Today one of the top economists in the world spoke with King World News about one of the most terrifying predictions for the year 2014. This is an incredibly powerful interview where he discusses his frightening prediction and what this will mean for global markets. An audio interview has now been released from KWN where Michael Pento, founder of Pento Portfolio Strategies, speaks about this terrifying situation.

Today one of the top economists in the world spoke with King World News about one of the most terrifying predictions for the year 2014. This is an incredibly powerful interview where he discusses his frightening prediction and what this will mean for global markets. An audio interview has now been released from KWN where Michael Pento, founder of Pento Portfolio Strategies, speaks about this terrifying situation.

The fundamentals tell Stefan Ioannou, mining analyst with Haywood Securities, that the outlook is good for copper and zinc in the midterm, while for nickel, stronger-for-longer is the watchword. In this interview with

The fundamentals tell Stefan Ioannou, mining analyst with Haywood Securities, that the outlook is good for copper and zinc in the midterm, while for nickel, stronger-for-longer is the watchword. In this interview with The Gold Report: In October, Haywood Securities revised its prices for several commodities and predicted that copper prices should remain strong in the short term, zinc prices should strengthen over the medium term, and nickel would remain a long-term price play. Can you recap the fundamentals for each metal, starting with copper?

Stefan Ioannou: Because it is so widely used, copper is the master of the base metals. All base metal prices have been stressed this year, due to global economic uncertainty. Despite some week-to-week and month-to-month volatility, copper prices have generally stayed in the $3.25 to $3.35/pound ($3.35/lb) range.

Concern over a near-term surplus in copper supply has kept the price from going higher. Over H1/13, London Metals Exchange (LME) inventories increased over 100,000 tonnes (100 Kt), venturing north of 600 Kt. Year-to-date, net LME inventories are up 40%. Many market forecasters still predict 2013 net surpluses of over 250 Kt.

TGR: Yet the Chinese are paying a premium of $0.08 to $0.10/lb in Shanghai.

SI: LME inventories are just one piece of the pie. There also are the Shanghai inventories, in-house inventories held by producers and inventories in what are called Chinese bonded warehouses.

Data through September suggest that, while LME inventories have been up 100 Kt, the Chinese bonded warehouse inventories are down 700 to 800 Kt, implying a net deficit on the order of 600 Kt. That paints a very different picture.

Of course, we don’t know how the copper moving out of the Chinese bonded warehouses is being used. Is it going into manufactured goods, used as finance collateral, or just being stored elsewhere? Furthermore, recent data pertaining to the month of October suggests Chinese bonded warehouse inventories have since rebounded by 150 to 200 Kt.

TGR: What are the fundamentals for zinc?

SI: Zinc inventories on the LME reached an all-time high of 1.2 million tons (1.2 Mt) in 2013 and remain very high. In the short term there’s a lot of zinc out there for consumption.

The key thing underpinning the zinc story is an anticipated shortfall on the supply side. The zinc space differs from the copper space in that a lot of production comes from smaller mines. Over the years, that has created a fragmented industry.

A number of very large zinc mines are poised to end production over the next two or three years simply because they’ve run their course. That will take 10–11% of global zinc production offstream. The current list of timely advanced-stage development projects doesn’t come close to filling that gap.

Today, zinc is $0.85/lb, but there is a strong argument that as we move into 2015 and especially by 2016, zinc prices could be well north of $1.50/lb.

TGR: That would be something. What about nickel?

SI: Nickel is a longer-term story. In 2007, nickel ran up to $25/lb. That price spike sparked the rise of nickel pig iron production, which is nickel made from lateritic ores. It’s a sub-grade product, but can be used in certain types of steel manufacturing in place of higher-cost nickel. When nickel pig iron came on strong, it drove the nickel price down.

Some fundamental, long-term changes are underway in the nickel space. A lot of nickel comes from Indonesia. The first change is that the Indonesian government is implementing export reform. Heavy export taxes will either restrict exports or raise the cost of exported ore considerably.

Second, the high-grade ore has already been mined in Indonesia. We’re left with lower-grade ore, and lower grade usually translates into higher cost.

Third, even the ore that does get exported—most of it to China, by the way—is put through furnaces in a very energy-intensive process. Power costs have been going up in China. This adds another cost to the nickel pig iron price equation.

In short, nickel pig iron has been pictured as a cheap alternative. It remains relatively cheap, but it’s getting more expensive.

I would add one caveat. More of the nickel pig iron production in China goes through rotary kiln furnaces, which are somewhat less energy intensive. Realistically, new nickel pig iron projects probably need a nickel price of $9/lb to be economically viable. With prices now in the low $6/lb range, new production facilities will need higher nickel prices to get going.

TGR: Thank you for a very thorough summary. What three things should investors look for in a copper project?

SI: Number one, look for high grade over low grade.

TGR: And what is high grade, above 1%?

SI: It depends on the type of mine: underground or open pit. These days, I would say anything greater than 0.5% to 0.6% copper in an open-pit scenario would be relatively high grade. Anything greater than 1% would be very high grade in an open-pit scenario.

As you move underground, you want at least 2% copper.

Obviously, the presence of other byproduct credits changes the economics, but those would be my back-of-the-envelope numbers.

TGR: What else should investors look for in a copper project?

SI: Number two is jurisdiction. Politics has always played a role, but we’re seeing more issues with projects in challenging areas. In Africa, for example, governments can change overnight and the resulting changes to ownership structures usually disadvantage the mining company.

It can cause trouble when the local population isn’t happy with mining in the neighborhood. Native groups, even in stable countries like Canada, are a significant consideration. For a mining project to work, everyone has to work together.

The last thing is infrastructure. Imagine two geologically identical projects. One is next to a highway with power lines and a port facility. The other is in the middle of the northern Arctic and you have to fly in. Those two projects have significant economic differences when it comes to development. Having established infrastructure is a massive advantage.

TGR: Which companies that you follow have not only those three characteristics, but could also get a lift from higher copper prices?

SI: One of the interesting ones just from an infrastructure point of view is Capstone Mining Corp. (CS:TSX). The company recently bought a mine called Pinto Valley in Arizona, which helped to change the Capstone story from short to medium term.

The company will produce about 85 million pounds (85 Mlb) of copper from its Cozamin and Minto mines this year. The addition of Pinto Valley, which is in production now, will take its production to more than 230 Mlb in 2014.

Capstone also has a development project in Chile called Santo Domingo, a very large, low-grade copper-iron project. Looking at infrastructure, it is next to a paved highway and close to port facilities. That kind of infrastructure makes a low-grade project potentially viable.

TGR: Capstone bills itself as a leading intermediate copper producer. Will Capstone ever be a major copper producer?

SI: I think it’s well on its way. The Pinto Valley acquisition was an important growth step for Capstone. Beyond that, the company has a very strong balance sheet, a good debt-equity ratio. Santo Domingo represents the next big step. It likely won’t be in production until at least 2018 or so, but when that happens, Capstone could be producing well over 400 Mlb annually. That puts it in the realm of Lundin Mining Corp. (LUN:TSX; LUMI:OMX) and HudBay Minerals Inc. (HBM:TSX; HBM:NYSE).

TGR: Nice company to keep. What’s one more copper play you follow?

SI: One that will merit more recognition as it goes forward is Nevsun Resources Ltd. (NSU:TSX; NSU:NYSE.MKT). A one-mine company, Nevsun is an established producer. Its Bisha mine is in Eritrea, which has frightened some investors off. That said, the company has worked extremely well with the government over the last decade to discover, permit, build and put Bisha into production.

Initially, Nevsun was thought of as a gold company as it mined through the oxide gold cap at Bisha, which is a polymetallic volcanogenic massive sulfide (VMS) deposit. However, the operation is now transitioning into supergene copper—copper mineralization that can be made into a concentrate for shipping. Its first, full-bore year of copper concentrate production will be 2014. In a geological sense, Bisha is truly a base metals mine.

TGR: A lot must depend on Nevsun’s relationship with the Eritrean government.

SI: Yes, and I give the Eritrean government a lot of credit. Bisha is a world-class deposit; on a total resource basis it contains more than 40 Mt of very high-grade material. When it was first discovered the government recognized right away that Bisha could be its ticket to greater financial viability. The government acted responsibly by bringing in independent, third-party engineers to evaluate its worth and set up an ownership structure with Nevsun. Nevsun owns 60% of the deposit, the government has a free 10% carried interest on the project and then it also bought an additional 30%. That makes a 60/40 ownership structure between Nevsun and the government.

The Eritrean government paid close to $250 million for its 30% interest. Any analyst on the street at the time would agree that, on a net asset value basis, was a pretty fair valuation. Bisha is a huge source of tax revenue for the country, and its 40% interest gives the government direct cash flow.

The Eritreans are working in a similar way with companies that have made subsequent discoveries. Nevsun really paved the way for doing business in Eritrea.

TGR: Moving on, what three things should investors want in a zinc project?

SI: Grade, jurisdiction and infrastructure are important to any commodity or mining play. With zinc, you really want to pay attention to grade. Typically, grade translates directly into a cash cost number. For instance, copper is trading at $3.25/lb. The cash cost for even the highest-cost copper producers is around $2.50/lb. That gives them a significant margin.

The zinc space is quite different. Zinc is trading around $0.85/lb. I would estimate that cash costs for 25% of the zinc production is at or near that price. The margins are a lot tighter. Miners without good grades run the risk of having a mine that may not be able to weather the down cycles within zinc’s overall price cycle.

TGR: Zinc is also tricky in that there are very few pure-play zinc producers. Which zinc equities does Haywood cover?

SI: There is pretty good market consensus that Trevali Mining Corp. (TV:TSX; TREVF:OTCQX; TV:BVL) is the go-to name. Its mine in Peru is just starting production and a second mine in New Brunswick is scheduled to come online late next year.

Foran Mining Corporation (FOM:TSX.V) is a notable developer. Its McIlvenna Bay project in Saskatchewan is just over the border from Manitoba. McIlvenna Bay is a 24 Mt VMS deposit, right on the doorstep of HudBay’s 777 and Lalor projects. That puts it close to infrastructure in a politically stable jurisdiction. Foran still has to define a mine plan, but over time, this could become the next mine in the evolution of the Flin Flon camps.

Canadian Zinc Corp. (CZN:TSX; CZICF:OTCQB), Chieftain Metals Inc. (CFB:TSX) and Sunridge Gold Corp. (SGC:TSX.V) also have safe development projects with a lot of zinc in their profiles. Any of them could do very well on the back of a strong zinc price.

TGR: As you suggested, nickel is facing headwinds. Is this a situation where you look for smaller companies with large resources that could be ready to go into production when the nickel price trades up?

SI: It is. First off, you have to believe in the thesis that nickel prices will rise. If you believe that, the next question is what kind of nickel projects you want to get involved with.

Nickel comes from three sources. First are the typical sulfide deposits like Voisey’s Bay, where you make nickel concentrate. The laterites are second. They are basically weathered dirt and are processed differently. Three is nickel pig iron, which we talked about earlier.

From both a technical and economic view, the sulfides are the least risky. The processing technology is well over 100 years old and is very well understood. If I had my pick, I would steer toward sulfides.

Then, I would look at projects that will touch the potential nickel cycle when it starts to kick up again. That means looking long term toward 2017–2018.

TGR: Which small-cap nickel equities does Haywood follow?

SI: The main one is Royal Nickel Corp. (RNX:TSX), because, number one, its Dumont project is a sulfide project. Two, Dumont is in Québec just outside Val-d’Or, which has well-established mining infrastructure. Three, this is a mining region where the Québec government is on its side.

The company has a very large resource. It is low-grade, so it is very leveraged to the nickel price, but if you believe in nickel’s longer price outlook, it fits the bill. This project should come onstream in 2017–2018, which positions it to catch that nickel price-cycle when it takes off.

TGR: The Dumont project will need at least a billion dollars to reach production. How will Royal Nickel raise that cash?

SI: Financing is a key challenge, especially when a junior company is behind the name. These days, juniors can’t finance development themselves through standard debt equity. Increasingly, we see juniors sell a direct project interest to a major partner, whether it be a major miner, an Asian smelting group or an entity that has strategic interest in securing concentrate. That is what Capstone did with Santo Domingo and others have followed suit.

The way the deal works, especially if it’s with an Asian smelter group, is that the smelter guarantees to arrange upward of 60% of the capital cost in the form of project debt. That leaves 40% outstanding, which is paid for by the company and smelter through equity.

What the smelter pays for the project interest basically offsets whatever the junior has to pay in its equity contribution going forward. If it’s structured just right, a company can end up with a situation where it sells a 40% interest in the project, but faces minimal equity dilution thereafter.

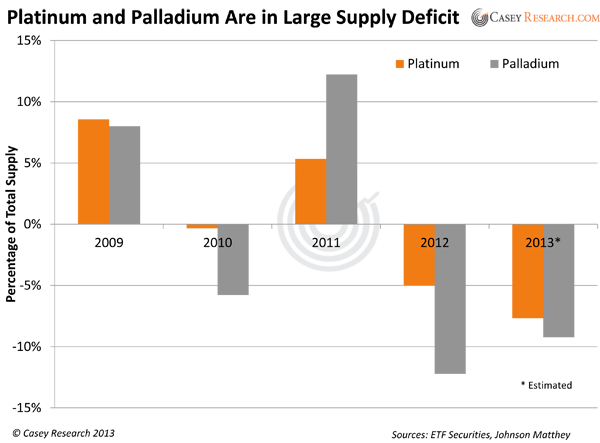

TGR: Do the platinum group metals (PGMs) in the Dumont deposit set it apart from other large, low-grade nickel deposits?

SI: I would say no. They’re not that significant in terms of volumetric production, but they do benefit Dumont’s nickel cash cost profile.

In our model, Dumont will produce close to 100 Mlb of nickel a year. It will also produce approximately 4,500 ounces (4.5 Koz) of platinum a year and 10 Koz of palladium a year.

The PGMs are a byproduct credit. In our model, the total life-of-mine average cash costs at Dumont, net of byproduct credits, are around $5/lb. If we were to take the PGMs out of the project, the cash costs would be closer to $5.50/lb. That means about a $0.50 credit—or 10%—to the cash costs. That is significant, especially when nickel’s trading so low; every penny counts.

The main caveat with Dumont is a stronger-for-longer nickel price outlook. Dumont’s economics are challenged at nickel prices below $9/lb.

TGR: What other nickel equities does Haywood follow?

SI: We don’t cover much in the nickel space, but there have been a few notable discoveries recently.

One of the best is North American Nickel Inc. (NAN:TSX.V). This is a grassroots play in Greenland. The company’s Maniitsoq project includes a recent discovery at a target called Imiak Hill. As early as this past summer, we knew the company had hit massive sulfides. At the time, the question was if they were nickel-bearing sulfides. The answer appears to be yes.

Last month, the company released a discovery hole: 19 meters (19m) of 4.3% nickel and 0.6% copper plus a bit of cobalt. A significant intersection. Subsequently, another hole returned 25m grading 3.2% nickel and 1.1% copper.

Those grades are similar to the Voisey’s Bay discovery in the 1990s, although that was underpinned by intervals upward of 100m thick. The thickness at Imiak Hill isn’t quite the same, but the grades definitely are.

It’s a quiet period for North American Nickel now; it won’t get back out to the project until the spring. In the meantime, it can go through the data and nail down drill targets for 2014 and start demonstrating Maniitsoq’s potential size.

TGR: North American Nickel bills Maniitsoq as being bigger than the Sudbury Basin. Is that valid?

SI: I think the land position is larger, yes. Obviously the question is if it is all nickel bearing.

TGR: Sudbury Basin isn’t all nickel bearing either.

SI: Fair enough. The interesting question is why look for nickel in Greenland? The rocks at Maniitsoq are the same rocks that host Voisey’s Bay. At one time, they were connected. Now, because of tectonics, there’s a sea between them.

TGR: Does this shift North American Nickel’s focus away from Post Creek/Halcyon and North Thompson to Maniitsoq?

SI: Maniitsoq is definitely North American Nickel’s flagship project. It’s a junior company with a modest market cap. Its value will be derived from Maniitsoq. Will the company shut off work at those other projects? Probably not, but the market will want to see the company spend most of its energy and capital at Maniitsoq.

TGR: Are there any other head-turning discoveries in the base metals world worth keeping an eye on?

SI: Colorado Resources Ltd. (CXO:TSX.V) made a significant discovery last spring in northern British Colombia. The North ROK project returned a 333m drill hole intersection grading 0.5% copper and 0.7 grams per ton (0.7 g/t) gold, including 242m at 0.63% copper and 0.85 g/t gold, basically starting from surface. That implies the project is open-pittable. Anything over 0.5% copper is great; having a gold grade kicker is even better.

North ROK has infrastructure too. It’s 5 kilometers from Imperial Metals Corp.’s (III:TSX) Red Chris development project. Ten years ago, this would have been considered the middle of nowhere, but Red Chris opened up the whole region.

TGR: Colorado was a rare performer in an otherwise bleak summer for mining equities. Should investors wait for the next drill results to come out or get in now?

SI: Looking at the stock chart, it’s already gone through the classic lifecycle of a mining stock profile. On discovery of that intercept, the stock price spiked to almost $1.50. It’s come off to below $0.25 now.

Colorado Resources is in that quiet period when ground truthing and engineering start to kick in. The stock price won’t pick up again until we have a sense of North ROK’s mineability and the company moves toward production.

There have been other holes, not as good as the first. Now it’s a matter of keeping it all together and getting tonnage. I think the market understands that Red Chris will get a lot bigger over time. North ROK has some better grades than Red Chris.

TGR: What can you tell our readers about discoveries in Europe?

SI: Reservoir Minerals Inc. (RMC:TSX.V) has a copper-gold project in Serbia called Timok—a very high-grade discovery with flashy drill hole intercepts. The discovery that got the stock going was a 70m intercept grading 11.6% cooper and 7 g/t gold.

This is a joint venture project with Freeport-McMoRan Copper & Gold Inc. (FCX:NYSE); Freeport owns 75% and Reservoir 25%. Freeport is paying for the exploration.

As a result, Reservoir has a great trap line of results coming in at no cost, and at great benefit to its share price.

In addition, Timok looks to be a high-grade, high-sulphidization epithermal system. One could argue that Freeport’s real interest is an adjacent, deeper-seeded porphyry that may have fed the high-sulphidization system. The porphyry would be lower grade, but much bigger tonnage, and would move the needle for Freeport-McMoRan.

TGR: Like a smallish Grasberg.

SI: Sort of. Even if Freeport decides the porphyry’s not there or not in a significant enough form, Reservoir will be left with a nice high-sulphidization project that would be attractive to a number of midtier companies out there looking for high grade.

TGR: Reservoir also has a 45% interest in the nearby Deli Jovan concession with Orogen Gold Ltd. (ORE:LSE). Are those two interests enough for investors to make money with Reservoir?

SI: I think investors will be focused on the company’s progress at Timok.

TGR: Can you leave our readers with one positive thought on the base metal space?

SI: Short term, I wouldn’t read too much gloom-and-doom into the copper numbers. The Chinese bonded warehouses provide one interesting data point suggesting that the surplus isn’t nearly as significant as some people would have us believe.

The zinc space is interesting because there are so few zinc players. When the zinc price runs, anyone associated with zinc stands to do well.

TGR: Stefan, thank you for your time and your insights.

Stefan Ioannou has spent the last seven years as a mining analyst covering mid-cap base metal companies at Haywood Securities. Prior to joining Haywood, he worked with a number of exploration and mining companies, as well as government agencies as a field geologist in Nevada and throughout the Canadian Shield in both the gold and base metal sectors.

Want to read more Gold Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

Related Articles

- China, Base Metal Tiger, Sets the Trend for Metals: Stefan Ioannou

- Jay Taylor: Cashing In on Deflationary Forces

- Richard Karn: Three Australian Miners Position

DISCLOSURE:

1) Brian Sylvester conducted this interview for The Gold Report and provides services to The Gold Reportas an independent contractor. He or his family own shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of The Gold Report: Trevali Mining Corp., Royal Nickel Corp. and Colorado Resources Ltd. Streetwise Reports does not accept stock in exchange for its services or as sponsorship payment.

3) Stefan Ioannou: I or my family own shares of the following companies mentioned in this interview: None. I personally am or my family is paid by the following companies mentioned in this interview: None. My company has a financial relationship with the following companies mentioned in this interview: Trevali Resources Corp. I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts’ statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned and may make purchases and/or sales of those securities in the open market or otherwise.

.

.

Most people — certainly most governments and economists — define inflation as a general rise in prices. But this is wrong. Inflation is an increase in the money supply, of which a rising general price level is just one possible result — and not the most common one.

Most people — certainly most governments and economists — define inflation as a general rise in prices. But this is wrong. Inflation is an increase in the money supply, of which a rising general price level is just one possible result — and not the most common one.