t give intrinsic value to gold, why would you give that title to any other asset?

People had their life savings in Lehman Brothers stock. Other people invested in mortgage-backed securities or were holding Argentine bonds or got sold the claims ofBernard L. Madoff Investment Securities LLC.

Stocks and bonds, though there are many facts available about them, are never 100% transparent. It is much like a hiring a baseball player. You may have his statistics and you may place him in the perfect spot on the best team in the league. Yet he may perform poorly due to an unknown injury or a problem with the change of venue or any other number of unknown reasons. This is the same for stocks and bonds. Though we have their statistics, we never know when some problem may cause some of these instruments to fail.

3. Gold Is Neither a Good Hedge for Stocks, Nor Inflation

Anyone looking at the 1980s and ’90s and concluding that gold is a poor inflationhedge misses the point. You didn’t need an inflation hedge when cash in the bank paid 5% above and beyond the rate of inflation each year, as it did on average for U.S. and U.K. savers for the last 20 years of the 20th century.

But gold doesn’t make a good hedge for stock market investments either, according to a long-running thread of comment. The frequent comparison is usually to the stock market overall, or the Dow Jones industrial average. Never mind that gold and stocks have, over extended periods, gone in opposite directions. That measure is not a just number to use, because the stock indexes frequently change. This is also true of the overall market, where stocks are delisted if they underperform or go bankrupt. If these types of stocks were kept on, how would the indexes and averages have changed? The stock market of 1989 did not have the same listed companies as that of 1996, 2000 or 2013.

In contrast, the gold of 1989 was the same gold of 1996, 2013 and even 2000 BC. Gold does not change, and its supply cannot be expanded (or reduced) at will. This is why gold functions so well as a form of exchange and transfer of value. It holds value due to its permanent unchangeable form. World history has shown us again and again that in the final analysis; only gold, out of all investable assets, holds value in catastrophic situations.

You can lose value owning gold if you buy high and sell lower, but you never lose it all. You could easily pick out a point in any chart of the stock market where an investor could have bought and then another time where you may have sold and lost money. There is no point to this kind of example, because it never speaks to an individual’s overall performance with their assets. They may have liquidated their stock at the low price because they needed the cash to invest in a particular business or real estate opportunity. All assets including gold have to be looked upon as part of a strategy for the investor and not as independent pieces of life’s asset management puzzle.

4. Gold Is an Article of Faith, Not Rational Investing

Some people denigrate gold to a relic of the past in terms of its economic importance. The most recognized of today’s detractors is perhaps Nouriel Roubini, the famed NYU economist who repeats John Maynard Keynes’ cry of the 1930s that gold is a “Barbarous Relic”. Still others go further, saying that choosing to own investment gold is anti-social. The argument is that there is no longer any need for gold as a form of exchange, nor as a store of value. Governments and central banks have done away with the need for gold. So apparently, gold’s only value today lies in the jewelry and electronics trades.

In addition, other analysts write about gold being a faith-based investment and mock it as a type of religion. There are certainly those who invest on faith, and they can be loud, giving the impression that investors in gold are extreme. But this can also be said about the defense of the U.S. Dollar. That currency in the end is only a piece of paper that has no other use than that ascribed by the government. If you put fire to a dollar bill it will turn to ashes and float away. But if you put fire to gold, at the right temperature, you get a liquid metal that not only is useful to the arts but important in the electronics and high-technology industries.

“We may one day become a great commercial and flourishing nation,” wrote George Washington, the first president of the United States of America, on the subject of paper money in a letter to Jabez Bowen, Rhode Island, on Jan. 9, 1787. “But if in pursuit of the means we should unfortunately stumble again on unfunded paper money or similar species of fraud, we shall assuredly give a fatal stab to our credit in its infancy.

“Paper money will invariably operate in the body of politics as spirit liquors on the human body. They prey on the vitals and ultimately destroy them.”

It is difficult for those in power to try to overcome this truth, embodied by all of recorded economic history. And it becomes more ludicrous as governments also hold gold bullion in vast amounts.

The modern central banking system, now more than 100 years old, may seem to shape this perception. Yet in the last decade, central bankers themselves, albeit in Asia and other emerging economies, have been significant buyers of the yellow metal. Western governments as a group have stopped selling gold.

Why? Economic chaos causes distrust among governments and central banks, leading those in power to seek out avenues to strengthen their position with other parties. The position central banks look for to strengthen their balance sheet and ensure their place in the global economy is gold. The United States rose to dominance worldwide alongside its dominant gold reserves. Now becoming a market economy, and hoping to become the next big global economy, China is also building its central bank gold reserves. It becomes obvious that gold has a very deep, very human value, ascribed to it by history and by all major powers today.

Value isn’t the same as price, of course, which explains, perhaps, how gold investing remains such a mystery to some people.

Adrian Ash is head of research, and Miguel Perez-Santalla is vice president of business development for BullionVault, the physical gold and silver exchange founded a decade ago and now the world’s No. 1 provider of physical bullion ownership online. There you can buy fully allocated bullion already vaulted in your choice of London, New York, Singapore, Toronto or Zurich for just 0.5% commission today.

Here are today’s short punchy videos, roughly 1.25 minutes each – Ed

Silver Money Flow Action Chart

GDXJ Stokes Oscillator Update Chart

Thanks,

Morris

Unique Introduction For Web Readers: Send me an email to alerts@superforcesignals.com and I’ll send you 3 of my next

Super Force Surge Signals free of charge, as I send them to paid

subscribers. I’ll also send you my free “US Dollar Debt Clock” report. Thank you!

By a 60-Year Market Veteran –

With continued uncertainty in global markets, a 60-year market veteran sent King World News an absolutely incredible piece discussing the terrifying big picture. He also included some fantastic commentary to go along with seven key charts and illustrations. Below is six-decade market veteran Ron Rosen’s extraordinary piece.

November 7 (King World News) – “The Terrifying Big Picture”

It’s easy to see that ever since the year 2000 gold bullion has been in a bull market and the S&P 500 has been in a megaphone pattern bear market. Gold has dramatically increased in price while the S&P 500 has done nothing but go up and down. The Fed’s QE’s, plus a twist, are placed on the chart of the S&P 500. They inform us of when the Fed believed it had to goose the economy and the markets in order to keep them from collapsing. OK, but what’s next? Will gold keep going up? Will the S&P 500 head down again?

Well, we now have a pretty good idea that the Fed will continue doing QE’s as far into the future as they can see….

That may or may not be very far. The general expectation is that if the Fed continues to do QE’s, the Stock averages will continue to move up. We know that gold is in a long-term bull market. The S&P 500 and the DJIA, if left on their own, would normally begin a leg E collapse at this time (see right hand side of chart below).

Continue reading the Ron Rosen piece HERE

On December 20, 1922, a surveyor — J.G. Tierney — made his way along the Colorado River by barge. Tierney, who worked for the U.S. government, was surveying a remote spot in the Mojave Desert called Boulder Canyon.

Boulder Canyon sits in the middle of some of the most unforgiving land in America.

During the summer, temperatures frequently top out near 120 degrees. Less than five inches of rain fall each year. Rattlesnakes and scorpions hide under rocks. And the sharp cliffs are near-impossible to scale.

And yet, this canyon in the heart of the desert holds one of the greatest investments in U.S. history… one that has generated billions of dollars in wealth and is practically guaranteed to keep doing so for decades.

But it wasn’t without its costs. In total, 112 men — beginning with J.G. Tierney, who on that December day drowned after falling off the barge that carried him and his equipment — died to create this investment.

I’m talking about Hoover Dam.

I’m talking about Hoover Dam.

Before I get too far… no, I am not recommending that you invest in the Hoover Dam. Even if you wanted to, it’s fully owned by the U.S. government. There’s not a stock you can buy that gives you access.

Instead, it’s what Hoover Dam represents that is the true opportunity to grow your wealth.

Let me explain…

Hoover Dam (originally called Boulder Dam) was finished in 1936, at which point it began damming the Colorado River to create Lake Mead — the United States’ largest reservoir.

The project was massive. At its peak, more than 5,000 people worked on it at the same time. And the dam contains enough concrete to pave a two-lane highway from San Francisco to New York City.

In total, construction costs came to $49 million.

That $49 million investment is the sole reason why millions of people are able to live in the Las Vegas area today. And it has generated billions of dollars of wealth in the process.

But Hoover Dam didn’t just create a massive reservoir to provide water to the middle of the desert. It also created one of the most lucrative electricity generation plants ever built.

Located in the base of the dam are 17 hydroelectric turbines that make up the Hoover Powerplant. These turbines generate roughly 4.2 billion kilowatt hours (kWh) of electricity per year, making it one of the largest hydroelectric plants in the United States.

Electric providers love hydroelectric power because it’s among the cheapest power sources on the planet. Hoover Powerplant sells its electricity on the wholesale market at just 1.6 cents per kilowatt hour. In comparison, Las Vegas residents pay an average of 11.6 cents per kWh for electricity — seven times as much.

But even at that low cost, Hoover Dam generates and sells about $63 million in electricity every year (1.6 cents x 4.2 billion kWh) — that’s nearly 130% of what it cost to build the dam in the first place.

Of course, there are a number of other costs such as maintenance and upkeep that figure into the equation, but the point remains — Hoover Dam has become one of the greatest individual investments ever made by the U.S. government. And it continues to increase its return year after year.

So how can this help us as investors? After all, as I mentioned earlier, you can’t invest directly in Hoover Dam.

You simply have to understand why Hoover Dam has been such a success…

Hoover Dam is what I like to call an “irreplaceable asset.”

No one can come along and build a competing dam. And the world isn’t going to run out of a need for electricity. If anything, we’ll need more electricity in the future.

That’s why even 76 years after it was built, the dam is more important today than ever.

And while you can’t invest in Hoover Dam, there are dozens of irreplaceable assets around the world — including many hydroelectric dams — that you can invest in.

And as you would expect, investing in these irreplaceable assets has proven to be extremely profitable.

Take oil and gas pipelines, for example. Pipelines are the ultimate irreplaceable assets. Another company can’t simply build a pipeline next to an existing one. And the pipelines that carry fuel, natural gas, oil, and other commodities across the country aren’t about to be replaced by some new technology.

That’s why I’ve loaded up on pipeline operators, which are typically structured as master limited partnerships (MLPs), in my Top 10 Stocks portfolio.

In fact, pipelines have been one of the strongest corners of the market for years. The benchmark for master limited partnerships — the Alerian MLP Index — has returned 328%, including dividends, during the past decade… or almost 16% a year. That’s over three times the S&P 500’s 10-year performance.

But there are more irreplaceable assets than just pipelines.

Take my investment in Brookfield Infrastructure (NYSE:BIP). Brookfield owns toll roads, electricity transmission grids, ports, and railroads all over the globe. All of these are irreplaceable assets. And they continue to earn a steady stream of cash for BIP and its investors.

This is exactly why I added the shares to my Top 10 Stocksportfolio more than two years ago. And it’s why the stock is one of my biggest winners — up 67% in just over two years while paying a yield of 4.4%.

Don’t get me wrong, there are no guaranteed winners in the investing world. Any investment can fall in value. But when you find the sort of securities that give you access to irreplaceable assets, they often end up being some of the most lucrative investments to own for the long term.

Note: It’s no surprise that our “Top 10 Stocks For 2014” report lists several companies that own irreplaceable assets, helping many of these companies dominate or even monopolize their markets. These cash-rich stocks not only throw off dividend yields twice as high as the S&P 500, they also handily outperform it. Through 2012, our annual list of Top 10 Stocks have beaten the market 7 out of 10 years. Visit this link to get all the details…

Good Investing!

Elliott Gue

Top 10 Stocks

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair