While the market has been rising steadily in the last month, I have been looking to raise cash.

related:

Larry Edelson on How Markets Outwit You

The late Richard Russell used to observe, “Stocks are going to great valuations.”

Have always enjoyed the line, especially when nicely timed. The Transports had been declining in the first part of 2015 when we used the old Dow Theory for the first time. The non-confirming signal occurred in May and we concluded that the bull market was ending. Our research on the curve and spreads indicated trouble after July. In July we concluded that the bear market had begun.

The hit into January accomplished all of the right technical readings and we thought the rebound could run to around March. That the likely leaders would be base metal miners helped with the March seasonality. And the materials sector became very overbought. We have been taking money off the hot tables.

As we have been noting, the NYA set the big Rounded Top last year. This year’s rebound has been looking somewhat like the second rebound in the 2008 bear market. Our March 17th Pivot concluded that the rally had a couple of weeks to go.

The NYA reached the 200-Day ma at 10281 on March 30. This has been the high for the move and the broad index has been following the moving average down.

Adding to the measures of exuberance, the NYA has registered a Weekly Inverse Springboard – similar to that on the big rebound into May 2008. The Inverse Springboard is a sell in a generally declining market. The Springboard is a buy on a dip in a rising market. The last one on the bull market registered in October 2014.

We like the symmetry and yesterday’s ChartWorks noted the Inverse Springboard Sell in a number of important indexes.

Of considerable importance, this rally has been similar to the key rebounds that failed and formally confirmed a bear market. Outstanding examples completed in October 1973, August 1937 and April 1929.

As the ChartWorks noted, the first week with a lower low marks the completion of this rally.

This week, the Sensational Season is shining upon the Biotechs as the IBB jumped out of the dull trading range. Yesterday’s 6 percent pop has moved the Daily RSI up 9 points to 67, which is accomplishing an outstanding swing in momentum. The limit could be found at the 70 level.

Credit spreads have resumed widening, which could curb further advances in the banks and financials.

Source: Zero Hedge

related: Larry Edelson on How Markets Outwit You

Link to April 8, 2016 Bob Hoye interview on TalkDigitalNetwork.com:http://talkdigitalnetwork.com/2016/04/us-fed-heads-still-think-theyre-great/

Listen to the Bob Hoye Podcast every Friday afternoon at TalkDigitalNetwork.com

In our article dated Dec 13, 2015 titled “What OPEC decision means to Oil and $USDCAD” we wrote about the oil revolution; the rise of shale oil producers from North America and the OPEC cartel trying to fight against this threat by flooding the market with conventional oil to fight for market share and also drive out the higher-cost shale rivals. This strategy by OPEC has created an over-supplied condition in the oil market and has caused oil price to plunge 60% in just a little more than a year from $100 in the middle of 2014 to $40 in December 2015. We said in the December article that as long as there’s no end in sight in this price war, oil is going to continue to slide until OPEC has no choice other than to take action to reduce the glut.

In our article dated Dec 13, 2015 titled “What OPEC decision means to Oil and $USDCAD” we wrote about the oil revolution; the rise of shale oil producers from North America and the OPEC cartel trying to fight against this threat by flooding the market with conventional oil to fight for market share and also drive out the higher-cost shale rivals. This strategy by OPEC has created an over-supplied condition in the oil market and has caused oil price to plunge 60% in just a little more than a year from $100 in the middle of 2014 to $40 in December 2015. We said in the December article that as long as there’s no end in sight in this price war, oil is going to continue to slide until OPEC has no choice other than to take action to reduce the glut.

In December 4, 2015 OPEC annual meeting, speculation started to emerge that OPEC members might attempt to cap production volume to prevent further price slide. Smaller OPEC member such as Venezuela has voiced concern over the oil price and wanted the cartel to take action to stabilize the market. However, with Iran soon to be free from the oil embargo at the time of the meeting, Saudi Arabia as the biggest oil producer in OPEC wanted to wait and see and unwilling to make a move. The failure to reach an agreement caused oil price to spiral down further from the already low price of $41 in December 2015 to just $28 in early February 2016 before the bleeding finally stopped.

The catalyst for the bounce came from a meeting in February 16 in which Saudi Arabia, Russia, and several key OPEC members agreed to freeze oil output production at the January level, if other suppliers follow suit. This news is what the market wants to hear, and oil has continued to recover from $28 low in February and now back to $42 in April (50% increase). There will be another summit this coming Sunday April 17 at Doha to secure commitment from a wider range of countries both inside and outside the OPEC cartel to freeze output production.

Oil analysts are skeptical that freezing output production at the January level will solve the oil glut for several reasons. First of all, freezing production output at January level means it is just maintaining the existing high production output, instead of reducing the production volume. Secondly, country like Iran whose economic sanction is recently lifted has also indicated they would not join the freeze and intend to raise production output from 3.1 million barrels to 4 million barrels a day. Last but not least, even if agreement to freeze production output can be reached from a wider range of producers and oil rally extends, this will encourage new supply from the US shale drillers and give pressure back to oil price.

Despite the limited impact of the production freeze to reduce the global supply glut, oil price still reacted positively due to the overextended selloff. At minimum, the summit is a positive sign as it demonstrates that oil participants are no longer indifferent about what happen in the market. If participants can come out from the summit this Sunday with a broader agreement to freeze output or some other measures, oil rally may continue. However, if the meeting falls apart, then oil could retrace back the rally from the February low.

Similar to USD Index, Oil completed the cycle from 2014 peak and it is currently doing the biggest correction if not already formed the weekly low. As shown in the chart above, Oil has broken above the 2014 weekly trend line channel and it has also made a sequence of higher high. Thus, regardless what the outcome of the Doha meeting is, the path of least resistance for Oil is to the upside. Even if the meeting does not produce good result and oil is pulling back, it is likely still to get support from the broken weekly channel

If you enjoy this article, you are welcome to read other technical articles at our Technical Blogs and check Chart of The Day. For further information on how to find levels to trade Oil, Gold, or other commodities, indices, and forex using Elliottwave, take our FREE 14 Day Trial. We provide Elliott Wave chart in 4 different time frames, up to 4 times a day update in 1 hour chart, two live sessions by our expert analysts, 24 hour chat room moderated by our expert analysts, market overview, and much more! With our expert team at your side to provide you with all the timely and accurate analysis, you will never be left in the dark and you can concentrate more on the actual trading and making profits.

With the Dow surging along with the dollar, today 3 veterans share crucial updates on major markets.

With the Dow surging along with the dollar, today 3 veterans share crucial updates on major markets.

Here is a portion of today’s note from Art Cashin: Conflicts And Causes In Oil Inventories – Last night, my good friend and fellow trading veteran, Jim Brown over at Option Investor, wrote this on crude inventories:

Tomorrow is all about earnings and oil.

also:

Demand for lithium — the hottest commodity on the planet and the only commodity to show positive price movement in 2015 — is poised to continue on its upward trajectory, becoming the world’s new gasoline and earning the moniker of “White Petroleum”. And the battle for market share in and around this commodity has everyone from major tech players to trend-setting investor gurus vying for a foothold.

Driven by the rise of battery gigafactories and game-changing Powerwall and energy storage businesses, the world now finds itself at the beginning of a lithium super cycle that is all about securing new supply, much of which is poised to come from lithium superstar Argentina.

We have Tesla in the far corner, building its battery gigafactory in Nevada, for which it needs tons of lithium at a reasonable price, and just last week Tesla announced its plans for the Model 3, which has already hit over 300,000 pre-orders. To give you an idea of just how meaningful this is, Tesla produced less than 50,000 cars last year. Elon himself mentioned during the unveiling that Tesla will be gobbling up much of the world’s lithium supply with plans to produce 500,000 EVs per year. “In order to produce a half million cars per year…we would basically need to absorb the entire world’s lithium-ion production.” Remember – this is one man, one company. Tesla’s soon-to-be-completed gigafactory will produce more lithium-ion batteries than the rest of the world combined.

And opposite Tesla, we have some other major players shifting gears that will affect the lithium space.

Chinese billionaire Jia Yueting is stepping onto Tesla’s playing field with its own electric car start-up, Faraday Future, and Apple is planning one too, by 2019. Through its Alphabet holding company, Google is also getting into the game with plans for a self-driving car.

They are fighting it out not only to be the first to capture the most electric vehicle market share and the best engineers, but they are getting down to the core of this arena, which is lithium — the key element that will make it all work.

This is D-Day for lithium miners, and it’s all about new entrants to a space that is about to change exponentially. Big investors are definitively standing up and taking notice — and even jumping into the game.

One of Canada’s most noteworthy investors in the mining sector, Frank Giustra, is the latest to see lithium for what it is — the single-most valuable commodity of our tech-driven future, and one that is already in short supply.

The investor extraordinaire with a focus on big mining deals has thrown his support behind Lithium X which is exploring in the key “Lithium Triangle” area of Argentina and is the largest land holder in Nevada’s Clayton Valley, the only producing lithium area in the entire United States. Lithium X has over 15,000 acres in Clayton Valley, near Albermarle’s Silver Peak mine, the only American lithium producer right now, and about three hours from Tesla’s gigafactory.

“Right now, there is a lot of ‘smart money’ getting in on the lithium land rush, and a mining legend like Giustra would never have been late to this party in Nevada — but the big attraction is our lithium plays in Argentina, which is ground zero for the commodity in South America,” Lithium X Chairman Paul Matysek told Oilprice.com.

“At the end of the day, Frank, likes to get involved in a project if he sees a massive shift in an industry’s fundamentals,” Matysek added. “Lithium — is certainly showing all the right signs!”

The fundamentals here are impressive, and the catalysts for lithium prices are spectacularly clear — all of which is pushing prices up and creating an aggressively competitive playing field that is likely to see a lot of acquisition talk.

There are plenty of reasons to be bullish about what Goldman Sachs calls the “new gasoline” that will fuel our technology-driven resource era.

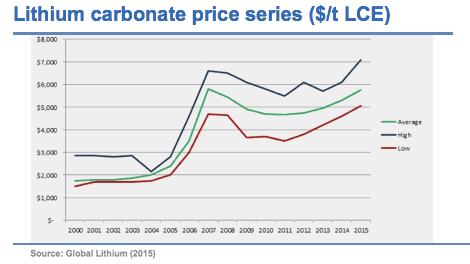

According to The Economist, the ”global scramble to secure supplies of lithium by the world’s largest battery producers, and by end-users such as carmakers”, among other things, has seen the price of lithium carbonate imported to China more than double just in November and December of last year alone, when it reached an amazing $13,000 per ton. Some contracts in China, according to Bloomberg, have seen over $23,000.

There is no denying that this is a euphorically tight market, with demand rising steadily and expected to spike drastically, and suppliers struggling to keep pace — which means that the door for new lithium supplies is wide open and this is now a fast-paced exploration and exploitation game.

And even without the battery gigafactories, a Powerwall and storage revolution or streets lined with electric vehicles — demand for lithium would still remain steady just to keep up with consumer electronics.

For the electric vehicle industry alone, Goldman Sachs predicts that for every 1 percent rise in EV market share, lithium demand will rise by 70,000 tons per year. Furthermore, Goldman Sachs predicts that the lithium market could triple in size by 2025 just on the back of electric vehicles.

The lithium that is currently being mined quite simply is not enough to put a dent in the projected demand dictated by our hunger for consumer electronics and the pending energy revolution. This means that the new market is all about new players.

Right now, most of the world’s lithium comes from Australia, China and the “Lithium Triangle” of Argentina, Chile and Bolivia. In North America, Nevada is the only player in this game, but more to the point, the U.S. state has the best lithium there is to have — lithium found in the brine.

Lithium sourced from brines, or salt water, is the most cost-effective on the market, and sourcing enough of it right at home would be a coup for all sides in the battery, storage and EV game.

And while lithium has traditionally been controlled by a handful of major global suppliers, spiking demand is changing this landscape drastically.

The four companies that currently control the lithium space — Albermarle (NYSE:ALB) in Chile and Nevada; SQM (NYSE:SQM) in Chile; FMC (NYSE:FMC) in Argentina; and Sichuan Tianqi in China — are about to make way for the new entrants.

And when it comes to new entrants, the biggest market share will be scooped up by those who can come up with the most lithium sourced from the brine. That means getting in on the new game in Nevada, but perhaps more importantly, securing positions in the bigger venues, particularly in Argentina.

Within the Lithium Triangle, it’s all about Argentina right now. Chile is not granting any new concessions, and opposition in Bolivia has led to a suspension of lithium mining. Argentina has recently announced a deal with creditors to repay debt stemming from the country’s 2001-2002 default, paving the way for Argentina’s return to global financial markets.

And the Argentina lithium rush is already in full swing, with miners eyeing resources of up to 128 million tons of lithium carbonate.

Investors have been pouring into this sector, according to Argentine Mining Secretary Jorge Mayoral, who recently noted that “all the big auto makers have been present in Argentina trying to get a foot in lithium development”, including Toyota, Mitsubishi and Posco.

For those who come up with the next supply, the industry will come right to them, and the sniffing around has already begun in full force.

related:

Experience has taught me to raise cash as the market rises.

Cash does not appreciate, but it offers opportunities when the market falls.

Madam, prices will fluctuate.

While the market has been rising steadily in the last month, I have been looking to raise cash.

related:

Larry Edelson on How Markets Outwit You

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

A sane voice in a scrambled investment world.

~ Ed R.

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair