Timing & trends

On Monday evening, something strange happened: Donald Trump became a “loser.”

Not in the pejorative sense of the word (as he so often uses the term), but rather in the sense that the GOP front runner who just two days ago surpassed Ted Cruz in Iowa pre-caucus polls for the first time since last August, lost to the Texas senator in the all important Iowa caucuses.

To be sure, few would have predicted last year that the brazen billionaire would have been competitive in Iowa, let alone place second. In that regard, last night’s performance was a validation of Trump’s legitimacy as a born again politician.

On the other hand, the results suggest Trump can’t win on mere bombast. Trump spent as much on “Make America Great Again” hats as he did on staff in the lead-up to the caucuses and that, some say, may have cost him.

Another Monday, another set of “surprisingly” bad economic numbers. A few representative headlines:

China manufacturing prices decline for 18th straight month

Oil prices fall 5% on bad China data, OPEC uncertainty

Global factories parched for demand, need stimulus

Junk bonds suffer a rare negative return in January

US consumer spending softens, savings hit 3-year high

US manufacturing weak again in January

China official PMI misses in January, Caixin PMI shows contraction

Japanese bond yields continue to collapse

There’s more, but you get the (very dark) picture. And thanks to the Atlanta Fed’s GDPNowprogram we can see in real time how these numbers translate into current-quarter GDP growth. Apparently the US is looking at yet another weak stretch in which economists (represented by the Blue Chip consensus) are gradually forced to admit that they’ve wildly overestimated our ability to manage our debt.

GDP growth matters for a couple of reasons. First, an economy that’s borrowing a lot of money (as all the major ones are) has to generate large amounts of new wealth or it sinks ever-deeper into a hole that eventually leads to a 1930s-style depression. 1.3% growth does not come close to stopping the expansion of debt/GDP. So every quarter like the current one brings a debt-driven collapse that much closer.

Second and far more interesting in the near-term, slow-growth/high-debt countries eventually conclude that their only remaining option is massive currency devaluation. Europe and Japan are already there, and are aggressively ramping up their own currency war offensives. The US, if history is any guide, will soon (either this year or as part of the next administration’s “first 100 days” political offensive) decide that a too-strong dollar is standing in the way of “progress” and will start looking for ways to devalue.

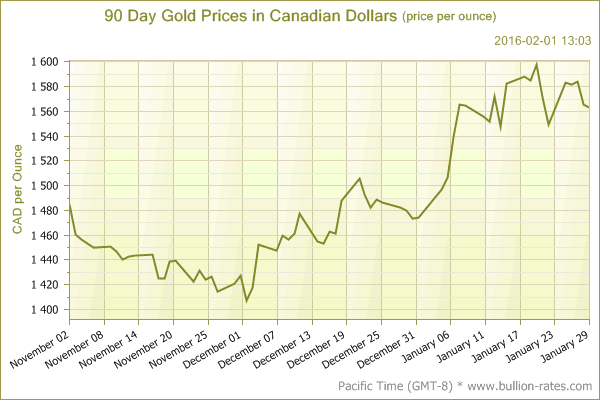

Then the real fun begins — at least for goldbugs. For holders of dollars it won’t be nearly as pleasant. Here’s the Canadian version of what’s coming for US investors, though the US chart will be steeper and will go on for years instead of months:

To review our stance, which is years along now, the gold sector is not going anywhere until it becomes widely accepted that developed stock markets, including and especially those in the US, are in bear cycles. We have also drawn analogies to the Q4 2008 event that took place in what felt like a nanosecond compared to today’s long, drawn out process. For this reason, a better ‘comp’ has been the 1999 to 2001 time frame. That was a process as well.

Regardless, gold boosters viewing inflation as the reason to buy the sector are still out there pitching, but even they have retooled their pitches for a deflationary world. It is now and always has been a global economic contraction environment (assuming it eventually coerces policy makers into inflationary actions) that would be the primary driver of the next gold bull market. Say, whatever happened to all the stories about China demand, a China/India love trade, supply/demand capers on the COMEX and ‘US jobs to spur inflation driving big, smart institutional money into gold’ anyway?

He Also Warned How Terrifying It Will Become

Devastating Bear Market To Correct Gains Since 1932

Richard Russell: “My thinking is that this is the big bear market that will correct the entire rise from the 1932 low. In all my years of writing since 1958 I have never allowed my subscribers to stay invested through a primary bear market. I have kept my subscribers out of common stocks (except gold). For most of this bear market, we will stay on the sidelines, until I have evidence the bear market has ended……continue reading HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair