Gold & Precious Metals

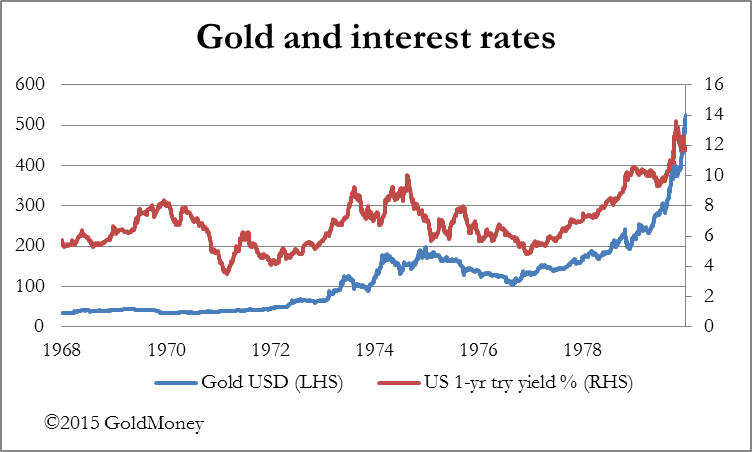

There is a myth prevalent today that the gold price always falls when interest rates rise.

The logic is that when interest rates rise it is more expensive to hold gold, which just sits there not earning anything. And since markets discount future expectations, gold will even fall when a rise in interest rates is expected. With the Fed’s Open Market Committee debating the timing of an interest rate rise to take place possibly in September, it is therefore no surprise to market commentators that the gold price continues its bear market. Only the myth is just that: a myth denied by empirical evidence.

The chart below is of a time when the opposite was demonstrably true. From March 1971 to December 1979 the trends in both interest rates and the gold price rose and fell at the same time. It is worth noting that this occurred over more than one business cycle, so it is not a relationship which was cycle-dependant.

The myth is therefore satisfactorily debunked. To understand why this relationship between interest rates and gold is not as simple as commonly believed, we must take the argument further to bring in commodities generally and visit the tricky subject of Gibson’s Paradox. This paradox is based purely on long-run empirical evidence, when gold was transaction money, covering the two centuries between 1730 and 1930. It observes that the level of wholesale prices and interest rates are positively correlated. It is not the price relationship that is consistent with the quantity theory of money, which presupposes that interest rates correlate to the rate of price inflation instead of the price level itself. This maybe a reason why monetarists mistakenly argue, as we also discovered in the seventies, that central banks can manage the rate of inflation through interest rate policy. The common view in markets today about the relationship between interest rates and price inflation is wholly at odds with the longer-run evidence of Gibson’s Paradox and accords with the more fashionable quantity theory instead.

Gibson and his paradox are generally forgotten today, and those who centrally plan our money and markets appear unaware of the challenge it poses to their monetarist preconceptions. Keynes, no less, described Gibson’s Paradox in 1930 as “one of the most completely established empirical facts in the whole field of quantitative economics”, and Irving Fisher also wrote in 1930 that “no problem in economics has been more hotly debated”. Even Milton Friedman agreed in 1976 that “The Gibson Paradox remains an empirical phenomenon without a theoretical explanation”.*

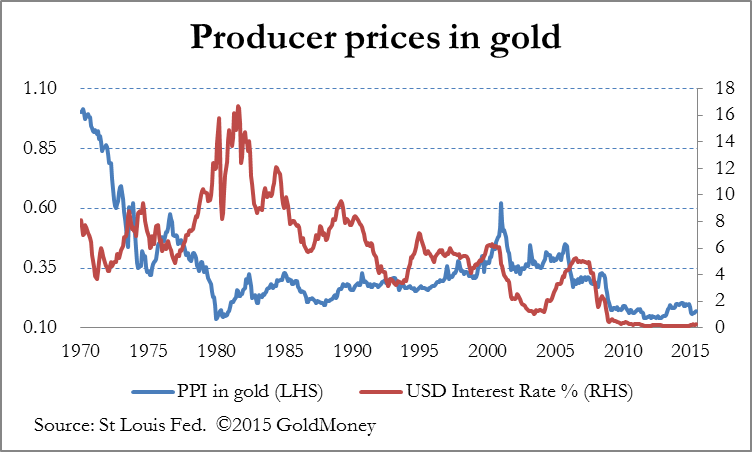

Resolving this paradox can be left to another time; instead we shall consider the implications by looking at price relationships between wholesale prices and interest rates in a post-gold world. The next chart is of producer prices measured in gold compared with one-year Treasury yields.

I have taken the St Louis Fed’s “Producer Price Index by Commodity for Crude Materials for Further Processing” to more closely reflect commodity price trends, and to reduce the additional considerations of changes in processing margins over time. The one-year interest rate is preferred to the original evidence of Gibson’s Paradox, which used the yield on undated British Government Consols stock as being the only continual information on rates available, because we need to more firmly link the evidence to modern interest rate policies.

Looking at the chart, it is hardly surprising that Gibson’s Paradox was quashed from the time of the Nixon Shock in 1971, when the US unlocked a huge rise in the gold price by ending the Bretton Woods Agreement. Instead, the gold price took on a life of its own, driving down wholesale prices priced in gold for the next nine years. The rise in the index from 1980 to 2000 reflected gold’s subsequent bear market when gold fell from $800 to $250, but the influence of Gibson’s Paradox appears to have returned thereafter.

This conclusion might be considered suspect; but the chart tells us that not only are producer prices at their lowest for thirty-five years when measured in sound money, the price level also coincides with zero interest rates. In theory, it accords precisely with Gibson’s Paradox. So where do we go from here?

There is only one way for interest rates to go from the zero bound, it being only a matter of time, time which according to the Fed is now running out. Commodity prices in their role as raw materials therefore seem set to rise with interest rates, if the Paradox is still valid. Furthermore, the evidence from this analysis suggests that wholesale prices are suppressed even more than the price of gold. This being the case, when the interest rate cycle turns the potential for higher raw material prices measured in dollars could be truly spectacular, even more so in the event the gold price rises at the same time, which seems likely in the event that financial markets become destabilised by higher interest rates.

It is worth repeating at this point that the economic consensus, which adheres to the quantity theory of money and has been comforted by the apparent absence of consumer price inflation in the wake of the post-Lehman monetary expansion, takes a diametrically opposite view to that indicated by the Paradox. The prospect of a turn in the interest rate cycle is expected to drive the dollar’s exchange rate higher still, weakening commodity prices and gold even further. In the language of the dealers, everyone is on the same side of the trade, meaning the dollar is technically over-bought and commodities over-sold.

Gibson’s Paradox says it will turn out otherwise, and it could be central to linking the cyclical relationship between interest rates, securities markets, and commodity prices. It becomes much easier to see how these relationships tie together. Rising interest rates would almost certainly be accompanied by a potentially large fall in overpriced bond and stock markets as speculative positions are unwound, the former even undermining bank solvency ratios.

The flight of speculative capital from falling markets has to go somewhere, particularly if cash balances held in the banks are at a growing risk from systemic default. The Paradox tells us that these are the conditions for commodities to become the safe haven of choice for the highest levels of speculative money ever recorded since fiat currencies dispensed with their golden anchor. Ergo, Gibson’s Paradox probably still holds.

*All three quotes are taken from Barsky & Summers, National Bureau of Economic Research Working Paper No. 1680, (August 1985).

The views and opinions expressed in the article are those of the author and do not necessarily reflect those of GoldMoney, unless expressly stated. Please note that neither GoldMoney nor any of its representatives provide financial, legal, tax, investment or other advice. Such advice should be sought form an independent regulated person or body who is suitably qualified to do so. Any information provided in this article is provided solely as general market commentary and does not constitute advice. GoldMoney will not accept liability for any loss or damage, which may arise directly or indirectly from your use of or reliance on such information.

Stock Trading Alert originally published on July 23, 2015, 6:55 AM:

Briefly: In our opinion, speculative short positions are favored (with stop-loss at 2,140, and profit target at 1,980, S&P 500 index)

Our intraday outlook is bearish, and our short-term outlook is bearish:

Intraday outlook (next 24 hours): bearish

Short-term outlook (next 1-2 weeks): bearish

Medium-term outlook (next 1-3 months): neutral

Long-term outlook (next year): bullish

The main U.S. stock market indexes lost 0.4-1.1% on Wednesday, as investors reacted to quarterly earnings releases, economic data announcements. The S&P 500 index remains relatively close to its late May all-time high of 2,134.72. The nearest important level of resistance is at around 2,130-2,135. On the other hand, support level is at 2,100. There have been no confirmed negative signals so far, however, we can see negative technical divergences:

Expectations before the opening of today’s trading session are slightly positive, with index futures currently up 0.1-0.2%. The European stock market indexes have gained 0.1-0.2% so far. Investors will now wait for some economic data announcements: Initial Claims at 8:30 a.m., Leading Indicators at 10:00 a.m. The S&P 500 futures contract (CFD) trades within an intraday consolidation, following yesterday’s rebound. The nearest important level of support is at around 2,100, as the 15-minute chart shows:

The technology Nasdaq 100 futures contract (CFD) trades along the level of 4,630. The nearest important level of resistance is at around 4,635, and support level is at 4,580-4,600, as we can see on the 15-minute chart:

Concluding, the broad stock market retraced some of its recent rally yesterday, as investors reacted to quarterly earnings releases. There have been no confirmed negative signals so far. However, we continue to maintain our speculative short position (2,098.27, S&P 500 index), as we expect a medium-term downward correction or an uptrend reversal. Stop-loss is at 2,140, and potential profit target is at 1,980. You can trade S&P 500 index using futures contracts (S&P 500 futures contract – SP, E-mini S&P 500 futures contract – ES) or an ETF like the SPDR S&P 500 ETF – SPY. It is always important to set some exit price level in case some events cause the price to move in the unlikely direction. Having safety measures in place helps limit potential losses while letting the gains grow.

Thank you.

In his July 17th Blog, Let’s Get Real About Gold, author and Wall Street Journal columnist Jason Zweig likened investor interest in gold with the “Pet Rock” craze of the 1970’s, when consumers became convinced that a rock in a box would provide continuous companionship, elevate their social standing, and give them something hip to talk about at parties. Zweig asserts that investor faith in gold, which he argues is just another inert mineral with good marketing, is similarly irrational, and has kept people from putting money in the much more lucrative stock market.

In his July 17th Blog, Let’s Get Real About Gold, author and Wall Street Journal columnist Jason Zweig likened investor interest in gold with the “Pet Rock” craze of the 1970’s, when consumers became convinced that a rock in a box would provide continuous companionship, elevate their social standing, and give them something hip to talk about at parties. Zweig asserts that investor faith in gold, which he argues is just another inert mineral with good marketing, is similarly irrational, and has kept people from putting money in the much more lucrative stock market.

First off, Zweig’s comparison of gold to equities as an investment vehicle sets up a false dichotomy. Gold is not an investment. It is, as Zweig indicates, nothing but a rock. But it is a rock that is extremely scarce, with highly desirable physical properties that have resulted in its being used as money for all of recorded human history. As a result, it should not be compared to stocks or real estate, but to other forms of money, such as any one of a number of fiat currencies now in circulation. Ironically, in a world awash in fiat currencies that are created at an ever increasing pace, and whose value is solely derived from faith in the issuing state, gold is the only form of money whose value does not require a leap of faith.

I have no emotional attachment to gold. I don’t use it to cover my walls, I don’t run my fingers through it and laugh, I don’t ask my wife to paint herself with it. What I do know is that before the world moved to a fiat monetary system in the latter half of the 20th Century, gold had become the money of choice for nearly every major culture in every age. This supremacy was based on gold’s scarcity, its versatility as a metal, its unique and useful properties, its beauty, and its wide cultural acceptance as a hallmark of love, permanence, wealth and success. There can be little doubt that people will always be willing to desire and accumulate gold…for any of a variety of reasons. The only question is how much they will be willing to pay. On that point, reasonable minds can differ. But to imply that gold has no more intrinsic value than a pet rock, is to recklessly ignore reality.

Up until 1971, the U.S. dollar was backed by the faith that the government would redeem its notes in gold. But, since then, that faith has been replaced by a simpler faith that others will always accept U.S. dollars in exchange for goods and services of real value. The transformation put the U.S. dollar in the same basket as all the other fiat currencies in the world whose value stems from the faith in the issuing government. In his piece, Zweigseems to assume that holding currencies is not an act of faith. But clearly this too involves a question of degree.

Most investors would certainly prefer gold to Argentine Pesos, Ghanaian Cedis, or Venezuelan Bolivars. In reality, what Zweig is saying is that good fiat currencies (the U.S. dollar being the gold standard of fiat currencies) require no faith to buy and hold. But why is that?

But the dollar’s strength is supposed to derive from faith that the U.S. government will remain fiscally sound. There is little evidence that this will be the case. All of the traditional factors that determine a currency’s value, i.e. trade balances, interest rates, government debt levels, economic growth, etc. should be putting downward pressure on the dollar. The U.S. government has done nothing to solve the nation’s long-term debt crisis. Even the Congressional Budget Office admits that the Federal deficit will increase by an average of $35 billion annually until the end of the decade. By 2025, Trillion dollar plus deficits become entrenched (and those projections are based on economic growth assumptions that currently have proven to be far too optimistic.)

Despite all this, the dollar has surged close to a 10-year high, based on the Bloomberg Dollar Spot Index. Wall Street has explained the dominance by pointing to troubles in Europe and Asia, saying that the dollar has its problems, but it is the “cleanest dirty shirt in the hamper.” Analysts pointed to the expected higher interest rates from the Fed that would under-gird demand for the dollar as other central banks around the world were lowering rates. But that outcome has yet to materialize.

At the end of 2014 most investors had assumed that the Fed would begin raising rates in the First Quarter of 2015. But disappointing economic growth has led the Fed to continuously delay lift off. Nevertheless, investors still think that the hikes are just around the corner. In reaching this conclusion, they blindly accept that our economy can survive higher rates when all the objective evidence leads to the conclusion that it can’t.

In reality, faith in the dollar is based solely on the belief that the U.S. dominance of the global economy will continue indefinitely, no matter how deeply we go into debt, how low our interest rates remain, and how unbalanced our trade becomes.

We have seen this movie before. When confidence in the infallibility of central bankers is high, mainstream voices tend to cast aside gold and put their faith in the judgment of man. In 1999, New York Times columnist Floyd Norris penned an article entitled, “Who Needs Gold When We Have Alan Greenspan?” Despite Norris’ dismissal, the real answer to that question was “everyone”. In the following 12 years, at its high, gold rallied 650%.

From my perspective, the markets are now placing more misplaced faith in the wisdom of Janet Yellen than they had in Greenspan. As a result, gold is being shunned as it was back in 1999. Alan Greenspan’s penchant for easing monetary policy to prop up financial markets led to the creation of two dangerous bubbles, the first in stocks in 2000, and then in real estate, which finally burst in 2007, leading to the Great Recession. Given that the easing of monetary policy made by Greenspan’s successors has been much larger, one can only imagine what may be the enormity of an economic disaster that looms on the horizon.

So yes, in a way my investment decisions are based on faith, but not the same type of faith that the Wall Street Journal assumes. My faith is that governments and central banks will continue to run up debt and debase currencies until a crisis brings the whole experiment to a disastrous conclusion. There is simply no historical precedent to reach any other conclusion. I also have faith that human beings will always prefer a piece of gold to a stack of paper. Separate a paper currency from its perceived value and you just have a stack of paper and ink. However, if they would just print it on softer and absorbent stock and put it on rolls, it might have some intrinsic value if we run out of toilet paper.

Read the original article at Euro Pacific Capital.

Best Selling author Peter Schiff is the CEO and Chief Global Strategist of Euro Pacific Capital. His podcasts are available on The Peter Schiff Channel on Youtube

It’s approaching that time of year when traders and central bankers alike depart for long holidays. But this summer is shaping up to be anything but quiet for markets, with betting on a “Greek Exit” from the Euro roiling markets, and Red-chip stocks in China nose diving and requiring unprecedented “Plunge Protection Team” intervention in order to halt the onslaught. After a few weeks of turmoil, the Greek debt crisis has been kicked down the road for another few years, with another EU bailout, and after the Shanghai red-chip index, staged a +10% rebound from its panic bottom lows hit on July 7th, traders now regard these sideshows as “fixed” and under the control of their central planners. With these worries can be put on the back burner for now, it’s back to business as usual, – that is to say,back toinvesting in heavily manipulated markets, in which extreme emergency policies, such as NIRP, ZIRP, and QE have distorted the pricing of virtually all assets, and where your local central bank has your back.

However, with the Federal Reserve poised to hike short-term interest rates for the first time in nearly a decade, “The actual raising of policy rates could trigger further bouts of volatility, but my best estimate is that the normalization of our policy should prove manageable,” said the Fed’s “Shadow” chief Stanley on May 26th. Fischer gave no time frame for when the Fed will start its first tightening cycle since 2004-06, but he made it clear that higher rates are coming. Still, he warns, communications can be a “tricky business,” and when the Fed does tighten, policymakers are bracing for spillovers to financial markets both at home and abroad. “Some of the world’s more vulnerable economies may find the road to normalization somewhat bumpier,” he added.

The key question hanging over the markets, in general, is whether the Federal Reserve and its Anglo sidekick, the Bank of England <BoE>, will finally begin to hike their short-term interest rates in the months ahead. On June 28th, the Bank for International Settlements, <BIS>, based in Basel, Switzerland, which is an adviser for global central banks, called on the world’s top central banks to start normalizing monetary policy, – either by raising interest rates, or shutting down the printing presses under the guise of “Quantitative Easing,” <QE>, and the sooner the better.

“By keeping rates anchored at these historic, ultra-low levels threatens to inflict serious damage on the financial system and exacerbate market volatility, as well as limiting policymakers’ response to the next recession when it comes,” the BIS warned. “Risk-taking in financial markets has gone on for too long. And the illusion that markets will remain highly liquid has been too pervasive. The likelihood of turbulence will increase further if current extraordinary conditions are spun out. The more one stretches an elastic band, the more violently it snaps back,” (like the recent experience in the Chinese stock markets), warned Claudio Borio, head of the BIS’s Monetary and EconomicDepartment.

“Cheap money encourages more debt and creates financial booms and busts that leave lasting scars on the economy. They underpin both the potentially harmful high risk-taking in financial markets, while subduing risk-taking in the real economy, where investment is badly needed. And while increases in interest rates could cause stock prices to fall, – the likelihood of turmoil is only increased by waiting,” the BIS warned. It advises that monetary policy should be normalized with a firm and steady hand. “Near-zero interest rates could become chronic in the world’s major economies unless “a firm hand is used to raise them back to more normal levels.” “More weight should now be attached to the risks of normalizing too late, and too gradually,” the BIS warned. “Restoring more normal conditions will also be essential for facing the next recession, which will no doubt materialize at some point. Of what use is a gun with no bullets left?” the BIS report said.

However, the BIS has routinely made such dire warnings over the past few years, and the major central banks have routinely ignored them. In fact, the Bank of Japan <BoJ> and the European Central Bank <ECB>, are engaged in a full blown currency war over the fate of the Euro /yen exchange rate. Both central banks are printing about $70-billion worth of Euros and yen, and flooding the markets with ultra-cheap liquidity, that is keeping long-term bond yields artificially low, and stock markets artificially high. Neither the BoJ nor the ECB have any plan to roll back the QE-liquidity injections, anytime soon.

US$ wins the Reverse beauty Contest; Moreover, the monetary policies of the big-4 central banks will soon be moving further out of sync. The Fed began to taper its $80-billion per month QE-3 injections back in January 2014, and finally mothballed it on October 31st, 2014. The Bank of England spent £375-billion on purchasing British Gilts and mothballed its QE-injections in Nov 12. And according to recent leaks to the media, both the BoE and the Fed are preparing to follow the advice of the BIS, and will be the first of the G-7 central banks to hike their short term interest rates, in the months ahead.

On the other hand, the global markets will be swimming in a sea of liquidity, as the Bank of Japan <BoJ> and the European Central Bank….continue reading HERE

Few people believed me when I repeatedly warned that gold was still in a bear market and had not yet bottomed.

Few people believed me when I repeatedly warned that gold was still in a bear market and had not yet bottomed.

They said European Central Bank (ECB) money printing would surely light a fuse under gold and propel it higher.

They said the rising tides of terrorism and war around the world would surely send it higher.

They said inflation would come roaring back, and gold would soar.

They even claimed China was aggressively accumulating massive amounts of gold, cornering the market to make its currency, the yuan, the strongest in the world.

Some even said it will soon be known to all that our own Fort Knox doesn’t really have any gold and that our government got rid of it all years ago.

While others claimed the dollar was going to crash, and hence, gold would shoot the moon.

To each and every one of these and more stories and conspiracy theories I said, “BALONEY.”

They are all merely theories put out there by analysts who either don’t have a clue what they are talking about, or have gross conflicts of interest, pretend analysts who are really gold dealers in disguise.

Instead, I said, the main facts are these …

A. The world is awash in deflation and cash is king. You’ll be hard pressed to find inflation anywhere. And certainly not in the two biggest economies in the world, Europe and the United States.

Moreover, as I have said all along, hair-brained policies enacted by inept politicians in Europe and the United States have sent money largely into hoarding cash, which by default is bullish for the U.S. dollar and deflation, and bearish for most asset prices.

True, some money is going into alternative assets like diamonds, artwork and jewelry — but that’s big savvy money that largely wants to get off the grid.

After all, you can hop on a plane with $10 million worth of jewelry or even a Picasso, but try doing that with gold bars or coins and you’ll likely have it confiscated and possibly even end up in jail.

B. $10 trillion of money printing can’t do anything when global debts are as high as $500 trillion. How can $10 trillion of printed money by the world’s central banks possibly make a dent in the global debt monster of nearly $500 trillion of official and unofficial government debt?!

It can’t. Which is why all the money printing has done absolutely nothing to prevent deflation from taking hold.

C. Terrorism and war will not be immediately bullish for gold. One day — in the not-too-distant future — the majority of investors will wake up and smell the coffee: That Western governments of the world are going broke, and as a distraction, are engaging in policies that provoke both civil and international unrest and even war.

When that time comes, then gold will start to explode higher, with or without inflation. But for now, the majority of investors don’t know what’s going on.

So with almost every bounce in gold, they buy more. And then they get chewed up and spit out as gold plummets still lower.

This is a necessary process in the bottoming of any market, not just gold. The majority of investors cling to the wrong side of the market, almost all the way down.

D. China is not looking to corner the gold market. I’ve said this before and I’ll say it again until I’m blue in the face.

A gold standard, in any currency, is ultimately contractionary and deflationary. It has never once worked, despite what anyone tells you.

It can’t work. Why? Because authorities in charge of setting the official exchange rate between gold and paper money can change it at will. And because it subjects an economy to the nuances of new supplies of gold, or the lack thereof.

If China were to impose a gold standard, its economy would implode. It’s that simple and Beijing knows it.

Moreover, as I have also stated many times before …

Moreover, as I have also stated many times before …

1. China has never had a gold standard. Not once in its 5,000 year history.

2. China invented paper money. During the Tang dynasty (618-907). Known as “flying cash” that was backed by copper-based hard money, the paper notes were soon replaced by paper money with bank seals.

China’s paper money invention traveled westward with the Mongols, and by 1661, Marco Polo brought the paper money concept to Europe.

E. Western central banks have zero interest in gold. They too have no interest in a gold standard. Period.

In addition, as I have also stated before, many Western central banks will end up selling gold. Why? Two simple reasons:

1. Many are flat broke and need the cash. Greece will be among the first to dump gold (or be forced to). Portugal, Spain, even Italy and France will ultimately sell gold. As will other bankrupt European countries.

2. Neither the ECB or our own Federal Reserve want gold to be a part of today’s monetary system. They don’t even want paper money to be a part of it.

Instead, they are actively pursuing electronic currencies — so they can track and tax you and even shut down the banking system at the press of a button.

So what’s next for gold? How low can

it go before it finally bottoms?

Subscribers to my Real Wealth Report and my premium trading services have my more specific targets, as they should.

So all I can tell you right now is …

A. Gold will likely soon bounce higher. That in turn will get many analysts and investors excited, proclaiming the bottom is in. But …

B. Once that bounce is over, gold will cascade lower to well below $1,000 before bottoming.

So don’t be fooled. Gold will go still lower. And so will silver, platinum and palladium.

If you own inverse ETFs on any of the precious metals that I have suggested in the past, hold them. I’ll let you know when precious metals have bottomed so you can grab your profits.

Best wishes, as always …

Larry Edelson

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair