Currency

Way back in 1998, before the euro even got off the ground, I told everyone I could that the currency wouldn’t last. At best, I said, it would last until the year 2020.

Way back in 1998, before the euro even got off the ground, I told everyone I could that the currency wouldn’t last. At best, I said, it would last until the year 2020.

Few believed me. Many said I was nuts. After all, how could I make such a definite longer-term forecast, especially involving a region of the world that then, and now, still represents the second-largest economic region in the world?

Well, forecasting that the euro would fail was simple: It wasn’t put together properly in the first place. It didn’t stand a chance to survive long-term and still doesn’t.

The architects of the euro — if you can call them that — didn’t have a clue as to what it takes to have a single currency. They just believed one size fits all. But oh, how very foolish, yet typical of leaders anywhere.

Fact: Although the European Central Bank (ECB) was created, each individual country’s former national or central bank was kept in place, with virtually all the powers it had previously.

In other words, the Bank of Italy, for instance, could create its own interest rate policy, set rates, itself, and yes, even print euros if desired.

Imagine that. It would be as if each of the 50 states in the U.S. had their own central bank that could decide its own interest rate policy and print dollars whenever it wanted.

Fact: Euro-planners also never set up a federal debt market. Instead, they figured the existing debts of the individual countries would suffice. No need to convert them to a national or federal debt. No need to unify anything. Just let those debts be.

Insane. What that did was create a potpourri of debts. Worse, underperforming countries could see their debts swing wildly in value as the new currency started to trade. No stability whatsoever.

And, it allowed other countries, such as Greece, to borrow oodles of euros at the low rates of another country when, in reality, its credit rating didn’t deserve such low rates.

To make another analogy, that would be as if the U.S. had no Treasury market whatsoever, and instead, relied on the debts of states as diverse as Mississippi and California as a kind of national debt market.

Fact: As a Continent, Europe is composed of almost 50 countries, each with its own language, own culture and own history. And some countries in Europe have even more than one national language.

So is there a common language in Europe so all Europeans can talk to each other? No, there isn’t.

Is there a common background of some sort that would unite them? No, there isn’t and never has been.

Is there a common future goal that would unite them? You might say an economic union would, which is what the designers of the euro had in mind. A United States of Europe so to speak. A peaceful, united Continent that could avoid the untold scores of wars that have plagued Europe throughout the millennia.

And that is certainly a nice goal or dream to have. But unless you put the infrastructure in place to make a real economic union, with sensitivity and empathy to all the different players and cultures involved …

Such an economic union doesn’t have a snowball’s chance in hell of a surviving.

And indeed, that brings us to today, where now, the euro is finally cracking the last vestiges of important, long-term support.

The currency has already plunged from a monthly high of 1.6028 in July 2008 to 1.08826 as I pen this issue. That’s a humongous plunge of 32.08% in the past eight years, a record decline for a supposed major currency.

And now, as you can see from my latest cyclic forecast chart, the euro’s plunge is about to get a whole lot worse.

The currency has just cracked important support at the 1.0900 level.

It should now fall to the 1.0500 level, then 1.0300 then to 1.000 …

And ultimately, far lower, ceasing to exist at all by the year 2020.

What’s worse are the geopolitical ramifications. What was meant to unite Europe will end up causing the opposite: More and more civil protests … more and more discontent … more revolutionary actions … secessions … anti-Semitism and more, including bloodshed.

For you see, it’s the grand experiments of harebrained politicians that are always the root cause of discontent. They endlessly tinker with the likes of you and me, with the economy, with things they don’t have a clue about …

Until the whole house of cards comes crashing down.

My view: Kiss the euro goodbye. Avoid doing business in the euro at all costs. Stay in U.S. dollars. Invest in U.S. dollars, trade in U.S. dollars.

Best wishes,

Larry

Trader Training – Some Ways to Fix Your Problems

Stock trading is simple, but not easy. As long as we are normal, emotional human beings, we will make mistakes in the application of our trading plans. Countless hours can be spent developing the rules for a profitable trading strategy but, unless there is absolute discipline in applying that strategy, results can be poor.

In This Week’s Issue:

– Stockscores’ Market Minutes Video – How Much Stock to Buy

– Stockscores Trader Training – Some Ways to Fix Your Problems

– Stock Features of the Week – Long Term Turnarounds

First, it was Kinder Morgan (KMI). Then, ConocoPhillips (COP). Which sacred dividend is going to get cut next?

Regular readers know that I believe big oil is a big avoid for now. But if you insist on speculating in the goo patch, stick with Exxon (XOM).

There are payout problems outside of energy, too. A quick look at Reality Shares’ DIVCON screen reveals seven 4% payers in “DIVCON 1” territory. This means they’re more likely to cut their dividend than raise it. Let’s discuss these, and a few more high yielding problem children.

1 Shaky Telecom

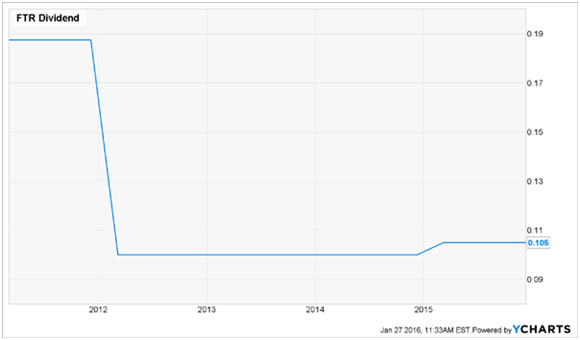

Frontier Communications Corp. (FTR) is a good example of a sky-high yield (8.8%) that should set off alarm bells. As for a low P/E, the “E” part of the equation is non-existent—the telco has posted losses in three of the last four quarters, and the Street forecasts a loss of $0.17 a share in 2016.

Add rising long-term debt (up 74% from a year ago as of the end of Q3) and a payout ratio that’s also headed in the wrong direction (81% of free cash flow, up from 67%) and you get a sense the dividend—which has barely budged since it was cut in 2011—is on borrowed time again.

FTR Hangs Up on Income-Seekers

From Crazy to Crazier

Considering how often “helicopter money” has been mentioned in the mainstream financial press of late, it is probably going to be on the agenda fairly soon. The always dependable Martin Wolf at the FT – who has never seen a printing press he didn’t think could solve all our economic problems – has come out forcefully in favor of the idea. See for instance his recent screed “The case for helicopter money”, followed by the promise – or rather, the threat – that “Helicopter drops might not be far away”.

Silver, at this current time of writing, remains below $15.00 per ounce; it is sitting at $14.76. This price is absurdly cheap given the current state of the global economy and the uncertainty that the world now faces.

Silver, at this current time of writing, remains below $15.00 per ounce; it is sitting at $14.76. This price is absurdly cheap given the current state of the global economy and the uncertainty that the world now faces.

One of the main reasons for silver being so depressed compared to the resilience that gold has shown is the incredible range of uses that silver has in the manufacturing of a vast number of products. This is a topic that we have covered here in the past that highlights why silver, with its dual purpose as both an industrial and monetary commodity, make it so desirable now and in the future.

With the global economy slowing down, so too has silver crashed, along with most other commodities. This has provided a unique opportunity for those of us who value silver as a monetary metal to accumulate it at insanely cheap prices given its current completely out-of-whack gold-to-silver ratio, a ratio that is screaming at the top of its lungs that silver is the steal of the century.

Resting at nearly 84:1, this is one of the highest gold-to-silver ratios that we have ever seen. Typically, throughout history, this ratio has rested at 16:1! What this is saying is that either gold is currently very overpriced, which is not the case – if anything, gold is still a relatively good price given the dangerous precipice we now find ourselves on – or silver is horribly under-priced and is destined to rocket higher in the future.

The latter of the previous two scenarios is the outcome that I am guessing will come to fruition. Silver mines are beginning to shut down due to low prices, which will inevitably lead to supply issues, given the massive physical demand that silver continues to see at these artificially depressed prices.

Mints around the globe have reported record silver sales and have even been forced to temporarily shut down sales multiple times over the past couple of years, indicating that 1) the price is too cheap, and 2) physical silver is in demand.

Another factor that barely anyone is talking about is how the silver mines that are still in production at these low prices have ramped up their mining operations to stay in business and to keep the cash flowing. They are selling their valuable asset for a fraction of its future value.

Yet this action is coming at a huge cost. As not only are they ramping up production, but in addition to this, they are mining their highest-grade product, ie, they are picking all of the low-hanging fruit to keep cost down and profitability up. This will come with a future cost that will force silver prices naturally higher.

Although it is incredibly hard to see at this time through all the gloom and doom surrounding the depressive silver markets, the future is inevitably bright. Silver will once again move higher when the time is right; all the fundamentals are backing this future rise in prices and it is only a matter of time before it takes place. Until then, take advantage of these low prices and keep stacking, my friends.

The views and opinions expressed in this material are those of the author as of the publication date, are subject to change and may not necessarily reflect the opinions of Sprott Money Ltd. Sprott Money does not guarantee the accuracy, completeness, timeliness and reliability of the information or any results from its use.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair