Stocks & Equities

NEW YORK, Nov 14 (Reuters) – U.S. stocks opened little changed on Thursday ahead of a congressional hearing on the nomination of Janet Yellen as Federal Reserve chair, while a slide in Cisco shares… … full article

It’s a big club…. and you ain’t in it.”

It’s a big club…. and you ain’t in it.”

— George Carlin

It must be a byproduct of the government-controlled education system; people still think they live in a free country with a representative democracy. It’s anything but.

Voting, elections, etc. are all just illusions to make people think that they have some influence in society.

A tiny elite orchestrates the whole system. And one of the most influential conductors is the Federal Reserve, a body soon to be chaired by Janet Yellen. Her confirmation process begins today.

Since most people have no idea how central banking really works, her confirmation hearing today is just a footnote.

Even people who are otherwise financially sophisticated simply trust that the men behind the curtain know what they’re doing.

This is quite strange when you consider that central bankers have nearly total control over the economy.

In their sole discretion, they are able to set interest rates, conjure money out of thin air, finance trillion-dollar government deficits, bail out commercial banks, etc.

And through these tools, they have the power to manipulate the prices of just about anything, from the Google stock to real estate in Thailand to turnips in Sri Lanka.

For the last several years, the US central bank has set the example for the rest of the world in aggressively using their policy tools.

Most significantly, they have unabashedly printed money in unprecedented quantities. And this has not been without consequence.

For some, the effects have been beneficial.

Rapid expansion of the money supply has pushed asset prices up all over the world. Stocks. Bonds. Many commodities. US Farmland. Artwork. Fine wines. Just about every asset class imaginable is near its all-time high.

People who are already wealthy have the available funds to invest in these markets. So their wealth has grown even more– exponentially.

The middle class, on the other hand, is experiencing an entirely different effect of money printing– retail price inflation.

And anyone who has been to a gas station, airport, university, doctor’s office, grocery store, etc. over the last few years understands this phenomenon very well.

A typical middle class family has little excess cash to invest after paying for rapidly increasing living expenses. Food. Fuel. Mortgage. Insurance. Etc.

And whatever wages or savings they have are being eaten away by inflation. So while the wealthy are getting wealthier exponentially, the middle class is actually getting poorer.

This explains why the wealth gap in the Land of the Free is the largest since 1929 at the start of the Great Depression.

Central bankers are responsible for much of this. In conjuring money out of thin air, they are benefitting one segment of society at the expense of another.

And with Janet Yellen soon chairing the Fed, very little will change.

Yellen has made it clear that she will continue to print unlimited quantities of money despite overwhelming data that such actions are ineffective and destructive for the the majority of the population.

Kyle Reese from the first Terminator movie sums up the consequences for the middle class rather succinctly:

http://www.youtube.com/watch?v=zu0rP2VWLWw

I’m an international investor, entrepreneur, permanent traveler, free man. Thisfree daily e-letter is about using the experiences from my life and travels to help you achieve more freedom.

Over the last few years I’ve traveled to over 100 countries, met with a President and several diplomats, briefed sovereign fund managers, flown an aerobatic stunt plane, started several companies, hitchhiked in Bogota, taken a train across the orient, lectured on entrepreneurship in Eastern Europe, and personally provided venture capital to new start-ups.

I’m a student of the world, and I believe that travel is the greatest teacher. My knowledge is practical, and hopefully of significant use to you. Off the top of my head I could quote you the price of beachfront property in Croatia, where to bank in Dubai, the best place to store gold in Singapore, which cities in Mexico are the safest, which hospitals in Asia are the most cost effective, and how to find condo foreclosure listings in Panama.

I believe that in order to achieve true freedom, you have to be able to make money, control your time, and eliminate the mindset that you are subject to a corrupt government that is bent on degrading your personal liberty.

Grow It, and They Will Eat It.

“Build it, and they will come” has been the motivation for many dreams. Baseball fields, restaurants, and other follies have sprouted from belief in this concept. Much of the real estate industry of times now past lived by this philosophy. That worked until they did not come, and then the bankers came for the remains.

In Agri-Food we have a similar motto: Grow it, and they will east it. We worry little about relying on such a belief, for people eating is, unlike baseball, not optional. That the world will eat it if it is grown can be observed in the following chart.

Note on chart: USDA works in crop years, not calendar years. At present we are in crop year 2014. That year runs from September 2013 through the end of August 2014. The current Northern Hemisphere harvest in process, which includes that now concluding in the U.S., is part of the data point for 2014 in the graph.

Plotted in the chart is percentage of the world’s total grain production that is consumed. That ratio is expressed as a percentage, and uses the right vertical axis. A solid black line highlights the 100% level which means that all of the world’s grain production is being consumed.

In the first three years plotted in the graph the world’s consumption of total grains produced averaged more than 100%. Essentially, over that period the world consumed all the grains produced plus some of that which had been stored from previous years. The value for 2013, the highest in the chart, is due in part to the drought which dramatically reduced U.S. grain production in the Fall of 2012.

…read more HERE

The rarest commodity on the planet…

If you were asked what the scarcest commodity on the planet was, I am sure many of you would say gold or oil.

But it’s neither of these, nor is it platinum or copper or one of the rare earth metals.

And I know many people will say fresh water, and they’d be close…

But no, land is one of the scarcest commodities on Earth, and for one simple reason… nobody will ever make more of it, yet demand for it is growing at a rapid clip.

While most people wouldn’t think of land as a “commodity,” it is, by definition, one of the scarcest commodities in the world.

Think about it this way… The world’s population is growing by about 200,000 people every day. That’s over a million new people a week crowding into a fixed amount of space to live, work and shop — placing upward pressure on housing, office parks and retail strip centers.

That’s exactly why forward-looking mega investors like Warren Buffett are placing big bets on land and buildings.

We tend to associate ultra-rich business tycoons with hard assets like steel and oil, but more often than not, the world’s billionaires have invested the bulk of their wealth in real estate.

Media mogul Ted Turner, for example, owns more than a dozen sprawling ranches from Oklahoma to Montana. This collection spans 2 million acres (an area more than twice the size of Rhode Island), making him one of the nation’s largest private landowners.

Turner’s explanation is simple: “I never like to buy anything except land. It’s the only thing that lasts.”

Sam Zell (No. 110 on the Forbes 400 list with a net worth of $4 billion) made a fortune by investing in commercial office properties. His current portfolio includes housing in China, shopping malls in Brazil and the Waldorf Astoria hotel in Chicago.

Now, let’s be realistic. Most of us don’t have the bankroll to buy an office tower, an apartment complex or a retail shopping center. But I’ve found a group of investments that might just be the next best thing. And now may be the best time in a generation to buy them.

Here’s why…

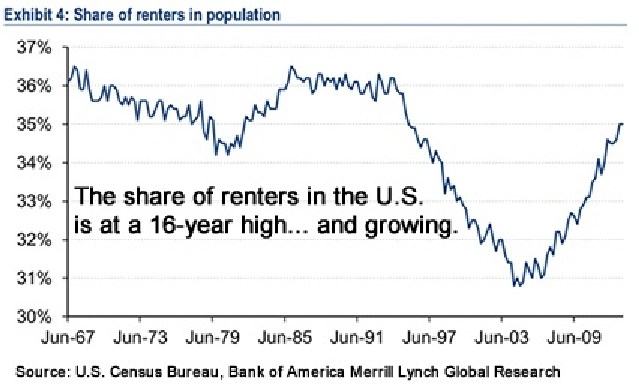

Millions of people across the country have essentially put the American Dream on hold, becoming renters rather than owning their own homes — a phenomenon I call “Renter Nation.”

Right now, there are nearly 100 million renters in the U.S. — 1 in 3 Americans. And new research estimates that half of all new households this decade will be renters. In fact, Harvard University predicts that as many as 7 million new rental households will form by 2020.

The National Apartment Association and the National Multi Housing Council seem to think the numbers could be much higher. They estimate that 77 million baby boomers may soon consider downsizing… while nearly 80 million 20-somethings will be looking to move out of their parents’ houses and into the rental market as their job prospects improve.

This means almost half of today’s population could turn into renters not too long from now if trends continue.

Just look at how fast the share of renters has already grown in recent years…

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair

So, how can individual investors to start cashing in on the Renter Nation phenomenon? A great way is to invest in companies that buy up real estate at bargain prices and essentially become a co-landlord with them as they rent those properties out.

Take Blackstone Group (NYSE: BX), for example, a publicly traded private equity company that’s making some huge land grabs across the country.

In fact, Blackstone is now the largest private real-estate owner in the United States.

In the past few years, the company has poured billions into housing and rental properties. And with housing prices up big in 2013, those bets are looking well-placed and timed.

Earlier this year Blackstone accelerated purchases of single-family homes to capitalize on rising prices, investing $2.5 billion in 16,000 homes and rental units.

But the firm has gone beyond that into much larger property ventures to expand on this winning idea. In August, Blackstone announced a $2.7 billion deal to buy 80 apartment complexes from General Electric (NYSE: GE).

Blackstone’s winning plan? Become one of the nation’s largest owners of houses, apartment complexes, malls and commercial real estate… Generate billions in income as it rents out all those properties to hundreds of thousands of reliable tenants… And finally, sell the properties when prices get high enough to bag a huge profit.

The endgame results in investors being rewarded with giant gains and increasing dividends.

It’s no wonder Blackstone is projected to grow earnings by 33% in 2013, 18% in 2014 and 16% annually over the next five years.

Blackstone is currently yielding 3.7% in spite of shares gaining 76% in the past year. But with nearly $900 million in cash on hand, manageable debt and $546 million in annual free cash flow, there’s plenty of room for future dividend growth.

Action to Take –> So what’s the takeaway? Real estate can be a sound, durable investment. Even if you’ve never considered being a landlord, owning companies that invest in property, like Blackstone, can be the next best thing.

Note: I’ve recently put together a special research report,”Living the New American Dream,” which profiles several companies like Blackstone. These companies are taking advantage of the Renter Nation phenomenon to give investors safe yields of 6.2%, 8.2% or higher. To learn more about this report and other income-generating Renter Nation ideas, click here.