For many, it’s the forgotten variable in accumulating wealth…

For many, it’s the forgotten variable in accumulating wealth…

A good blue-chip stock can bring you thousands of dollars in dividend income every month.

But if you’re blowing money on things you don’t need, you’ll never build substantial wealth… no matter how well your investments are performing.

When it comes to watching your spending, it’s best to focus on big-ticket items like homes, vacations, and furniture. You can also make the mistake of spending unwisely on cars.

Below are two of the costliest mistakes you’ll ever make on your car…

Most people have heard that when you buy a new car, it loses a big chunk of value as soon as you drive it off the lot… But how much?

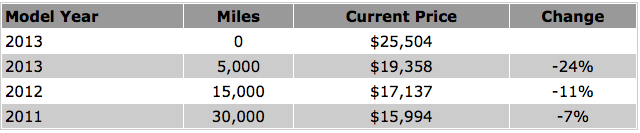

We ran a quick test using my favorite American car – the Ford Taurus. According to the Kelley Blue Book independent vehicle-valuation service, you can still buy a new 2013 Taurus for $25,504.

The “fair price” for a used 2013 Taurus in excellent condition: $19,358. The car drops in value by 24% that first year. Is it worth an extra $6,000 just to be the first to drive this car? Not to me.

You can see how big your savings are going to be from new to used when you look at a few more years in this table below. The table shows the current prices on the following model years and mileages, according to the Kelley Blue Book.

Don’t ever pay extra for the “new-car premium.” The savings of $8,000 every six or seven years over a few decades of car driving adds up to nearly $100,000 extra money in retirement.

The dividends from investing that money over time could allow you to drive a brand-new car and do other things with the extra money in your retirement. But spend it early, and you’re broke in your later years…

Many rental-car companies will pressure you to accept their insurance when you pick up one of their cars… Don’t fall for the hard sell.

The premium adds $10-$30 extra per day. Instead, just pay with a credit card (which is required in most cases anyway)… Many cards offer collision-damage coverage on domestic (and even foreign) car rentals.

Visa, for example, will reimburse your auto-insurance deductible, towing charges, administrative fees, and loss-of-use charges imposed by the rental company.

You just need to do a few things to make sure you’re covered. Most credit-card companies will require you to use the card that offers the coverage to pay the rental in full.

You also have to decline any coverage the rental company provides. Visa, MasterCard, American Express, and Discover all have slightly different policies. And not every card offered by the company has this coverage.

Just call the company’s customer service to determine if you have this coverage, learn the terms, and save hundreds of dollars a year in fees.

Also, it’s likely that much of the coverage you have under your regular car-insurance policy carries over to your rental car. Just call your insurance company to find out what’s covered before you rent next time.

As I mentioned at the start of this essay, making good money with your investments is just one part of accumulating wealth. Smart spending is another. Keep these ideas in mind when spending on cars… and your wealth will grow much faster.

Here’s to our health, wealth, and a great retirement,

Dr. David Eifrig

Further Reading:

While the economy is looking up, Doc says investors are still afraid to buy big banks. “That is exactly why bank stocks are cheap today.” Learn why Doc thinks banks are a great buy… and a simple way to trade them… here.