Timing & trends

Gold and Commodities Supercycle

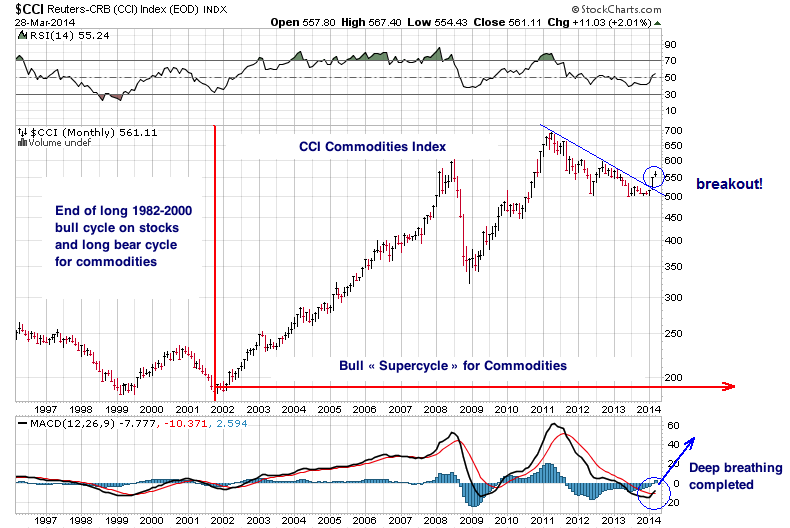

The breakout observed on the CCI commodities index should correspond to another leg in the bear market for the dollar and to another leg in the bull market for commodities that started in 2001 and that can be qualified as a « supercycle ».

During this supercycle, a large part of the rise in prices has to be attributed to the loss of purchasing power of the dollar. To the point, if we measure this bull market in swiss francs, the general rise in prices since 2001 doesn’t exceed 40%, whereas, in dollar terms, prices have already gone up by 200%!

Gold, as an excellent safe haven against the fall of the dollar (and of the other currencies, but mainly the dollar), will perform best (along with silver) for the total duration of this supercycle.

A commodities supercycle can easily last between 15 and 20 years. If we take into account the pressures exerted on commodities by countries such as China and India, world population growth, peak production already reached in several commodities and climactic changes affecting soft commodities production, this supercycle is far from being done!

One thing is certain : The commodities index will not get back to its bull market without gold and silver!

By comparing gold with commodities, we can get the monetary risk premium associated with gold with a gold/CCI ratio, which gives us gold’s relative strength versus all other commodities.

We clearly see that gold started its bull market in all currencies only when it started to emancipate itself from the whole commodities sector, around the Fall of 2005. Up to that time, the monetary risk premium was zero, and the bull market in gold was only seen in dollar terms.

The risk premium went up to 90% with the first financial crisis, in 2008, marked a pause in 2010, and then exploded to 126% with the Eurozone debt crisis.

The current low-risk premium environment is about to end, because the current actions by the Fed will be unkind to the real estate market, the bond market (less and less buyers of U.S. debt = long-term interest rates rising), and to the stock market, in a bubble situation.

It is as if the Fed were walking on very old boxes full of explosives on which the only remaining solid plank was the faith in the system, e.g. this on-going bluff about an economic recovery! The Fed doesn’t have a choice anymore… it is only recharging its rifle to keep a semblance of integrity, but all it can do to fight against the deflationary pressures of this long cycle (Kondratieff’s winter) is to print, print, and print some more.

The next crisis, in all probability, will be a dollar crisis, and it will contaminate the whole of the monetary system, which is already in a competitive devaluation contest. The need for physical gold as a debt extinguisher and a guarantee of stability for currencies will become larger and larger and will most probably lead to the final phase of this supercycle. $1,300 gold will be seen as an aberration in a few years!

Regarding this current test of the 200-day moving average for gold, the breakdown is only 1%, so it is within the margin for tolerance, if we compare today’s golden cross with the one we had in the bull market of 2001, where the breakdown had reached 1.3% (read my preceding analysis). If this test fails, we could still be trading without any clear direction in a sideways range between $1,250 and $1,425 for a few more months, but this will only make the next price retracement move and the monetary risk premium more violent!

About Léonard Sartoni

Léonard Santoni is an independent contributor who often publishes for a Swiss Dealer GoldBroker.com. Léonard has been analysing the gold market since 2003. In 2007, he wrote a book, 2008-2015: Why Gold Will Outperform Stocks and Bonds”

The Dow rose 74 points yesterday. Gold dropped $3 an ounce.

What do you expect? Yesterday was April Fools’ Day.

This should be a good quarter for stocks, according to economist Richard Duncan. He believes “excess liquidity” – cash and credit in excess of what borrowers and spenders actually need – drives asset prices.

We haven’t been able to connect every tarsal, hallux and tibia of Duncan’s theory. But the skeleton, as he presents it, is serviceable… even attractive. The more excess liquidity, the more people use it to bid up asset prices. As excess liquidity goes down, so do asset prices – particularly stocks.

Duncan expects the coming quarter to produce a record of excess liquidity. The Fed is still pumping liquidity into the market at the rate of $65 billion every month. Meanwhile, it is tax time, so the government’s needs for borrowing will be relatively low. And according to Duncan, the difference between the available liquidity and the need for it in the regular economy has to go somewhere.

But after this quarter, the outlook changes. The Fed is scheduled to wind down QE by the end of the year. And the federal government’s rosy budget scenario will begin to fade – meaning more government borrowing. That means the third quarter is expected to produce only a slightly positive excess of liquidity. And in the fourth quarter, says Duncan, the excess turns into a shortage.

If the Fed persists in its plans to taper QE, in other words, the third quarter will likely see a selloff in the US stock market. This will give the Fed’s forward guidance a kick in the rearward quarters.

Instead of continuing to taper, the Fed will panic. Its entire theory of life… its philosophy… and its sacred religion will be challenged. In its view, credit, prices and stocks must ALWAYS go up.

There was a time when the Fed was merely charged with making sure the value of the nation’s money was stable. It failed miserably. So it was rewarded with more responsibility. Its mission creeped toward making sure the nation had full employment.

At that, too, it fails regularly. So, now it has taken upon itself (Congress never authorized it) to hold interest rates down and push consumer prices up.

Actual consumers prefer lower, not higher, prices. But such is the hubris of central bankers that they are willing to contradict 100 million households. They insist on dollar earners and savers losing about 2% a year of their buying power.

As we have been saying, it is an odd recovery that leaves the average American with less income than he had before it began. But it is an odd recovery that we have.

Stock prices – not to mention prices for antique guitars and gaudy modern “art” – have soared. Incomes, meanwhile, have limped downward. This leaves the typical American feeling richer… but with less money in the bank.

At $81 trillion, total US household wealth has never been higher. But it is supported by precious little household income.

Duncan tells us the ratio of household disposable income to household wealth is important. That’s because wealth must be supported by income… or it disappears.

This is exactly what happened – twice – in the last 15 years. From 1952 until the 1990s, the ratio of household wealth to disposable income was fairly stable – at about 525%. Then it rose above 600% – on two occasions. At the end of the 1990s, before the dot-com crash. And in 2006-07, before the global financial crisis.

Today, once again, the ratio is above 600% – for only the third time in history. And once again, we should be prepared for a crash – or at least a substantial bear market – in US stocks.

That will probably happen in the third or fourth quarter of this year. And it will probably be followed by an announcement by the Fed that, instead of taking QE off the table, it will continue the program.

And instead of allowing short-term rats to rise six months after QE ends, as Janet Yellen suggested in her recent post-FOMC press conference blooper, the target rate will stay at zero for this year… and all of 2015, too.

Duncan believes “QE 4” will produce the same results as QE 1, 2 and 3: It will send stocks flying again. If so, we could be looking at another big run-up in the stock market… after, of course, a substantial decline.

Our advice: Get out of the US stock market now. This market is manipulated, overpriced and dangerous.

Regards,

Bill

P.S. Will has put together a detailed report on the coming central bank-induced crash… and how to protect your savings. To learn more, follow this link.

Two Ways to Protect Yourself

from Modern-Day “Mohawk Indians”

From the desk of Braden Copeland, Editor, Building Wealth

If you saw the latest 60 Minutes bit about Michael Lewis’s new book, Flash Boys: A Wall Street Revolt, you’re probably eager to know how you can avoid being exploited by the nasty trading activity the book exposes.

If you saw the latest 60 Minutes bit about Michael Lewis’s new book, Flash Boys: A Wall Street Revolt, you’re probably eager to know how you can avoid being exploited by the nasty trading activity the book exposes.

Here you will find your answer…

Flash Boys goes behind the scenes to reveal certain truths about high-frequency trading (HFT). This is where computers trade billions of dollars in and out of the market at lightning-fast speeds.

Their goal is to scalp money off of investors by taking advantage of inefficiencies in the electronic execution of trades. Think of them as modern-day “Mohawk Indians.”

Lewis’s show-stopping quote at the start of the 60 Minutes segment was, “The stock market’s rigged. The United States stock market, the most iconic market in global capitalism, is rigged.”

Lewis went on to explain how HFT operators are abusing investors. (To see the entire segment, go here. The video will open in a new window so you may close it and easily return here to finish reading.)

In case you have any doubt, I want to tell you Lewis is right. The proof is undeniable. But I also want to tell you this…

If you are an individual investor managing your own account – and making investments with time horizons of months or years instead of seconds and days – this big Lewis reveal does not matter, as long as you:

1. Use “limit orders” when buying and selling

2. Use “stops” based on closing prices and do not enter them in the market

First, let me explain what “limit orders” are. They are orders that include instructions for your trade to be placed only at a certain price or “limit.”

For example, when you want to buy a stock trading for about $20, entering a “limit order” with a limit price of $19.80 will tell your broker not to buy the shares unless they are trading at or below that price.

Entering a “market order” will tell your broker to make the trade at the best market price he can get when he places your trade. It could turn out to be more than you expect (or want) to pay – $20.20, for instance.

Sell limit orders work exactly the same way. The limit price in this case tells the market the minimum price you are willing to accept for your shares.

Placing a simple market order would again put you at the mercy of the market. And that, in turn (although practically guaranteeing your order will be completed) puts you closer to the situation Lewis’s story exposes.

A limit order keeps you in control.

Now, let’s turn to the second rule about “stops.”

Stops are something I discuss in detail in my upcoming special report, “Two Simple Ways to Keep the Wealth You Build.” (You can learn how to find out more about it below.) A stop in this case is a trigger – a price you have set that, should the price of shares fall below it, signals it is time to sell.

To protect yourself from the situation Lewis has outlined, there are two simple parts to the rule about using stops that you need to follow:

1. Only let closing prices trigger your stops. (Don’t let intraday volatility – much of it caused by HFT scalpers – stop you out of your positions.)

2. Don’t enter your stops in the market. (Keep them away from your broker and monitor them yourself.)

Properly managing your stops this way will help you avoid nasty, unexpected surprises. It will keep you in control of your trades. It’s that simple.

If you follow the rules here with your independent investing – use limit orders for buying and selling and make sure to follow both parts of the stop rule – you’re set. Lewis’s revelation about the market’s modern-day “Mohawk Indians” will not be your problem.

Editor‘s Note: To learn more about Braden’s new report, “Two Simple Ways to Keep the Wealth You Build,” you can email him at bwfeedback@bonnerandpartners.com. Include “Two Simple Ways” in the subject. You can also follow him on Facebook atfacebook.com/braden.copeland or Twitter with @BradenCopeland.

Q: How much below the asking price can an offer be made to seem reasonable for the seller? I hear people saying 7-8% on average, but if I believe that the true value of the property is closer to -30% off the asking price – will it look like I’m trying to low-ball?

Q: How much below the asking price can an offer be made to seem reasonable for the seller? I hear people saying 7-8% on average, but if I believe that the true value of the property is closer to -30% off the asking price – will it look like I’m trying to low-ball?

A: That is never the issue … offer and acceptance are a matter of negotiation, market conditions, terms and urgency of the seller’s need to sell and buyers ability to pay … etc.

In the US properties have been sold for a number of years at 50% below asking price.

In Vancouver for many years, nothing sold over asking.

You never find out a vendor’s condition until you try.

Much success,

Ozzie

One of the most difficult and perplexing problems for realtors and investors is finding current Gross and Net Income Multipliers and Cap Rates. Determining the value of an income property generally involves establishing either the Gross or Net Income Multipliers, or the Cap Rate according to comparables.

There are a number of difficulties:

Information relating to a sale of a commercial property is often confidential and difficult to obtain. While the sale price can usually be determined, the Income and Expense Statement, Net Operating Income etc. is often not available, making it difficult to calculate the financial measures.

Finding comparables for a residential property is relatively easy. There are usually plenty of recent sales and an abundance of comparables or near comparables. In contrast, there are relatively few commercial sales, and finding comparables is very difficult because there may not be many comparables available, and obtaining the information such as the income and expenses may be difficult.

The Net Operating Income is probably the most widely used indicator of the building’s financial performance, and is frequently used in determining the value of the property. The Net Operating Income is the cash remaining after deducting the Operating Expenses from the Effective Gross Income (EGI). There are several items, which often appear on financial statements, which must be deleted before calculating the Net Operating Income (NOI).

The Capitalization Rate:

The Cap Rate is calculated as follows:

Cap Rate = (Net Operating Income / Market Value) x 100

Cap Rate = (NOI / MV) x 100

Example:

Net Operating Income (NOI): $239,430

Market Value (MV): $3,420,000

Cap Rate = (239,430 / $3,420,000) x 100

Cap Rate = 7%

The Cap Rate of 7% represents the annual return before mortgage payments and income taxes on the total investment of $3,420,000.

Alternatively, if the Cap Rate can be established from comparables, we can determine the likely selling price of a property. For example, if the cap rate is 7.5 % based on comparables, and the Net Operating Income (NOI) for the building is $105,000 , the potential selling price can be calculated as follows:

MV = (NOI / Cap Rate) x 100

= (105,000 / 7.5) x 100

= $ 1,400,000

The Net Income Multiplier (NIM)

The Net Income Multiplier (NIM) is the inverse of the Cap Rate

NIM = 100 / Cap Rate

or Cap Rate = 100 / NIM

As an example, if the NIM is 11, the Cap Rate is:

Cap Rate = 100 / NIM

Cap Rate = 100 / 11

Cap Rate = 9.09%

Both the Cap Rate and its counterpart the Net Income Multiplier are used in the real estate industry to estimate the market value of a property. However, in recent times, the Cap Rate has become the more popular financial measure. Regardless of which measure is used; they both produce the same estimate of market value.

The Net Income Multiplier is expressed as follows:

Net Income Multiplier (NIM) = Market Value / Net Operating Income

i.e. NIM = MV / NOI

Example:

Net Operating Income: $239,430

Market Value (MV): $3,420,000

NIM = MV / NOI

NIM = 3,420,000 / 239,430 = 14.28

Alternatively, if the Net Income Multiplier can be established from comparables, we can determine the likely selling price of a property. For example, if the Net Income Multiplier is 7.0 based on several comparables, and the Net Operating Income for the building is $180,000 , the potential selling price can be calculated as follows:

MV = NOI x NIM

MV = $180,000 x 7

MV = $1,260,000.

About the Writer:

Ozzie Jurock is the president of Jurock Publishing Ltd., Editor of Real Estate Insider. Publication and Author of Forget About Location, Location, Location

Related Links:

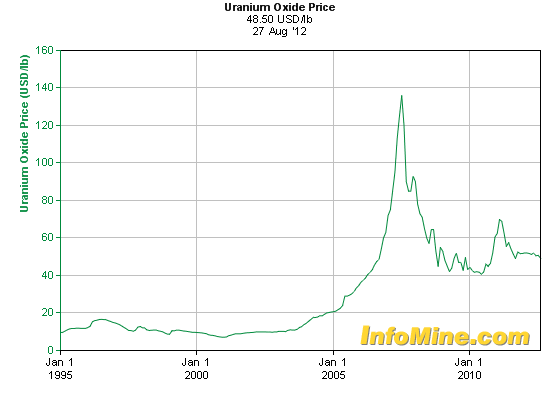

Uranium, Rare Earths, Graphite, Lithium & Cobalt. Take for example Uranium. At the end of March/2014 it was trading at $34, that’s a big discount from the $135 you can see on the chart below. With the coming Japanese reactor restarts on top of the long term Green movement’s opposition to nuclear power, supplies are getting tight.

The author of this thorough article also goes over the Rare Earth markets plus projects & companies in reliable political jurisdictions. With the anticipated boom in agricultural foodstuffs there is research too on what he expects to be a long-term boom in Fertilizer.

A really good read HERE – Money Talks Editor

For many, it’s the forgotten variable in accumulating wealth…

A good blue-chip stock can bring you thousands of dollars in dividend income every month.

But if you’re blowing money on things you don’t need, you’ll never build substantial wealth… no matter how well your investments are performing.

When it comes to watching your spending, it’s best to focus on big-ticket items like homes, vacations, and furniture. You can also make the mistake of spending unwisely on cars.

Below are two of the costliest mistakes you’ll ever make on your car…

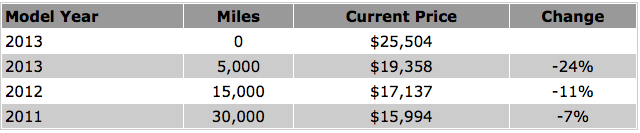

Most people have heard that when you buy a new car, it loses a big chunk of value as soon as you drive it off the lot… But how much?

We ran a quick test using my favorite American car – the Ford Taurus. According to the Kelley Blue Book independent vehicle-valuation service, you can still buy a new 2013 Taurus for $25,504.

The “fair price” for a used 2013 Taurus in excellent condition: $19,358. The car drops in value by 24% that first year. Is it worth an extra $6,000 just to be the first to drive this car? Not to me.

You can see how big your savings are going to be from new to used when you look at a few more years in this table below. The table shows the current prices on the following model years and mileages, according to the Kelley Blue Book.

Don’t ever pay extra for the “new-car premium.” The savings of $8,000 every six or seven years over a few decades of car driving adds up to nearly $100,000 extra money in retirement.

The dividends from investing that money over time could allow you to drive a brand-new car and do other things with the extra money in your retirement. But spend it early, and you’re broke in your later years…

Many rental-car companies will pressure you to accept their insurance when you pick up one of their cars… Don’t fall for the hard sell.

The premium adds $10-$30 extra per day. Instead, just pay with a credit card (which is required in most cases anyway)… Many cards offer collision-damage coverage on domestic (and even foreign) car rentals.

Visa, for example, will reimburse your auto-insurance deductible, towing charges, administrative fees, and loss-of-use charges imposed by the rental company.

You just need to do a few things to make sure you’re covered. Most credit-card companies will require you to use the card that offers the coverage to pay the rental in full.

You also have to decline any coverage the rental company provides. Visa, MasterCard, American Express, and Discover all have slightly different policies. And not every card offered by the company has this coverage.

Just call the company’s customer service to determine if you have this coverage, learn the terms, and save hundreds of dollars a year in fees.

Also, it’s likely that much of the coverage you have under your regular car-insurance policy carries over to your rental car. Just call your insurance company to find out what’s covered before you rent next time.

As I mentioned at the start of this essay, making good money with your investments is just one part of accumulating wealth. Smart spending is another. Keep these ideas in mind when spending on cars… and your wealth will grow much faster.

Here’s to our health, wealth, and a great retirement,

Dr. David Eifrig

Further Reading:

While the economy is looking up, Doc says investors are still afraid to buy big banks. “That is exactly why bank stocks are cheap today.” Learn why Doc thinks banks are a great buy… and a simple way to trade them… here.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair