Stocks & Equities

On Jan. 12, President Barack Obama presented his final State of the Union Address.

On Jan. 12, President Barack Obama presented his final State of the Union Address.

After seven years in office, Obama has said his final 12 months would feature efforts to curb gun violence. As he outlined his recent executive actions, an empty chair sat in the Congressional balcony – a symbol and reminder of Americans who have lost their lives to gun violence.

A week prior, his Administration released a list of executive orders aimed at curbing gun violence, including the expansion of background checks for would-be arms buyers and sellers.

In any other industry where regulations may limit access to a consumer good, that sector’s manufacturing stocks would likely suffer a decline. But the gun sector is unlike any other.

The Bank For International Settlements just released a report stating that the spread of negative interest rates hasn’t caused the world to end. From this morning’s Bloomberg:

Negative Interest Rates Are Working Just Fine So Far: BIS

Negative interest-rate policies currently in use by central banks around the world have worked through their respective systems in much the same way as positive rates, though it’s not known how far below zero that would continue to be the case, the Bank for International Settlements said.

In its quarterly report published Sunday, the Basel-based “central bank for central banks” said that “so far, zero has not proved to be a technically binding lower limit for central bank policy rates.”

The BIS’s verdict on negative rates gives backing to the European Central Bank, the Bank of Japan and others at a time when such unconventional methods are facing increasing criticism for their potential impact on the financial industry and currency markets. A sell-off in European bank stocks this year was partly driven by fears that further rate cuts by the ECB would damage profitability in a sector still recovering from the debt crisis.

“The experience so far suggests that modestly negative policy rates are transmitted to money-market rates in very much the same way as positive rates are,” report authors Morten Bech and Aytek Malkhozov said. “Anecdotal evidence suggests banks seek to avoid negative rates by either extending maturities or lending to riskier counterparties.”

The report also presented calculations of the average effective rate that banks pay on cash above the minimum requirements or exemptions at the ECB, the Swiss National Bank, the Riksbank and the Danish central bank, showing that a lower negative policy rate doesn’t necessarily translate into a more expensive proposition for lenders.

The BIS report does include some caveats along the lines of “it’s early in the process and there’s no way to know if more deeply negative rates will cause trouble.” Still, the idea that the system isn’t being stressed by today’s negative rates is belied by some trends that have gotten a fair bit of press lately. Consider:

(Wall Street Journal) – Negative interest rates have the law-abiding scrambling for bills.

Are Japan and Switzerland havens for terrorists and drug lords? High-denomination bills are in high demand in both places, a trend that some politicians claim is a sign of nefarious behavior. Yet the two countries boast some of the lowest crime rates in the world. The cash hoarders are ordinary citizens responding rationally to monetary policy.

The Swiss National Bank introduced negative interest rates in December 2014. The aim was to drive money out of banks and into the economy, but that only works to the extent that savers find attractive places to spend or invest their money.

With economic growth an anemic 1%, many Swiss withdrew cash from the bank and stashed it at home or in safe-deposit boxes. High-denomination notes are naturally preferred for this purpose, so circulation of 1,000-franc notes (worth about $1,010) rose 17% last year. They now account for 60% of all bills in circulation and are worth almost as much as Serbia’s GDP.

Japan, where banks pay infinitesimally low interest on deposits, is a similar story. Demand for the highest-denomination 10,000-yen notes rose 6.2% last year, the largest jump since 2002. But 10,000-yen notes are worth only about $88, so hiding places fill up fast. That explains why Japanese went on a safe-buying spree last month after the Bank of Japan announced negative interest rates on some reserves. Stores reported that sales of safes rose as much as 250%, and shares of safe-maker Secom spiked 5.3% in one week.

That academics and bureaucrats have responded by calling for the partial elimination of cash isn’t helping calm the masses. From the above Wall Street Journal article:

“In certain circles the 500 euro note is known as the ‘Bin Laden,'” former U.S. Treasury SecretaryLarry Summers wrote last month in calling for a global ban on notes worth more than $50 or $100. He noted interest from European Central Bank President Mario Draghi and said that “if Europe moved, pressure could likely be brought on others, notably Switzerland.”

Fellow Harvard economist Kenneth Rogoff wants to retire cash altogether, primarily because “a significant fraction, particularly of large-denomination notes, appears to be used to facilitate tax evasion and illegal activity.” But he doesn’t hide the additional monetary-policy motive: “Getting rid of physical currency and replacing it with electronic money,” he wrote in 2014, would allow central bankers to set negative interest rates without people “bailing out into cash.”

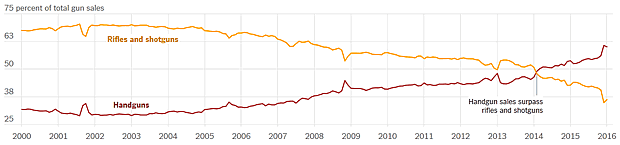

On a different but related note, gun sales are up along with cash and safes. See Gun Sales Soar After Obama Calls for New Restrictions, which includes this fairly striking chart of Americans’ shift from rifles to handguns. The red line is handgun sales as a percentage of total sales. We’re clearly envisioning more up close and personal uses for our guns these days:

Similar trends are taking hold in Europe, where gun culture is not traditonally part of the mainstream.

German Gun Sales and Permit Applications Soar After Cologne Sex Attacks

(Breitbart) – Gun sales and gun permit applications have soared in Germany in the wake of the sex attacks in Cologne on New Years Eve. Cologne, Düsseldorf and Frankfurt are all reporting an influx of requests for permits with Cologne police estimating at least 304 applications since the attacks. In 2015 the entire year saw only 408 applications total in the city.

Spokesman Andre Hartwich of the Düsseldorf police estimates at least eight to ten application requests per day, which if continued throughout the year would dwarf the previous year’s requests total of 1,500.

Ralph Pipe of the Frankfurt Police procedural office has said, “We have been beginning every day with at least 13 applications,” in comparison to last year in which there were only one or two applications per day.

Cologne police also mentioned that pepper spray is not covered under the Arms Act and does not require a permit or license. Sales of pepper spray in Germany have likewise increased and, as Breitbart London has reported, many vendors are even sold out.

This is all part of the same process, in which fiat currency printing presses lead to excessive debt and unwise foreign adventures, which lead to slowing growth, greater wealth inequality and geopolitical blowback, culminating in the kind of generalized mess that we see today.

People react to these uncertainties by trying to protect themselves with cash and guns, and governments respond by trying to limit citizens’ ability to do so.

If this play has a third act, it will involve the abolition of cash in some major countries, the rise of various kinds of black markets (silver coins, private-label cash, cryptocurrencies like bitcoin) that bypass traditional banking systems, and a surge in civil unrest, as all those guns are put to use.

The speed with which cash, safes and guns are being accumulated — and the simultaneous intensification of the war on cash — imply that the stress is building rapidly, and that the third act may be coming soon.

‘Gloom, Boom & Doom Report’ Publisher Marc Faber provides insight into the global market selloff.

‘Gloom, Boom & Doom Report’ Publisher Marc Faber provides insight into the global market selloff.

“It could be worse… what we’re seeing here is just an appetizer of something larger”

“My sense is that many policies that were implemented- in particular zero interest rates and more recently negative interest rates- are rather negative for asset markets than positive,” he explained. “They create a lot of uncertainty in investors’ minds and we have statistics on all the countries that have introduced negative interest rates. In all these countries actually the savings rate went up.”

On the heels of eight weeks of chaotic trading in markets, today the man who has become legendary for his predictions on QE, historic moves in currencies, and major global events, just warned that a massive global money printing program is about to shock the world.

Egon von Greyerz: “Eric, gold is now in a hurry and will surprise everyone with the speed of its move. The heavily massaged and false unemployment numbers on Friday pushed gold down $20 temporarily, but 70 minutes later gold surged to new highs and then closed unchanged on the day. In my view there is now nothing that can hold back gold from going to new highs in 2016.

Question: If there’s another financial catastrophe, can the government save the day again?

Question: If there’s another financial catastrophe, can the government save the day again?

Until recently, nearly all experts would have responded with a stubborn “yes.” They used to think that the Fed and the Treasury, along with their cohorts overseas, could simply spend, print and pump as much money as needed to avoid another global meltdown.

Now, though, they’re not so sure. And some astute analysts are saying the true answer is a flat “no.”

I’ll tell you who in just a moment. But first, I want you to remember one thing: Over the last two weeks, I’ve shown you precisely how to achieve maximum protection from such a disaster. I gave you 5 ETFs for Protection in Another 2008 and my 7-Step Portfolio Protection Strategy.

Today, I’m taking this story one step further. I will show precisely why you can’t rely on anyone else — especially the government — to provide that kind of protection for you. If you want it, you must build it yourself.

The Pundits Throw in the Towel

Let’s not forget who these experts are: They’re the same guys who swore on a stack of Bibles that the almighty Fed would always keep the economy afloat.

Now, however, Barron’s writes, “Based on what is happening in global markets today, central banks won’t be able to ride to the rescue this time.” The Telegraph declares that “the lifeboats are all used up.” And most seem to agree that the next big government rescue could fail — or even fail to materialize — for three reas

Reason #1. The central banks’ latest weapon of mass desperation — below-zero interest rates — could cause more fright that fight … and more market panic than market rally.

Reason #1. The central banks’ latest weapon of mass desperation — below-zero interest rates — could cause more fright that fight … and more market panic than market rally.

Barron’s put it succinctly…

“Negative interest rates are a sign of desperation, a signal that traditional policy options have proved ineffective and new limits need to be explored.”

Reason #2. Instead of prodding banks to make more loans, below-zero interest rates will kill bank profit margins and prod banks to make fewer loans. Instead of easy money, they’ll bring tighter money.

Reason #3. Bank share prices will plunge, weaker banks will go bankrupt and the whole rescue scheme of recent years will backfire.

How big is that scheme? Brace yourself for the answer …

Since the Big Bang of all financial disasters — the collapse of Lehman Brothers on Sept. 15, 2008 — central banks have been expanding their rescue mission at a mind-boggling pace, creating a whole new universe of monetary excess.

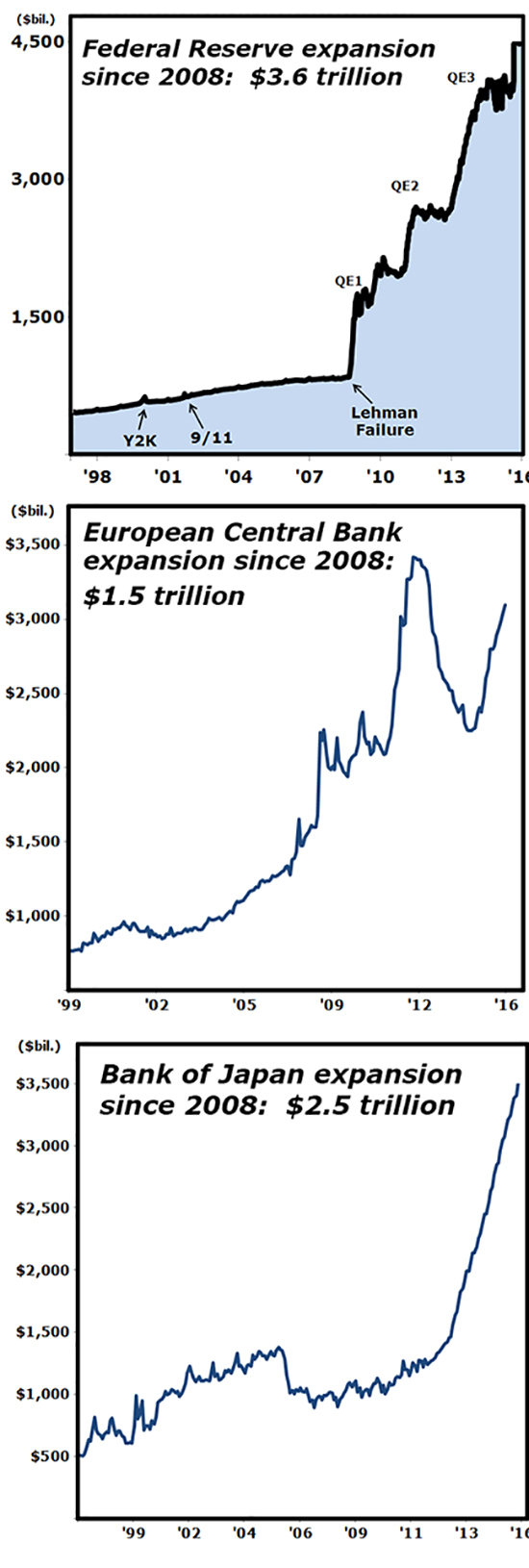

The U.S. Federal Reserve went stark, raving mad, abandoning any semblance of restraint, and expanding its assets by a mammoth $3.6 trillion.

Two prior emergency expansions — on the eve of the Y2K turnover and immediately after the terrorist attacks of 9/11 — were minuscule by comparison.

And in just a matter of weeks, all the rule books of Fed policy, written by generations of Fed chairmen, were dumped into the Potomac River.

A set of completely new rules was created on the fly.

And quantitative easing (QE) was born.

The European Central Bank immediately followed in the Fed’s footsteps, expanding their assets by $1.5 trillion.

At one point, they also tried massive lending to banks in a different form, which temporarily replaced their central bank expansion. But now they’ve resumed their quantitative easing, throwing in below-zero interest rates for extra measure.

The Bank of England, although smaller, was equally aggressive, expanding its balance sheet by $435 billion since 2008.

After the Lehman Brothers failure, their money printing went ballistic; and during the European debt crisis, it went ballistic again.

Now it’s on hold temporarily. But the $435 billion in new money is locked in place with no sign whatsoever of retreat.

If you think all of the above is crazy, wait till you see what the Bank of Japan has done:

Since the Lehman Brothers blow-up in 2008, the BOJ has expanded its balance sheet by a whopping $2.5 trillion.

Adjusted for the smaller size of Japan’s economy, that’s the equivalent of a $9.4 trillion expansion in the United States, or more than 2½ times more than the Fed’s.

Even excluding all the other central banks of the world, this big-bang expansion is absolutely unprecedented in all of recorded history:

The Fed’s $3.6 trillion … PLUS … the Bank of England’s $435 billion … PLUS … the European Central Bank’s $1.5 trillion … PLUS the Bank of Japan’s $2.5 trillion … add up to a grand total of more than 8 trillion dollars in monetary expansion just since the Lehman Brothers big bang.

This $8-trillion monster is what had been fueling all the government rescues since the 2008 debt crisis.

This is what’s not working anymore.

This is fundamentally what the experts are now so worried about.

And this is why you need your own portfolio defenses.

Whatever you do, don’t get caught off guard.

Good luck and God bless!

Martin

Dr. Weiss founded Weiss Research in 1971 and has dedicated the past 40 years to helping millions of average investors find truly safe havens and investments. He is president of Weiss Ratings, the nation’s leading independent rating agency accepting no fees from rated companies. And he is the chairman of the Sound Dollar Committee, originally founded by his father in 1959 to help President Dwight D. Eisenhower balance the federal budget. His last three books have all been New York Times Bestsellers and his most recent title is The Ultimate Money Guide for Bubbles, Busts, Recesssion and Depression.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair