Asset protection

“Today features a piece by a man whose recently released masterpiece has been praised around the world”

‘During the press conferences of the recent FOMC meetings, millions of well-educated investment professionals will have been sitting in front of their screens, chewing their fingernails, listening as if spellbound to what Janet Yellen has to tell them. Will she finally raise the federal funds rate that has been zero bound for over six years?”

…read it HERE (fascinating article – Money Talks Ed)

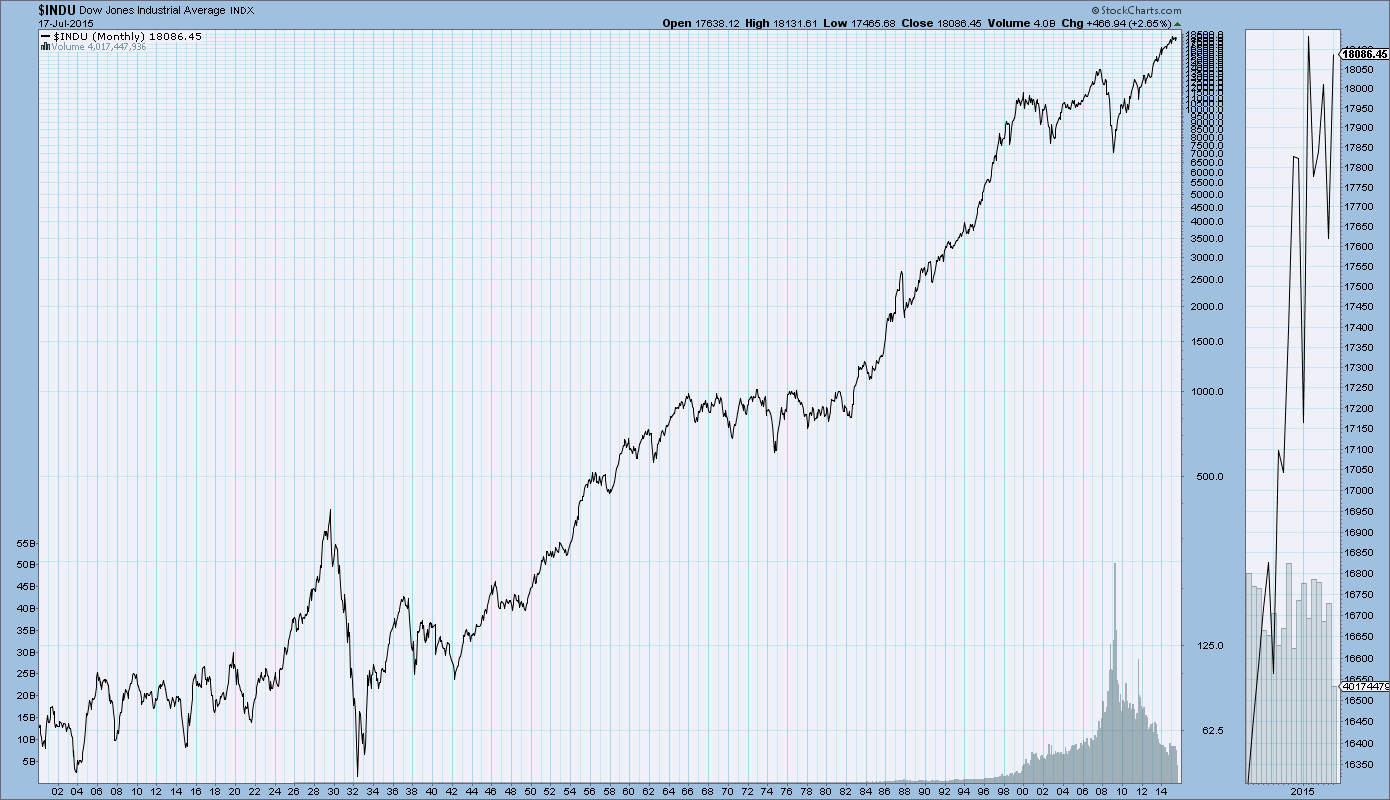

One look at this 115 year chart of the Dow Industrials reveals that despite World Wars, Depressions and financial catastrophes, stocks have always produced outsized returns. Outsized returns for the very patient mind you, but outsized returns nonetheless. Take a look:

- The long-term, more than 100-year performance: Since 1900 (end-of-year 1899), through 2012, the average total return/year of the DJIA was approximately 9.4% — 4.8% in price appreciation, plus approx 4.6% in dividends.

- The average annual stock market return for the past twenty-five calendar years (since 1987) was 10.6% (7.9%, plus 2.7%) The market was up over 40% before the October 19, “Black Monday,” crash. After a significant recovery, the Dow actually closed up 6% for the year. (For further time periods and statistics go to Observation HERE)

So even in an absolutely worst case scenario of an investor buying the index at the very peak of the Dow at 381 in 1929, that person would have been even index wise 25 years later and have well more than doubled (including dividends) long before the Dow hit its peak at 1000 in 1966.

In a better scenario you will get the likes of a quality stock buyer like Warren Buffet earning a 20% annual return over the period 1965 – 2012, a period that just happened to have one of the longest stretches of stock market underperformance between 1966 – 1983, not to mention the crashes of 1987 and 2008.

When you invest in stocks, you must know there will be periods when stock market returns will go negative, and you must accept the risk of occasional bear markets. But you do get paid for it through the “Equity Risk Premium. Or in other words you earn more in return for being willing to endure periods of loss. (Ed Note: Currently that premium is estimated be 5.5% over 30 year Treasury Bonds, or over the long term stocks will outperform Treasury Bonds by 5.5%)

Summary:

Over the long term at least, the return on stocks is greater than bonds.

Current State of the Markets

The Central Banks zero (now minus zero) interest rates, stimulus from the ECB, China, Japan and directly and indirectly from the U.S. Federal Reserve will ultimately force equity prices higher. Nevertheless recent stock market gains lead me to believe that keeping 25% cash take advantage of any further selloffs is a good idea for now. Marc Leibovits recent advice is also very wise:

“eliminating long-term bonds from your portfolios, avoiding the most rate-sensitive sectors of the stock market, sticking only with the highest-rated stocks in powerful sectors experiencing their own private bull markets, and dabbling (gingerly) in the most beaten-down, dirt cheap stocks that already reflect a huge amount of pessimism.”

In my opinion some of those dirt cheap stocks definitely reside in the precious metals sector, and for those more cautious you can always use the options market to reduce your risk.

Robert Zurrer

NORMANDY, France – “Now, I think I’ve seen everything” is an expression that – like “this is the end of history” and “I’ll never leave you” – usually turns out to be premature.

But it is what we found ourselves saying yesterday.

Not out loud. We just moved our lips in mute amazement.

On Tuesday, the Italian government sold a 2-year note yielding MINUS 0.023%.

We don’t know what is more preposterous: that the Italians were able to borrow money at a negative nominal interest rate or that the press reported this transaction with a straight face.

The Fed’s Big Pivot

It should have provoked howls of laughter, withering scorn, and unvarnished derision.

But here at the Diary, we will not point the finger and chuckle. We will not invoke our usual tone of sarcasm. We will not damn the whole thing to Hell with loud and blustery cussing.

Instead, we’ll take the high road; we just want to know what it means.

But before we get to that, let us pick up the news. Here’s the latest, from Bloomberg:

Federal Reserve officials pivoted toward a December interest-rate increase, betting that further job gains will lead to higher inflation over time and allow them to close an unprecedented era of near-zero borrowing costs.

The Federal Open Market Committee dropped a reference to global risks and referred to its “next meeting” on Dec. 15-16 as it discussed liftoff timing in a statement released Wednesday in Washington, preparing investors for the first rate rise since 2006.

“Pivot” has become the latest fad verb. It seems to mean “move” or “go toward.” You can use it in practically any setting.

Investors pivoted toward higher prices yesterday, with a 198-point increase in the Dow. You might tell your husband that you’re pivoting toward buying a new Tesla. And we pivoted back to France last night… after a few days in Ireland.

It is a gray day in Normandy this morning. But the leaves have pivoted to such glorious shades of orange that the effect is a profound and melancholy splendor.

But let us pivot back to our subject for today…

An Odd World

A negative nominal interest rate – meaning a negative rate before you account for inflation – implies an odd world…

…maybe even a world that cannot really exist.

To lend at less than zero suggests you believe the present value of money is less than its future value – in other words, deflation. And you must assume that the risk of default or inflation is near zero.

This allows the Italians to go out and build roads or pay pensions with money that cost them less than nothing.

How long this will last, we don’t know. But as long as rates remain below zero (and they could go lower!) money is not just free… it’s a cost not to borrow!

Imagine you are buying a house. (Now, you can see the mischief afoot!) If lenders are willing to grant a loan at a negative nominal interest rate that’s secured by nothing more than the full faith and credit of the Italian government, then lenders should surely be willing to extend credit to you against the value of your house.

That would leave you with a curious mortgage – one that pays you interest. At the Italian rate, a $1-million house would come with an extra income of about $19.16 a month.

This raises profound metaphysical issues. If a mortgage carries negative interest, it implies that the house (an equal capital value) also has negative value.

After all, you have to pay someone to live in it. And if houses are worth less than nothing, we have to wonder what a car is worth… or a diamond ring… or a luxury cruise?

Does that mean that money has no value? Or even negative value?

After all, you can no longer give it to someone in exchange for a positive interest payment. Now you must pay him to store it for you, as though it were furniture that won’t fit in your house. You don’t like it anymore. But you don’t have the heart to throw it away.

And if money has no value, what happens when you hire, say, a gardener to pull out weeds? Should you pay him? Or should he pay you? How many hours should he have to work for you before you consent to take his money?

The whole thing is so contrary to nature we gasp when we think of it. We are flummoxed.

But you are a smart person, dear reader: Maybe you can figure it out for us.

The Strange Case of Sweden

This is all prelude to taking up the strange case of Sweden…

All we know about Sweden is what we learned by watching the movie The Girl with the Dragon Tattoo.

And all we learned from that was that Swedes tend to be murderers, sadists, lesbians, and pock-marked wimps.

Maybe that accounts for the torturous financial system the Swedes are creating.

Reports Business Insider:

“Sweden is shaping up to be the first country to plunge its citizens into a fascinating – and terrifying – economic experiment: negative interest rates in a cashless society.

The Swedish central bank, the Sveriges Riksbank, on Wednesday held its benchmark interest rate at -0.35%, the level it has been at since July.

Though retail banks have yet to pass that negative rate on to Swedish consumers, they face increased pressure to do so as long as the rates remain where they are. That’s a problem, because Sweden is the closest country on the planet to becoming an all-electronic cashless society.

Remember, Sweden is the place where, if you use too much cash, banks call the police because they think you might be a terrorist or a criminal. Swedish banks have started removing cash ATMs from rural areas, annoying old people and farmers. Credit Suisse says the rule of thumb in Scandinavia is: “If you have to pay in cash, something is wrong.”

A resistance is forming, and some people are protesting the impending extinction of cash. Björn Eriksson, former head of Sweden’s national police and now head of Säkerhetsbranschen, a lobbying group for the security industry, told The Local, “I’ve heard of people keeping cash in their microwaves because banks won’t accept it.”

Alert readers will recognize this negative interest story as one we have been following. We believe it won’t be long before we have negative rates in the U.S., too”.

The feds will pivot to even stricter controls on cash to gain more control over the economy and practically unlimited power to tax and spend – without congressional approval.

Sweden is ahead of the U.S. feds on this one. We can only hope it goes far ahead, fast, and blows itself up before the U.S. pivots down that path, too.

Regards,

Bill

Further Reading: Yesterday, we began a special Diary series with currencies expert Jim Rickards on governments’ ongoing war on cash. Catch up on Part I of our three-part Special Edition here.

Tech Insite

[Editor’s Note: We’ll soon be launching a new investment advisory, Exponential Tech Investor, to help you profit from game-changing innovations. Below, editor Jeff Brown identifies an exciting area of breakthrough technology.]

DNA sequencing is an area of tech I’m keeping a close eye on. That’s because it’s undergoing exponential change…

The technology has been around for decades. But it was far too expensive to be practical. We just didn’t have the abundance of low-cost computing power that’s available today.

The first human genome was sequenced in 2000 at a cost of $2.7 billion. Today, the cost of sequencing has dropped to less than $1,000. Within two years it will be less than $100. By 2020, I expect it will essentially be free.

Why will DNA sequencing be free? Because companies will pay for the information, so you won’t have to.

Facebook is free because it sells your valuable personal information to companies all around the world. Similarly, DNA sequencing will be free because companies will pay to have access to the data they collect.

Which industry players would want access to DNA data?

Biotechnology and pharmaceutical companies want the data to accelerate their testing and developing of new medicines. This will help bring new products to market more quickly. Drugs will be personalized for individuals. Fewer side effects, better efficacy, more revenue, higher profits.

Health insurance companies want the data for preventive medicine techniques. This will help reduce costs.

Employers have similar interests. DNA-sequencing would help reduce their costs by improving the health of their employees.

Highly personalized and preventive medicine will lead to longer lives. Living to 120 will not be unusual for anyone young and in good health today… 100 will be the new 60.

The DNA-sequencing market is expected to grow to $20 billion by 2020. And right now, Illumina (NASDAQ:ILMN) is the global leader in sequencing equipment.

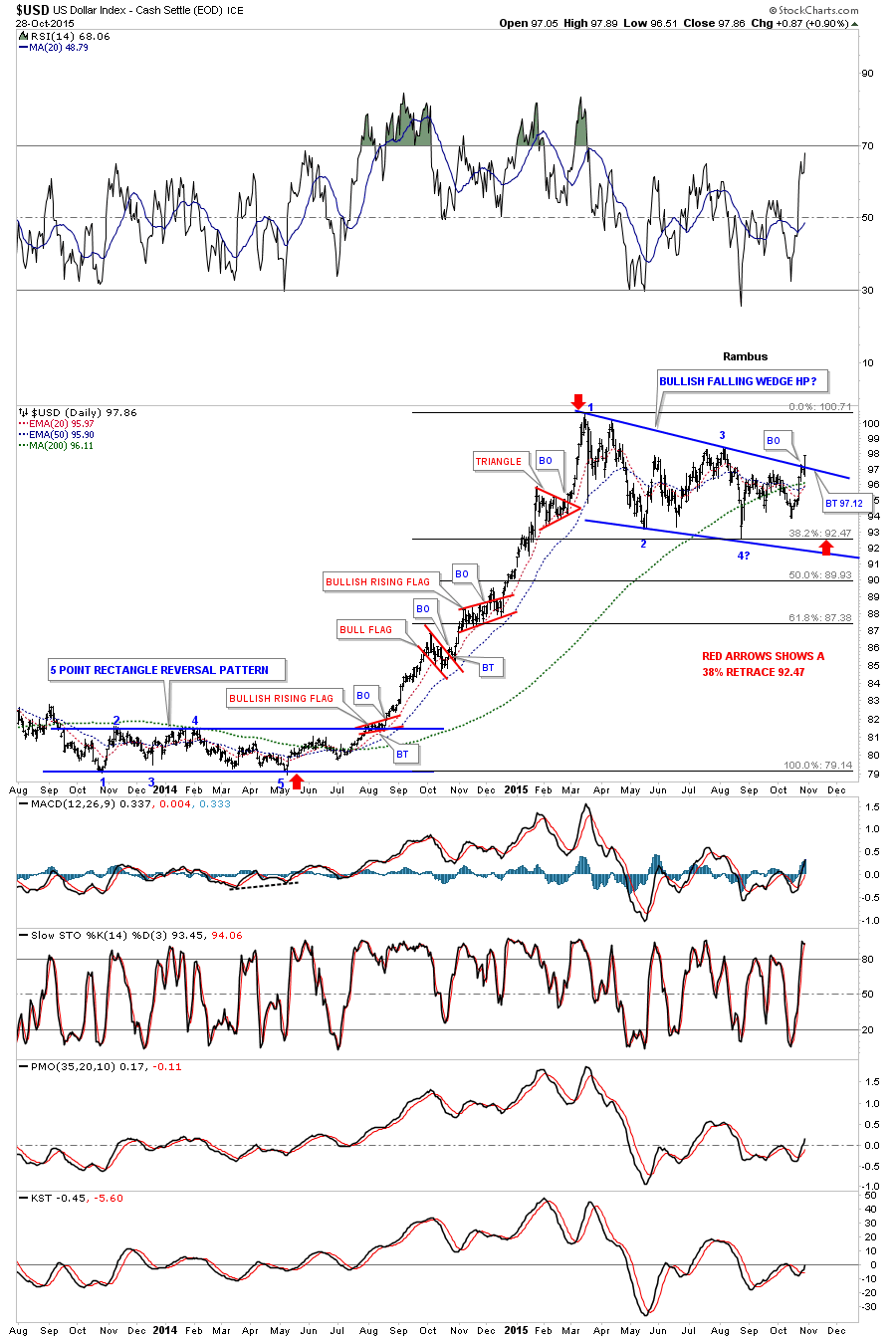

It finally looks like a major inflection point is getting very close to resolving itself in many different areas of the markets. The US dollar is the key driver of this inflection point which is starting to breakout from a nearly eight month bullish falling wedge consolidation pattern. This afternoon the US dollar began a strong rally that is somewhat unusual during the afternoon hours unless it is Fed Day where anything goes . The daily chart below now shows today’s bar clearly above the top rail of the bullish falling wedge. It’s still possible that we could see a backtest to the top rail at 97.12 before the next impulse move up begins in earnest.

There are some positive developments in regards to the US dollar on the daily chart below. First there are four completed reversal points in the blue bullish falling wedge. This eight month consolidation pattern corrected 38% of the first big impulse leg up as shown by the red arrows. The 20 day ema has just recently crossed above the 50 day ema giving a buy signal. The US dollar is now trading well above its 200 dma which shows the long term nature of this bull market.

…..click HERE or the chart below for much bigger charts and a comprehensive analysis – Editor Money Talks

…..click HERE or the chart above for much bigger charts and a comprehensive analysis – Editor Money Talks

1970s: Gold rallied from about $35 in 1970 to nearly $200 in December 1974, and then fell to about $100 in August 1976.

So what?

Examine the graph of average monthly gold prices Jan. 1970 – Sept. 1976. Compare it to the graph of gold prices from April 2002 – October 2015. Note that the second graph was prepared with the same number of data points, but the time scale was doubled – each point is a two month average price. Note the similarity in form. The first is scaled $0 to $200 and the second $0 to $2,000.

What we see

- Gold prices increased by a factor of almost six from 1970 to 1974, and then fell by about 45%.

- Gold prices increased by a factor of about six from April 2002 to August 2011, and then fell by about 45% from the peak.

- Both the rally and correction in 2002 – 2015 took about twice as long as in the 1970s.

- Subsequent to the 1976 bottom, gold prices increased by a factor of about eight in a massive bubble inspired by, among others, inflation worries, fear, and loss-of-confidence in government and central banks.

What does this prove? Well … it proves nothing. But it suggests a few observations.

- Gold prices can be amazingly volatile, especially when fear increases and a majority of people lose confidence in debt based fiat currencies, central banks, and politicians.

- If the analogue continues for several more years, we might see gold prices increase by a factor of five to ten into the $5,000 to $10,000 range in five to seven years (double the 3.5 year rally in the 1970s).

- We should not expect this analogue to predict gold prices, but we should NOT discount the possibility of a similar pattern unfolding.

Why?

- In the late 1970s the US had lost international prestige due to a weak President (Carter), massive inflation and excessive debt.

- Today the US has lost considerable prestige in the Middle-East, Europe and Asia, has excessive debt, no capacity to balance the budget, and has twice elected a President who is …. (your choice of complaint).

- The late 1970s inflation was partially a consequence of massive spending on the Vietnam War – which benefitted few besides military contractors and bankers.

- Today the US has yet to experience and pay for the consequences of wars in Afghanistan, Iraq, Libya, Syria, and Ukraine, but unpleasant consequences will occur. Those wars primarily benefitted military contractors and bankers.

- Central bankers and politicians lost considerable respect in the late 1970s.

- Central bankers and politicians have lost considerable respect in the past several years.

- Debt based fiat currency, backed by nothing but faith, hope, delusions, and taxing authority was deeply devalued in the late 1970s.

- Debt based fiat currency, backed by nothing but faith, hope, delusions, and taxing authority will be deeply devalued in the coming years.

CONCLUSIONS:

There are similarities between the late 1970s and present day. Gold rose substantially for 3.5 years in the late 1970s and increased in price by a factor of about eight. Something similar could (probably will) happen again.

NONSENSE – such as deficit spending, massive debt, excessive leverage, unindicted fraud, pervasive corruption, derivative contracts with minimal margin, hope and delusions, bond monetization, suppressed interest rates, levitated stock markets, forever wars, and so much more – encourages people to think:

- People want to be prepared with the 4 G’s: God, gold, guns, and grub.

- The politicians and central bankers created most of the problems so it is foolish to believe they will solve current problems. Expect more fiscal and monetary nonsense, devaluation of currencies, inflation, and higher gold and silver prices.

- War pays extremely well – if you are a military contractor, banker, or politician – so expect more war. More war creates much more debt, inflation, and fiscal and monetary nonsense.

- The US Congress has a low approval rating – for good reason.

- Debt cannot grow to infinity nor can interest rates remain near zero forever.

- The “silly season” when the US elects a new president is not a time to expect serious and intelligent discourse or change toward fiscal and monetary sanity.

- Time to prepare may be quite short.

- Paper dies, gold thrives.

- Paper dies, silver thrives.

Read:

Graham Summers The Greatest Central Banking Con Job

Steve St. Angelo Collapse of the Western Financial System

Bill Holter Harry Dent is Delusional

Gary Christenson

The Deviant Investor

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair