Analyst David Sadowski of Raymond James sees a lot on the horizon for uranium: a supply shortfall, escalating Asian demand and seasonality, to name just a few. As a former geologist-turned sellside analyst, Sadowski’s conviction in uranium’s bullish future is rock solid, and he urges investors to get exposure now, as prices in this sector can climb quickly once they’re set in motion. In this exclusive interview withThe Energy Report, Sadowski shares his favorite names that are set to deliver megawatt-size returns to investors.

COMPANIES MENTIONED: AREVA – BHP BILLITON LTD. – CAMECO CORP. – DENISON MINES CORP. – PALADIN ENERGY LTD. – RIO TINTO PLC – UR-ENERGY INC. – URANIUM ONE INC. – URANIUM PARTICIPATION CORP. URANERZ ENERGY CORP.

The Energy Report: David, how does your background as a geologist help you to see value and growth potential in mining companies?

David Sadowski: Defining ounces or pounds is not an easy business. If it was, there would certainly be far more economic deposits out there and metal prices would be a lot lower. Luck is involved, but most companies use systematic evaluations like geological surveys, drilling and other data to take a lot of the guesswork out of finding the next discovery. The ability to interpret these data is equally important, and it allows an analyst to make an independent determination on the growth potential of a project rather than just relying on what management is saying. In this way, I feel like having an understanding of how economic ore deposits form is essential to developing a meaningful forward-looking opinion, particularly on early-stage prospects. In my view that’s one of the most important tools for the successful analyst.

TER: You’re also clearly comfortable speaking with engineers and geologists at these companies.

DS: Yes, quite right. That’s a very important element to my role. You have to be able to speak the same language and understand what they’re doing on the ground, and that helps the analyst determine whether or not the company is headed in the right direction. It’s a key skill to have.

TER: I was also very curious about your transition to finance as a sellside analyst. You once had a responsibility to the companies for which you worked, but now your stakeholders are institutional and retail investors. What mental shifts did you have to make?

DS: As an exploration geologist, one is really focused on the rocks, sometimes even at the microscopic level, and that’s a much different scope of focus than that of a mining analyst. The financial and operational outlook for the company and its share price must always be on the analyst’s mind, and we’re not looking at companies in isolation, as a geologist might do. If you’re in the business of projecting where the commodity price is going, as I am for uranium, the scope of analysis is global and extends from government policy right down to whether we think a specific ore zone will be amenable to heap leach, for example. As you mentioned, first and foremost I look out for the interest of investors rather than the mining companies, and this responsibility demands even higher levels of objectivity, precision and rigor. It’s a constant challenge and that makes it an exciting and fulfilling role.

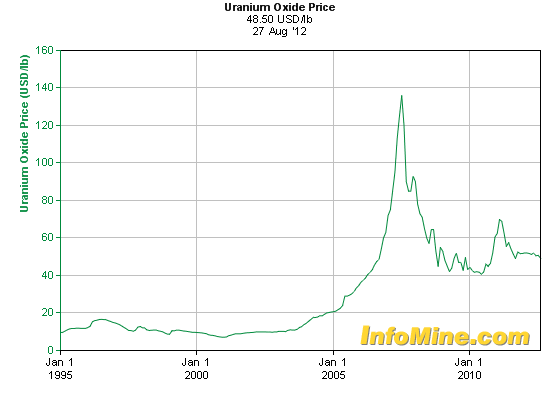

TER: Speaking of forecasts, uranium has dipped below the $50/lb level. I’m not sure, but I think these round numbers represent psychological support and resistance levels. What minimum price level must be sustained for small or near-term producers to maintain adequate margins?

DS: Well, if we look at existing operations, the majority of them would be losing money by selling their material at $40/lb. But there are a few exceptions, some of which are quite large producers, likeCameco Corp.’s (CCO:TSX; CCJ:NYSE) McArthur River or BHP Billiton Ltd.’s (BHP:NYSE; BHPLF:OTCPK) Olympic Dam. By our estimates, the only two potential projects that are likely to work in the $40/lb range of average realized price would likely be Cigar Lake and the expansion at Olympic Dam, but these are definitely major outliers. Cigar Lake is the second-highest grading deposit in the world, and it’s located in an excellent jurisdiction in northern Saskatchewan with significant existing infrastructure nearby. Meanwhile, Olympic Dam only works at that price because its uranium production is a byproduct of much more significant gold and copper output. When we look at the majority of additional projects needed to fill the looming supply gap, we think they need prices north of $70/lb to go forward. This is one of the key reasons why we feel the sub-$50/lb prices are unsustainable.

TER: What is your case for rising demand for uranium?

DS: We’re definitely bullish on the outlook for uranium. Although prices have softened in recent months, we have a very strong conviction that this trend is soon to reverse and investors should be exposed to uranium today. Beyond the high incentive prices for new supply that we just touched on, there are three primary reasons for our view. The first one is compelling supply/demand fundamentals. Next, there is the seasonality of uranium prices. And, most importantly, there are industry catalysts. Shall we take a look at each one?

TER: Please, go right ahead.

DS: After the Fukushima Daiichi accident last year, the nuclear industry has done some soul searching and decided to take a slower, more cautious pace in the construction of new reactors globally. But what many people don’t realize is that according to World Nuclear Association (WNA) data, there are nine more reactors in the planned and proposed category today than there were before the accident. Demand for nuclear power has remained resilient with ramping electricity requirements around the world, volatility in fossil fuel prices, energy supply security concerns and a global preference for carbon-neutral sources. The majority of this demand is from Asia. In fact, we estimate 82% of new capacity through 2020 will be built in only four countries—China, India, Russia and South Korea. Part of the reason for that is that state-owned utilities don’t face the same problems associated with other regions, like high upfront construction costs, widespread antinuclear public sentiment and lengthy regulatory timelines. So, this continued growth should support commensurate levels of demand for uranium for decades to come.

All of this demand begs the question, where is this uranium going to come from? Well, we don’t think supply is going to be able to keep up. Due to recent soft prices, many major projects have been delayed or shelved, like BHP’s Olympic Dam expansion, which I mentioned earlier, and Cameco’s Kintyre project,AREVA’s (AREVA:EPA) Trekkopje project and the stage 4 expansion at Paladin Energy Ltd.’s (PDN:TSX; PDN:ASX) Langer Heinrich mine. Even the world’s largest producer, Kazakhstan, may slow its pace of production growth. And, further complicating this issue is dwindling secondary supplies, like surplus government stockpiles, which in recent years have contributed 50 million pounds (Mlb)/year. But, that number is expected to halve over the next few years. We are projecting a three-year supply shortfall starting in 2014, and that certainly paints a very rosy supply/demand picture for investors.

Seasonality also favors uranium exposure today. Over the last 10 years, uranium spot prices have dropped on average $4/lb during the third quarter (Q3) but have rebounded by at least that amount in Q4, which is the strongest quarter of the year. This is often correlated with the annual WNA symposium, where many market participants sit down and hammer out new supply agreements. This year’s conference is going to be held September 12–14 in London.

Last but not least, there are several near-term catalysts that we think will start the price upswing. In Japan, all but two reactors are now offline, and there’s significant uncertainty and government debate about how many will eventually restart. As the world’s third-largest nuclear fleet, it has obvious implications for future uranium demand. For a variety of economic, political and environmental reasons, we think Japan will restart most of its reactors by 2017 with the first batch of reactors likely starting early in 2013. As more units start to return to service, it will provide additional confidence that the nuclear utilities in Japan are unlikely to dump their inventories into the market, which should support prices in the near-term.

Meanwhile in China, the government paused construction approvals for new reactors immediately after last year’s Fukushima accident. But with these safety reviews now successfully completed, they’re poised to start re-permitting new projects, and this should undoubtedly support increased uranium contracting. Let’s not forget that China will be far-and-away the largest source of nuclear demand growth for the foreseeable future. We expect a six-fold increase in installed nuclear capacity by the end of this decade.

The final major catalyst is the expiry of the Russian Highly Enriched Uranium (HEU) agreement to down-blend material from nuclear warheads into reactor fuel. This agreement has supplied the Western World for two decades but is due to conclude at the end of 2013. The Russians have repeatedly stated they’re not interested in extending this agreement, and we expect this to remove about 24 Mlbs/year or 13% from the global supply. That’s equivalent to shutting down the world’s largest mine, McArthur River, as well as all six operating mines in the U.S. That’s a massive impact. So, for these reasons we think prices are poised to turn here. We forecast prices to average above $60/lb in 2013 and north of $70/lb in 2014 and 2015 before settling to $70/lb in the long-term.

TER: These catalysts are spread out over the next 18 months, which is not a long time. Stock markets generally look ahead. So, why are prices lagging as they are?

DS: That’s a good question. I think what we’re seeing is a significant amount of uncertainty in the marketplace surrounding the availability of some material and who is going to be a near-term buyer. The purchasing side is largely comprised of nuclear utilities, which are usually very conservative and cautious. Based on our experience, they tend not to make rash moves and prefer to wait until all information is available before jumping into new sales contracts. For instance, they would rather have certainty on whether utilities in Japan and Germany are going to be selling any of their inventories before they start buying. This has led to very low volumes in recent months.

However, we’re already starting to see contracting activity pick up with major long-term deals signed by Paladin and one with the United Arab Emirates, both this month. And the WNA meetings are now only a few weeks away. This mounting activity could be just what the market needs for the metal price to shift to higher and more sustainable levels. And recent history shows that when the price moves, it can move really quickly as we saw in 2007, mid-2009 and late-2010 when the weekly uranium spot price jumped in increments of $5–10/lb.

TER: Could these current low prices force juniors to sell themselves to the larger companies, the producers?

DS: Well, we certainly expect further consolidation in the space. This industry is pretty much divided into the haves and have-nots. On one side we have state-owned utilities in countries like China and Korea, which essentially have zero cost of capital and the stated intention to build their exposure to uranium production. We also have large producers, like Cameco and Uranium One Inc. (UUU:TSX), that are cashed up and looking to grow. But, meanwhile many have-not companies have been under significant pressure in this current low uranium price environment with weak balance sheets and share prices. They could be looking to either sell assets or be taken over completely. Last year we saw Hathor get acquired by Rio Tinto Plc (RIO:NYSE; RIO:ASX; RIO:LSE; RTPPF:OTCPK). Extract Resources was bought by the Chinese nuclear utility, China Guangdong Nuclear Power Corp. (CGNPC). And, Mantra Resources was just purchased by Russia’s ARMZ Uranium Holding Co. These major deals could just be the start of another major trend of M&A in our view.

TER: I’m surprised that those acquisitions you just mentioned haven’t been a bullish signal to the market.

DS: We definitely think that they’re a bullish signal. It means that the larger companies are willing to lay out capital and put it at risk to build their future pipelines, which is a sign to us that they have confidence in where the uranium price is going and that they want to have higher production in the future to take advantage of those higher prices.

TER: David, everything you have said sounds to me like you believe that we are now in a legitimate value market in uranium equities. Is that the way you feel?

DS: Yes, definitely.

TER: What are your best ideas that you’re telling investors about?

DS: We prefer higher-quality, lower-risk names with minimal capital requirements. One of those is Cameco. It’s the world’s largest publicly listed uranium producer. Its market cap is over $8 billion (B). So that makes it very acceptable for many investors who have certain constraints and mandates to get exposure to the uranium space. It’s historically been the go-to name in the space. This company features strong production growth and a very low production cost. And it’s got a critical milestone coming up with the startup of its massive 50%-owned Cigar Lake project, which is due to come on-stream in late 2013. When fully ramped up, Cigar Lake is going to be the second-largest mine in the world. Cameco also has a very healthy balance sheet with access to about $4B in capital, and we wouldn’t be surprised if it puts that money to work by making an acquisition in the next 6–12 months.

TER: You have a $28 target price on Cameco, which does not represent huge upside gain from current levels. Is this what you think of as a safer, more conservative play?

DS: Yes, certainly. It reduces your risk via diversification into the other parts of the fuel cycle, such as conversion, refining and electricity generation, while you’re still getting some serious exposure to the uranium space. Even if we don’t project a really big return to our target, we think it’s a safe play and we recommend it. There’s less volatility in this one.

TER: What’s your next idea?

DS: The next one in terms of lower-risk names we’d recommend is Uranium Participation Corp. (U:TSX). Our target is $8, but we’ve got a Strong Buy on it because we think this is a great low-risk way to get into the space. It’s the world’s only physical uranium fund, and it’s designed to give investors pure-play exposure to the uranium price without any of the associated exploration, development or mining risks. The fund usually trades at slight premium to its net asset value (NAV), but currently it’s about 13% below NAV. We think it’s trading at a great entry point right now. Its current share price implies a uranium price of about $44/lb. If you’re like us and you think spot prices are unlikely to descend to those levels, then Uranium Participation offers good value today. If you’re an investor looking for more leverage, it may not be the one for you. But, I think if you’re going to buy a basket of equities this is one that you may want to include.

TER: What about investors who are willing to take on a bit more risk for greater returns?

DS: If you want more leveraged exposure to a potential spot-price rebound, we would consider a couple of other companies. The first one is Ur-Energy Inc. (URE:TSX; URG:NYSE.A), and we’ve got a $1.80 target and a Strong Buy rating on this one as well. It’s got an excellent flagship project called Lost Creek in mining-friendly Wyoming. We see production starting up there in the second half of next year. The project’s got low capital and operating costs and it’s scalable as well. Despite a somewhat small 1 Mlb/yr mine plan, the design of the backend of the Lost Creek plant should accommodate about 2 Mlb/year of uranium. It should be able to incorporate other satellite deposits, such as those acquired from Uranium One earlier this year as well as from Areva last month. Ur-Energy is also a catalyst story. It’s got only one final mine permit required before construction can start, and we have strong conviction that final approvals from the Bureau of Land Management (BLM) will come in by the end of September, particularly following release of the Final Environmental Impact Statement (EIS) last week—a major milestone. Currently Ur-Energy’s valuation is very attractive, trading at the lowest price/NAV (0.5x) of any of our covered equities, and we think receipt of that approval from the BLM could help close the gap towards developer valuations.

TER: Over the past four weeks it’s up 34%. I’m guessing that the near-term expectation of this BLM permit is the reason for this stock’s very high relative strength.

DS: I think so. I think we’re trending towards that date, and it’s become very important because this company has faced a little bit of difficulty over the last few years with some of its permitting timelines. It has missed a few targets, and that has really hurt the share price. And, yes, when this permit comes in we think it should be a great catalyst for the stock to re-rate towards developer valuations.

TER: Would you mention another name?

DS: Uranium One is another one of these stocks with a bit higher risk profile, but we think this risk is justified, and that is demonstrated by our higher target price. We are rating it Outperform with a $3.60 target. It’s got an excellent suite of low-cost in situ leach mines in Kazakhstan. It’s the world’s fourth-largest producer, and it’s also one of the fastest-growing producers out there as well. We modeled over 15 Mlb of production in 2015, up from only 10.7 Mlbs in 2011. Uranium One has the highest exposure to spot prices than any other company in our coverage universe, so it’s a great way to play this space if you’re a strong believer in uranium prices going upwards. Uranium One is 52% owned by ARMZ Uranium Holding Co., a strong partner, and that’s allowed it to access the Russian ruble bond market, which has been a boon for the company. It’s at a great entry point at current levels, with a 0.7x current price/NAV.

TER: David, Uranium One has a $2.3B market cap, and because of that there are a lot of mutual funds that could buy this stock. But it strikes me that its market value is a quarter the size of Cameco. Mutual funds could get some very significant upside from Uranium One.

DS: That’s a really good point to make. There are very few universally investable uranium equities. And by that I mean that there are very few publicly listed uranium equities in Canada, for example, that exceed that $1B market-cap threshold. Cameco is the biggest one at over $8B in market cap, and then you’ve got Uranium One, and Paladin Energy. And, beyond that there are very few places that you can put your money if you’re the type of investor that’s got the specific size and liquidity constraints or mandates, like you said, as a mutual fund. Those are pretty much the top three go-to places if you want uranium exposure.

TER: Is there one more you could mention? You have a Market Perform rating on Denison Mines Corp. (DML:TSX; DNN:NYSE.A). I’m interested in hearing about it because the company is once again an explorer.

DS: Denison Mines has a great management group lead by Ron Hochstein, and it has a 60%-interest in an excellent exploration project called Wheeler River, which is one of the best discoveries that we’ve seen in about a decade, perhaps trailing only Hathor’s Roughrider. It’s also one of the highest-grading uranium deposits that has ever been discovered. We think that the project could nearly double its resources at depth, along strike and on regional targets, and so we model 70 Mlbs at 12% target resources at Wheeler River. Denison also has a 22.5% ownership of the state-of-the-art JEB mill, which is one of only four active conventional uranium mills in North America. It’s unique in that it can process high-grade ores without having to downblend. That’s a strong competitive advantage. For those reasons, we think Denison is a good takeout target. Cameco and Rio Tinto’s faceoff for Hathor last year was probably their first battle in a larger war for the prime assets in the basin, and Denison has two of them. That said, we are cautious on the name today given limited visibility to production at its minority-held Canadian projects and in Mongolia and Zambia, as well as potential financing risk next year. We have a Market Perform rating and $1.80 target on the company.

TER: I have enjoyed meeting you very much, David.

DS: Thanks for having me George. It was a pleasure to speak with you as well.

David Sadowski has been a member of Raymond James’ mining team since June 2008, and now covers the uranium and junior precious metal spaces as a research analyst. Prior to joining the firm, David worked as a geologist in Central and Northern B.C. with multiple Vancouver-based junior exploration companies, focused on base and precious metals. David holds a Bachelor of Science in Geological Sciences from the University of British Columbia.

Want to read more exclusive Energy Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Exclusive Interviews page.

DISCLOSURE:

1) George S. Mack of The Energy Report conducted this interview. He personally and/or his family own shares of the following companies mentioned in this interview: None.

2) The following companies mentioned in the interview are sponsors of The Energy Report: Ur-Energy Inc. Streetwise Reports does not accept stock in exchange for services. Interviews are edited for clarity.

3) David Sadowski: I personally and/or my family own shares of the following companies mentioned in this interview: None. I personally and/or my family is paid by the following companies mentioned in this interview: None. I was not paid by Streetwise Reports for participating in this story.