Energy & Commodities

As a general rule, the most successful man in life is the man who has the best information

“Stock-market bulls argue that Fed rate hikes are bullish for stocks, because the Fed wouldn’t dare raise rates unless the underlying US economy is really improving.

Meanwhile the stock-market bears believe Fed rate hikes are bearish for stocks because they mark the end of the easiest monetary policies on record which levitated the stock markets. It is rather amusing to see stock markets’ historical action during past Fed-rate-hike cycles support neither thesis!

If the SPX’s performance during all 11 Fed-rate-hike cycles is averaged together, it is almost a wash with a mere 2.8% gain.

Gold’s average gain during these same 11 Fed-rate-hike cycles of the modern era was 26.9%, nearly an order of magnitude greater than the stock markets’! Gold also rallied in 6 of these 11, but by a far-greater average of 61.0%. So while stock markets’ performance in Fed-rate-hike cycles has been ambiguous and directionless, gold’s has proved just the opposite. Stock-market bulls are betting on the wrong horse.” Stocks in Rate-Hike Cycles, Adam Hamilton

Loonie Road Kill

Because Canada relies on exports of commodities the multi-year decline in the prices of metals, minerals, natural gas and oil wrecked havoc on the Canadian dollar under the Conservatives.

A Federal Liberal win in Canada’s last election ensured the ‘loonie’ will be crushed further. The Liberals promised deficits less than $10 billion, within one month after being elected, they reneged on that promise. The Libertarian Party now says Liberal deficits could now be as high as $25 billion.

The Bank of Canada’s trend-setting rate is currently 0.5 per cent. It could go to -0.5.

“What we’re saying today is that we now believe that we have roughly a hundred basis points’ worth of room to manoeuvre underneath our current interest setting.” Stephen Poloz, governor of the Bank of Canada

Another of the policies that could be implemented is stimulating the economy through quantitative easing.

Does zero bound interest rates (and perhaps lower), quantitative easing (QE) and running massive deficits sound familiar?

Regardless of it’s performance over the last few years gold’s performance is only negative in USD terms.

Gold’s Bottom Line? In no other currency but the U.S.’s is gold in a bear market. As I write this gold is priced at US$1,065.85 an oz, in Cdn$’s gold is trading for $1,478.87 an oz, a difference of Cdn$413.02. That’s an enormous effect on your bottom line if you’re a soon to be miner or already mining gold in Canada – costs are priced Canadian, profits are priced American.

With disease, famine, drought, floods, climate change, heightened political tension, outright war, a normalization of U.S. interest rates and economic collapse all bubbling together to make a witch’s nasty brew, precious metals look attractive once again.

Conclusion

A Junior exploration company’s place in the food chain is to acquire and explore properties. Their job is to make the discoveries that the mid-tiers and majors takeover and turn into mines.

The bottom line for precious metal investors is that junior exploration companies own the majority of the world’s future gold mines.

This author believes that there is exceptional, and as of yet, undiscovered value in junior companies with quality assets in safe stable countries.

Investors seeking leverage to precious metals should focus on these companies as they have historically provided the best exposure to a rising precious metals price environment.

Have you got gold and a precious metal junior, with an excellent asset in Canada on your radar screen? I do.

If you don’t, maybe you should.

Richard (Rick) Mills

Richard lives with his family on a 160 acre ranch in northern British Columbia. He invests in the resource and biotechnology/pharmaceutical sectors and is the owner of Aheadoftheherd.com. His articles have been published on over 400 websites, including:

WallStreetJournal, USAToday, NationalPost, Lewrockwell, MontrealGazette, VancouverSun, CBSnews, HuffingtonPost, Beforeitsnews, Londonthenews, Wealthwire, CalgaryHerald, Forbes, Dallasnews, SGTreport, Vantagewire, Indiatimes, Ninemsn, Ibtimes, Businessweek, HongKongHerald, Moneytalks, SeekingAlpha, BusinessInsider, Investing.com, MSN.com and the Association of Mining Analysts.

***

Legal Notice / Disclaimer

This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment.

Richard Mills has based this document on information obtained from sources he believes to be reliable but which has not been independently verified.

Richard Mills makes no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Richard Mills only and are subject to change without notice. Richard Mills assumes no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission.

Furthermore, I, Richard Mills, assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information provided within this Report.

Videos and charts (double click to enlarge):

Ed Note: For all charts in visual form plus video links below go HERE

US Stock Market Video Analysis

Gold & Silver Bullion Video Analysis

Key Precious Metal ETFs Video Analysis

Trader Time Swing Trade Video Analysis

Key Individual Precious Metal Stocks Video Analysis

Thanks,

Morris

Seven years after ZIRP (then NIRP) was launched and central banks grew their balance sheets by $13 trillion, in the process inflating the biggest bubble the world has ever seen, sending risk prices to record highs and trillions in government debt to record negative yields, first the Fed admitted QE was a mistake, and now the investment banks – especially those who were bailed out and were the biggest beneficiaries of QE such as Citigroup – admit central bank quantitative easing failed.

Seven years after ZIRP (then NIRP) was launched and central banks grew their balance sheets by $13 trillion, in the process inflating the biggest bubble the world has ever seen, sending risk prices to record highs and trillions in government debt to record negative yields, first the Fed admitted QE was a mistake, and now the investment banks – especially those who were bailed out and were the biggest beneficiaries of QE such as Citigroup – admit central bank quantitative easing failed.

The reason for this failure? What we said from day one dooms all unconventional monetary policy – too much debt.

Here is Citi’s Willem Buiter, finally catching up to what we said in early 2009.

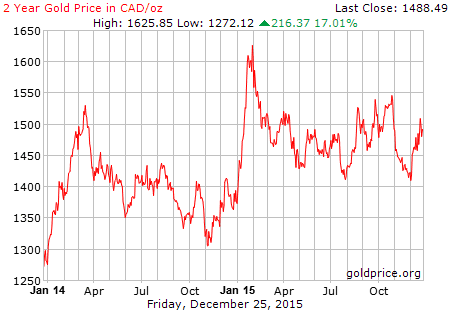

Along with the currencies of most other commodity-exporting countries, the Canadian dollar has been in near-freefall lately.

Gold, meanwhile, has been sucked down with the rest of the commodities complex, falling hard since 2013. But only in US dollars. For Canadians, with their weak domestic currency, gold has been behaving just fine. It’s up 17% in C$ terms over the past two years and looks ready to rally from here:

Protection from currency trouble is why people own it, and why in the vast majority of places it’s owners are very happy.

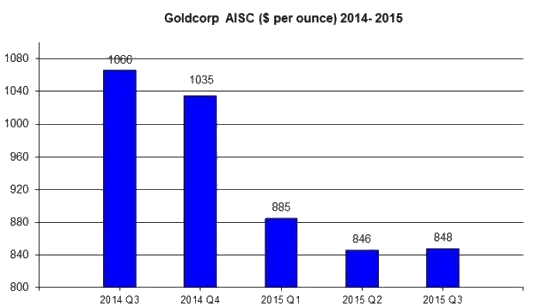

Now combine a falling currency with a crashing oil price and the result is a surprisingly favorable environment for Canadian and other weak-currency-country gold miners. Big mostly-Canadian miner Goldcorp, for instance, has seen its production costs fall by almost 20% in USD terms in the past two years, with more to come based on the subsequent cheapening of the diesel fuel required to run its equipment.

If 2016 plays out according to the script that has rising US interest rates producing an even stronger dollar (and correspondingly weaker currencies elsewhere) the terms of trade for non-US gold miners should become even more favorable. Many of them will report positive earnings comparisons while most other industries are doing the opposite, putting them on the radar screens of momentum traders and value investors who haven’t been paying attention since the last gold/USD bull market ended.

…also:

ETF.com: Do you see value in the emerging market stock market after they’ve come down so much?

ETF.com: Do you see value in the emerging market stock market after they’ve come down so much?

Marc Faber: There is value here and there. But in general, considering the slowdown I’m expecting, there’s no hurry to buy these emerging markets. You can wait for another six months or so.

If you said, “Marc, here’s $1 million. You have to choose, and you can only choose one thing: You can buy the U.S. stock market or you can buy emerging market stocks.” If this was an investment for the next five to 10 years, I would say to buy emerging market stocks.

related:

Marc Faber : Everything is distorted, and it’s a Relative Game

“The global economy is probably already in recession now. It will be more obvious in the U.S. in March or June of next year,” Marc Faber told ETF.com.

“At that time, the Fed will say, “Well, we didn’t want to increase interest rates, but there was pressure on us to do so. So we increased them, and now we have a recession, and now we have to cut them again and flood the market with QE4,”

“If you said, ‘Marc, here is $1 million, but you have to put everything in either gold or in the Dow Jones,’ then I would say I’d take gold,” he said.

“Everything is distorted, and it’s a relative game. Looking at the fundamentals of the world, including the quantity of money, the magnitude of debt as a percent of GDP, the low economic potential and the mad frame of mind of central bankers and their intellectual dishonesty, I would own gold,”

Marc Faber is an international investor known for his uncanny predictions of the stock market and futures markets around the world.Dr. Doom also trades currencies and commodity futures like Gold and Oil.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair