Stocks & Equities

“Intermediate a sell – Long term bullish for all major world markets, including those of the U.S., Britain, Canada, Germany, France and Japan” – From “The Bottom Line” below

Todd Market Forecast for Wednesday November 13, 2013

Available Mon- Friday after 6:00 P.M. Eastern, 3:00 Pacific.

DOW + 71 on 900 net advances

NASDAQ COMP + 46 on 850 net advances

SHORT TERM TREND Bullish (change)

INTERMEDIATE TERM TREND Bearish

STOCKS: In the early going, very early, the Dow dropped sharply being down 78. But, within 5 minutes the bottom was seen and the averages surged for the remainder of the day.

The initial weakness emanated from declines in Europe on concerns about the limits of the ECB.

But, on our side of the Atlantic, traders seemed to be fixated on the confirmation hearings for Janet Yellen tomorrow. She is the most dovish member of the FOMC and it is anticipated that she will talk about the need for even more money printing in spite of the fact that QE has been a miserable failure. Just look at where our economy is after 5 years of providing a sugar high for the stock market.

GOLD: Gold was up $2. It’s very oversold.

CHART: We’ve had weak breadth and an excess of exuberance. I didn’t think the S&P 500 would only give us a sideways correction, but it seems to have done just that.

It broke out of a congestion range today (top arrow) and the McClellan Oscillator has curled up from an oversold condition (bottom arrow). I’m concerned about the euphoria, but I don’t like fighting the tape.

TORONTO EXCHANGE: Toronto was up 45.

S&P\TSX Venture Comp: The Venture Comp was flat.

BONDS: Bonds curled up from an oversold condition.

THE REST: The dollar moved lower. Silver was lower. Crude oil was higher and copper got murdered.

BOTTOM LINE:

Our intermediate term systems are on a sell signal. We are long term bullish for all major world markets, including those of the U.S., Britain, Canada, Germany, France and Japan.

Ed Note: For subscribers there are 8 Buy and Sell recommendations as follows:

We’re moving back to a buy for bonds as of today November 13.

We’re moving back to a sell for the dollar and a buy for the euro as of today November 13.

We’re on a buy for gold as of October 24.

We’re on a buy for silver as of October 24.

We’re on a sell for crude oil as of November 5.

We’re on a sell for copper as of August 29.

We’re on a buy for the Toronto Stock Exchange as of October 17.

We are on a buy for the S&P\TSX Venture Comp. as of August 16.

NEWS AND FUNDAMENTALS:

There were no important releases on Wednesday. On Thursday we get the trade deficit and jobless claims.

As H.L. Mencken opined, “The most dangerous man to any government is the man who is able to think things out for himself, without regard to the prevailing superstitions and taboos. Almost inevitably he comes to the conclusion that the government he lives under is dishonest, insane, and intolerable.”

As H.L. Mencken opined, “The most dangerous man to any government is the man who is able to think things out for himself, without regard to the prevailing superstitions and taboos. Almost inevitably he comes to the conclusion that the government he lives under is dishonest, insane, and intolerable.”

It is no wonder that, according to a Gallup Poll conducted in early October, a record-low 14% of Americans thought that the country was headed in the right direction, down from 30% in September. That’s the biggest single-month drop in the poll since the shutdown of 1990. Some 78% think the country is on the wrong track.

Some readers will, of course, ask what this expose about the political future has to do with investments. It has nothing to do with what the stock market will do tomorrow, the day after tomorrow, or in the next three months. But it has a lot to do with the future of the US (and other Western democracies where socio-political conditions are hardly any better).

I have written about the consequences of a dysfunctional political system elsewhere. In the May 2011 I explained how expansionary monetary policies had favored what Joseph Stiglitz called “the elite” at the expense of ordinary people by increasing the wealth and income of the “one percent” far more than that of the majority of the American people.

I also quoted at the time Alexander Fraser Tytler (1747–1813), who opined as follows: “A democracy cannot exist as a permanent form of government. It can only exist until voters discover that they can vote themselves largesse from the Public Treasury. From that moment on, the majority always votes for the candidates promising the most benefits from the Public Treasury with the result that a democracy always collapses over loose fiscal policy, always followed by dictatorship” (emphasis added).

Later, Alexis de Tocqueville observed: “The American Republic will endure until the day Congress discovers that it can bribe the public with the public’s money.”

To be fair to Mr. Obama, the government debt under his administration has expanded at a much slower pace in percentage terms than under the Reagan administration and the two Bush geniuses. In fact, as much as I hate to say this, Mr. Obama has been (or been forced to be) a fiscal conservative.

However, what 18th and 19th-century economists and social observers failed to observe is that democracies can also collapse over loose monetary policies. And in this respect, under the Obama administration, the Fed’s balance sheet has exploded. John Maynard Keynes got it 100% right when he wrote:

By a continuing process of inflation, Governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. By this method they not only confiscate, but they confiscate arbitrarily; and, while the process impoverishes many, it actually enriches some… Those to whom the system brings windfalls… become “profiteers” who are the object of the hatred… The process of wealth getting degenerates into a gamble and a lottery… Lenin was certainly right. There is no subtler, no surer means of overturning the existing basis of society than to debauch the currency. The process engages all the hidden forces of economic law on the side of destruction, and does it in a manner which not one man in a million is able to diagnose [emphasis added].

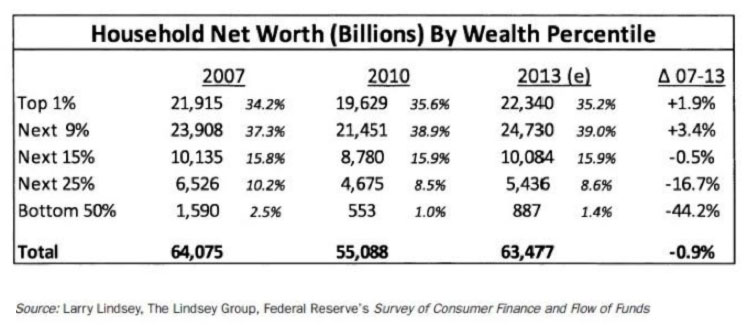

The Fed takes great pride in the fact that US household wealth has now exceeded the 2007 high. However, I was pleasantly surprised when I recently attended a presentation by Larry Lindsey, at my friend Gary Bahre’s New Hampshire estate. He unmistakably showed, based on the Fed’s own Survey of Consumer Finance and Flow of Funds, that the recovery in household wealth has been extremely uneven.

Readers should focus on the last column of Table 1, which depicts the change in household wealth between 2007 and 2013 by wealth percentile. As can be seen, the bottom 50% of the population is still down more than 40% in terms of their “wealth” from the 2007 high. (Lindsey is a rather level-headed former Member of the Board of the Governors of the Federal Reserve System, in which capacity he served between 1991 and 1997.)

Besides the uneven recovery of household wealth among different wealth groups, a closer look at consumer credit, which is now at a record level, is also revealing. Furthermore, consumer credit as a percentage of disposable personal income is almost at the pre-crisis high. But what I found most interesting is how different income and wealth groups adjusted their outstanding total debt (including consumer credit, mortgage debt, etc.) following the crisis.

Larry Lindsey showed us a table — again based on the Fed’s own Survey of Consumer Finance and Flow of Funds data — which depicts total debt increases and decreases (in US$ billions) among these different income and wealth groups. I find it remarkable that the lower 40% of income recipients and the lower 50% of wealth owners actually increased their debts meaningfully post-2007. In other words, approximately 50% of Americans in the lower income and wealth groups who are both voters and consumers would seem to be more indebted than ever. A fair assumption is also that these people form the majority of the government’s social benefits recipients.

Now, since these lower income and wealth groups increased their debts post-2007 and enjoyed higher social benefits, they were also to some extent supporting the economy and corporate profits. But what about the future?

Entitlements are unlikely to expand much further as a percentage of GDP, and these lower-income recipients’ higher debts are likely to become a headwind for consumer spending. Simply put, in my opinion, it is most unlikely that US economic growth will surprise on the upside in the next few years.

It is more likely there will be negative surprises.

Regards,

Marc Faber

for The Daily Reckoning

[For Retirees: If you’re like many Americans who want to retire (or have already) you’re worried about running out of the money you’ve worked your entire adult life for… just when you need it most. And as Dr. Faber pointed out, it’s harder for average Americans to grow their wealth now more than ever before.

But luckily for you, we’ve recently uncovered an incredibly effective strategy that could allow you to make as much money as you need, within a month. We know, it sounds unlikely but the proof is right here. The strategy has been popular so far. In fact, we have under 200 spots left to learn about it. We don’t want you to miss out, so click here for details on this opportunity.]

- It’s a cycle…it’s a business fluctuation… no, it’s a K-wave!

- Concerns about stunted growth continue…

- Plus, Marc Faber on the problem we faced… the people who caused it… and what to expect going forward…

Ed Note: If you are in a hurry, go down to the 9th paragraph on “K Waves” for a really important quick understanding of where we are in the cycle of Boom & Bust.

Doubts about long-term growth continue…

“Unless Washington does everything right,” said Bluford Putnam to Reuters this morning, “and that’s just not going to happen — the U.S. is a 2% economy now.” Mr. Putnam is a chief U.S. economist at CME Group and a former economist at the New York Federal Reserve Bank. He isn’t alone in his pessimism, either.

Yesterday morning, the NFIB Small Business Optimism Index numbers were released for October. For what it’s worth, the index, which attempts to measure small businesses’ economic outlook, was down over 2 percentage points, indicating growing pessimism. The index was down in September too… both months’ decline were pinned on the partial shutdown last month.

Meanwhile, the Chicago Fed National Activity Index — a monthly attempt to take the economy’s pulse — was flat. At the same time, consumer sales data last week were conflicted. The ICSC-Goldman report showed an increase, while the Redbook showed a decrease. In a word, the data is more confusing than helpful. Even when the numbers are clear… they’re often soon contradicted by other data. But that hasn’t stopped the Fed from throwing out optimistic predictions — especially for future U.S. growth.

In September, the Fed predicted 3% GDP growth for 2014… and 3.5% by 2015. “We are seeing continuing positive signs about momentum going forward,” said San Francisco Federal Reserve President John Williams last week, whatever that means.

“This sense that real GDP growth is going to pick up soon — I’m very skeptical about that,” reposted Jeffrey Lacker from the other coast, earlier this month. Mr. Lacker is the president of the Richmond Federal Reserve Bank. “I know it’s a popular forecast,” he admitted, “but I’m skeptical. I see 2% growth ahead.”

Still, the modern fixation on short-term growth at all costs we discussed yesterday continues. In the past, we said, you could coax economic growth with a little government spending, debt and inflation. Now that doesn’t seem to work as well… and it hasn’t been for a lack of trying.

In 2010, a year after the Fed started its massive asset purchases, they forecast that GDP would have risen between 3.5-4.5% by 2012. As 2012 approached, however, the Fed trimmed their forecast to 2.2-2.7%. Sadly, 2012 growth ended up being just 2%. Let’s hope they have better luck with their new forecast.

Cycles happen, we noted yesterday. Try as you might, there’s no way to make the market go all up or all down. It will always ebb and flow between the two. The Kondratiev waves (pronounced Kon-DRA-tee-eff) we mentioned, or K-Waves for short, are one interesting lens to analyze these ups and downs through.

We’ve written about K-waves in these pages before, but if you’ve never heard of them, they try to explain economic cycles over 50-60 years. The theory has been popularized by breaking the phases of the cycle into seasons — spring, summer, autumn and winter.

In the spring, business activity and employment start to pick up. As they do, consumers start to feel more confident about the economy. At the same time, consumer prices, stocks prices, credit and interest rates start to gradually increase. By the end of spring, the stock market’s peaked. That’s summer’s cue.

Summer is driven by a large inflation of the money supply. Consumers feel very good about the economy. As such, gold and real estate prices start to rise quickly along with interest rates. Stocks have also come down from their spring peak, until they bottom out — ushering in the autumn.

In the autumn, monetary and fiscal policies become even more loose, fueling a massive bull market in stocks. You would describe the environment as euphoric. Despite the monetary policy, the rate of price inflation falls, while gold enters a downturn. People start to take on way too much debt, but are confident because stock and real estate prices have created a wealth effect. Around the time that gold bottoms out, the dreaded winter has arrived.

The Kondratiev winter is economic hell on earth… but a natural step in the process. Stocks enter a massive bull market proportional to the size of the bull market that begot it. There are defaults and bankruptcies, bank crises, a credit crunch, a currency crisis as deflation runs its course through the economy. The price of gold rises.

According to the framework — we’re in a Kondratiev winter right now. Though there are some obvious differences between what we just described and what you see happening around you. That’s probably because this theory was made in the 1920s, when the entire globe wasn’t run on fiat currencies. Stay tuned for more on that tomorrow…

Even still, you might ask, is there any particular reason that cycles have to be 50 or 60 years long?

Not as far as we can tell. But we don’t think that means K-waves are a useless way to look at the world, either. As Mike Shedlock, editor of Mish’s Global Economic Trend Analysis wrote of K-Waves in these pages back in 2006, “Is ‘cycle’ even the right word? Would ‘business fluctuation’ be better? Then again, ‘What’s in a name? that which we call a rose/ By any other name would smell as sweet.'”

We’ll pick up the discussion, tomorrow. If you want to weigh in, message us at: peter@dailyreckoning.com Until then, we pass the baton to Dr. Marc Faber. In today’s episode of The Daily Reckoning, he discusses one of the enablers of the debt, spending and money printing that leads to a Kondratiev winter.

Read on…

What is the Problem, and Who Caused It?

by Dr. Marc Faber

As H.L. Mencken opined, “The most dangerous man to any government is the man who is able to think things out for himself, without regard to the prevailing superstitions and taboos. Almost inevitably he comes to the conclusion that the government he lives under is dishonest, insane, and intolerable.”

It is no wonder that, according to a Gallup Poll conducted in early October, a record-low 14% of Americans thought that the country was headed in the right direction, down from 30% in September. That’s the biggest single-month drop in the poll since the shutdown of 1990. Some 78% think the country is on the wrong track.

Some readers will, of course, ask what this expose about the political future has to do with investments. It has nothing to do with what the stock market will do tomorrow, the day after tomorrow, or in the next three months. But it has a lot to do with the future of the US (and other Western democracies where socio-political conditions are hardly any better).

I have written about the consequences of a dysfunctional political system elsewhere. In the May 2011 I explained how expansionary monetary policies had favored what Joseph Stiglitz called “the elite” at the expense of ordinary people by increasing the wealth and income of the “one percent” far more than that of the majority of the American people.

I also quoted at the time Alexander Fraser Tytler (1747–1813), who opined as follows: “A democracy cannot exist as a permanent form of government. It can only exist until voters discover that they can vote themselves largesse from the Public Treasury. From that moment on, the majority always votes for the candidates promising the most benefits from the Public Treasury with the result that a democracy always collapses over loose fiscal policy, always followed by dictatorship” (emphasis added).

Later, Alexis de Tocqueville observed: “The American Republic will endure until the day Congress discovers that it can bribe the public with the public’s money.”

To be fair to Mr. Obama, the government debt under his administration has expanded at a much slower pace in percentage terms than under the Reagan administration and the two Bush geniuses. In fact, as much as I hate to say this, Mr. Obama has been (or been forced to be) a fiscal conservative.

However, what 18th and 19th-century economists and social observers failed to observe is that democracies can also collapse over loose monetary policies. And in this respect, under the Obama administration, the Fed’s balance sheet has exploded. John Maynard Keynes got it 100% right when he wrote:

By a continuing process of inflation, Governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. By this method they not only confiscate, but they confiscate arbitrarily; and, while the process impoverishes many, it actually enriches some… Those to whom the system brings windfalls… become “profiteers” who are the object of the hatred… The process of wealth getting degenerates into a gamble and a lottery… Lenin was certainly right. There is no subtler, no surer means of overturning the existing basis of society than to debauch the currency. The process engages all the hidden forces of economic law on the side of destruction, and does it in a manner which not one man in a million is able to diagnose [emphasis added].

The Fed takes great pride in the fact that US household wealth has now exceeded the 2007 high. However, I was pleasantly surprised when I recently attended a presentation by Larry Lindsey, at my friend Gary Bahre’s New Hampshire estate. He unmistakably showed, based on the Fed’s own Survey of Consumer Finance and Flow of Funds, that the recovery in household wealth has been extremely uneven.

Readers should focus on the last column of Table 1, which depicts the change in household wealth between 2007 and 2013 by wealth percentile. As can be seen, the bottom 50% of the population is still down more than 40% in terms of their “wealth” from the 2007 high. (Lindsey is a rather level-headed former Member of the Board of the Governors of the Federal Reserve System, in which capacity he served between 1991 and 1997.)

Besides the uneven recovery of household wealth among different wealth groups, a closer look at consumer credit, which is now at a record level, is also revealing. Furthermore, consumer credit as a percentage of disposable personal income is almost at the pre-crisis high. But what I found most interesting is how different income and wealth groups adjusted their outstanding total debt (including consumer credit, mortgage debt, etc.) following the crisis.

Larry Lindsey showed us a table — again based on the Fed’s own Survey of Consumer Finance and Flow of Funds data — which depicts total debt increases and decreases (in US$ billions) among these different income and wealth groups. I find it remarkable that the lower 40% of income recipients and the lower 50% of wealth owners actually increased their debts meaningfully post-2007. In other words, approximately 50% of Americans in the lower income and wealth groups who are both voters and consumers would seem to be more indebted than ever. A fair assumption is also that these people form the majority of the government’s social benefits recipients.

Now, since these lower income and wealth groups increased their debts post-2007 and enjoyed higher social benefits, they were also to some extent supporting the economy and corporate profits. But what about the future?

Entitlements are unlikely to expand much further as a percentage of GDP, and these lower-income recipients’ higher debts are likely to become a headwind for consumer spending. Simply put, in my opinion, it is most unlikely that US economic growth will surprise on the upside in the next few years.

It is more likely there will be negative surprises.

Regards,

Marc Faber

for The Daily Reckoning

[For Retirees: If you’re like many Americans who want to retire (or have already) you’re worried about running out of the money you’ve worked your entire adult life for… just when you need it most. And as Dr. Faber pointed out, it’s harder for average Americans to grow their wealth now more than ever before.

But luckily for you, we’ve recently uncovered an incredibly effective strategy that could allow you to make as much money as you need, within a month. We know, it sounds unlikely but the proof is right here. The strategy has been popular so far. In fact, we have under 200 spots left to learn about it. We don’t want you to miss out, so click here for details on this opportunity.]

[Re. Cancellation Request: On a side note, our publisher is making what could be the most bizarre request ever. If you still want to receive the Daily Reckoning each day, you should see what he has to say. Click here for his message.]

There are two ways to invest your money in real estate: you do it yourself, or you do it with others.

Besides public market REITs with their volatile ups and downs like any stock, private syndications in the so-called “exempt market” are becoming quite popular. Syndicating a large piece of real estate i.e. pooling of your money with others to buy larger commercial real estate projects is a great idea – if executed well. It is indeed a proven path for wealth creation – if bought at the right price and managed well.

Not all real estate classes are created equal – and not all operators are equal either – and the not-to-distant recession and collapse of prominent syndicators such as First Leaside, League, Concrete Equities, Shire, Signature Capital or Libertygate, is a case in point.

There are nine typical steps in real estate syndication projects that you must check ! What are they ?

More here: http://www.prestprop.com/2013/11/13/nine-steps-invest-successfully-real-estate-syndicates-lps-private-reits/

In summary: it has to be win/win Are the operator’s profits aligned with yours, the investors i.e. usually at the end on exit? Or are they just growing assets under management, like mutual funds, to gather asset management fees, regardless of asset performance ? Is the NAV realistic ? Are distributions sustainable ?

There are quite a few scams out there .. and many were in the news lately .. but even more exist that just exploit the legal loopholes .. but there are many honest folks too. Use these nine guidelines to distinguish between the honest and the dishonest operators .. and you too can successfully and profitably co-own a larger piece of real estate or a pool of hard assets with others !

Thomas Beyer, is President of the Prestigious Properties Group, an investment group which has transacted over $175M in multi-family real estate over the last decade. The group is head-quartered in Canmore, AB and Vancouver, BC with holdings in W-Canada and Texas. He can be reached at 403-678-3330 or at tbeyer@prestprop.com or via www.prestprop.com.

In just outlandish political apeals, NDP leader Thomas Mulcair argues for higher consumer costs, lower wage growth, and less employment. seemingly the complete opposite of what they usually stand for.

In just outlandish political apeals, NDP leader Thomas Mulcair argues for higher consumer costs, lower wage growth, and less employment. seemingly the complete opposite of what they usually stand for.

Michael takes apart their demands with common sense and facts, those two things that Thomas Mulcair and his Party seem to be immune to….

{mp3}mcbuscomnov13fp{/mp3}

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair