Timing & trends

![]() PDAC 2014: Don’t Rely on Elon Musk or Vladimir Putin to Boost Metal Prices

PDAC 2014: Don’t Rely on Elon Musk or Vladimir Putin to Boost Metal Prices

- We have just returned from our annual pilgrimage to PDAC

- This year the tone of the conference “felt” different– not necessarily in a good way

- There are several significant questions looming that the industry must consider

- Differentiation and diversification are key to survival and prosperity

Through last weekend and into this week, we attended the annual Prospectors and Developers Association of Canada (PDAC) Conference in freezing cold Toronto. PDAC is the largest mining conference in the world. It attracts just about everyone involved in the mining industry. More than anything, it represents a fantastic networking opportunity.

It has been most interesting to watch how sentiment has changed in recent years given the fall in metals prices and resulting struggles faced by ALL mining companies. This includes major producers Mid caps and across the value chain to Greenfield exploration companies.

I have to say, that despite the “buzz” which results from 30,000 people together, the tone of the conference this year was flat. That prevailing sense of optimism we have typically felt at a conference of this magnitude just didn’t appear to be there this year.

And so the question is why? Why, after three years of generally down markets for mining companies, did this year’s PDAC in particular feel different from others? 2014 has started off on a positive note with the TSX up 4.96% and the TSXV up 10.35% year-to-date. This has helped erase memories of a most challenging 2013.

The uncertainty I mention above can be boiled down to several questions – many of which we have discussed and debated in past Morning Notes. Paradoxically, this uncertainty and feeling of capitulation may be a good sign, that of a behavioural bottom.

I am on record early this year stating that the commodity super cycle is not dead, but has changed its complexion. I still believe that and think that profits can be made in mining equities as long as selectivity and patience are the hallmarks of an investment strategy.

The mining boom in the first decade of the 21st Century added a significant mineral capacity in the mining infrastructure, and reserves and resources across the entire commodity spectrum.

The two year decline in metals prices, from gold, rare earths, silver, and graphite has rendered much of this investment worthless at current prices. This has caused massive write offs in the gold industry for example. Many commodity prices have settled at levels above their historic averages, but costs have increased also.

While there are a number of questions we in the industry must face, I see six specific questions to consider at this point in the cycle:

1. How quickly can excesses be worked off? – It is clear that the days of the “wind at the back” of the mining industry (with China’s increasing appetite for a host of commodities) is over or at least paused. Mining companies of all market capitalizations have written down the value of assets, sold properties at a discount, or instituted strict cost discipline. Can this newfound focus help the market “turn” up as many of us are hoping for?

2. How quickly can China change its growth paradigm from investment and export-led to internal consumption? – I don’t believe China is headed for a hard landing, but give China’s leadership credit for acknowledging the necessity for a slower, more sustainable growth paradigm. Can this change, which is really a change in the average citizen’s mindset, occur fast enough to breathe life into a junior mining sector desperate for signs of increasing global demand?

3. How quickly can the rest of the Emerging Markets and Frontier Markets sop up this lack of demand from a slowing China? – China has size and scale, which is why so many of us focus on the country. Careful study of the growth dynamics of countries such as Indonesia, Poland, and Colombia is a wise. It is these countries and others that will fill a demand void left by China.

4. If not fast enough, what does this mean for the junior sector? – I think this question answers itself. In this scenario the Junior sector shrinks laying the seeds for the next metals cycle.

5. Is Geopolitics set to play an increasingly important role in the typical mining portfolio? The crises in Ukraine and Venezuela bring this question to the fore. Additionally, issues like slowing growth and inflationary pressures in emerging markets and resource nationalism appear set to provide investment opportunities elsewhere, but also may wipe out unsuspecting or careless resource investors.

6. What is a realistic investment strategy in the face of slow growth and excess capacity? – I explore this below.

Despite the dour tone of this Note, I am still optimistic over the medium to long term vis-à-vis commodity demand. Population dynamics and the ubiquity of technology dictate that many more individuals in the future are poised to live more commodity-intensive lifestyles.

A key takeaway from PDAC this year was that all commodities are not created equal. Uranium is clearly the “belle of the ball” right now. Differentiation and diversification amongst metals and across the value chain are keys to success going forward if you’re investing at this stage of the cycle.

It is increasingly clear that large projects, either in terms of tonnage or capital expenditure, are being re-evaluated in favor of smaller sized projects better able to fit into current and future demand forecasts. This is a good development.

On an additional positive note, there does seem to be a flurry of significant financings taking place, with NexGen Energy (NXE:TSXV) announcing a $10MM bought deal most recently. This is good news, specifically for the sustainability of junior uranium companies. If more financings of this type can be completed across various commodities, some of the questions I listed above will have a favorable outcome.

It was also abundantly clear at PDAC that money is pooling and consolidating assets across a host of metals in the precious and base categories. Private equity money has moved into the mining sector and is intent on consolidating properties, recapitalizing companies, and eventually spinning them out. Again, this is a longer-term positive sign for the industry as a whole, but differs from one metal to the next.

I wrote above that you can’t rely on Elon Musk or Vladimir Putin to boost metals prices. This may sound silly, but it’s true. With the recent announcement of Tesla’s (TSLA:NASDAQ) “Gigafactory”, share prices of US and Canada-based lithium exploration and development plays exploded. Similarly, Russian President Vladimir Putin’s movement of Russian troops into Ukraine sent gold and silver much higher.

I’ll be writing a note shortly on the TSLA Gigafactory and its implications for the junior sector. My point is that these isolated events tell us nothing about true supply and demand dynamics of commodities but do tell us everything about speculation and the fear and greed paradigm in financial markets.

Only organic growth, technological breakthroughs, and sound fiscal and monetary policies will provide the basis for increasing and sustainable demand. The travails in the mining markets today are setting the stage for the next move higher, but I continue to believe that a mixed global growth picture and excess capacity have delayed this move into the future. Patience and selectivity are still the most prudent way forward and can be rewarding in the interim as we’ve seen with select uranium plays.

Note on a portfolio sale: I will be taking profits in half of my position in URZ (5,000 shares) within 24 hours of receipt of this note. I still like the story and believe that near-term production plays in uranium are the most appealing, but want to lock in a portion of my gains.

Note on a portfolio sale: I will be taking profits in half of my position in URZ (5,000 shares) within 24 hours of receipt of this note. I still like the story and believe that near-term production plays in uranium are the most appealing, but want to lock in a portion of my gains.

To sign up for For FREE Morning Notes go HERE

The material herein is for informational purposes only and is not intended to and does not constitute the rendering of investment advice or the solicitation of an offer to buy securities. The foregoing discussion contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 (The Act). In particular when used in the preceding discussion the words “plan,” confident that, believe, scheduled, expect, or intend to, and similar conditional expressions are intended to identify forward-looking statements subject to the safe harbor created by the ACT. Such statements are subject to certain risks and uncertainties and actual results could differ materially from those expressed in any of the forward looking statements. Such risks and uncertainties include, but are not limited to future events and financial performance of the company which are inherently uncertain and actual events and / or results may differ materially. In addition we may review investments that are not registered in the U.S. We cannot attest to nor certify the correctness of any information in this note. Please consult your financial advisor and perform your own due diligence before considering any companies mentioned in this informational bulletin.

“Between two evils, I always pick the one I never tried before.”

“Between two evils, I always pick the one I never tried before.”

Mae West

Time for Oil to trend lower as Ukraine pressure ebbs: Chart View

I have been getting my clients whacked on my short oil idea. But maybe hope springs eternal, as this setup may add some validation a “corrective top” may be in place. I shared these comments yesterday (chart updated this morning):

On Monday, crude surged on the Ukraine concerns breaching key resistance at 104.38 and likely triggering a bunch of “buy stops” for price led players who were short. Non-commercial speculators in the futures market are extremely long this market. The latest Commitment of Traders report shows 514,502 long with 98,064 short contracts on the NY Mercantile Exchange. That seems a one-way bet. You can also see in the bottom panel there was divergence, or momentum loss, into the recent price high. Momentum leads price! I have not been shaken from the fundamental supply/demand story which still seems bearish for crude.

If you are interested in either of the currency services we offer—Black Swan Forex or Currency Options Strategist—you can learn more at our website at www.blackswantrading.com .

Regards,

Jack Crooks

Black Swan Capital

www.blackswantrading.com

Twitter: @bswancap

Phone: 772-349-6883

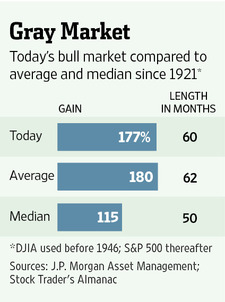

“A five-year anniversary should give pause to anyone who lends much credence to historical patterns. Going back to 1921, the current bull market’s rally is only two percentage points shy of the average performance. And the average bull market has lasted only six weeks longer.”

On Fifth Birthday, Aging Bull Market May Tire Easily

Talk about a lavish birthday gift.

Strategist Sam Stovall of S&P Capital IQ points out that when bull markets reach their fifth anniversary—as the current one will this week—they have historically clocked another 26% gain, on average, if they survived for another year. That would, given today’s level, create up to an additional $5 trillion in U.S. stock-market value.

But the same people who suggest that history might repeat, or at least rhyme, ignore less pleasant parallels. The last time pundits trotted out similar measures was in October 2007 when that bull market turned five. It ended just days later.

Those who suggested the market could rise into 2008 and beyond had convincing arguments. The market’s trailing price/earnings ratio was 16.9 times—actually lower than at the start of that bull run. And stocks had merely doubled from the bottom, a lower increase than in a typical bull market.

Most convincingly, the Federal Reserve had the market’s back. Less than a month earlier, it had reduced rates by half a percentage point. Deeper than expected, that cut catapulted the Dow higher by 336 points on the day.

Trimming half a percentage point seems positively quaint compared with trillions of dollars in quantitative easing recently. But it would be foolhardy to assume that monetary policy has rendered bear markets extinct. And for what it’s worth, the current bull market has seen the S&P 500 rise by 177%. Today’s trailing P/E ratio of 17.9 times, meanwhile, is a full point higher than in October 2007.

In fact, a five-year anniversary should give pause to anyone who lends much credence to historical patterns. Going back to 1921, the current bull market’s rally is only two percentage points shy of the average performance. And the average bull market has lasted only six weeks longer.

Moreover, those averages are skewed higher by the long 1920s and 1990s bull markets, marked by speculative manias and ending in economic crises. One way to factor out those extremes is by focusing on median performance and life span instead. These are 115.4% and 50 months, respectively—leaving the current bull market looking long in the tooth indeed.

This week’s market milestone may lead to plenty more open road. Just remember that dangerous curves are tough to see at such high speeds.

Write to Spencer Jakab at spencer.jakab@wsj.com

What do you need to keep on the path towards your goals? Ultimately, it comes down to you making the choice and sticking with it.

What do you need to keep on the path towards your goals? Ultimately, it comes down to you making the choice and sticking with it.

Most of us need a set of circumstances to work in our favor in order to get to the point of getting on the path. Of course, there are those who need to be slapped around by life a bit before they realize that drifting aimlessly does not work.

Let us look at some of the criteria that is necessary to get on a winning path:

Knowing there is a path

In the Fidelity ads they show a green path, which basically tells you that they will guide your future investments as soon as you become a customer. So what do they have that you need to acquire so you can do it on your own? You need to know what you want to achieve and you need a list of what you feel are achievable steps to get you there.

Creating a plan

A plan consisting of achievable steps leading to your end goals makes the path easier. With a plan you are less likely to deviate from the path and know when you do. Contingency planning for every possible scenario will give you the confidence to overcome the hurdles along the way.

Managing obstacles

Instead of looking at obstacles or difficult moments as problems, you must see them as challenges. Break each problem down into doable actions within the context of your overall plan. Remember to ask for help and delegate. You then give others an opportunity to give and to feel important in your life.

Having people who are rooting for you

Each of us needs or wants to have a cheerleading squad who roots for us when we are up and picks us up when we fall down. While you can be your own cheerleader, that extra positive energy you get from others gives you a great motivation towards your path.

Believing that you have what it takes

You have to believe that you have what it takes, or that you can get what it takes. A belief is what is true for you in your universe. When you can picture what you want and see yourself in that picture, you are on your way. When you dream about the same picture repeatedly adding more detail, you give your neurological system the map it needs to follow. When you limit your dreams you limit yourself.

Enjoying the process of successes along the way

The process must be enjoyable, satisfying and make you feel that you are heading towards the finish line. Most people need the incentive of rewards. Rewards come in many different packages and it is important to know what reward motivates you.

Rewards can be:

· The satisfaction of accomplishment of each step

· The recognition of someone whose opinion has value to you

· A physical reward like a book, a massage or a vacation

Conclusion

Sticking to a predetermined path towards each area of your life and having each area complement the other will guide you towards your goals. You only have one life in this body so you may as well enjoy the process of a path towards your ultimate goals.

Adrienne’s Free Webinars

Adrienne presents free webinars on the psychology of trading

Website: www.TradingOnTarget.com

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair