Gold & Precious Metals

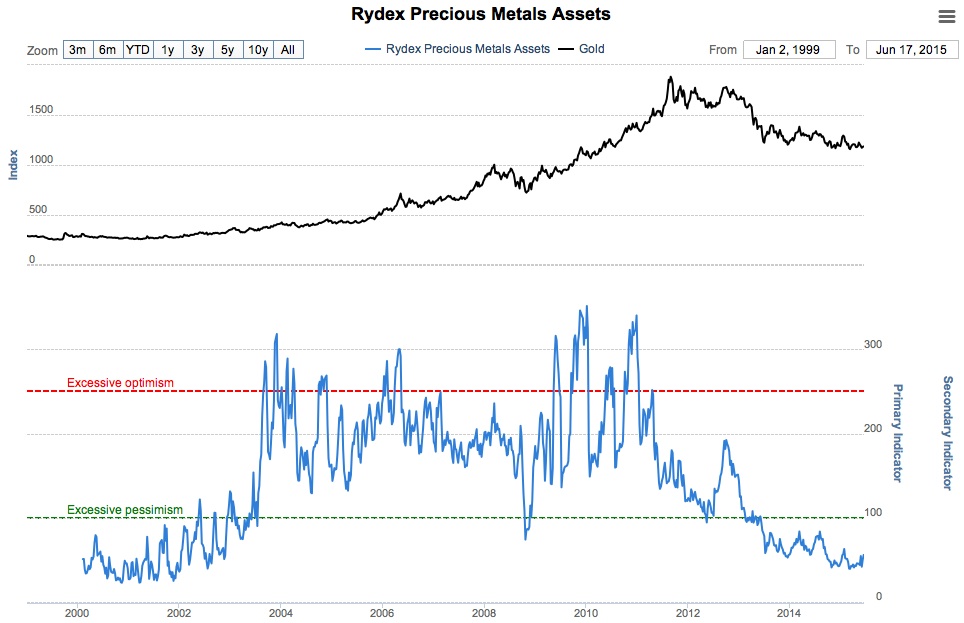

Interestingly, as the public’s confidence has soared when it comes to banks and the overall stock market, commodity hedgers now have one of the more bullish postures based on their overall commodity positions.

….read more of Sentiment Trader’s article HERE

also:

Gold in the Age of Soaring Debt

by Frank Holmes

Ever wonder how much gold has ever been exhumed in the history of the world? The GFMS Gold Surveyestimates that the total amount is approximately 183,600 tonnes, or 5.9 billion ounces. If we take that figure and multiply it by the closing price on June 16, $1,181 per ounce, we find that the value of all gold comes within a nugget’s throw of $7 trillion.

This is an unfathomably large amount, to be sure, yet it pales in comparison to total global debt.

According to management consulting firm McKinsey & Company, the world now sits beneath a mountain of debt worth an astonishing $200 trillion. That’s greater than twice the global GDP, which is currently $75 trillion. If we were to distribute this amount equally to every man, woman and child on the face of the earth, we would each owe around $28,000.

More surprising is that if gold backed total global debt 100 percent, it would be valued at $33,900 per ounce.

Try convincing your gold dealer of this next time you want to sell a coin.

…….read the Rest of the Article HERE

More articles by Frank Holmes

- U.S. Economy Turns on the Afterburners-Is a Rate Hike Next?

- Breaking from the Gold Standard Had Disastrous Consequences

- Billions and Billions Pour into India and China

For the first time in more than 50 years, doctors have found a way to treat this dreadful disease — by using the capabilities of our own immune system.

For the first time in more than 50 years, doctors have found a way to treat this dreadful disease — by using the capabilities of our own immune system.

This technology is called immunotherapy. (I recently told you how the long-awaited revolution in the fight against cancer is here.)

Some of the biggest pharmaceutical companies in the world are pouring tons of cash into this new treatment. And results show these companies are making amazing strides to prolong the lives of patients with some of the worst forms of cancer.

Immunotherapy is one of the biggest early-stage trends in the world. And I shared some of my favorite small-cap stocks that will benefit greatly from this trend.

Today, there is a new generation of immunotherapy. It’s not only curing deadly diseases like cancer — but also preventing patients from catching these diseases in the future.

This “new generation” technology has opened up another huge investment opportunity for investors.

Immunotherapy is one of the biggest trends in healthcare.

In short, this technology trains your body (immune system) to attack just the bad cells … not the good ones. That’s a big difference from current cancer treatments like radiation and chemotherapy, which kill all cells.

This new technology is being used to fight all kinds of diseases — including almost every form of cancer.

And recent test results from this new technology are nothing short of remarkable.

For example, melanoma and pancreatic cancers used to be viewed by doctors as a death sentence. Today, patients can live for years instead of months through different types of immunotherapy treatments.

For the first time in decades — there is now hope for people diagnosed with deadly cancers.

I’ve spent a lot of time researching this subject over the past two years. That’s because my dad passed away from cancer. Plus, my wife is a breast cancer survivor.

And over the past nine months, I’ve recommended several immunotherapy stocks to my subscribers. This includes the dominator in the field (Bristol-Myers) and several small-caps with unique technologies.

Here is how these picks have fared thus far …

* These stock picks were recommended in a previous publication when Frank was an editor at S&A Research. BMY was recommended in the Disruptors & Dominators newsletter, where Frank is the current editor.

The average percentage return from these five picks is 180.6%. And every position has generated positive returns since its recommended date.

I’m not posting these winners to brag. Like most investors, I’ve had my share of losers — including several within the biotech industry.

However, this illustrates how much money you can make by investing early in game-changing technologies.

For immunotherapy, it’s not too late for investors to make money.

This trend is still in its infancy. And as I explained before, there is new technology that’s helping patients with deadly diseases live even longer. This includes stimulating T-cells is ways never seen before. (T-cells are a type of white blood cell that destroys cancerous or infected cells.)

It’s almost like awakening an army inside your body to fight cancer. Not only is this army defeating cancer (by shrinking tumors) — but it’s also preventing these diseases from coming back in the future.

My advice is to start researching immunotherapy companies that have recently come to the market through Initial Public Offerings (IPOs).

This includes names like Aduro BioTech (ADRO) and Adaptimmune Therapeutics (ADAP).These are companies with new immunotherapy platforms.

I don’t suggest buying these stocks right away. They are extremely volatile — and just became public companies.

However, you may want to keep them on your watch list.

If we get an overall market pullback, it could create a great opportunity to get exposure to this secular game-changing trend.

Good investing,

Frank Curzio

One way of grasping the latest tumble in the US dollar is to think of the following:

As expectations of a 2015 Fed hike grew increasingly cemented in the market, traders demanded a higher bar of positive US data performance, especially as macro-normalisation in Europe transitioned into outright progress. Not only most US figures failed to show a sufficient upside surprise since end of April, but business surveys and inflation data from Europe revealed evidence of progress from the ECB’s QE program.

In Jan-Mar, the greenback soared to decade highs against most currencies on the possibility that the Fed would raise interest rates in 2015. In yesterday’s FOMC announcement, the USD sold off due to bigger than expected downgrade in 2015 GDP growth (revised to 1.8-2.0% from 2.3-2.7% in March), as well as lack of clarity with regards to the pace of future Fed hikes.

Although 15 of 17 FOMC officials expect lift-off to begin this year, FX markets require a faster pace of subsequent rate hikes in order for the US dollar to regain the momentum it once had when the possibility of a 2015 rate hike were sufficient for the rally.

The US dollar rally has now reached critical levels on both fundamental and technical grounds.

Fundamentally:

– Bank of England will likely have at least two hawks dissenting against the monetary policy status quo by end of summer due to persistent improvement in jobs and earnings figures, as well as anticipated rise in inflation data.

– Increased probability that Eurozone CPI will overshoot the ECB’s 0.3% y/y projection, with 0.8%-0.9% as the more likely year-end figure — should sway the German-US yield spread further near positive levels from the current -152 bps.

– Increased resistance inside the Bank of Japan’s policy board over stepping up monthly further asset purchases will stand in the way of  further yen weakness, especially if US and European bourses are rattled by the simultaneous threat of disappointing US earnings season and persistent chatter of 2015 Fed lift-off.

further yen weakness, especially if US and European bourses are rattled by the simultaneous threat of disappointing US earnings season and persistent chatter of 2015 Fed lift-off.

Technically, the ensuing Death Cross formation in the US dollar index, and Golden Cross in EURUSD (occurring when key measures of short-term trend exceed longer-term trends) is taking place for the first time since almost exactly 365 days. The developments are backed by important resistance levels in GBPUSD and EURUSD, while USDJPY tests key 122.30 support foundation. (Click Image for Larger Clhart)

FOMC will hold off an interest rate hike until Sept 2015. Markets should bullish for a few months more. Keep your fingers crossed!

The Dow Transports looks to recover. A very nice cycle. Expect a bullish up swing. However dont expect it to be a great up swing with impending interest rate hikes.

The Risk on or off chart suggest that a few more months of strength to the risk on sectors (XLK, XLI, XLY). But note that the down cycle is due, in a few months.

NOTE: readtheticker.com does allow users to load objects and text on charts, however some annotations are by a free third party image tool named Paint.net

Investing Quote…

“Mathematics is the only exact science. All power under heaven and on earth is given to the man who masters the simple science of mathematics.” ~ William D Gann

“Until an hour before the Devil fell, God thought him beautiful in Heaven.” ~ Arthur Miller, “The Crucible” [Contrarian Investing]

“It’s easier to fool people, than to convince them they have been fooled.” ~ Mark Twain

“The minute you get away from the fundamentals – whether it’s proper technique, work ethic, or mental preparation – the bottom can fall out of your game.” ~ Basketball Legend Michael Jordan.

“Investing should be more like watching paint dry or watching grass grow. If you want excitement, take $800 and go to Las Vegas.” ~ Nobel Laureate for Economics Paul Samuelson

Geopolitics Will Trump Economics

Geopolitics Will Trump Economics

Based on the continued failure of the negotiating parties to make any substantive progress in the talks over Greek debt payments, the financial world is tied up in knots over a possible Greek exit from the European Union. The uncertainty has manifested in both high and low finance, with a sharp sell-off in bonds, particularly EU and Greek government debt, and heightened retail withdrawals from Greek banks as depositors become wary of capital controls that would be imposed in the case of an exit. All concerned parties should likely breathe easier. Despite Greece’s almost complete lack of financial integrity, neither NATO nor the EU can afford the political cost of a Greek exit from the EU.

The unacceptable specter lurking behind the EU negotiators is that, if Greece is shown the door by the EU, Russia or even China might step in to provide financing to Greece in return for a strategic foothold in Western Europe and gateway to the Eastern Mediterranean. This is a

fffff possibility that Europe cannot abide. In short, international political ramifications will trump any economic or financial issues.

As reported several months ago in this column, modern Greece has been used continuously by Europe as a bulwark against unwanted incursions. In the 1820s, Greek independence from Ottoman Turkey was financed and supported by Western powers as a way to contain and rollback Turkish influence in the Mediterranean. In the 20th Century, Greece became a key battleground of the Cold War, with the West expending considerable blood and treasure to ultimately keep socialist Greece from falling into the Soviet orbit.

Although the Greeks received countless sums from abroad, Greek governments have been notoriously feckless, and have been instrumental in ensuring their nation’s economic demise. By opting for generous socialist entitlements and blatantly anti-capitalist regulations, Greek governments decided to borrow irresponsibly to meet its obligations.

With the formation of the European Union (EU), strenuous efforts were made to include Greece to prevent the rise of Communism. This encouraged the surreptitious acceptance of untruthful economic statistics to facilitate Greek membership, both of the EU and the Eurozone.

Eurozone membership gave Greece access to vast amounts of cheap debt, offered largely under the false assumption that an early conclusion of a single political union would offer an implied EU guarantee for Greek debt. It was similar to investors assuming, erroneously, that the debt of Freddy Mac and Fannie Mae carried the ‘implied’ guarantee of the U.S. Government.

But, as was the case with Fannie and Freddy (whose collapse many believed would have plunged the U.S. into deep Depression), the political cost of failure was too great to accept. Therefore, the financial costs of technical failure had to be borne by citizens. In addition, over the past few years, much of the Greek debt has been transferred from EU banks to EU governments that have the much abused ability to pass the bad debt onto future generations of their citizens.

Likely aware of this, the Greek government has faced off repeatedly against some of the world’s most powerful politicians and central bankers, winning time and yielding little.

Even more importantly, when Greece’s socialist Prime Minister Alexis Tsipras faces Germany’s Chancellor Angela Merkel, he knows that she is acutely aware that any soft deals offered to Greece may be seen as a precedent encouraging Portugal, Ireland, Italy and Spain to push (even acting as a united block) for similarly favored treatment. Furthermore, any perceived increase in the prospect of a potential break-up of the EU might encourage voters in Great Britain, in the 2017 referendum, to vote to leave a sinking ship. A British exit could put an end to the European dream and place at risk trillions of dollars’ worth of European debt and even the Euro-currency itself.

In addition to these serious concerns, Merkel has one overriding fear. Should talks break down, Greece will likely go searching for other sources of funding. It may find many willing givers, all with strings attached. Russia may offer funding to Greece in return for a naval base. If not Russia, even China might attempt to offer a vast, soft funding rescue package in order to buy entry to the European and NATO landmass. It is no secret that China has a strong interest in taking over operations of the Port of Piraeus, one of the largest ports in the Mediterranean.

While Merkel and her supporting fellow EU leaders may talk tough to Greece’s leaders, they know it is politically unacceptable to allow a financial default to open the way to EU dissolution or the slightest possibility of a Russian or Chinese strategic incursion.

As a result, whatever the eventual financial costs to EU taxpayers of a Greek default, the political costs of a Greek exit are likely to be seen as unacceptable. Therefore, after much posturing, delays and threats, I believe that the chances of an actual Greek exit are far lower than are commonly believed. Most likely the EU will allow a covert Greek default, disguised for the time being by extended repayment schedules, bogus refinancing formulae and possible delayed haircuts as bonds mature. They may insist that such moves are not a technical default. Despite that absurdity, our obedient press corps may even concur with such a characterization, and investors may be so thrilled that a relief rally occurs in stocks and bonds. Extend and pretend will once again be the only acceptable manner to confront our intractable problems.

###

Jun 17, 2015

John Browne

Senior Market Strategist

Euro Pacific Capital, Inc.

1 800-727-7922

email: jbrowne@europac.net

website: www.europac.net

John Browne is the Senior Market Strategist for Euro Pacific Capital, Inc. Mr. Browne is a distinguished former member of Britain’s Parliament who served on the Treasury Select Committee, as Chairman of the Conservative Small Business Committee, and as a close associate of then-Prime Minister Margaret Thatcher. Among his many notable assignments, John served as a principal advisor to Mrs. Thatcher’s government on issues related to the Soviet Union, and was the first to convince Thatcher of the growing stature of then Agriculture Minister Mikhail Gorbachev. As a partial result of Browne’s advocacy, Thatcher famously pronounced that Gorbachev was a man the West “could do business with.” A graduate of the Royal Military Academy Sandhurst, Britain’s version of West Point and retired British army major, John served as a pilot, parachutist, and communications specialist in the elite Grenadiers of the Royal Guard.

John Browne is the Senior Market Strategist for Euro Pacific Capital, Inc. Mr. Browne is a distinguished former member of Britain’s Parliament who served on the Treasury Select Committee, as Chairman of the Conservative Small Business Committee, and as a close associate of then-Prime Minister Margaret Thatcher. Among his many notable assignments, John served as a principal advisor to Mrs. Thatcher’s government on issues related to the Soviet Union, and was the first to convince Thatcher of the growing stature of then Agriculture Minister Mikhail Gorbachev. As a partial result of Browne’s advocacy, Thatcher famously pronounced that Gorbachev was a man the West “could do business with.” A graduate of the Royal Military Academy Sandhurst, Britain’s version of West Point and retired British army major, John served as a pilot, parachutist, and communications specialist in the elite Grenadiers of the Royal Guard.

In addition to careers in British politics and the military, John has a significant background, spanning some 37 years, in finance and business. After graduating from the Harvard Business School, John joined the New York firm of Morgan Stanley & Co as an investment banker. He has also worked with such firms as Barclays Bank and Citigroup. During his career he has served on the boards of numerous banks and international corporations, with a special interest in venture capital. He is a frequent guest on CNBC’s Kudlow & Co. and the former editor of NewsMax Media’s Financial Intelligence Report and Moneynews.com. He holds FINRA series 7 & 63 licenses.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair