Gold & Precious Metals

Warren Buffett doesn’t like gold. Neither does Dennis Gartman. That settles it for us; gold must be a table-pounding buy.

In this year’s annual letter to Berkshire Hathaway shareholders, Warren Buffett scorned gold as an asset that is “forever unproductive.”

“[Gold] will never produce anything,” he wrote. “Gold has two significant shortcomings, being neither of much use nor procreative.”

Buffett’s statement is literally correct, but it has two significant shortcomings, being neither of much use nor insightful. No one holds gold hoping it will produce something. They hold gold because no one can produce it. Precisely for this reason, mankind has considered gold the ultimate money for several thousand years…and it has performed this role with meritorious distinction.

Gold’s appeal waxes and wanes, of course, depending upon the monetary environment in which it resides. But the less folks trust the cash in their pockets, the more they trust gold…and that’s exactly what’s been happening throughout the Western world for more than a decade.

Therefore, despite gold’s “significant shortcomings,” it has delivered a much higher return during the last 14 years than the “useful” and “procreative” Berkshire Hathaway. As the chart below shows, the “rolling 10-year return” of gold has been higher than that of Berkshire Hathaway since January 2008.

In other words, an investor who purchased gold at any time after January of 1998 would have received a higher investment return over the following 10 years than an investor who purchased Berkshire Hathaway. That seems like a fairly useful investment result.

But Buffett is the investment genius sans pareil. We aren’t. He knows gold is a losing bet. We don’t. But here’s the good news: You don’t need to be a genius to buy gold. You can be an idiot. In fact, according to Buffett, you are.

“This type of investment,” says the Oracle of Omaha, “requires an expanding pool of buyers who, in turn, are enticed because they believe the buying pool will expand still further. Owners are not inspired by what the asset itself can produce — it will remain lifeless forever — but rather by the belief that others will desire it even more avidly in the future.”

Like Buffett, Dennis Gartman has also scorned gold recently. Unlike Buffett, Gartman has recommended buying gold from time to time — and even buys it for himself on occasion. But he recently notified the world that gold was a “Sell” and the he would no longer be “long of gold,” as he says in his bizarre version of English.

On December 15, the editor of “The Gartman Letter” announced, “I sold all gold in my personal account… Since the early autumn here in the Northern Hemisphere gold has failed to make a new high. Each high has been progressively lower than the previous high, and now we’ve confirmation that the new interim low is lower than the previous low. We have the beginnings of a real bear market, and the death of a bull.”

A week later, Gartman kicked the “yellow dog” again. “I expect equities will outperform gold [in 2012] without any question,” Gartman told the CNBC viewers. Unfortunately for Dennis, his “Sell alert” on gold happened to coincide with a brand-new “Buy alert” from Ben Bernanke and a few of the Fed Chairman’s counterparts around the globe.

As you may recall, last November the Federal Reserve and the European Central Bank (ECB), along with the Bank of Canada, the Bank of England, the Bank of Japan and the Swiss National Bank announced “coordinated actions…to provide liquidity support to the global financial system.”

These banks have kept their promise. They have all ramped up their money supplies since November 30.

The day this announcement crossed the wires, we observed:

A new phase of monetary destruction is underway…All the largest central banks are committing to printing money in some way, shape or form.

Who knows what’s next? Probably, we can look forward to a new era of clandestine bailouts, backdoor lending facilities with inscrutable acronyms and global monetary game-playing that will look a lot like a massive money-laundering operation.

Perhaps someone should notify the authorities. The Fed is engaged in highly suspicious, un-American activities.

As it turns out, the Fed’s suspicious activities are merely part of a global crime syndicate — a worldwide counterfeiting ring. The following chart, courtesy of James Bianco at Bianco Research, tells the tale.

“Bianco’s chart,” observes Tim Price, Director of Investment at PFP Wealth Management, “shows the extent to which the eight largest central banks (China, the ECB, the US, Japan, Bank of England, Banque de France, Swiss National Bank, and Germany’s Bundesbank) have allowed their balance sheets to explode, in a desperate attempt to compensate for banking and private sector deleveraging since the debt crisis began. The Big 8 central banks now account for the equivalent of one third of world stock market capitalization.”

“If the basic definition of quantitative easing (QE) is a significant increase in a central bank’s balance sheet via increasing banking reserves,” Bianco remarks, “then all eight of these central banks are engaged in QE.”

True statement…which means that as long as the line on the chart above continues soaring higher, the precious metals are a “Buy”… no matter how frequently and self-assuredly Buffett and Gartman call it a “Sell.”

The “mother” of all gold bull market lives and it “ain’t over until I say its over”.

I received this email from a 40-yr. Wall Street trader right after the “flash crash” in gold last week:

Hey Peter

Funny thing happened the other day, Nadler went bullish on gold.

I said, “I’M DEAD”

LANCE JORDAN

While I suspect I’m not the only one in the world who wishes Crocodile Dundee wasn’t just kidding, it was funny that the “Tokyo Rose” of gold had once again thrown out a hedge to cover his decade-long horrifically wrong forecasting record like he does every once and awhile when gold gets far away from his usual dribble, only to see the flash crash occur. Sure enough, he is back to his only usually reliable anti-gold self so take comfort in the fact that the greatest contrarian gold signal of all-time is back where he belongs.

I’ve played this video for quite some time now to remind the very small army of us who have enjoyed virtually the entire ride up in gold that we’re at war with most of the financial industry and the media that follows it. They hate gold and what it stands for and come out of their foxholes every so often during these nasty, but rather short-lived corrections. They did so late last year when gold was more than $100 below where it is now, only to see it rally $200+ in just two months.

Nothing has changed (not even their spiel) fundamentally and I plan on using the cash I’ve built up of late to go back into several positions and new ones.

For me, I shall remember this belief each time the airwaves are filled in the near-term with yet another wave of anti-gold rhetoric:

GOLD IS GOING TO AN INFLATED-ADJUSTED ALL-TIME HIGH BEFORE IT’S ALL SAID AND DONE!

Todd Market Forecast for Monday March 5, 2012

Available Mon- Friday after 6:00 P.M. Eastern, 3:00 Pacific.

DOW – 15 on 600 net declines

NASDAQ COMP – 26 on 350 net declines

SHORT TERM TREND – Bearish (change)

INTERMEDIATE TERM TREND – Bullish

A projected attenuation of Chinese growth and renewed concerns about Greece caused a Dow drop of as much as 90 points in the early going, but about 2 hours into the trading day, the market began to come back.

This has been the pattern for the past few months. It has been a winning trade to buy into intraday weakness. One of these days that trade isn’t going to work anymore.

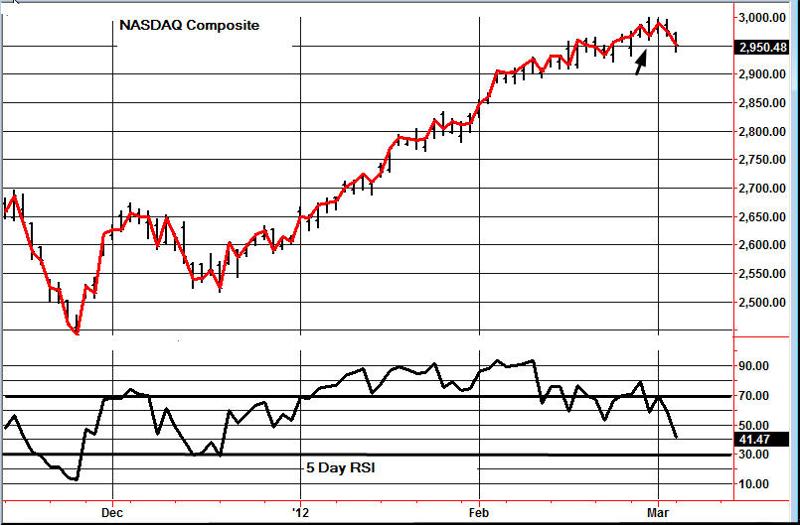

Today the NASDAQ Composite closed below a previous low (arrow) for the first time since mid December. The same is true for the S&P 500. For this reason, we will move to a short term sell. If this index decides to turn and move to another high, then we will have to move back to a buy.

TORONTO EXCHANGE: Toronto got whacked pretty good, down 119 points.

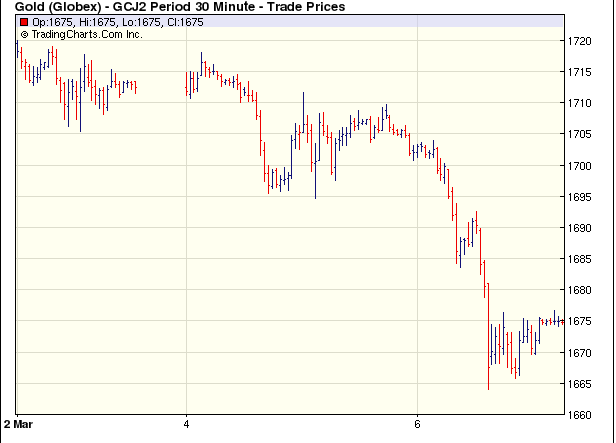

GOLD: Gold was down 15 intraday, but manage to claw its way back. It was still down for the session.

BONDS: Bonds were down marginally.

THE REST: The dollar was down just a bit. Not much influence on gold, copper and silver which were lower and crude oil, which was higher.

BOTTOM LINE:

Our intermediate term systems are on a buy signal.

System 2 traders are in cash. Stay there on Tuesday.

System 7 traders sold the SPY at 136.86 for a loss of .07, essentially break even. Stay in cash on Tuesday.

NEWS AND FUNDAMENTALS:

The services ISM number was 57.3, better than the expected 56.0. Factory orders dropped 1.0%, better than the consensus 1.6% drop. There are no important releases scheduled for Tuesday.

————————————————————————————–

We’re on a sell for bonds as of December 21.

We’re on a sell for the dollar and a buy for the euro as of January 18.

We’re on a buy on gold as of Feb. 21.

We’re on a buy on silver as Feb. 21.

We’re on a buy for crude oil as of Feb. 13.

We’re on a buy for copper as of December 20

We’re on a buy for the Toronto Stock Exchange TSX

We are long term bullish for all major world markets, including those of the U.S., Britain, Canada, Germany, France and Japan.

#1 Timer of the Year

Gold timing was rated # 1 for 1997 and # 2 for 2006. Late word! We were rated # 1 for 2011.

We were # 1 in long term stock market timing for the years 1998 and 2004 and # 4 in 2010.

To subscribe to the Todd Market Forecast go HERE

The Gold Report: The Global and Mail reported that more than 50 private-equity mining deals were struck in Canada in 2011—more than in any other sector. Why is private equity pouring venture capital into junior mining plays faster than any other Canadian business sector?

Stephen Taylor: The important thing is that private equity funds have the patience and the experience to take the long-term view that’s required with development-stage mining companies. There’s been a growing dysfunction in the U.S. initial public offering market for small-cap companies and development-stage enterprises of any type. It has led to depressed valuations. It’s not surprising that managers of private equity funds have the patience and see some bargains and are jumping into the sector.

TGR: Most of the deals involved minority positions, not takeovers. Why?

ST: That is really the best way to do deals as a private equity investor. These firms are looking to partner with or back experienced management teams. Experienced management teams are increasingly reluctant to cede control to an outside firm that doesn’t have real expertise in the mining sector. Trying to seek majority control would be a mistake.

TGR: What was the performance of The Taylor Fund in 2011?

ST: The fund, which has about $45 million under management, had a rough year. It was down about 20% in 2011 after a gain of 21% in 2010 and 96% in 2009. Since inception, it’s averaged just more than 26% a year versus about 9% a year for the S&P 500.

TGR: What’s the current industry weighting of the fund?

ST: It’s about 40% invested in energy, which is mainly oil and gas. Mining comprises about 30%. About one-third of the companies are in China, another third are in the U.S. and the final third are in Canada. The Canadian component includes many companies that have substantial operations in other parts of the world.

TGR: You previously told The Gold Report that you saw some “overdone selloffs in the resource space.” Was the selloff that occurred in the latter half of 2011 overdone?

ST: It clearly was. It seemed that 2011 was particularly fierce in the junior resource space. Sharp selloffs have been followed by quick bounce-backs. Miranda Gold Corp. (MAD:TSX.V) sunk from $0.67/share to $0.24/share at year-end but has since recovered somewhat. Silvermex Resources Inc. (SLX:TSX; GGCRF:OTC) went from about $1/share to $0.36/share at year-end, but is back up to $0.46/share.

TGR: Did the Taylor Fund add to existing positions or new positions as other investors were exiting junior mining plays?

ST: We were indeed. We were selective buyers on our core positions like Lumina Copper Corp. (LCC:TSX). We participated in the recent Anfield Nickel Corp. (ANF:TSX.V) financing. We want to be selective in our new additions, but we’re always going to be looking to quality management teams as one of our first conditions.

TGR: How long on average do you hold a position in junior mining?

ST: Typically, two to three years. Last year, we did lighten up in some names where the results weren’t what we had hoped. We lightened a bit on Fire River Gold Corp. (FAU:TSX.V; FVGCF:OTCQX) after some disappointing results.

TGR: You remain bullish on precious metals in general?

ST: As long as central governments around the world continue to print money and to telegraph a low to negative real interest-rate policy, precious metals are the place to be quite frankly. The next two quarters may be flat to sideways, but over the next two to three years precious metals are going much higher.

TGR: News about the Greek debt deal pushed the gold price up recently. Was this just a short-term uptick?

ST: The Greek debt deal is the first of many as other countries around the world will ultimately be forced to restructure their obligations as well. All of these will contribute to rising demand for precious metals and will support higher prices. It could occur in the next quarter or the next year, but I won’t be so bold as to make that distinction. I do know I want to be long on precious metals and that they’re going to be much higher over the course of several years.

TGR: Anfield and Lumina are nickel and copper plays. Do you see value in base metals?

ST: I do. There’s a long-term secular rise in living standards that will continue for a huge portion of the world’s population in China, India and Brazil. As this process grinds forward over the next 10–30 years, regardless of short-term disruptions, there will be an inevitable increase in demand for base metals. Existing deposits also continue to be depleted. As owners of some of the largest undeveloped base metals projects in the world, Anfield and Lumina are going to be well positioned.

Lumina is one of many Ross Beaty–related companies with which we’ve been involved. He has a tremendous record at generating shareholder value. The company has done extensive drilling on the Taca Taca property in Argentina during the past couple of years. There has also been significant historic drilling done on the project. The deposit just gets bigger and bigger. It’s close to being the largest undeveloped copper deposit in the world, if it’s not already.

That’s going to be a very valuable resource to someone. The company has indicated that it’s going to put itself up for auction at some point in the next several months. Based on transaction prices for other undeveloped copper deposits, the ultimate sale price could be in the neighborhood of $1 billion, or about $20/share. I think Lumina will be acquired or bought out in 2012 at a price in excess of $20/share.

TGR: David Strang, who is president and CEO of Lumina, was also involved in the management teams of Global Copper, Northern Peru Copper, Lumina Resources and Regalito Copper, all of which were bought by bigger players. How long before Lumina gets a takeover bid?

ST: Within the next 6 to 12 months. It’s possible that an unsolicited, unexpected bid could emerge before then, but I believe the company will begin to actively solicit bids in the first half of 2012.

TGR: What does Lumina need to do before that happens?

ST: It just needs to continue to derisk the project. The largest elements have been done. Frankly, the deposit is so big at this point that I almost wish the company would explore creating a spin-off vehicle to hold a portion of it for further exploration and perhaps to sell down the road.

TGR: It’s an interesting story because it’s less than 100 kilometers from the Escondida Copper Mine owned and operated by BHP Billiton Ltd. (BHP: NYSE, BLT: LON, BHP:ASX) and Rio Tinto Plc (RIO:LSE). That certainly seems like a likely dance partner.

Anfield, which has essentially the same management group as Lumina, has a nickel laterite project in Guatemala. Anfield was assembled by Ross Beaty years ago and seems to work pretty well. Is Anfield a takeover target as well?

ST: I believe it is. This team has skin in the game. They have substantial personal investments in these companies. They also participated in the recent financing. As a side note, they also participated in the Lumina financing in November. I really respect that. It sends a very positive signal when management teams put up their own money and buy at prices that are close to what other investors paid.

TGR: What are some of the companies that you have positions in that are developing precious metals projects?

ST: We continue to be fans of Miranda. It has a number of irons in the fire and, ultimately, one or more of them are going to hit. It did a joint venture with Red Eagle Mining Corp. (RD:TSX.V) on the Pavo Real project in Colombia. I wouldn’t be surprised if Miranda continues to pick up projects in Colombia and elsewhere.

Red Eagle continues to drill Pavo Real. It has been able to attract some sophisticated, smart investors. I’ve heard that Ross Beaty and his group have a position slightly less than 10% in Red Eagle. That speaks volumes as to the quality of the group that Ken Cunningham, CEO of Miranda, and Ian Slater, CEO of Red Eagle, put together.

TGR: Red Eagle has two main projects, Pavo Real and Santa Rosa. Which one of those excites you more?

ST: The drill results from Santa Rosa were OK. Clearly, one hopes for a homerun. The potential for those in a place like Colombia always exists. However, I don’t play favorites. I will stand by the management team and not play geologist today.

TGR: You weren’t overwhelmed by the drill results from Santa Rosa?

ST: Don’t get me wrong. I was not disappointed by the Santa Rosa results. It’s just that I’d love to see a homerun and this was double.

TGR: Do you think it’s starting to look like a bulk tonnage target?

ST: It’s always a possibility. The company didn’t have any preconceptions. The point of the drilling program was to see what it had and which direction that would take it. It’s got some good potential there. Let’s see where the drill bit takes us.

TGR: Miranda has projects in Colombia, Nevada and Alaska. Which one is getting the lion’s share of the attention?

ST: It has good joint venture partners that are busy drilling away in Nevada, one of which is Agnico-Eagle Mines Ltd. (AEM:TSX; AEM:NYSE). But the attention going forward in terms of new developments could be additional land in Colombia. CEO Cunningham clearly has his eyes and ears open. It wouldn’t surprise me to see the company pick up some additional property there.

TGR: You mentioned Silvermex earlier. What are your thoughts on it?

ST: Silvermex continues to do a good job ramping up production at La Guitarra. It’s slow and steady. Its stock got caught in the selloff that we talked about earlier, but it’s trudging along.

I’m very bullish on silver. I believe that could outperform gold on a percentage basis over the next two to three years. Silvermex is a great way to play that trend.

TGR: What’s the next catalyst for that stock?

ST: It’s going to be either the silver price and the macro developments that drive that or further delineation of its plans going forward at La Guitarra. Silvermex is getting some good drill results in some high-grade areas. Everyone’s waiting to see where it wants to go.

TGR: Does Pan American Silver Corp.’s (PAA:TSX; PAAS:NASDAQ) purchase of Minefinders Corp. (MFL:TSX; MFN:NYSE) bode well for a company like Silvermex?

ST: Clearly, Silvermex could be a good acquisition target at some point. It’s a process that will continue into the years ahead, however.

TGR: You also have a position in Largo Resources Ltd. (LGO:TSX.V)?

ST: We have a small position. We like CEO Mark Brennan, Largo and vanadium. It had to do a bit of a dilutive financing to get its mine under construction. We may invest more in that name at some point, but we’re largely on the sidelines at the moment.

TGR: Do you have any final thoughts on the space for investors?

ST: My biggest worry for a lot of these development-stage companies is governmental risk. Governments and jurisdictions around the world may get greedy when faced with the pressure to restructure their financial obligations and debt. They may attempt to take a bigger piece of the pie. That’s a risk that’s always been part of the mining business, but investors should be particularly attuned to that over the next two to three years.

Stephen Taylor is chairman and CEO of Taylor Asset Management, a Chicago-based investment management firm focusing on small-cap domestic equities and emerging markets. He also serves as a portfolio manager for the Taylor International Fund Ltd., a small-cap equity fund. In addition to emerging markets, Taylor’s area of expertise includes private equity, restructuring and turnaround situations and both small- and mid-cap companies. He has considerable experience in the natural resources and finance industries in Canada and China.

Want to read more exclusive Gold Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Exclusive Interviews page.

Today billionaire Eric Sprott told King World News that a staggering 500 million ounces of paper silver traded hands during the takedown in the metals this week. Eric Sprott, Chairman of Sprott Asset Management, had this to say about what took place the day of the plunge in gold and silver: “I can only imagine it’s the same forces that for the last twelve years have been at work in the gold market, trying to keep the volatility very large on the downside. As you are aware, we hardly ever get days when you get an intraday $100 rise in gold. When we look back at what happened (on Wednesday) we saw huge sell orders in gold and silver.”

Eric Sprott continues:

“When I look at the silver market in particular, in a 30 minute span we had sellers of 225 million equivalent paper ounces, in a market that in one year the silver miners only produce 800 million ounces. So again, it’s the paper markets overwhelming the physical market. It’s stunning to me that on a day like Feb. 29th we traded 500 million ounces of silver.

No rational person could believe it had anything to do with the real market for silver….

Continue reading the Eric Sprott interview (scroll down) HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair