Timing & trends

Home ownership rates are sinking and demographics are part of the reason. But does that constitute a new housing crisis?

The Wall Street Journal writer Nick Timiraos makes the case in New Housing Crisis Looms as Fewer Renters Can Afford to Own.

Last decade’s housing crisis has given way to a new one in which many families lack the incomes or savings needed to buy homes, creating a surge of renters and a shortage of affordable housing.

The latest crisis looks very different from the subprime mania of the early 2000s, but it does share one

trait: Policy makers in Washington appear either unaware or unwilling to do much about it.

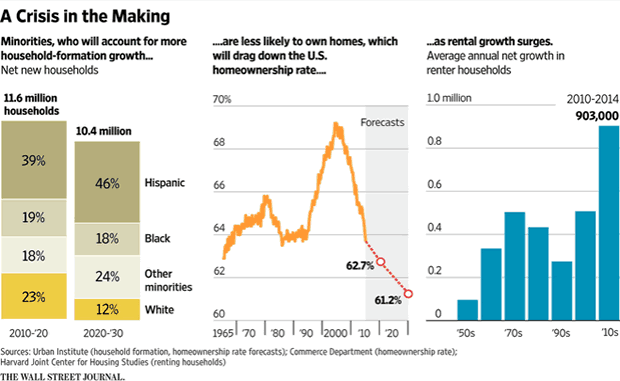

The U.S. homeownership rate is now below where it stood 20 years ago when President Bill Clinton launched a national campaign to encourage more Americans to buy homes. Conventional wisdom says the rate, now at 63.7%, is leveling off to where it was for decades before the housing-market peak.

But this is probably wrong, according to research from the Urban Institute, which predicts homeownership will continue to slip for at least the next 15 years.

Demographics tell the story. The Urban Institute researchers predict that more than 3 in 4 new households this decade, and 7 of 8 in the next, will be formed by minorities. These new households — nearly half of which will be Hispanic — have lower incomes, less wealth and lower homeownership rates than the U.S. average.

The declines reflect a surge of new renter households, which is boosting rents. Together with tougher mortgage-qualification rules, this will leave households stuck between homes they can’t qualify to purchase and rentals they can’t afford, says Ron Terwilliger, who spent two decades running Trammell Crow Residential, one of the nation’s largest apartment developers.

As rental households devote a greater share of their income to rent, families could face greater challenges in saving for a down payment. This could restrain a housing market that has failed to provide any real lift to the economy in the current expansion.

What’s to be done? Given budget pressures, it may not be realistic to expect the government to spend any more money on housing than it already does. Thus, the focus now should be on reallocating what is already committed, says Mr. Terwilliger, a Republican, who this month will formally launch a foundation designed to start these conversations. His goal is legislation after the 2016 election that realigns housing policy with the shifting dynamics.

Breaks for Apartment Builders

Given that Terwilliger spent two decades as one of the nation’s largest apartment developers the answer should be easy to figure out. He wants to end tax breaks for home ownership to subsidize new home owners and “free up funds for the rental side.”

His complaint: 75% of the housing tax breaks go to the top 20% of individuals. That is hardly shocking given the top 20% buy the most expensive homes and therefore pay the most in interest.

Timiraos, buys all Terwilliger’s nonsense hook line and sinker, finishing the WSJ article with “Politically, none of this will be easy . Some will say it’s a zero-sum game — helping renters at the expense of owners. Not so, says Mr. Terwilliger. If renters can’t ever become homeowners, who will buy those homes when today’s homeowners need to sell?”

Housing Crisis Past and Present

The 2015 housing crisis was caused the same way as the one in 2007: Interference by the Fed, by Congress, by local officials wanting to create affordable housing.

Terwilliger wants a combination of affordable housing and affordable renting. Lovely.

Driving up home ownership rates does is guaranteed to do one thing: drive up prices.

Fannhie Mae, Freddie Mac, and hundreds of other government programs culminating with president Bush’s “Ownership Society” all contributed to make housing unaffordable.

The government has no business promoting one form of living over another.

Self-Correcting Problem

Terwilliger ends with the question “If renters can’t ever become homeowners, who will buy those homes when today’s homeowners need to sell?”

The answer should be obvious: Prices will fall until there is a pool of buyers!

In the wake of the great financial crisis, home prices actually fell to the point of being affordable. Few seemed happy with the result. The Fed wanted to prevent deflation and in the greatest financial experiment in history unleashed round after round of QE.

Asset prices recovered, but wages didn’t. As a result, homes are once again unaffordable.

Does Terwilliger want affordable housing or not?

If government and the Fed got out of the way, there would be no problem. Instead, Terwilliger wants the government to “do something”.

I suggest the government and the Fed have done far too much already.

Solution is Undoing

Instead of promoting something, a process that has failed every time, how about undoing everything that contributed to the mess.

My proposal

- Eliminate Fannie Mae

- Eliminate Freddie Mac

- Eliminate the FHA

- Eliminate rent rent controls

- Eliminate itemized deductions and replace with a flat tax

That’s the real solution to the problem, not more self-serving affordable housing nonsense from people with a vested interest in promoting something for their own benefit.

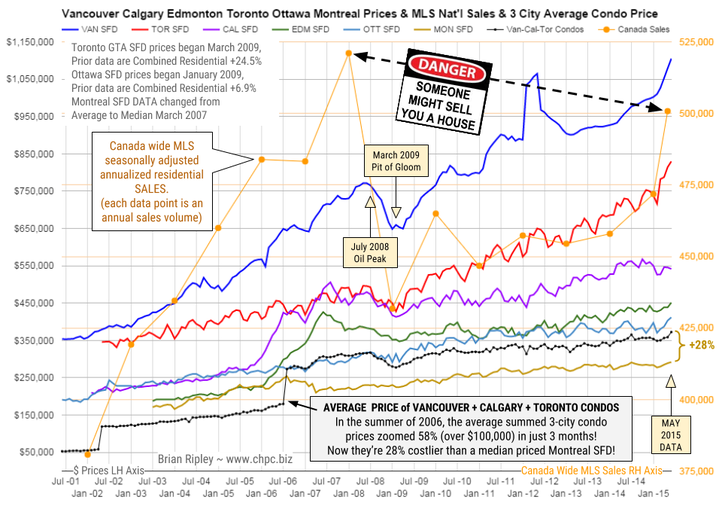

The chart above shows the average detached housing prices for Vancouver, Calgary, Edmonton, Toronto*, Ottawa* and Montréal* (the six Canadian cities with over a million people) as well as the average of the sum of Vancouver, Calgary and Toronto condo (apartment) prices on the left axis. On the right axis is the seasonally adjusted annualized rate (SAAR) of MLS® Residential Sales across Canada.

Check out Brian Ripley’s Plunge-o-meter HERE (The Plunge-O-Meter tracks the dollar and percentage losses from the peak and projects when prices might find support.)

May 2015 Canada’s big city metro SFD prices all caught a bid and only Calgary houses did not set new historic highs. Apparently it’s all about the land that real estate sits on; big money is willing to pay a premium for sitting on it.

Price gains were accomplished on a zoom higher in sales volume of the Canadian national MLS residential annualized housing sales data. Trophy hunters are looking for well located SFD properties in hot markets and the hoi polloi want in before they are priced out.

Can the “posted retail” 5 year fixed rate mortgage low of 4.64% (sub-3% on the street) drive the hunger games into overtime in 2015? Or is the commodity crash signalling an upcoming major correction for Canadian housing? Your opinion is welcome.

Mattress money has gushed into condos with no respect for fundamentals or plan for contingencies that may be required if Pit of Gloom II develops and one must write off capital gains and or rely on employment earnings to subsidize negative yields.

The Money Tsunami Returns!

Martin D. Weiss takes a look at global events and what the effect will be on your investments. What’s going on in places like Mosul, Ramadi, Russia, China and elsewhere really do affect you. Click here to read Martin’s analysis.

Drone Stocks Take Flight

Jon Markman examines the buzz taking place in the drone industry and turns the spotlight on some investments ideas. Click here to read more.

China vs. the United States?

War cycles are spreading globally. Now, tensions are building between two giants — China and the U.S. Where will it all lead? Larry Edelson examines the issue. Read his take on the situation by clicking here.

The Greek Drama

The Greek Drama

Talk about a cliff-hanger ending. In terms of last-minute plot twists and turns, Game of Thrones has got nothing over the ongoing Greek debt drama playing out in Europe. Mike Burnick takes a look at what’s going on. Click here to read more.

Is Inflation Making a Comeback?

Yes, if you know where to look. That’s the view of Mike Larson. Click here to read his outlook and other views on the direction of the economy.

The Week’s Hot News

Money and Markets columnist Mike Larson takes a look at key financial and political events around the globe after the markets close. Here are the week’s highlights:

A Big Week: Greece, Oil, Jobs …

Get Mike’s take on the big events of this past week for the markets. Click here to read his outlook.

A “Let’s Make a Deal” Market

M&A activity is heating up on Wall Street. Is it a bullish indicator or a warning sign for your investments? Mike examines the issue. Read more by clicking here.

Key Levels Loom for Treasuries … What to do

The days of continually falling interest rates appear to be rapidly coming to an end. Treasury prices fell sharply (and yields consequently rose) this past week. What’s going on? Mike takes a look. Click here to read more.

Wondering Why You’re Not Getting Paid More?

Why aren’t you making more money in your job? Click here to find out.

Best wishes,

The Money and Markets Team

Last week we reviewed the gold sector from a big picture perspective. The view was one of an incomplete process that should lead to the next big trend trade beginning on a horizon of multiple months on the short end, up to 1-2 years on the longer end. This week, we excerpt NFTRH 346’s fairly brief Precious Metals segment, which shows a more bearish short-term view.

Precious Metals

From NFTRH 345 with respect to this chart: “If at any time you see gold drift below 1180, please consider having extreme caution if you are a ‘price’ player. If you are a long-term holder like me… as you were, sleep well.”

I am going assume that price players are doing what they need to do in the event this situation worsens.

As we have noted all through the bear market, speculators should not care about whether or not they miss the earliest parts of any new bull market. That is because the next cyclical bull market will be an extended and profitable affair. But in the here and now, there is risk.

Silver lost the short-term trend line noted last week and is now below the 50 day averages as well as the SMA 200. This is non-actionable at best.

HUI has dropped to the key 160 support parameter. That is lateral support as well as ‘higher lows’ (to November, December & March) support. It had better hold or else.

Junior Miners ETF GDXJ dropped out of the uptrend channel noted last week and the exploration ETF (GLDX) continued downward after losing its channel.

Finally, the perspective chart on the Gold Miners (GDM) vs. S&P 500. The time to favor the miners is coming. But if past is a prologue, it could still be up to a year or more before the ratio bottoms. A safe signal would be a moving average trigger as in 2001.

The best investment situation in the gold sector is going to be when gold bottoms vs. stock markets, out performs commodities and comes back into favor amidst a risk ‘OFF’ environment. Don’t let them tell you that strong jobs = inflation = a panic for gold. That is promotion. Risk is still ‘ON’ in the financial markets, so gold is still ‘OFF’.

<end excerpt>

The above is just a small portion of NFTRH 346’s 33 pages, which included additional discussion and context on the precious metals, as well as a comprehensive overview of the the economic backdrop, interest rates (the key to most other markets), US and global stock markets and discussion about individual stocks and favored sectors.

I firmly believe that the gold sector should be kept in view as the next big trend trade, but not obsessed upon (to the exclusion of so many other long and short opportunities across several other asset classes) in the interim.

For consistent, high quality analysis (weekly report and in-week updates on markets and individual equities) that keeps subscribers on the right side of markets, consider an affordable premium subscription to NFTRH.

Forget your typical utility companies and Oreo-peddling consumer staples — these are income plays of a completely different color

With bond yields in the gutter for almost six years now, investors have grown accustomed to looking in … shall we say….. “nonconventional” places for yield.

Whether in odd corners of the stock market or in dodgy-looking private placements, anything offering a respectable current income is bound to get at least a little attention.

It’s easy enough to understand why. The 10-year Treasury yields barely more than 2%, and traditionally high-dividend stocks like utilities and REITs yield less than 4%.

Today, we’re going to take a look at seven high-dividend stocks that fall a little outside the mainstream. Not all of these are dividend stocks that I would necessarily recommend, but all are worth at least keeping on your radar.

After all, it is their quirkiness and lack of inclusion in major benchmark indices that tends to keep them off-limits to large institutional investors … creating the very conditions that make them worth considering for us.

High-Dividend Stocks: StoneMor Partners, LP (STON)

High-Dividend Stocks: StoneMor Partners, LP (STON)

STON Dividend Yield: 8.4%

I’ll start with a stock that is one of my personal favorites … but one that also tends to give a lot of investors the heebie jeebies: publicly traded crypt keeper StoneMor Partners, LP (STON).

StoneMor owns and operates 303 cemeteries and 98 funeral homes across the United States and Puerto Rico, and its business is anything if not predictable.

As none other than the great Benjamin Franklin noted, nothing can be said to be certain but death and taxes. And as the baby boomers — the largest generation in history — enter their golden years, end-of-life services are about to enjoy an unprecedented boom. Based on current life expectancies, the number of annual deaths in America will rise by more than 80% between 2015 and 2035. Even allowing for an increased preference for cremation over traditional burial, an incredible amount of growth is all but guaranteed to come down the pipeline.

And even better, we’re getting paid to wait: StoneMor pays an 8.4% distribution, and it has steadily raised its payout over the past 10 years.

If the unpleasant association with death wasn’t enough, StoneMor has some other quirks that make it difficult for a lot of investors to own: It’s structured as a master limited partnership (“MLP”) and can generate unrelated business taxable income (“UBTI”), which makes it all but untouchable for an IRA or Roth IRA account. Its status as an MLP also makes StoneMor problematic for a lot of institutional investors and non-U.S. persons to own.

Their loss is our gain. StoneMor is a stable company that throws off a high and growing cash distribution. Buy it and plan to own it until … well, until you become one of StoneMor’s permanent residents.

.….read about the next stock HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair