Timing & trends

– U.S. private-sector hiring rose in November at the fastest clip in a year, opening the door wider for the Federal Reserve to start trimming its bond purchases within the next few months.

Other data on Wednesday also pointed to a brightening outlook, with the services industry expanding at a decent pace last month and exports hitting a record high in October.

There was also good news on the housing market as new home sales posted their largest increase in nearly 33-1/2 years.

“The economy seems to be building enough momentum that growth should accelerate as we move through the first part of next year,” said Joel Naroff, chief economist at Naroff Economic Advisers in Holland, Pennsylvania.

Private employers added 215,000 new jobs to their payrolls last month, according to payroll processor ADP.

It was the biggest rise in a year and beat economists’ expectations for a gain of 173,000 jobs. At the same time, the figure for October was revised up to 184,000 from 130,000.

Full Article HERE

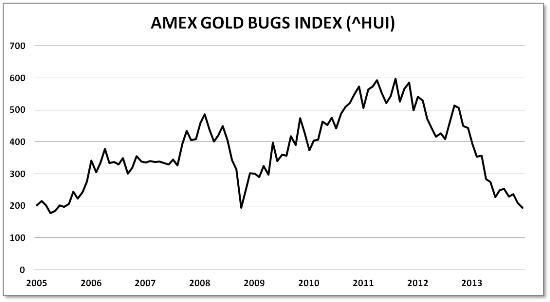

Let’s say you’ve got some traditional mutual funds full of stocks and bonds and they’re way up. You’re worried by all the taper talk and the charts that show share prices and margin debt back up to pre-crash levels, and you’re wondering whether it’s time to redirect some of that capital to someplace that no one is calling a bubble.

Meanwhile, you’ve noticed that precious metals mining stocks are in another of their periodic corrections, with this one looking a lot like 2008’s bloodbath — which was followed by an epic bull market:

But with gold and silver below the production cost of a lot of miners, there’s a ton of risk to go with the seemingly huge upside. So committing to individual miners is terrifying. Still, that’s how it always looks at the bottom.

So if you’re going to buy one, which would it be?

….continue reading HERE

In this exclusive article Clem Chambers, Forbes columnist and author of the Amazon No.1 investing bestseller 101 Ways to Pick Stock Market Winners, discusses the five golden rulesto help you start trading successfully.

There are many more people watching share prices than investing in stocks. Most realise that investing is the way out of living from pay check to pay check, but do not know where to start.

Stocks and shares seem to be the reserve of the rich; a risky business where the novice loses their shirt. But there must be away to get started without getting burned?

Here are five rules to stock market investing success to get you started.

Rule 1 – Build a stock portfolio of 30 shares.

Take no notice of the people that say put all your eggs in one basket. A portfolio gives you a certainty that bad luck won’t hurt you and that your choices on average will deliver the return your share picking deserves. This portfolio return over the years will outperform anything a bank will offer you on deposit and will compound.

A diversified portfolio will mean you will miss out on good luck, but investing isn’t about good luck. Bad luck and good luck cancel out over time but if you have too much of your money in too few shares then bad luck can knock you out of the game.

….Rules 2 thru 5 HERE

WASHINGTON (MarketWatch) — The Federal Reserve on Wednesday said the economy continued to expand at the same “modest to moderate pace” it has seen over most of the past year, though the details of the latest so-called Beige Book report show plenty of positive news with scarcely any negative developments.

According to the report, manufacturing continued to expand and plant managers were optimistic about the near term.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair