Mike's Content

Did you know…

Did you know…- There are $3,744,000,000,000 worth of negative yield government bonds in circulation in Europe. That represents 40% of the total.

- The US hasn’t created a single manufacturing job in 2015. Actually they’ve lost 6,600 manufacturing jobs.

- At $21,000 per person, ($294 billion total), Ontario has the highest debt per capita in the world of any non-sovereign entity.

- 23 stock markets crashed in 2015.

- In China, $1.2 trillion US dollars were borrowed in 2015 to pay interest on existing debt. China’s total debt is estimated at $30 trillion.

- The S&P 500 is still at the same level it was in August 2014 – 502 days and counting.

This is just part of the context that we’re dealing with as investors. Throw in facts like there are more people without jobs in the US, France, Spain and Greece than at any time in history and the fact that markets are still within shouting distance of all time highs in the US and parts of Europe, and it’s not tough to see why people are confused.

As legendary investor Jim Rogers recently stated – thanks to central bank action, “we are all floating around on a sea of artificial liquidity right now.” The question is – how and when is it going to end?

In China the answer may well be – it already has. As this week has demonstrated, despite unprecedented intervention by the Chinese government and central bank the market turmoil continues. It’s already started in Japan where the central bank now owns over 53% of all Exchange Traded Funds and has been forced to buy hundreds of billions worth of stocks in its government pension plan in order to support the Nikkei Index. It is already ending in Venezuela and Brazil.

But what about Europe and North America? When does the music of excessive debt, especially at the state and provincial level, combined with unaffordable entitlement promises stop? And more importantly what are the repercussions for every financial market?

This is where we can help

What I love about the markets is the scorecard. In the end there is no BS, no stories, no excuses – just results. And the results of recommendations at the World Outlook Financial Conference are crystal clear.

We nailed the top in oil and the subsequent decline to the $34 level thanks to energy analyst Josef Schachter. This year Josef will talk about why he thinks a bottom is forming.

At the Conference, and on MoneyTalks, we called the dramatic fall in the Canadian dollar when it was still above par. This year John Johnston, the man who shocked audiences three years ago in predicting that the loonie could hit 70 cents is back. And wait til you hear what he sees coming now.

The Outlook Conference’s track record on real estate is exceptional thanks to the work of Ozzie Jurock. As early as 2011 Ozzie told audiences to get into the Phoenix area and now with the appreciation of the US dollar and the recovery in prices, investors who followed the advice have done incredibly well.

This year Keystone’s Ryan Irvine will reveal the 2016 World Outlook Small Cap Portfolio. While past performance is not a guarantee of future results, it is impressive that the Outlook Small Cap portfolio has achieved double digit returns every single year.

Arguably, the most incredible forecast at any World Outlook Conference was Martin Armstrong’s prediction in 2013 that Russia would invade Ukraine in late February the following year immediately after the close of the Olympics. That’s not the first time Martin has wowed audiences with incredibly accurate predictions – and thankfully Martin will be back this year. And there are no shortage of issues to talk about.

These results have not been achieved by accident. Our analysts have been chosen precisely because they do have strong track records. No, they are not right every time but their uncanny ability to read the various investment markets while employing proven risk management techniques has clearly raised their probability of success dramatically. Which, by the way, explains why if you were to personally book a single hour with any of them the cost would start at $3,700. Yet at the World Outlook Financial Conference you can get access to them and get your individual questions answered for as little as $129.

I’m Really Excited About This Change

This year for the first time, we’re featuring a special Real Estate Investing section beginning at 1:00 pm on Friday, January 29, hosted by Ozzie and featuring one of my favourites – Vision Capital’s Jeff Olin. Jeff is one of my favourites not only because he is a nice guy but because he also told us specifically on MoneyTalks two years ago how to play the commercial real estate market downturn in Calgary. And that’s been a big winner.

Jeff’s insights and recommendations will be worth the price of admission alone.

Finally

The bottom line is that we take your time and money seriously. With that in mind we have put together our best Conference ever in the hope of making you a significant amount of money and just as importantly, saving you money in the chaos that’s to come.

I promise it will be worth the time for anyone concerned about their personal finances and investment returns.

Sincerely,

Michael Campbell,

Host of MoneyTalks

Conference Details

Where: Westin Bayshore, Downtown Vancouver

When: Friday, January 29th beginning at 1:00pm with the Real Estate Outlook, and all day Saturday, January 30, 2016

Agenda: http://moneytalks.net/agenda.html

Cost: $129 for a full access General Admission pass.

To book Your Ticket: CLICK HERE

or Call # 604.926.6848 – email info@moneytalks.net

P.S. As you may know I am hugely interested in educating our younger generation. And thanks to the sponsorship of the Online Investment Club service at myvoleo.com we are able to offer a complimentary ticket for young people/students when you purchase a ticket for yourself. And I might add that in the past those that took advantage of the offer really enjoyed the Conference. It is a great way to share/create a common interest with your children – no matter what their age.

P.P.S. Can’t make it in person? No worries, we will have the archive video – shot in HD this year with a four camera crew – available for viewing within 48 hours of the event. It is a great way to access all these speakers and more on an unlimited basis for a year. CLICK HERE to order

The ISM purchasing managers’ index for the manufacturing sector in December 2015 in the USA has plummeted to its lowest level since June of 2009. This warns that the U.S. economy is entering a recession that is in line with the forecast of the ECM and the rise in the dollar.

The ISM purchasing managers’ index for the manufacturing sector in December 2015 in the USA has plummeted to its lowest level since June of 2009. This warns that the U.S. economy is entering a recession that is in line with the forecast of the ECM and the rise in the dollar.

However, keep in mind that this is simultaneously coming with the changing technology trend. By that, we mean that low-level jobs are being replaced rapidly by automated computers, in part, because of Obamacare and its Draconian tax burden upon business exceeding 25 employees. Therefore, unemployment will rise due to this expansion in technology and raising the minimum wage will accelerate that trend further.

In business, inventories are also shrinking as companies move to “just in time” methods by using technological advancements to minimize carried inventory. This trend is only further accelerated by the banks moving toward transactional banking where they are no longer interested in relationship banking. This also reduces the availability of loans for small business as banks do not want the risk.

The convergence of these trends will feel the recession ahead. Eventually, this will materialize in rising unemployment, a deepening crisis in student loans, and the fiscal mismanagement of governments demanding more and more taxes which will become a toxic cocktail of doom.

The ultimate rise in stocks in the years ahead (after a correction sling-shot move) will unfold simply as capital tries to secure its future by getting out of government bonds and banks.

Happy New Year! I hope you had a wonderful holiday with friends and family. And, most of all, here’s to a healthy, wealthy and prosperous 2016!

Happy New Year! I hope you had a wonderful holiday with friends and family. And, most of all, here’s to a healthy, wealthy and prosperous 2016!

Today I’m going to cut right to the chase. My Real Wealth Reportmembers already have my detailed top forecasts for 2016 and naturally, they will get all of my recommendations. Here, I can only give you a sneak peek of what I expect this year.

Mind you, I’m not an alarmist. I simply tell it like it is. How I see things unfolding based on my economic models. How I see the markets developing. So heed my views in this very important first column of the new year.

By doing so, you’ll be better prepared for what’s coming: One heck of a wild and wooly year in the markets, loaded with dangers and profit opportunities.

Let’s get started …

Sneak Peek #1:

Destructive economic winds continue to

steadily pick up, in almost every conceivable way.

Europe’s economy continues to slide, all with worsening sovereign debt-to-GDP ratios … unemployment starting to rise again … industrial production starting to slump again … and deflation worsening almost monthly.

And throughout Europe, currencies are swooning. Not the least of which is the euro, down a whopping 21.3% since its high in May 2014. Also sliding, the Czech koruna, down 6.2% in 2015. Hungary’s forint, down 8.27%. Poland’s zloty, down 9.87%.

Then there’s Russia, with GDP having plunged 4.1%. The Russian ruble has crashed 21.6%.

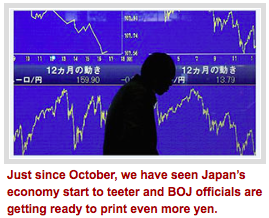

And just since early October, we have also seen Japan’s economy start to teeter again, with sovereign debts skyrocketing … the economy barely muddling along … and Bank of Japan officials getting ready to print even more yen.

And just since early October, we have also seen Japan’s economy start to teeter again, with sovereign debts skyrocketing … the economy barely muddling along … and Bank of Japan officials getting ready to print even more yen.

Worse will be the increasing geopolitical stress — domestically and internationally — that is now coming true, sadly, in spades. ISIS, Boko Haram, the deadly Paris attacks. And now, Saudi Arabia and Iran, causing global equity markets to plunge on the very first trading day of the new year.

In fact, according to the Institute for Economics & Peace’s recent report on its 2015 Global Terrorism Index — deaths from terrorism increased 80% in 2014 alone to its highest level ever.

Sneak Peek #2:

Another bull run higher for the dollar.

And collapse in the euro.

Yes, someday, most likely by the end of 2020, the dollar will lose its almost singular reserve currency status …

Not because it will crash and burn. But because it will eventually become so strong that it breaks the back of almost every country that has dollar denominated debt — including our own government.

Sure, there will be short-term setbacks for the dollar, but overall, the dollar is headed higher in 2016, possibly much higher.

The forces are easy to see:

- Europe. It’s sure to go even further down the drain in 2016. The European economy will continue to slow, debts will continue to pile up and on top of all that, the Syrian refugee crisis will take its toll on European budgets, not to mention precipitate even more domestic unrest, cultural conflict, and terrorism.

- Moreover, Mario Draghi will be forced to print even more euros and keep interest rates even more negative in the European Union. Meanwhile …

- Economic growth, though modest at best in the U.S., will continue to attract capital inflows into the U.S. dollar.

- Geopolitical tensions and rising terrorism, also will benefit the dollar, as will … surprisingly …

- China’s yuan. Yes, to the surprise of many except for you and those reading my Real Wealth Report and related services … since the International Monetary Fund (IMF) admitted China’s yuan as a reserve currency on Nov. 30, the yuan started plunging, falling as much as 2.4%. So much so that authorities in Beijing are now worried about an outright tsunami of yuan leaving the country.

And they should be. Chinese investors will be among the first to diversify their assets now that the currency is becoming freely convertible. But that’s the part of the story almost no one told you about, unless again, you were one of my subscribers.

Remember, wherever the global economy slows, whenever there are troubled spots in any part of the world, not to mention rising geopolitical conflict and terrorism …

Dollars get bought to either buy assets or pay down debt, and the dollar rallies.

It’s that simple.

Yet despite a stronger dollar …

Sneak Peek #3:

A rolling thunder of commodity bottoms and new bull markets are right around the corner.

I have shown you some of my forecast charts in recent columns. Gold, silver, platinum and palladium have all followed my forecasts to the tee, plunging throughout 2015, reaching new lows for their bear markets nearly right on time in November and December.

But it’s not just precious metals that are bottoming and should soon start awakening in new bull markets.

It’s also oil, natural gas, grain markets, and yes, oil and gas exploration companies and mining shares — where more money will be made in the next few years than any other asset class out there.

The commodity markets are coming together in a way that hasn’t been seen since the middle of the Great Depression …

Where despite deflation and all the problems in the world, commodities — as tangible assets — came roaring back into favor amongst the savvy … rightfully concerned that entire governments would be collapsing.

Stay tuned and stay safe,

Larry

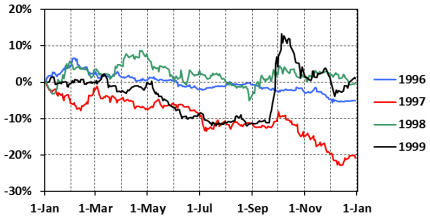

My recent work has focused on seasonality of the gold price (Mercenary Musings: October 19; October 26; November 23). Today, I present new research covering a 20-year time frame from 1996- 2015 that includes a 12-year bull market for gold from 2001-2012 bracketed by bear markets in the late 1990s and mid-2010s.

In a series of normalized charts, I will show that regardless of overall year-over-year bull or bear market conditions, there are predictable intra-year trends in the gold price.

The first series of charts shows the percentage change in the daily gold price normalized to January 1 for each year from 1996 to 2015. Please note that all gold prices are London afternoon close:

The Federal Reserve’s recent rate hike is symbolic, intended to signal the end of the financial crisis and the start of normalization.

The Federal Reserve’s recent rate hike is symbolic, intended to signal the end of the financial crisis and the start of normalization.

The rise will have minimal effect on consumption and investment. Analysts have already moved beyond the Fed’s well-telegraphed decision, focusing on the future trajectory of U.S. monetary policy.

The Fed forecasts around four additional rate increases in 2016 and a similar number in 2017. This would mean that U.S. official rates would be around 1.375% and 2.375% by the end of 2016 and 2017, respectively. The median estimate for the longer-term federal funds rate is around 3.5%.

Yet the central bank’s moves may be more gradual than most Fed-watchers expect. Here’s why:

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair