Currency

Crash Proof Your Portfolio

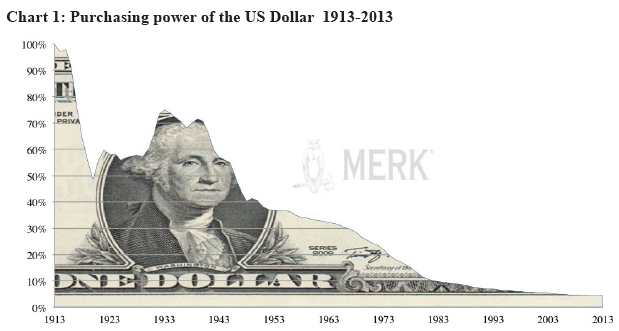

The U.S. debt burden and accommodative monetary policy may be exerting downward pressure on the U.S. dollar. The stock market may be in bubble territory. Bond fears abound. Where can one hide: where to invest to both Profit and Protect?

….read Where & How HERE

Wowee! More highs in the stock market. The Dow rose 128 points yesterday.

Wowee! More highs in the stock market. The Dow rose 128 points yesterday.

Is the US stock market headed for a bubble? Maybe… but what do we know?

Our guess is that the people who are buying stocks today have a lot more confidence in the Fed than we have. As near as we can tell, today’s stock prices owe a lot to the Fed’s manipulation of asset prices and little to the fact that the companies are more intrinsically valuable… or more likely to produce higher earnings per share.

In fact, as Chris reported yesterday, earnings-per-share estimates have been falling as US stocks have been rising.

Watch out. Artificially priced markets are like huge bungee cords. You can stretch them out. But the further they get pulled out, the greater the sting when they snap back.

When will that happen? We don’t know that, either. But we’re not going to stand in front of it waiting for it to happen.

There are two groups of people in the world.

In one group are those who think they know things. In the other are the people who think those in the first group are idiots.

These are not absolutely separate categories. Instead, they share a long border and plenty of spots for crossing under cover of night.

Aristotle was perhaps the first and foremost of those who thought he knew something. He had it all figured out more than 2,000 years ago. There was a natural order to things, he thought.

Civilized people should live in city states; anyone beyond the city walls was either a “beast or a god.” And the city state itself – the ideal form of political organization – was to be ruled by… well… the rulers.

That was just the way it worked. Aristotle: “For ruling and being ruled are not only necessary, they are also beneficial, and some things are distinguished right from birth, some suited to rule and others to being ruled.”

Why a city state and not a country state? Why couldn’t people rule themselves? Who was to say who the ruler should be?

You could ask as many questions as you wanted. Aristotle would have just as many silly answers. But even the ancients were on to him.

“None of us knows anything, not even whether we know anything or not,” said Metrodorus of Chios, aiming for Aristotle’s head.

But it was the great Pyrrho from Elis who developed the philosophy we know today as “skepticism.” Loosely, a skeptic is someone who suspects that other people don’t know nearly as much as they think they do.

And loosely speaking, the skeptics are mostly right. When it comes to central banking and central economic planning, they are always right.

The planners and world improvers are reliable sources of amusement, and not much more.

Tom Friedman, Ben Bernanke and Paul Krugman reduce the sum of human wisdom every time they open their mouths. Bernanke thinks he can solve a debt problem… with more debt.

Krugman thinks he can solve a spending problem with more spending. Friedman doesn’t think at all. But that doesn’t stop him having a solution for every problem. (And if you applied his solution, you’d have a much bigger problem.)

Our old friend Pierre Lemieux reminds us of Adam Smith’s comment:

The man of system […] is apt to be very wise in his own conceit, and is often so enamored with the supposed beauty of his own ideal plan of government, that he cannot suffer the smallest deviation from any part of it.

He goes on to establish it completely and in all its parts, without any regard either to the great interests or to the strong prejudices which may oppose it: he seems to imagine that he can arrange the different members of a great society with as much ease as the hand arranges the different pieces upon a chessboard; he does not consider that the pieces upon the chessboard have no other principle of motion besides that which the hand impresses upon them; but that, in the great chessboard of human society, every single piece has a principle of motion of its own, altogether different from that which the legislature might choose to impress upon it.

The idea that you can organize a society according to your own prejudices is ancient. Old, too, is the notion on which it depends: that you have some knowledge that others don’t.

In fact, all you know is what everyone else knows: nothing! And we’re not even sure about that.

Regards,

Bill

More from Bill:

Repeat After Me: Economics Is NOT a Science

Mike Campbell: Is the Twitter IPO a foreshadowing of the new dotcom bubble or just a continuation of the Social Networking Revolution?

Mike Campbell: Is the Twitter IPO a foreshadowing of the new dotcom bubble or just a continuation of the Social Networking Revolution?

Quick Facts

- 1.15 billion Facebook users

- The +1 button is served 5 billion times per day (surely this post is worthy of a plus one.)

- 343 million active users on Google+

- 238 million linkedin users

- 232 million Twitter users

- 130 million Instgram users

- 4.2 billion people use mobile device to access social media

- There are over 10 million facebook aps

- 250 billion photos are uploaded every day

- 500 million tweets are sent a day

- There are over 1 billion unique monthly visitors on YouTube

Mike

“Normalization Of Long-Term Yield Is Inevitable”

The exact starting point and pace of tapering does not matter very much at all. As long as you believe that QE will end at any time within the next three years, the 10Y Treasury Note and virtually all long-term bonds are severely overvalued and constitute bad investments.

Normalization Of Long-Term Yield Is Inevitable

By definition, the end of QE implies economic normalization. Economic normalization implies annualized real GDP growth of 2.5%-3.0% and CPI of 2.0%-3.0%. In turn, this implies 10Y US Treasury yields in the range of 4.5%-5.5% based on historic norms.

There is every reason to believe that 10Y yields will reach or surpass this normal range for 10Y yields when the Fed ends QE. First, it is important to note that the current 10Y yield of 2.69% is a product of extreme levels of intervention by the Fed; the Fed has purchased and now holds 49% of all US Treasury bonds outstanding with a maturity of 10-15 years. This extreme level of Fed manipulation has had a major impact on long-term yields, and ending the manipulation can be expected to have an equal and opposite effect. Second, by the time economic conditions normalize, the risks of owning US Treasuries will be higher than ever. At that particular point in time, the deterioration of long-term US fiscal fundamentals and the risks associated with them will be at all-time highs. Furthermore, at that particular point in time, the historically unprecedented level of excess liquidity in the economy combined with a normalized level of risk aversion and liquidity preference (associated with a normal economic growth rates) suggest that inflationary risks will be at extraordinarily high levels.

A 10Y Treasury note yielding 4.5%-5.5% any time in the next three years implies a capital loss in the order of 12%-20%+ for holders of those bonds. The yield differential between the 10Y which is currently yielding 2.69% and safe short-term alternatives yielding 0.5%-1.0% simply do not compensate the prospective capital loss and/or the opportunity cost of holding 10Y Treasury notes – even if you assume interest rate normalization will take another three years.

The Fed has warned you: QE is coming to an end. It may not happen in mid-2014 as originally targeted by the Fed. But QE will come to an end one way or another – most likely within the next 1-2 years. It will come to an end either because of a normalization of economic growth and employment conditions (optimistic case) or because the unprecedented levels of excess liquidity in the economy and their related distortions in asset and/or product markets force the Fed to end QE “prematurely” (pessimistic case).

Take Action Now: Sell Bonds Into Strength

Traders and hedgers have been caught wrong-footed by the Fed’s taper surprise. As a result, bonds should experience a brief rally based on short covering. However, this rally is likely to be very short-lived as longer-term bondholders are aware that the math is working against them. Many large bondholders are going to be selling heavily into this short-covering rally, so the rally is unlikely to go very far or for very long.

So what are you waiting for? Don’t look a gift horse in the mouth. The market is providing you with what may be your last opportunity to get rid of fixed income duration in your portfolio. Investors should take advantage of the sharp rally to sell out of all long-term duration in their portfolios. Sell long-term government and corporate bonds, long-term bond funds. Sell all ETFs such as TLT, IEF, AGG, JNK and HYG.

Long-term implications for equity indices such as the S&P 500 and index ETFs such as SPY are more ambiguous. Stocks never truly priced in treasury yields at their lows. Therefore, it is not clear that movements in long-term interest rates will have a significant effect on equities as a whole. However, dividend sensitive sectors such as REITs, mREITs and utilities may be more affected

So it would seem to me that Karl Marx might prove to have been right in his contention that crises become more and more destructive as the capitalistic system matures (and as the “financial economy” referred to earlier grows like a cancer) and that the ultimate breakdown will occur in a final crisis that will be so disastrous as to set fire to the framework of our capitalistic society.

So it would seem to me that Karl Marx might prove to have been right in his contention that crises become more and more destructive as the capitalistic system matures (and as the “financial economy” referred to earlier grows like a cancer) and that the ultimate breakdown will occur in a final crisis that will be so disastrous as to set fire to the framework of our capitalistic society.

Not so, Bernanke and co. argue, since central banks can print an unlimited amount of money and take extraordinary measures, which, by intervening directly in the markets, support asset prices such as bonds, equities and homes, and therefore avoid economic downturns, especially deflationary ones. There is some truth in this. If a central bank prints a sufficient quantity of money and is prepared to extend an unlimited amount of credit, then deflation in the domestic price level can easily be avoided, but at a considerable cost.

….read Faber’s Real US Economy Trampled by White Elephants HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair