Gold & Precious Metals

Have mining companies’ stock valuation ever been more undervalued relative to the price of gold? As the $XAU:$GOLD ratio chart below illustrates, the answer is NO!

After cutting costs to the bone in 2013, mining companies in 2014 have resorted to decreased production and shuttering mining operations. As the second chart below illustrates – mining companies, as represented by $XAU, are presently valued at the same level as they were when gold traded as low as between $350 – $500/oz!

Perhaps these “whacked-out” metrics will matter someday, maybe even soon. Maybe even to mining company executives – who apparently are finding it more convenient and cost effective to buy their metal on the open market rather than actually mine it, and who – in response to the ongoing decimation of their industry, as well as their investors’ portfolios – we hear from leadership the collective and thunderous sound of…

…crickets.

About Ruben Varela, Jr.

Ruben is an independent trader specializing in the precious metals sector. Email: rtvarela@yahoo.com. The foregoing is for entertainment and educational purposes only and not investment advice. Please do your own research before investing.

Dear Diary,

Dear Diary,

How do you like that Dow? Down 272 on Tuesday. (Oct 7th) Then back up almost exactly as much on Wednesday.

As we predicted, volatility is rising. Investors are beginning to squirm.

Why?

The Fed is ending QE. And it could hike short-term interest rates as soon as next year. The EZ money is getting scarce.

“We are trapped in a cycle of credit booms,” writes Martin Wolf in the Financial Times.

Wolf is wrong about most things. But he is not wrong about this. “On the whole,” he writes, “there has been no aggregate deleveraging since 2008.”

He does not mention his supporting role in this failure. When the financial world went into a tailspin, caused by too much debt, in 2008, he joined the panic – urging the authorities to take action!

As a faithful and long-suffering reader of the FT, we recall how Wolf howled against “austerity” in all its forms.

His solution to the debt crisis?

Bailouts! Stimulus! Deficits! In short, more debt!

….related: Before You Put a Cent in Stocks Read This

Crashing Oil Prices Portends Unspeakable Horrors

Frankly, we could write entire articles on no less than a dozen “horrible headlines” this morning, including…

- Greek stock and bonds collapsing as a 2015 default appears certain

- The collapsing French government, as Hollande has lost political support

- Plunging German growth estimates

- The growing Italian movement to secede from the Euro monetary system

- Growing support of Catalonian secession

- This morning’s horrifying plunges in U.S. Retail Sales, the Empire State Manufacturing Index and Mortgage Purchase Originations

- Wells Fargo reporting yesterday that mortgage activity has plummeted to 2008 Lehman levels

- The all-out global commodity crash, highlighted in today’s article

- Exploding currency volatility – i.e., the “single most bullish precious metals factor imaginable”

- Unmitigated Western bond yield crash as the “most damning proof yet of QE failure” exposes a collapsing global economy.

- Exploding U.S. debt about to eclipse $17.9 billion due to the “unreported” $100 billion spent on Iraq, Syria and the Ukraine

- Last night’s absurd stock repurchase admission by Intel – likely, marking the painful end of one of QE’s most hideous shareholder-destroying practices. It is estimated that 95% of all 2014 U.S. corporate earnings were plowed into buybacks – often supplemented by new debt – at historically high valuations, whilst average property, plant, and equipment averaged 22 years of age, its oldest level in 60 years.

- A new study purporting the largest “TBTF” banks may require $900 billion of capital to remain solvent

{kind=link}

However, we don’t have time – so suffice to say, this morning’s burgeoning global market crash may well constitute the beginning of what could be a very, very rapid end. The U.S. 10-year yield closed last night at 2.21%; but as I write, is down to an astounding 1.93%, in perhaps its largest daily move ever – en route first to ZERO, and subsequently INFINITY, when the upcomingimminent (yes, I said imminent) announcement of QE’s 4, 5 and 6 emerges. Frankly, if the PPT can’t pull a rabbit out of its hat and “save” the world with unprecedented market manipulation, we think it likely the Fed will not only cancel the “taper” at its October 29th meeting but hint at reversing it entirely.

If we really get a sustained, disinflationary forecast … then I think moving back to additional asset purchases should be something we should seriously consider.

– John Williams, SF Fed President, October 14, 2014

In other words, the “countdown to the Yellen reversal” has commenced”; and if it occurs this Fall, we may well see the long-awaited collapse of the gold Cartel.

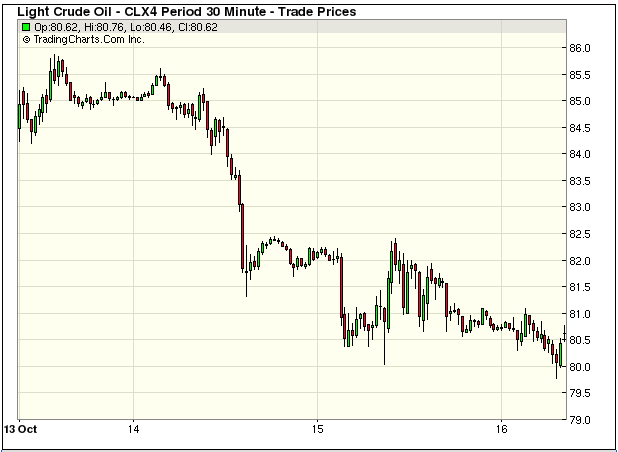

This morning (Oct 15th), WTI crude prices are down another $1+ to $81/bbl., whilst Brent Crude has plunged to $84/bbl. The carnage on energy industry equities is catastrophic, as all energy-related sectors have broken down to multi-year lows, portending a horrific 2008-style crash.

(Chart from 5:20am today)

….continue reading HERE

In an article in the UK’s Telegraph on October 10, veteran economic correspondent Ambrose Evans-Pritchard laid bare the essential truth of the nearly universal current embrace of inflation as an economic panacea. While politicians, CEOs and economists talk about demand stimulus and the avoidance of a deflationary trap, Evans-Pritchard reminds us that inflation is all, and always, about debt management.

In an article in the UK’s Telegraph on October 10, veteran economic correspondent Ambrose Evans-Pritchard laid bare the essential truth of the nearly universal current embrace of inflation as an economic panacea. While politicians, CEOs and economists talk about demand stimulus and the avoidance of a deflationary trap, Evans-Pritchard reminds us that inflation is all, and always, about debt management.

Every year the levels of government debt as a percentage of GDP, for both emerging market and developed economies, continue to go higher and higher. As the ratios push out into uncharted territories, particularly in Europe’s southern tier, the ability to “inflate away” debt through monetization remains the only means available to postpone default. Evans-Pritchard quotes a Bank of America analyst as saying that even “low inflation” (not to mention actual deflation) is the “biggest threat to the dynamics of public debt.” IMF Managing Director Christine Lagarde ramped up the rhetoric further when she recently told the Washington Press Club that “deflation is the ogre that must be fought decisively.” In other words, governments need inflation to remain viable. It’s the drug they just can’t do without.

But as this simple truth is just too embarrassing to admit, politicians and central bankers (and their academic, journalistic, and financial apologists) have concocted a variety of tortured theories as to why inflation is not just good for overly indebted governments, but an essential economic good for all. In a propaganda victory that even Goebbels would envy, it is now widely accepted that purchasing power must decrease for an economy to grow.

Despite centuries of economic evidence to the contrary,they argue that if prices do not rise by at least 2% per year consumers will not spend, business will not hire, and economies will slip into an intractable deflationary death spiral. To prevent this, they recommend governments spend without raising taxes. Not only would such a move involve a direct stimulus by increased government spending, but the money printed by the central bank to finance the deficit will push up prices, which they argue is very healthy for the economy. As the Church Lady used to say, “How convenient.”

Offering voters something for nothing is the Holy Grail of politics. But as a matter of reality, voters should know that a free lunch always comes with a cost. This isn’t even economics, its physics.

When increased government spending is paid for with higher taxes, workers notice that their paychecks have been reduced. This provides clear evidence that government spending comes with a cost. But this bright line is much more difficult to see when the spending is paid for by inflation (printing money). But the net impact on consumers is the same.

Inflation does not reduce the nominal amount of one’s paycheck. But rising prices reduce the amount of goods and services it can buy. So when governments run deficits, workers will be stuck with the bill. Whether they pay though higher taxes or inflation, their standard of living will be diminished. The main difference is that workers know to blame government for higher taxes, which explains why politicians prefer inflation.

To give cover to this tendency, economists have come up with the bizarre concept that falling, or even stable, prices squelch demand and deter consumption. The idea is that if consumers know that something will cost less in the future (even if it’s just 2% less) they will defer their purchases indefinitely, perhaps waiting for the cost of their desired product or service to approach zero. They argue that this can push an economy into a deflationary spiral of falling prices and diminished demand which may be impossible to escape.

But this idea ignores the time value of a product or service (people will tend to pay more for something they can enjoy sooner rather than later) and the economic law that shows how demand goes up as the price falls. But common sense has absolutely nothing to do with the current practice of economics. Instead, the dominant argument is that inflation is needed to seed the economy with demand.

However, this argument is merely a smoke screen. The only thing that inflation can do is to help governments spend. Economies do just fine with low inflation. In fact during the late 19th century, in the Great Sag, the United States experienced sustained deflation while creating much faster economic growth than we have seen in the last few generations. As recently as during the early 1960s the U.S. experienced consistently low inflation (barely 2%) and strong economic growth based on government figures. But in their call for more inflation, modern economists tend to forget or downplay those periods.

But inflation is actually more economically harmful than taxation. By blurring the link between higher government spending and reduced purchasing power, the public is less likely to oppose government expansion. And therein lies the truth. Inflation is not needed to grow economies but to grow governments.

The problem is particularly acute in Europe where countries of radically different fiscal characteristics have been locked into a politically unworkable monetary union. On one side are countries like Italy, Spain, and France whose governments have been notorious for offering generous benefits for which they can’t pay. Before adopting the euro, these countries had currencies that were not known for their bankability. Germany, on the other hand, had built its reputation on balanced budgets and a strong Deutsche Mark. But given the strict monetary restrictions that were needed to grease the skids toward union, the European Central Bank has not been able to create inflation as freely as the U.S. or Japan. As a result, the debt crisis there has been placed in particularly sharp focus, as the problem is perceived to be much larger than in other developed countries that can print at will.

The calls for more inflation in Europe should be raising hackles on the streets of the Continent. But Keynesian economists have provided cover for politicians for years, and true to form, they have again risen to the occasion. While it is understandable that governments are motivated to champion inflation, it is harder to see why professional economists are similarly inspired. Perhaps they believe modern economics has the magic ability to create something from nothing. But the idea that a properly applied macroeconomic formula can somehow circumvent the laws of supply and demand is ludicrous and dangerous.

Of course, the idea that governments can hold inflation to just 2% per annum is preposterous. Once it breaches that level, governments will be powerless to contain it. The endgame will be hyperinflation. That is because escalating levels of debt will prevent them from raising interest rates high enough to break the inflationary spiral. The last time that inflation really got out of hand was back in the early 1980s when a boldly inspired Federal Reserve was able to put the genie back in the bottle by hiking interest rates all the way up to 18%. The economy not only survived that harsh medicine, but it prospered as a result. Does anyone seriously believe that we could survive even a quarter of that dosage today?

Since the central banks are now destined to forever remain behind the inflation curve, it will continue to accelerate until the real threat of hyperinflation looms much larger than did the contrived threat of deflation.

Best Selling author Peter Schiff is the CEO and Chief Global Strategist of Euro Pacific Capital. His podcasts are available on The Peter Schiff Channel on Youtube

![]() Are you thinking about selling? Best to consider these factors and avoid the following traps.

Are you thinking about selling? Best to consider these factors and avoid the following traps.

1. Profit has been maximised: When a property has reached maximum value, there is little value in holding onto it for longer. Therefore this is generally considered the optimum time to sell.

2. Property has not performed: Having cash or equity tied up in an investment that has not performed (over a reasonable time period) can prevent an investor from reaching their financial goals.

3. Better opportunity elsewhere: Investors should know how each of their properties are performing relative to a) others in their portfolio and b) those in the market place. If another opportunity presents itself with greater investment prospects then it should be considered.

4. Depreciation has been maximised: Depreciation on a property lasts for up to 40 years from the time of construction. Over time the value of depreciation recedes. This could weaken a property’s cash-flow position to the degree that it becomes better to sell.

While a forced exit can cause investors to panic and make easily avoidable mistakes, there are a number of traps that any investor wanting to exit a property needs to be aware of, according to experts.

These include:

-Selling too soon – before the market has started moving. This can impact on capital gains and, thus, the profit made.

-Holding for too long until demand has dropped off and the market is going down. This can prolong the sales process and result in a lower price.

-Selling to buy in a rising market, but then sitting on the sidelines. If an investor sells in this scenario, they shouldn’t then neglect to buy a property as intended.

-Forgetting to factor in selling costs (eg: agent commissions, legal costs and the like).

-Cross-collateral implications with lenders: Selling might trigger the need for valuations on other properties in a portfolio. This, in turn, could impact on the value of the portfolio.

….related by Canadian Real Estate Wealth:

Calls for more transparency from CMHC denied

Why you should consider commercial investing?

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair