Stocks & Equities

“I continue to think that this bull market will end in an upside explosion. I believe it is fated to go higher than anybody now believes. A wise move here might be buy the farthest out calls as possible on the thesis that the sellers are convinced they will never be hit. Wise heads are now warning that this market has now passed all sane appraisals, and as such it is highly dangerous. Nevertheless I believe that this market is fated to go higher than even the most bullish practitioners can conceive.

“I continue to think that this bull market will end in an upside explosion. I believe it is fated to go higher than anybody now believes. A wise move here might be buy the farthest out calls as possible on the thesis that the sellers are convinced they will never be hit. Wise heads are now warning that this market has now passed all sane appraisals, and as such it is highly dangerous. Nevertheless I believe that this market is fated to go higher than even the most bullish practitioners can conceive.

Reading my favorite advisories, they are overwhelmingly bearish, from the standpoint of the usual technicals, including the margin accounts, and the number of bullish advisories vs. the thin bears. All this aside, my instinct tells me that the stock market is heading into the clouds … I sense that the retail public is moving toward an extreme of bullishness, and that all negative indications will be swept aside. This bull market will not end with the usual and obvious technical indications. It will end with an extreme of bullishness from the crowd.

I note that talk about debt has simmered down. The US debt is so huge that reasonable talk about it is almost impossible. I believe in the end the US will turn to hyperinflation in its effort to minimize the debt. The debt is now so huge that I believe there are only two possible outcomes: default or hyperinflation. With the advent of hyperinflation, gold will come into its own. In the end, those who have been patient enough to hold bullion will be rewarded. Ultimately, a new monetary system will come into being, and its core will be built around gold. I think it may be three to five years before this country moves into hyperinflation, but the only alternative is default.

The government will attempt to diminish our debt by way of printing, to the point of hyperinflation … The miracle of inflation diminishes the power of debt over time. In the face of America’s unbelievable debt, prepare for inflation, rising inflation and finally hyperinflation … For a period of this third phase, speculative positions in the DIAs should be profitable, but only for a short while. In the meantime, position in gold bullion and gold items should be held.”

The US Dollar surged higher last week and the major American stock indices hit New All Time Highs…as the ECB unexpectedly cut interest rates and the Americans reported much stronger than expected employment. Market Psychology, which had been bearish the Dollar and bullish the Euro, shifted to realizing that policies and actions by the Fed and by the ECB may be diverging in the weeks and months ahead. I liquidated my long US Dollar Index positions on Friday Nov 8 after a good two week run…but continue to hold other short currency positions Vs. the USD.

Market prices go up and down, in various time frames, as Market Psychology changes. I try to anticipate whether Market Psychology is going to extend or reverse market trends over whatever time frame I want to trade. For instance, if I think a market has gone up “way too far, too fast” I will watch for a sign that the market has turned down and I will get short…looking for a swift correction as over-leveraged positions are liquidated.

At a recent conference in Calgary, Alberta I used the acronym RAWCTER to describe my trading method…I Research the markets…read analysts, look at charts…I Anticipate what markets might do, but I Wait for a Confirmation that it is Time to Enter the market with the appropriate Risk controls. For instance, I watched the Euro rally (from 1.28 to 1.38) against the USD since the Fed’s “about face” on taper talk in July. My Research caused me to Anticipate that the Euro should be going down not up…but I had no Confirmation that it was Time to Enter the market with a short position so I Waited. As Time went by I Anticipated that the Euro had gone “way too far” (COT data, for instance) and was vulnerable to a sharp correction, or more, if there was ever a catalyst for a change in trend. In other words, I Anticipated a coming reversal in Market Psychology, but I Waited for the market to set-up…waited for some Confirmation that it was Time to Enter the trade…I respected what the Euro was doing…rising…even though I thought it should be falling.

Chart Section: 16 Charts Give Us Direction

US Dollar Index – Weekly: The USD had (circled) Weekly Key Reversals down in July 2012 and July 2013. The market had another WKR down in October 2013 and I thought that it was getting very over-sold as it approached chart support (red line) around the 7900 level. I Anticipated that it would turn around, but I Waited for a Confirmation that a rally might be starting.

US Dollar Index – Daily: I bought the USD two days after it bounced off the 7900 support level. I had Anticipated that the market was very oversold and due for a rally. Since I was “picking a bottom” to a strong downtrend I need clear Risk controls…so I bought only 50% of a normal position size and planned to bail out if the market made new lows. Prices ran into some resistance around the 8100 “support/resistance” level and the downtrend line from the three year highs made in July. The market spiked higher on the ECB announcement last Thursday but gave up more than half of its gains by the end of the day. The market rallied again Friday on the American jobs report but could not take out the previous day’s highs. So despite making gains on both Thursday and Friday I felt that the market was struggling…so I took profits on my long positions and return to the safety of the sidelines. From the sidelines I can now look at the market as an agnostic…without having to “defend” my positions. At the moment I’m predisposed to looking for a spot to buy the USD.

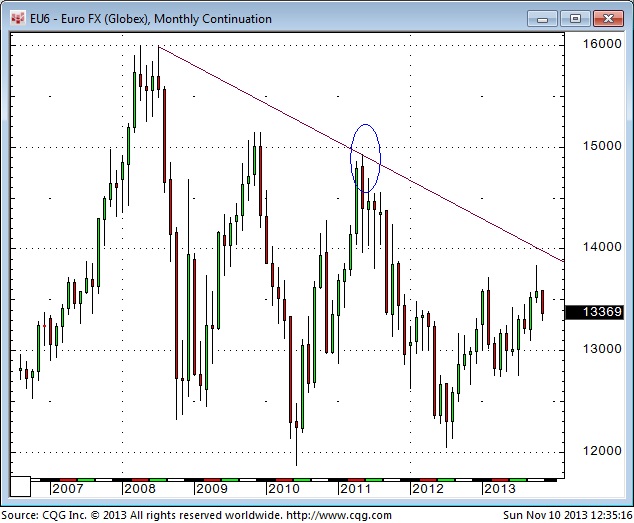

The Euro – Monthly: The Euro traded to All Time Highs in early 2008 and then fell sharply during the financial crisis as people everywhere sought the safety of the US Dollar. The circled area on the chart notes the high made in May 2011…a date I have frequently referred to as a Key Turn Date across a number of markets. The market has registered big price swings over the past few years…and seems to trending lower…

…view & read the other of 16 charts HERE

Just click on INTERACTIVE here or below….

Just click on INTERACTIVE here or below….

Want to know if your Twitter feed produces enough value to retire? Enter your username to find out!

Now that Twitter has a market capitalization of at least $24.9 billion, more than a few of the social network’s 230 million users have noticed their tweets are making other people rich. Many people want their cut.

So what would that be exactly? TIME has crunched the numbers. Plug in your username (or anyone else’s) below to find out how valuable your Twitter feed is.

The leader of the free world is owed $5,160,650, but he’s a small-timer compared with 19-year-old pop star Justin Bieber, who is due $20,916,384 thanks to his nonstop tweeting and devoted following.

How Much Does Twitter Owe Me?

Just click on and enter the twitter username into INTERACTIVE HERE (of ANY public account to measure its share of Twitter’s fortune).

WHOLESALE GOLD bumped up to $1285 Tuesday lunchtime in London, reversing an overnight drop to fresh 3-week lows at $1277 as European stock markets slipped with government bond prices.

“A slip through the six-month support line at $1270.16 will confirm our bearish outlook,” says Commerzbank’s Axel Rudolph.

“We could potentially,” says French bank Natixis’ precious metals analyst Bernard Dahdah, “see gold prices reach levels of $850 to $1,000. But this is our very low-case scenario.”

Gold prices that low could unleash a wave of forward selling by mining companies, says French investment bank BNP Paribas, with miners trying to lock in current prices for fear of further falls ahead.

“Producers, the share prices of which have not been faring well of late,” BNP’s commodity team notes, “might initiate and/or accelerate hedging were we to approach the symbolic $1000 level, adding supply to the market and further downward pressure to prices.”

Were gold to fall below that price, investment author and hedge-fund manager Jim Rogers told India’s ET Now TV last week, “I hope I’m smart enough to buy a lot more.”

Explaining why he’s not buying gold right now, “It went up 12 years in a row, which is highly unusual for any asset,” says Rogers. “And of course, India’s doing its best to kill the gold market.”

This month’s Diwali festival saw gold buying drop by more than one-third from 2012, according to retail dealers, thanks to the lack of supply caused by the Indian government’s anti-gold import rules.

Even with gold falling a further 3% in the wholesale bullion markets for November so far, “There’s little sign yet of a boost in physical demand,” says one Asian dealing desk.

“Gold is clearly lacking bullish conviction,” says another.

“With equities performing well,” agrees Scotiabank’s latest Metals Matters monthly, “and with the global economy looking more stable, investment demand for gold may well remain subdued.

“That could keep the lid on prices.”

Confidence levels amongst UK private investors rose in October for the third month running, says a survey from retail stockbrokers Hargreaves Lansdown, reaching a nine-year high with 8 in 10 respondents saying the stock market will rise again in 2014.

Market professionals have also “fallen into a state of relative complacency,” says bond-fund giant Pimco’s CEO Mohamed El-Erian, “comforted by the notion of a ‘central-bank put’.

“The result is financial risk-taking that exceeds what would be warranted strictly by underlying fundamentals.”

Contrasting with last week’s strong GDP and new jobs figures, the National Federation of Independent Businesses said Tuesday that its optimism index dropped 2.3 points to 91.6 last month, primarily due to the government shutdown.

Gold for UK investors had earlier turned higher from its 3rd dip below £800 per ounce this year as the British Pound sank on news of much weaker than expected consumer price inflation.

The news comes after strong GDP and other data raised expectations that the Bank of England could soon raise UK interest rates from their all-time low at 0.5%.

Adrian Ash

Gold price chart, no delay | Buy gold online

Adrian Ash is head of research at BullionVault, the secure, low-cost gold and silver market for private investors online, where you can fully allocated bullion already vaulted in your choice of London, New York, Singapore, Toronto or Zurich for just 0.5% commission.

Please Note: This article is to inform your thinking, not lead it. Only you can decide the best place for your money, and any decision you make will put your money at risk. Information or data included here may have already been overtaken by events – and must be verified elsewhere – should you choose to act on it.

The death of the dollar is coming, and it will probably be China that pulls the trigger. What you are about to read is understood by only a very small fraction of all Americans. Right now, the U.S. dollar is the de facto reserve currency of the planet. Most global trade is conducted in U.S. dollars, and almost all oil is sold for U.S. dollars. More than 60 percent of all global foreign exchange reserves are held in U.S. dollars, and far more U.S. dollars are actually used outside of the United States than inside of it. As will be described below, this has given the United States some tremendous economic advantages, and most Americans have no idea how much their current standard of living depends on the dollar remaining the reserve currency of the world. Unfortunately, thanks to reckless money printing by the Federal Reserve and the reckless accumulation of debt by the federal government, the status of the dollar as the reserve currency of the world is now in great jeopardy.

As I mentioned above, nations all over the globe use U.S. dollars to trade with one another. This has created tremendous demand for U.S. dollars and has kept the value of the dollar up. It also means that Americans can import things that they need much more inexpensively than they otherwise would be able to.

The largest exporting nations such as Saudi Arabia (oil) and China (cheap plastic trinkets at Wal-Mart) end up with massive piles of U.S. dollars…

The largest exporting nations such as Saudi Arabia (oil) and China (cheap plastic trinkets at Wal-Mart) end up with massive piles of U.S. dollars…

Instead of just sitting on all of that cash, these exporting nations often reinvest much of that cash into low risk securities that can be rapidly turned back into dollars if necessary. For a very long time, U.S. Treasury bonds have been considered to be the perfect way to do this. This has created tremendous demand for U.S. government debt and has helped keep interest rates super low. So every year, massive amounts of money that gets sent out of the country ends up being loaned back to the U.S. Treasury at super low interest rates…

And it has been a very good thing for the U.S. economy that the federal government has been ableto borrow money so cheaply, because the interest rate on 10 year U.S. Treasuries affects thousands upon thousands of other interest rates throughout our financial system. For example, as the rate on 10 year U.S. Treasuries has risen in recent months, so have the rates on U.S. home mortgages.

Our entire way of life in the United States depends upon this game continuing. We must have the rest of the world use our currency and loan it back to us at ultra low interest rates. At this point we have painted ourselves into a corner by accumulating so much debt. We simply cannot afford to have rates rise significantly.

For example, if the average rate of interest on U.S. government debt rose to just 6 percent (and it has been much higher than that at various times in the past), we would be paying more than a trillion dollars a year just in interest on the national debt.

But it wouldn’t be just the federal government that would suffer. Just consider what higher rates would do to the real estate market.

About a year ago, the rate on 30 year mortgages was sitting at 3.31 percent. The monthly payment on a 30 year, $300,000 mortgage at that rate is $1315.52.

If the 30 year rate rises to 8 percent, the monthly payment on a 30 year, $300,000 mortgage would be $2201.29.

Does 8 percent sound crazy to you?

….read page 2 HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair