Bonds & Interest Rates

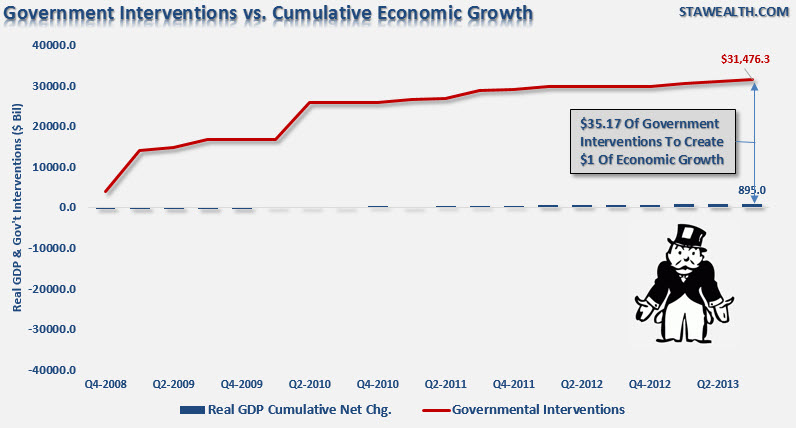

Despite Janet Yellen’s commitment to continue supporting the economic recovery the transmission system of government interventions is clearly broken. As STA Wealth Management’s Lance Robertss hows in the simple chart below, it has taken $35.17 of government intervention to generate $1 of economic growth over the past 5 years. More importantly, the rate of diminishing returns is increasing. In other words, it is taking consistently more dollars of intervention to create an incremental increase in economic growth.

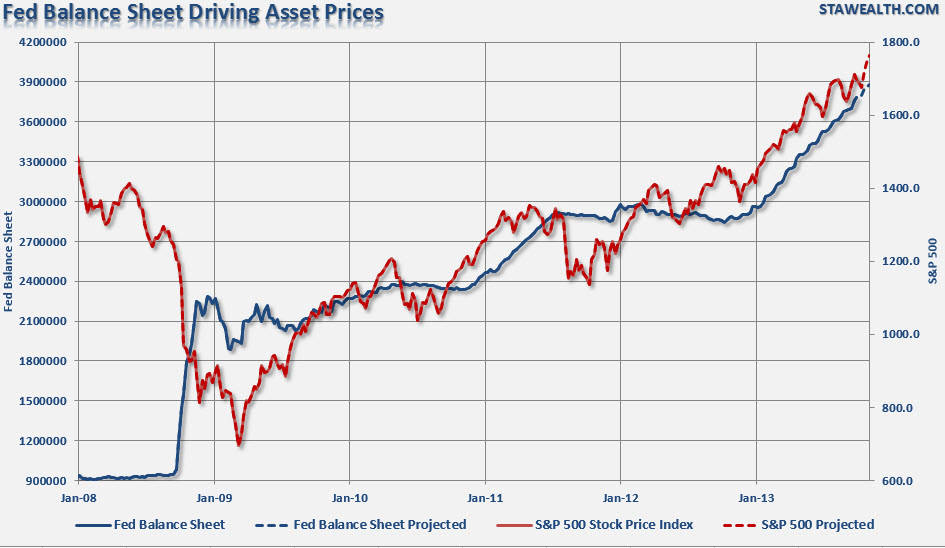

In the meantime, as shown below, the continued liquidity programs from the Federal Reserve continue to boost asset markets towards more exuberant levels.

However, despite signs of a potential market “bubble” Janet Yellen clearly sees no such thing…

More from ZeroHedge:

EU Citizenship Goes On Sale, Price War Breaks Out

Academic Insanity Costs You 2% Of You Purchasing Power Per Year

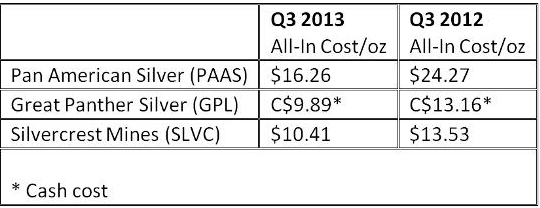

Miners Reporting Serious Progress

This was supposed to be the year that gold and silver miners pretty much imploded. The story in a nutshell is that during the boom years of 2009 -2011, the markets threw so much cash at the industry that a lot of CEOs went a little crazy, racing to accumulate the most ounces in the ground without regard for whether those ounces could be gotten out profitably at prevailing prices. When the metals got whacked in 2012 and 2013, the miners that had gone the craziest found themselves with uneconomic mines, way too many people and equipment, costs that had doubled in just a few years, and in many cases serious doubts about their future existence.

But one of the nice things about an easy-money binge is that it leaves an industry with a plenty of fat that can be trimmed right away. The miners have spent the past six months in survival mode, firing non-essential people, closing uneconomic mines and cancelling big development projects. Based on the most recent numbers it’s going better than the expected. The following table compares Q3 2013 silver mining costs to the year-ago number for three companies that just reported.

These are serious reductions. Only…

….read more HERE

Stock market continue its momentum from yesterday but struggled to climb. More weak comments from Fed Chair nominee Janet Yellen suggested that she would likely see QE continue for a while to help the US economy get back up on its feet.

Stock market continue its momentum from yesterday but struggled to climb. More weak comments from Fed Chair nominee Janet Yellen suggested that she would likely see QE continue for a while to help the US economy get back up on its feet.

QE liquidity has been one of the main forces driving the stock rally over the past year and today was…

Read Full Report: http://www.thegoldandoilguy.com/articles/etf-trading-strategies/

Ed Note: Very good, clear video

Chris Vermeulen

The U.S. Dollar has made a sharp move since October against a basket of currencies

Who wants a strong currency? If that question was for an opinion poll of finance ministers and central bankers, the response would be a firm no one. But in reality, no poll is needed. The last couple of weeks’ action has spoken louder than words.

Forex traders were once again reminded that when a currency makes strong gains the chances of verbal or monetary intervention are probably not far off. Losses on long positions can swiftly follow. Those long the U.S. dollar (USD) should be cautious.

Talk of currency wars has made the headlines regularly since the outbreak of the financial crisis in late-2007. A lack of economic growth prompts countries to try and grab a slice of someone else’s demand. The quickest way to do that is to devalue the national currency giving goods and services of that country a short-term competitive advantage.

The yield advantage made AUD and NZD attractive to investors engaged in carry trades – that’s borrowing in a low interest rate currency to buy a higher interest rate one. However, policy makers in those two countries decided recently that enough is enough.

Last week, the European Central Banks cut interest rates ostensibly to avoid deflation. But many observers interpreted it as a move to also weaken the EUR. It worked. On the same day of the ECB announcement the Czech Central Bank intervened sending the CZK plummeting.

A currency war victory for the ECB

How strong of a U.S. dollar is the Fed prepared to stomach?

With EUR/USD (FOREX:EURUSD) down, GBP/USD (FOREX:GBPUSD) stalled and the USD/JPY (FOREX:USDJPY) weakening, that leaves the (USD) as a potential stand-out among the majors. Since late October, the U.S. Dollar Index (NYBOT:DXZ13) has moved from around 79 to just over 81 against a basket of currencies – a fairly sharp move — although USD is still sitting below a high of 84.58 reached in September.

The question is, “Will the U.S. Federal Reserve allow USD to make continuing substantial gains against other major currencies?” After all, the U.S. economy, although not quite firing on all cylinders, is still doing better than most European counterparts. And Japan has yet to prove it can sustain its recent growth.

But the answer is that the Fed probably does not want a strong USD. That will certainly be one dilemma it faces if it ever manages to taper its quantitative easing program. Another often overlooked factor is that U.S. debt is substantially held by foreigners. This gives the U.S. authorities a strong motive to devalue – a form of default by stealth.

If USD does start making sustained gains – particularly sharp ones – dollar bulls should be cautious.

About the Author Justin Pugsley

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair