Timing & trends

Russia confirms our tracking of capital flows. Adopts our figure of $50 billion for the quarter.

We have been investigating the Russian capital flows in more detail. We see two trends emerging that is reflecting the war tensions. Foreign capital that invested in Russia is pouring out, but at the same time, the Russian Oligarchs are pulling back money in western banks. They do not yet seem to be investing in Russian banks for they fear the ruble. They have been buying the euro and taking cash home rather than dollars. This is giving some lift to the euro. Clearly, capital is confused on both sides of the conflict.

We have been investigating the Russian capital flows in more detail. We see two trends emerging that is reflecting the war tensions. Foreign capital that invested in Russia is pouring out, but at the same time, the Russian Oligarchs are pulling back money in western banks. They do not yet seem to be investing in Russian banks for they fear the ruble. They have been buying the euro and taking cash home rather than dollars. This is giving some lift to the euro. Clearly, capital is confused on both sides of the conflict.

Nonetheless, prior to every war, capital flows give advance warning more often than not. It appears those who know, move money appropriately. This time, the Russian Oligarchs are grabbing the euro in cash for that can be obtained in larger denominations than US dollars, plus they have no idea whose currency will survive given it could be cancelled as well or counterfeited as part of the economic war (another reason to cancel the currency and move totally electronic using war as the excuse). The Oligarchs are between a rock and a very hard place. The ruble looks risky, but then the USA is the enemy.

Here is a German counterfeit British 5 pound note from World War II. It was very, very good. So beware. War at this time would have the benefit of eliminating currency altogether to prevent counterfeiting, but then again that has been the goal to get every penny of tax. It is also suggested that it will eliminate crime.

Keep in mind eliminating currency will also eliminate bank runs. It is a win-win for government and war may be the excuse they need to eliminate all cash and that would help Europe right now who is staring straight in the eye of perhaps the worse banking collapse in history of banking.

The propaganda war still rages. There is all sorts of disinformation hitting the internet under the pretense of being part of the Anonymous movement, but this is just counter-intelligence right now. There are a lot of fake emails and claims of reports and phone calls all designed to move the public opinion in one direction or the other,

Then there is the missing Malaysian plane. Rumors now fear that it was taken someplace to be used for a terrorist attack later in China to get the masses there outraged. This is purely speculation at this point, but we are trying to test the veracity of this theory. Of course it could just be aliens who escaped from Area 51 or the White House – hard to tell the difference sometimes.

Ed Note: Here is a long explanation by Martin of the Russian people and how to understand them, that you can understand their likely moves during crisis:

For those with Short Term speculative money, Przemyslaw Radomski lays out the case for making money on a decline and protecting your capital with stops he lists below – Editor Money Talks

PMs Decline on Huge Volume

Briefly: In our opinion short speculative positions (half) in silver and mining stocks are justified from the risk/reward perspective.

The precious metals sector declined yesterday, which was likely to happen regardless of many factors pointing to a different conclusion, or simply because the precious metals sector was overvalued. The question is if we (charts courtesy of http://stockcharts.com) think that lower precious metals values are likely:

Click on image for larger view

They are. The Euro Index is still below the declining long-term resistance line and it’s still likely to decline. What we wrote previously is also up-to-date:

Consequently, the index is likely to decline sooner rather than later and this could trigger a decline in the precious metals sector. Of course, if the situation in Ukraine gets worse, PMs might rally or the decline could be postponed, but at this time the tendency for this market seems to be to move lower.

Click on image for larger view

Gold was likely to move lower based on numerous technical factors and it has. The decline is not significant yet, but the volume on which the decline has materialized suggests that it will soon be. The small breakout above the 38.2% Fibonacci retracement level was just invalidated, which is a bearish sign.

Click on image for larger view

As far as silver is concerned, we didn’t see a major plunge, but we see a move below the 2008 high once again. Overall, silver’s recent moves are not bullish (it almost hasn’t reacted to the situation in Ukraine) and the outlook remains bearish.

Gold wasn’t the only part of the precious metals sector that invalidated a move above a previously broken retracement – miners also declined below one, an important one. The GDX ETF moved below the 61.8% Fibonacci retracement level and invalidated the breakout above it. Moreover, just like it was the case with GLD, the move took place on huge volume.

Now, the miners haven’t moved below the rising support line (at least not yet), so the short-term outlook isn’t extremely bearish, but it seems that we will see lower mining stock values relatively soon.

It seems that the precious metals sector will move lower in the coming weeks, but just in case the situation in Ukraine deteriorates, we are keeping half of the long-term investment position in gold. In fact, gold has been outperforming both silver and mining stocks since Russian troops entered Crimea.

If the precious metals market declines, it seems that short positions in silver and mining stocks will gain more than the long-term investment in gold will lose, and if the sector rallies, then gold’s appreciation – due to its outperformance – can more than make up for the loss on the short positions in miners and silver. Naturally, the above depends on the size of the positions, but still, it seems that utilizing this spread (long gold and short silver and miners) has been a good idea.

It seems to us that if it weren’t for the events in Ukraine, the precious metals sector would be already declining and perhaps testing the 2013 lows or moving below them. This could still take place and it’s quite likely to happen once the situation in Ukraine stabilizes.

To summarize:

Trading capital (our opinion): Short position (half): silver and mining stocks.

Stop-loss details:

– Silver: $22.60

– GDX ETF: $28.9

Long-term capital (our opinion): Half position in gold, no positions in silver, platinum and mining stocks.

Insurance capital (our opinion): Full position

Thank you.

Przemyslaw Radomski, CFA

Founder, Editor-in-chief

Tools for Effective Gold & Silver Investments – SunshineProfits.com

Tools für Effektives Gold- und Silber-Investment – SunshineProfits.DE

* * * * *

Disclaimer

All essays, research and information found above represent analyses and opinions of Przemyslaw Radomski, CFA and Sunshine Profits’ associates only. As such, it may prove wrong and be a subject to change without notice. Opinions and analyses were based on data available to authors of respective essays at the time of writing. Although the information provided above is based on careful research and sources that are believed to be accurate, Przemyslaw Radomski, CFA and his associates do not guarantee the accuracy or thoroughness of the data or information reported. The opinions published above are neither an offer nor a recommendation to purchase or sell any securities. Mr. Radomski is not a Registered Securities Advisor. By reading Przemyslaw Radomski’s, CFA reports you fully agree that he will not be held responsible or liable for any decisions you make regarding any information provided in these reports. Investing, trading and speculation in any financial markets may involve high risk of loss. Przemyslaw Radomski, CFA, Sunshine Profits’ employees and affiliates as well as members of their families may have a short or long position in any securities, including those mentioned in any of the reports or essays, and may make additional purchases and/or sales of those securities without notice.

With continued chaos and uncertainty in global markets, today KWN is publishing another incredibly important piece that was written by a 60-year market veteran. The Godfather of newsletter writers, Richard Russell, warns that “gold is being outrageously manipulated,” as the Fed prepares to stun the world by opening up “the floodgates of liquidity” for “QE5.” He also discussed Putin, stocks, the Great Recession, and China.

Russell: “Success in investing includes a number of nonspecific items. Patience, avoidance of greed, desire for peace of mind, avoiding huge losses, experience and judgment. From the low of 2009, the major Averages have more than doubled, and have moved into overvalued territory in terms of book value, price to earnings and dividend yield.

….read more HERE

Concern about the vulnerability of US stocks right now.

Concern about the vulnerability of US stocks right now.

Value investor and founder of the Baupost Group, Seth Klarman, has expressed similar concerns in his recent letter to shareholders. (If you’ve never heard of Klarman, that’s because he tends to shun the limelight. But the performance of the Baupost Group is legendary. It is one of the largest hedge funds in the world. And according to Bloomberg, it is ranked 4th in net gains since inception.)

Klarman has focused his attention on the big gap between recent US stock market gains and sluggish underlying corporate earnings:

No one can know what the future holds, but any year in which the S&P 500 jumps 32% and the NASDAQ Composite 40% while corporate earnings barely increase should be cause for concern, not further exuberance. It might not look like it now, but markets don‘t exist simply to enrich people.

And he’s warned that someday the current rally will mutate into big declines:

Someday, financial markets will again decline. Someday, rising stock and bond markets will no longer be government policy. Someday, QE will end and money won‘t be free. Someday, corporate failure will be permitted. Someday, the economy will turn down again, and someday, somewhere, somehow, investors will lose money and once again come to favor capital preservation over speculation. Someday, interest rates will be higher, bond prices lower, and the prospective return from owning fixed-income instruments will again be roughly commensurate with the risk.

The best protection against these inevitable declines is portfolio diversification.

Diversification is simple enough. The less that any single bad event of any kind can affect your portfolio, the more diversified you are.

That means investing in a range of asset classes – commodities, real estate, cash, tangible assets, etc. – outside of stocks. And also diversifying your stock market investments outside of the US.

This won’t make for exciting dinner-party conversation. But it will be your best defense in another market downdraft. Prepare now before it’s too late.

Wealth comes in many forms, but only two general categories: tangible and financial. Tangible wealth is made up of real, physical things like buildings, farmland, oil wells, commodities, etc. These things can be seen and touched, and – crucially – they don’t have counterparty risk. That is, no one else has to make good on a promise for a tangible asset to have value.

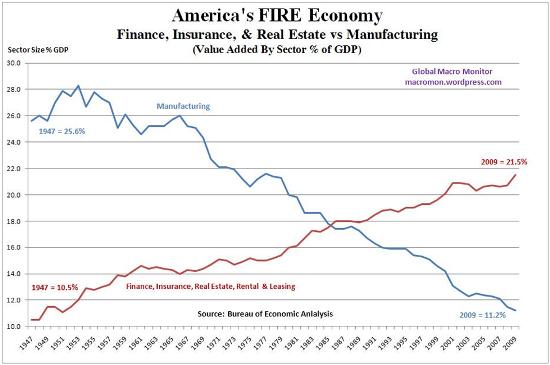

Financial assets like bank deposits, insurance policies, bonds, and annuities do have counterparty risk, which is to say they depend on someone else’s promise. A bank deposit, for instance, only has value if the bank is willing and able to produce that money when the account holder requests it. And a piece of paper currency is only valuable if the government manages the money supply properly. The part of the economy represented by industries that deal primarily in financial assets is known as FIRE, for finance, insurance, and real estate (real estate in this case referring to mortgages and other property loans that are packaged and traded).

Equities, because they represent ownership shares in public companies, can be either tangible or financial depending on the underlying company. A share of Exxon Mobil stock is a tangible asset because oil wells are real, while a share of Goldman Sachs or JP Morgan Chase would be financial because a bank’s wealth is primarily in the form of loans and other financial instruments.

Over long periods of time these two asset categories tend to move in and out of favor, with tangible assets being more prized in hard, uncertain times when preservation of capital is paramount and counterparty risk is suspect, and financial assets being favored when times are good and people have grown to trust major financial institutions and governments to keep promises and generate big returns.

One of the keys to successful money management is to understand which category is ascendant and therefore the more profitable/safe place to be. During a boom, one should own financial assets until they become relatively-overvalued (as they did in 1929, 1968, and 2000), then shift into tangible assets and own them until they become overvalued (1947 and 1980).

As this is written in late 2013, the world is at one of these inflection points, perhaps the biggest ever. As the following charts illustrate, during the expansion of the credit bubble that began after World War II Americans gradually became more and more optimistic about the future and more trusting of banks and governments. Because the good times seemed likely to continue, using other people’s money to achieve one’s ends came to be seen as increasingly reasonable and wise. Debt expanded and finance (i.e. the debt industry) became an ever-more important part of the economy, while manufacturing in particular and tangible assets in general became relatively less important. The FIRE economy doubled as a percent of GDP between 1947 and 2008 while manufacturing fell by nearly two-thirds. For investors, the standard portfolio of stocks, bonds and dollar cash was a great way to build wealth, with very little long-term downside risk.

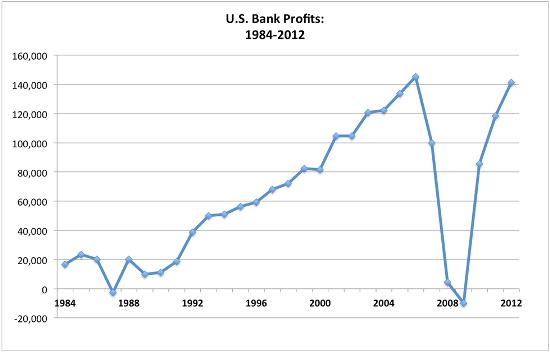

That faith was shaken by the crash of 2008, which should have marked the end of the post-WWII cycle of credit expansion and ushered in a mass-migration out of finance and into tangible assets. Instead, the world’s fiat currency managers upped the ante, cutting interest rates to zero and flooding the system with newly-created currency in an attempt to re-inflate the financial bubble. They handed the biggest banks effectively-unlimited amounts of free money, and the banks, reluctant to lend so soon after their near-death experience, simply deposited their excess reserves with the Fed, earning a small but risk-free return. Illustrating just how much money the banks were given, even with this hyper-conservative investment strategy, the industry reported record profits in 2013.

And within the banking industry it was the major banks, as the recipients of most of the Fed’s largesse, which reaped most of the rewards. In 2013, the 1.5 percent of banks with the largest asset bases earned about 80 percent of the industry’s profits. Big-bank stocks, meanwhile, were among the best performers of the post-crash bull market. The debt monetization experiment had succeeded in lengthening what was already an extreme pendulum swing towards financial assets.

So now the question becomes, will the monetary authorities be able to push the pendulum further, or was the financial asset recovery of 2009-2013 the last gasp of a dying trend? By now you know that we’re firmly in the latter camp. The expansion that began after World War II has produced extraordinary amounts of debt, leverage and complexity, from a financial standpoint achieving “peak” everything. Finance has no further to go, and the great migration out of financial assets and into tangible things is about to begin, on a scale commensurate with the historically-unprecedented size of the post-WWII credit bubble.- Read more here.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair