Energy & Commodities

![]() Recently, I wrote on these pages that a remarkable turnaround was taking place in the President’s fortunes. It’s an impressive display of rising from the depths of falling popularity last fall, and it is starting to be felt in many areas, with major impacts on the future of energy.

Recently, I wrote on these pages that a remarkable turnaround was taking place in the President’s fortunes. It’s an impressive display of rising from the depths of falling popularity last fall, and it is starting to be felt in many areas, with major impacts on the future of energy.

At his lowest point, the U.S. President was widely regarded as a lame duck, shedding influence and power, and on a down-hill slide.

This was followed by a number of embarrassments, with one of the worst coming from Russia, when it chose to provide sanctuary to Edward Snowden who revealed that the U.S. was hacking the strategic communications of its closest allies.

More damaging, the revelation came at the worst possible time for the U.S., seriously discrediting its campaign to enlist allies against alleged Russian and Chinese hackers.

This was followed by another embarrassment where the U.S. utterly failed to prevent U.S. allies from joining the Chinese-sponsored Asian infrastructure bank. It seemed that the doomsayers were proving correct about America’s decline and fall.

Since then, Obama has been on a roll, with victories in Congressional trade agreements and at the Supreme Court with decisions that removed legal and constitutional challenges to the President’s health program, and gay marriage.

Following hot upon these achievements were the successful negotiations with Cuba and Iran, that went far beyond expectation, climaxing with the signing of the historic Iran nuclear agreement.

Even more surprising was the President’s ability to marginalize the powerful lobbies and opponents of these agreements, including hard-liners in the U.S., Iran, Israel, and the Gulf Kingdoms.

Not Your Father’s Sanctions

In the past, the effectiveness of sanctions was often questioned because of the difficulty of tracking compliance. The result was that targeted countries easily hid and continued banned activities. The sanctions golden rule: if you can’t track them, you can’t enforce them.

But current sanctions are nothing like they were in the past. The difference is that technology has lifted surveillance to unprecedented levels. What with spy satellites, drones, and sophisticated listening devices, the U.S. now has the capacity to pierce nearly every form of communication and transaction. That is the secret weapon which enables the west to impose iron bound constraints that can level just about any economy.

Whether the participants in the recent negotiations will comply with the terms of their agreements, only the future can tell. But there’s little question that none would have come to the table without the sanctions.

Recall also that only first stage sanctions had been imposed on Cuba, Iran, and Russia, with each nation clearly warned that far worse lay in store if targeted activities continued.

The message was hardly lost on the ever pragmatic President Putin, who despite brave words of resistance, suddenly saw that it was to his country’s benefit to cooperate with the U.S. and its allies, particularly in the Iranian nuclear negotiations, and the ongoing war in Syria and Iraq.

Nor was the message lost on China either, who also suddenly found it in their interest to stop island building in the South China Sea, and began negotiations with its neighbors over territorial claims, as urged by the U.S. and its allies in the region. China ‘acting poor’ when Russia recently came calling for financial help also smacked of western influence.

Contrary to their rhetoric, Iran and Russia were deeply chastened by sanctions, even more so by the oil price collapse, and have agreed to major concessions. It’s no accident that both countries are also becoming ever more important in the world’s anti-terrorism campaign, an effort clearly being coordinated with the U.S.

OPEC Support

Playing into Obama’s hand was a different sort of victory taking place during the same period. That was the Saudis leading OPEC to defend their traditional market share by flooding the oil markets.

The ensuing trade war against competitors has caused every other major oil producing country and oil companies to cut future development plans. Importantly, the oil glut reinforced the damaging effects of sanctions on targeted countries.

Some conspiracy theorists have claimed that the U.S. Administration conspired with the Saudi King to create an oil glut by over-producing, directly aimed at crashing the Russian economy, where energy accounts for nearly 50 percent of its budget.

U.S. Investment Bank, Morgan Stanley recently reported that the Saudi’s were over-producing by some 1.5 million barrels per day in a market with a surplus of around 800,000 barrels per day.

The Bank added that the oil markets’ fall could be worse and last longer than the one created 1986, in which Saudi Arabia grew tired of shouldering the burden of production cuts and decided to flood the market in an effort to pursue market share.

With Iran expected to return to markets, thereby adding to the glut, the bank also stated that these current moves made the risk in oil markets “historically unanalyzable,” a red alert to the investment community.

Oil Glut Ricochet

The Saudis enthusiastically took up the opportunity to lower global energy prices, ostensibly claiming they were not aiming to kill off rivals in Russia or the U.S., but merely that they were not the highest cost producer.

There were also other unexpected reversals. It has been widely reported that the Gulf Kingdoms are outraged over the U.S. drawing closer to Iran, as well as the U.S. distancing itself from the wars in the Middle East. Evidence for this view can be found in the Saudis’ multi-billion dollar deals with the Russia, which fly in the face of U.S./EU sanctions.

The clincher in the Russian-Saudi entente may just have occurred with the sudden ISIS terrorist attacks in Saudi Arabia.

The Saudis are all too aware of the threat that ISIS presents, the monster that some claim they created, and are now badly in need of military assistance, especially with the U.S. declining full scale military engagement in the region.

The Glut’s Toll

The result of the ensuing glut is a fast declining industry that is now willingly accepting new production cutbacks, while oil producing countries like Russia, Canada and Australia, are edging dangerously close to recession, with their currencies hitting six year lows.

As reported by CNBC, global job losses in the oil industry have reached over 141,200, with severe ripple effects across supporting industries. The U.S. is by no means immune to the downtrend, where current lay-offs in the energy field are approaching 71,000, and expected to climb.

U.S. Strategy for the Middle East

If, as it seems, Obama is back on top as a world leader, it’s important to understand his overall strategy and the likelihood of success.

The consensus amongst energy mavens is that if the Iran nuclear deal eventually leads to a withdrawal of sanctions, the results will be increased Iranian supplies, forcing prices lower by some $10 per barrel, according to World Bank estimates.

But Iran’s nuclear deal is about much more than the price per gallon. What the U.S. and its allies are trying to accomplish is no less than the reversal of political hostilities that have marginalized Iran for over thirty years and fueled hostility across the region.

As the President recently stated, the nuclear agreement is also meant to restore Iran as a regional leader in the Mid-East and turn a hostile relationship into at least a neutral one. That could go a long way in changing the political structure of the Middle East, while reducing the West’s dependency on its traditional allies in the region.

That’s not to say that the U.S. and Iran are destined to become close allies, but to recognize that they have important shared interests in combatting radical Islam that could lead to far greater cooperation.

There are some who claim that despite denials, the U.S. and Iran are already cooperating in the West’s battle against ISIS in Iraq and Syria. If so, that could go far in supporting Obama’s goal to pivot from the Middle East and towards Asia.

As stated here, another overriding U.S. goal is to prevent Iran’s drift eastward into a commercial and military alliance with Russia and China, as a partner in the recently formed Shanghai Cooperation Organization, the Eurasian Economic Union, and Silk Road project. Instead, the U.S. wants Iran positioned as a competitor to Russia for EU and Asian energy markets, and as a bulwark against Russian and Chinese expansion.

The problem for the administration is that hard-liners at home and abroad, having failed to kill the deal, are continuing their efforts to stop any broader entente emerging between the Iran, its neighbors, and the world.

Here, the road is likely to be far less smooth for Obama. Unlike the nuclear deal that was undertaken under the banner of a UN resolution, any further U.S. political deals with Iran would be subject to congressional approval, something few experts view as forthcoming.

What with these formidable barriers to entente, a continuing drift eastward by Iran towards a closer commercial and military relationship with Russia and China remains a strong possibility.

But I think that the nearly two years of nuclear negotiations with Iran, if it accomplished nothing else, restored Iran to the position of a recognized regional power.

Iran is also unlikely to forget that both China and Russia voted in the UN to support sanctions against Iran. Nor is the fact likely to be ignored that Russia also declined to breach sanctions to deliver a previously contracted system of advanced missile defense systems to its erstwhile ally. Russia’s sudden close relationship with the Saudis is also not likely to sit well in Tehran.

For Iran, an over-riding goal in the deal was the repeal of sanctions, enabling the country to regain its former status as OPEC’s third largest producer. With that goal more realistic in light of a successful conclusion of the recent negotiations, Iran is unlikely to adopt policies to antagonize its newfound partners.

Instead of becoming captive to either Russia or China, Iran is far more likely to promote itself as an anti-terror partner with both west and east, while building investment markets with both sides of the ‘great game’ for its own benefit.

At the same time, Iran is leading the movement to form a united front against terrorism, partnering with the U.S., the Gulf Kingdoms, Turkey, Russia, and Syria.

Conclusion

In a region often beset by conflicts, with hardliners at home and abroad working against it, the odds are high against the success of the American strategy and the Iran deal.

Israel’s Prime Minister Netanyahu has turned the deal into a partisan issue in the midst of a presidential election campaign, in which it will undoubtedly play a major part.

Leading U.S. Democrat Congressmen have gone rogue against their administration, voicing opposition to the deal. Advocates on both sides are now raising the specter of war as the sure results of their opponents’ plans. Can pictures of mushroom clouds be far behind?

Arrayed against the deal opponents are the powerful interests of the international business community, now impatiently chomping at the bit to get into Iran’s virtually untapped market.

Nearly every major western country has recently sent trade missions to Iran in anticipation of sanctions being lifted. Representatives included major international oil companies, banks, and manufacturers. Their enormous influence and immense wealth will weigh heavily in resolving the issue.

A surprising announcement came that may hint at trending opinions in Europe: Yesterday Switzerland became the first country in the world to lift sanctions on Iran, in support of the nuclear deal.

For the President’s supporters, the deal holds real promise for the creation of a partnership of former adversaries united against terror.

If it proves successful, the world may finally have cause to breathe a sigh of relief, but as nearly everyone involved agrees, the outcome is still far from certain.

Briefly: In our opinion, speculative short positions are favored (with stop-loss at 2,140, and profit target at 1,980, S&P 500 index)

Our intraday outlook is bearish, and our short-term outlook is bearish:

Intraday outlook (next 24 hours): bearish

Short-term outlook (next 1-2 weeks): bearish

Medium-term outlook (next 1-3 months): neutral

Long-term outlook (next year): bullish

The U.S. stock market indexes lost 0.7-0.9% on Wednesday, retracing their recent move up, as investors reacted to the FOMC’s Minutes release, among others. Our yesterday’s bearish intraday outlook has proved accurate. The S&P 500 index remains within half-year long medium-term consolidation, as it continues to fluctuate along the level of 2,100. The nearest important level of resistance is at around 2,100-2,115, marked by local highs. On the other hand, support level is at 2,040-2,060, marked by some previous local lows. There have been no confirmed negative signals so far, however, we still can see negative medium-term technical divergences:

Expectations before the opening of today’s trading session are negative, with index futures currently down 0.7%. The main European stock market indexes have lost 0.4-0.8% so far. Investors will now wait for some economic data announcements: Initial Claims at 8:30 a.m., Existing Home Sales, Philadelphia Fed, Leading Indicators at 10:00 a.m. The S&P 500 futures contract (CFD) trades within an intraday downtrend, as it continues its recent move down. The nearest important level of resistance is at 2,080-2,100, and support level is at 2,040-2,050, as the 15-minute chart shows:

The technology Nasdaq 100 futures contract (CFD) follows a similar path, as it continues its short-term downtrend. The nearest important level of resistance is at around 4,500. On the other hand, support level is at 4,430-4,450, as we can see on the 15-minute chart:

Concluding, the broad stock market retraced its recent move up yesterday, as it extended its short-term consolidation. There have been no confirmed medium-term negative signals so far. However, we continue to maintain our speculative short position (2,098.27, S&P 500 index), as we expect medium-term downward correction or an uptrend reversal. Stop-loss is at 2,140, and potential profit target is at 1,980. You can trade S&P 500 index using futures contracts (S&P 500 futures contract – SP, E-mini S&P 500 futures contract – ES) or an ETF like the SPDR S&P 500 ETF – SPY. It is always important to set some exit price level in case some events cause the price to move in the unlikely direction. Having safety measures in place helps limit potential losses while letting the gains grow.

Thank you.

On the heels of the Shanghai stock market plunging over 6%, the Godfather of newsletter writers, 91-year-old Richard Russell, declares gold bottomed as China shocked the world. The legend also discussed the chaos in China as well as a trapped and increasingly desperate Federal Reserve.

On the heels of the Shanghai stock market plunging over 6%, the Godfather of newsletter writers, 91-year-old Richard Russell, declares gold bottomed as China shocked the world. The legend also discussed the chaos in China as well as a trapped and increasingly desperate Federal Reserve.

……read more HERE

Economic Basis For Large Bear Market Declines

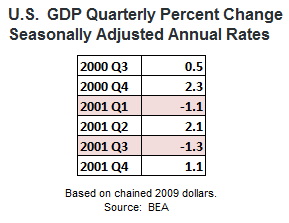

As we noted in a recent “recession odds” article, bear markets typically are caused by one of two things: a recession or tight monetary conditions. For example, the 2000-2002 bear market featured a rough economic period in 2001 (see table below).

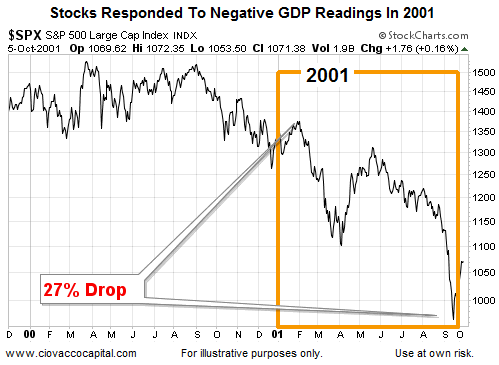

The chart below shows a period in 2001 that featured a 27% drop in the S&P 500, which even in isolation crossed the widely accepted 20% threshold defining a bear market. The big drop occurred during the period of weak economic growth as shown in the table above.

2001 vs. 2008 vs. 2015: Another Perspective

Almost everyone I talk to thinks the European sovereign-debt crisis has passed. They say Greece’s bailout fixed the problem. Europe is on the mend, they say.

But as far as I’m concerned, nothing could be further from the truth.

First, severe austerity measures continue to this day and they are causing debt-to-GDP ratios to worsen.

The proof is in the numbers. Before the Greek crisis flared up, debt-to-GDP in Greece stood at 113%. Today, Greece’s debt-to-GDP stands at a tad north of a whopping 177%.

In Spain, pre-crisis debt stood at 40% of GDP. Today it’s more than 97%.

In Italy, it was 106%. Now it stands at 132%.

In France, it was 68%. Now it’s 95%.

In France, it was 68%. Now it’s 95%.

Even Germany’s debt-to-GDP is worsening, leaping from almost 67% in 2008 to almost 75% today.

In each and every case, debt-to-GDP is worse than it was at the beginning of the crisis — and the austerity measures are literally causing the entire European continent to implode.

Second, austerity and climbing debt levels are hollowing out Europe’s economic growth.

According to Eurostat, Europe’s GDP in the second quarter of 2015 slowed to 0.3%, leaving output 1.2% higher than a year ago. The figure disappointed all 19 economists polled who were expecting 0.4% growth.

France’s economy is slumping. GDP growth of 0.2% was expected, but growth came in at 0.0%.

Italy’s GDP came in at 0.2% compared with 0.3% in the first quarter, leaving output only 0.5% higher than a year ago.

And Germany’s economy, the only engine left holding the feeble union together, expanded by 0.4%, lower than the consensus forecast of 0.5%.

All of this continues to create …

Third, some of the worst unemployment we’ve seen in modern times.

Each and every one of these countries is in hock way over its head. And each and every one of them is in the depths of a nightmare caused by austerity measures.

Unemployment in Greece is at 25.6%. Spain: 22.5%. Portugal: 12.4%. Belgium: 8.6%. Italy: 12.7%.

Unemployment among youth (under 25) is still off the charts. In June 2015, 3.181 million young persons were unemployed in the euro area, an unemployment rate of 22.5%.

The lowest rates were observed in Germany (7.1%), Malta (10%), Estonia (10.1% in May 2015), Denmark and Austria (both 10.3%).

And the highest rates were seen in Greece (53.2%), Spain (49.2%), Italy (44.2%) and Croatia (43.1% in the second quarter 2015).

Corporate and personal bankruptcies are surging. Social discontent is on the rise again. And tensions between countries within Europe are higher than ever.

Pretty picture? Hardly. It’s the ugliest economic picture for Europe since the 1930s, when 17 European countries went belly up, sending hundreds of billions of dollars’ worth of francs, marks, lira, and more flooding into the U.S.

That, in turn, sent the U.S. stock markets exploding higher. It sent the dollar and gold simultaneously into a moon shot as well. And it’s all about to happen again.

Fourth, deflation is picking up momentum.

With austerity measures squashing growth all over Europe, deflation is starting to run rampant.

According to the latest data, prices eurozone producers charged for their goods fell a whopping 2.2% at the August data release.

In short, nothing, and I mean nothing, has been solved in Europe. The crisis will soon escalate with a vengeance.

When (not if) Europe’s economy roils again:

First, you’re going to see trillions more euros stampede for the exits. That’s going to send several large European financial institutions down the tubes.

Second, that flood of capital is going to send the U.S. dollar again into rally mode. Just like it did in the early 1930s when Europe last went bankrupt.

Third, after a correction, it’s also going to send our stock markets roaring higher. Just like it did between 1932 and 1937 when the Dow Jones Industrials soared 387% as Europe went under.

Fourth, it’s going to give you multiple profit opportunities to potentially make more money than you ever dreamed of. In stocks. In commodities. In the dollar. And in gold and silver.

My suggestions right now are …

A. Keep your eyes on Europe. And keep most of your liquid funds in cash, ready to be deployed on a moment’s notice, but as safe as can be right now.

The best way, in my opinion: A short-term Treasury-only fund in the U.S., or the equivalent.

B. Earmark a portion of your cash for speculation. Not too much, and not too little. I recommend 25% of your total investable funds. Funds that you do not need for anything else.

Finally, don’t let anyone kid you. Europe’s problems are simply the beginning of a great sovereign-debt crisis that will soon spread around the globe, creating some of the worst times we have ever seen …

And some of the biggest threats to your wealth, ever. But along with this crisis will also come some of the greatest speculative profit opportunities, ever …

And you should do everything in your power to take advantage of them. I know I will.

Best wishes,

Larry

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair