Timing & trends

Assets, including illiquid ones like art, cars and houses have become volatile. A Picasso that traded for GBP 18.9 million in January had traded for GBP 28 million in 2013.

And then there is the mania in Vancouver. Nice house with a view into English Bay lists for $7 million and trades for $9 million.

ECB/Draghi Band-Aids Not Able To Stem Bubble Bursting On Europe’s Zombie Banks

ECB/Draghi Band-Aids Not Able To Stem Bubble Bursting On Europe’s Zombie Banks

Stock Market Vulnerable To 15%+ Plunge

Oil Price Should Retest Lows At US$26/b Over Next Two Months

What’s Inside:

-

The weakness worldwide in the banking sector as central banks move further to negative interest rates will depress bank earning even further which will result in falling world stockmarkets.Intermarketmargincalls arelikely.

BUY Favourite Names On This Next Phase Of Market Weakness!

-

Maison Universe High Impact Drilling Watch List

-

Terminating Coverage:

Long Run Exploration Ltd. (LRE)

LRE shareholders approved the sale of the company to

Calgary Sinoenergy Investment Corp. on Feb/29, 2016.

Petromanas Energy Inc. (PMI)

PMI sold its key asset in Albania to a subsidiary of Royal Dutch Shell plc., and on March 14, 2016 shareholders approved a special distribution of most of the funds.

Sterling Resources Ltd. (SLG)

SLG has entered a recapitalization agreement with debt holders and as a result value creation has been delayed.

-

Research Updates:

-

Gran Tierra Energy Inc. (GTE)

-

Pengrowth Energy Corporation (PGF)

-

Top Picks: No Picks This Month – Downside Risk High

-

Recommended Buy List

-

Coverage List

Oil prices have shown signs of life over the past few weeks, as production declines in the U.S. raise expectations that the market is starting to adjust. As a result, Brent crude recently surpassed $40 per barrel for the first time in months.

A growling list of companies are capitulating, announcing production cuts for 2016. Continental Resources, for example, could see output fall by 10 percent. A range of other companies have made similar announcements in recent weeks. The energy world has been speculating about declines from U.S. shale, and the declines are finally starting to show up in the data.

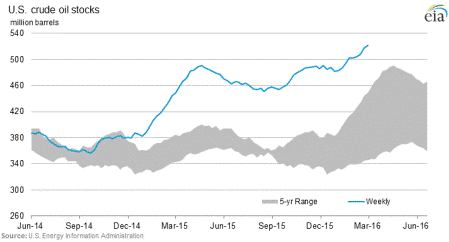

Despite the newfound optimism that oil markets are balancing out, crude oil sitting in storage is at a record high in the United States. Energy investors may have preferred to focus U.S. production declines, or the fall in gasoline inventories in early March, but meanwhile crude oil stocks continue to signal that oversupply persists.

Crude stocks rose once again last week, hitting yet another record of 521 million barrels. Storage levels at Cushing, Oklahoma, an all-important hub where the WTI benchmark price is determined, have surpassed 90 percent of capacity. U.S. output may be starting to decline, but it is doing so at a painfully slow rate.

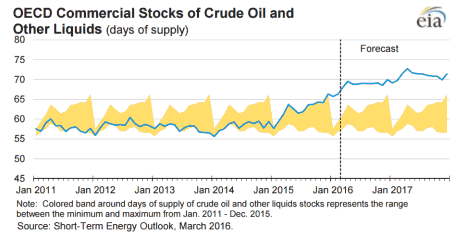

It isn’t just a U.S. problem. Crude oil storage levels continue to climb around the world. Commercial stocks in the OECD surpassed 3 billion barrels in 2015. The EIA sees oil storage in the OECD rising to 3.24 billion barrels by the end of this year. It doesn’t stop there. Storage levels rise a bit more next year, hitting 3.30 billion barrels by the end of 2017.

That is a staggering forecast that should scare any oil investor. It also suggests that the price rally over the past few weeks, which has pushed oil prices up around 40 percent since early February, could be fleeting. There is evidence that suggests the rally was driven by speculators closing out short bets on oil, after accruing net-short positions at multiyear highs in recent months. In early March, hedge funds and other major investors shed short positions at the fastest rate in almost a year. The rally, then, hinged on the sudden shift in sentiment from oil speculators.

The underlying fundamentals, however, have not appreciably changed in recent weeks. U.S. oil production is declining, but more or less at the same pace that it has for months.

On the other hand, rising inventories undercut the notion that the market is adjusting. As a result, as the short-covering rally reaches its limits, and the markets digest the fact that the world is still oversupplied with oil, prices could fall once again.

The problem, as mentioned above, is that inventories could continue to rise around the world through the rest of this year, if EIA data is anything to go by. Oil prices may have rallied in recent weeks, but the EIA was more pessimistic in March than it was in February. The EIA says that global storage levels could rise by 1.6 million barrels per day (million b/d) in 2016 and by another 0.6 million b/d in 2017. Those predictions are higher than the EIA’s February estimate.

“With large global oil inventory builds expected to continue in 2016, oil prices are expected to remain near current levels,” the EIA concluded in early March. The EIA lowered its price forecast for Brent by $3 per barrel, expecting it to average $34 for the year. 2017 does not look much better: the EIA sees Brent prices averaging just $40 per barrel next year, a whopping $10 lower than what the EIA predicted last month. That could mean prices stay below $50 per barrel through 2017.

Price forecasts are always wrong, and often wildly off the mark. While it is difficult, if not impossible, to accurately predict price movements, especially a year or two out, it is impossible to argue with the sky-high levels of oil sitting in storage. Even if U.S. oil production continues to decline, the greater than 500 million barrels of oil inventories – a record high – need to start declining in a substantial way before the oil markets will see a sustained rally.

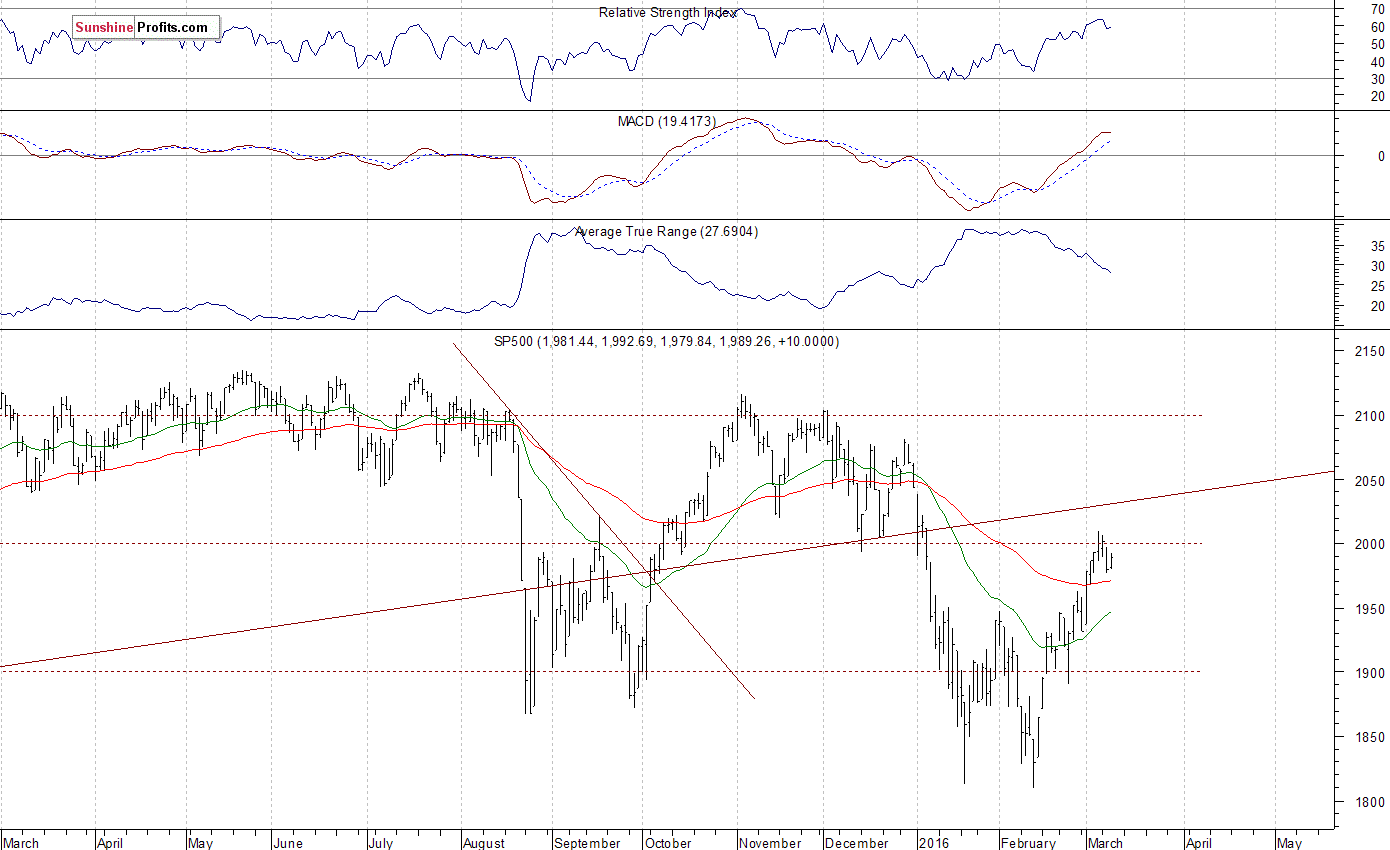

Sent to subscribers on March 17, 2016, 6:56 AM.

Briefly: In our opinion, speculative short positions are favored (with stop-loss at 2,050, and profit target at 1,900, S&P 500 index).

Our intraday outlook is bearish, and our short-term outlook is bearish, as we expect a downward correction or short-term uptrend’s reversal at some point. Our medium-term outlook remains bearish, as the S&P 500 index extends its lower highs, lower lows sequence. We decided to change our long-term outlook to neutral recently, following a move down below medium-term lows:

Historic day in the coal sector yesterday. With one of the world’s largest producers saying that it may soon disappear completely.

The news comes after Peabody missed payment Tuesday on $71 million in interest due on $1.65 billion worth of bonds. The company has now entered into a 30-day grace period to make the payments.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair