Energy & Commodities

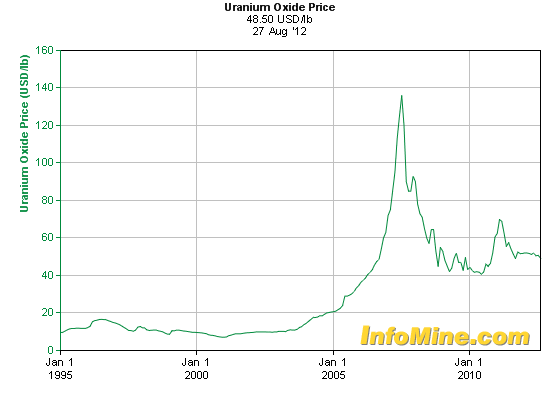

Uranium, Rare Earths, Graphite, Lithium & Cobalt. Take for example Uranium. At the end of March/2014 it was trading at $34, that’s a big discount from the $135 you can see on the chart below. With the coming Japanese reactor restarts on top of the long term Green movement’s opposition to nuclear power, supplies are getting tight.

The author of this thorough article also goes over the Rare Earth markets plus projects & companies in reliable political jurisdictions. With the anticipated boom in agricultural foodstuffs there is research too on what he expects to be a long-term boom in Fertilizer.

A really good read HERE – Money Talks Editor

Commodity returns vary wildly, as experienced resource investors can attest and Frank’s popular periodic table illustrates. This inherent volatility spells opportunity for the adept & strong minded who are prepared to look past the mainstream headlines to identify hot spots.

Frank’s global resources expert, Brian Hicks, CFA, identified four they believe are revved up for a resources boom. These areas’s are fertile ground for everyone from an aggressive trader thru to conservative investors. For a remarkable 60-100 year look at some of the commodities (Oil, Gold, even Real Estate) involved be sure to click HERE at some point – Money Talks Editor

1. Plenty in the Tank for Energy Stocks

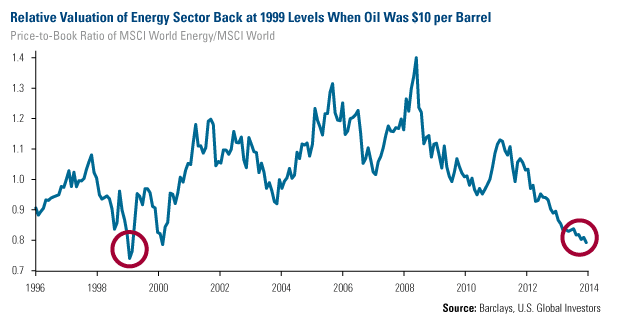

Because of the previously low expectations of global growth and oil demand, energy stocks have been shunned by investors and have languished in recent years. In fact, according to Goldman Sachs, oil equities held in the Energy Select Sector SPDR ETF have underperformed the broader market by 32 percent since 2008!

Global energy stocks have also suffered: In a comparison of the price-to-book valuations of the MSCI World Energy Index to that of the MSCI World Index, the ratio is at a level we haven’t seen since the late 1990s and early 2000s. Back then, crude oil plummeted to a very low price of $10 per barrel.

Today, with oil hovering around $100 a barrel and improved economic conditions in the U.S., energy stocks appear to be a tremendous bargain compared to overall stocks.

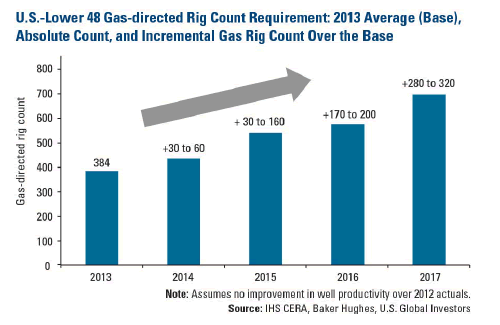

When it comes to natural gas, the cold, snowy winter has caused inventories of the commodity to rapidly decline. As the U.S. is experiencing the coldest winter in 13 years – some parts of the country have had the coldest weather in nearly three decades – natural gas inventories have been drawn down to levels we haven’t seen in 10 years.

Still, Old Man Winter hasn’t been persuasive enough for companies to respond with supply.

Based on data from the research firm IHS, 384 gas-directed rigs were online in the lower 48 states to refill storage and meet new demand coming online from the industrial sector in 2013. However, looking ahead over the next few years, the rig count is going to have to rise dramatically “as the gas market tightens in late 2014 and 2015,” which is a tremendous opportunity for investors, says IHS.

Before rig counts can increase, higher natural gas prices are needed to incentivize operators to invest in natural gas. Based on last quarter’s earnings reports, many major producers, such as EOG, Southwestern or Pioneer Natural Resources, are not planning on increasing their natural gas budgets. Bill Thomas, Chairman and CEO of EOG Resources, explained his reasoning that is part of the collective thought process across the industry:

“For the sixth year in a row we are not [trying to] grow EOG’s North American natural gas production. This is reflective of our view of low returns on natural gas investments. We won’t drill any dry gas wells in North America during 2014 because we don’t see a change in the gas oversupply picture until the 2017-2018 time frame.”

As we come out of this winter season, the complacency toward adding to rig counts may amplify the deficit in natural gas inventories.

2. U.S. Chemical Industry Has a Competitive Edge

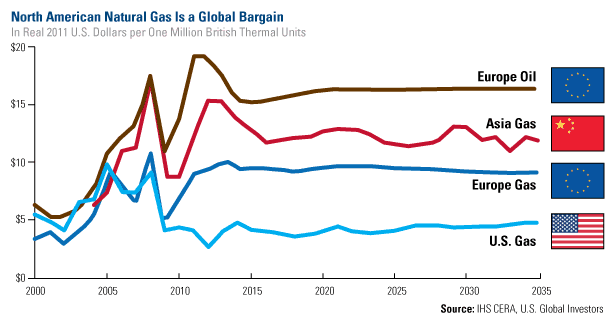

One upside to the low natural gas prices in North America is that it equates to relatively cheap feed stock for U.S. chemical companies. Whether it’s Asia or Europe, gas prices outside of the U.S. tend to be benchmarked to the higher price of crude oil.

Along with the global economic recovery, natural gas is giving the U.S. a competitive advantage. We’re seeing chemical companies coming back to the states, creating jobs, expanding exports out of the U.S., and helping the nation’s current account deficit.

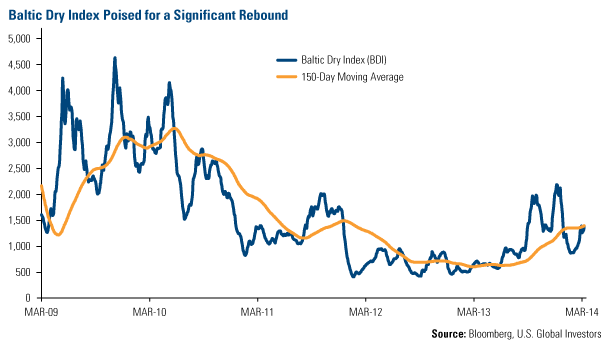

3. Shipping Companies at a Possible Inflection Point

The prices to ship commodities around the world have been hovering around the lowest we’ve seen in five years. However, demand for shipping is starting to overtake the supply of new ships, which bodes well for shipping companies.

Take a look at the chart showing the Baltic Dry Index over the past five years. The index is made up of various sizes of carriers including the Baltic Capesize, Panamax, Handysize and Supramax indices and measures the price of moving raw materials by sea. Primarily, these vessels transport iron ore and grains, i.e., wheat, corn and soybeans, which are especially vital goods for China.

To keep its population of 1.3 billion fed, China needs to import millions of tonnes of wheat, corn, rice and soybeans. As this demand is recognized, shipping companies should benefit.

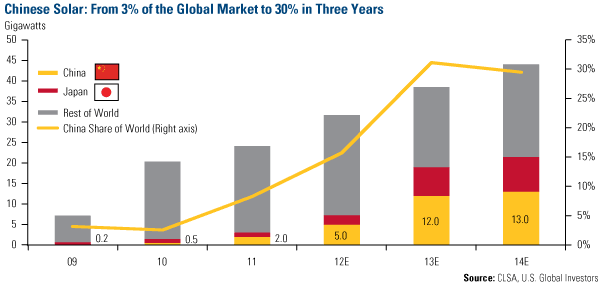

4. Alternative Energy Could Get You More Green

In China, residents have been dealing with increasing cancer-causing pollutants and vehicle congestion on roads, and public discontent is rising. This winter, as pollution grew to be 10 times higher than the acceptable rate, Beijing University students protested the conditions by putting masks on iconic statues.

The effect that pollution is having on China’s economy benefits certain industries, including renewable energy or clean energy, whether it’s solar or wind power

You can see just how dramatic the investment has been over the last five years. Specifically, wind power and solar look especially attractive. Take a look at CLSA data: In 2009, the country had about 0.2 percent of the global market. By 2014, it’s estimated to grow to one-third of the global market.

China isn’t the only country with a growing renewable energy market. With the Fukushima nuclear reactors incident after the massive earthquake in Japan, the solar market is taking off there too.

The Diverse Approach of the Global Resources Fund (PSPFX)

We believe these areas of the market offer the most exciting opportunities today. They have the wind at their back, giving us the confidence to overweight the companies within these areas of the market that are also showing extremely robust fundamentals.

Because of the diversity and volatility of each commodity, we believe investors benefit by holding a diversified selection of commodity stocks actively managed by professionals who understand these specialized assets and the global trends affecting them.

I just flew back from Asia, where I spoke at Robert Friedland’s Asia Mining Club and Mines and Money Hong Kong, with a special stop in Carslbad, CA on my way home to speak at the Investment U Conference. It has been an exhilarating week meeting with global entrepreneurs, mining executives and curious investors. I look forward to sharing their advice and insights with you next week.

P.s. It’s not too late to join me for an investment adventure in Turkey in May.

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting www.usfunds.com or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Distributed by U.S. Global Brokerage, Inc.

Fund portfolios are actively managed, and holdings may change daily. Holdings are reported as of the most recent quarter-end. Holdings in the Global Resources as a percentage of net assets as of 12/31/13: Energy Select Sector SPDR ETF 0.00%; EOG 0.00%; Pioneer Natural Resources (2.18%); Southwestern 0.00%

Because the Global Resources Fund concentrates its investments in a specific industry, the fund may be subject to greater risks and fluctuations than a portfolio representing a broader range of industries.

The first quarter is in the bag. While stocks managed to stay out of the red (barely) to end the first three trading months of the year, I continue to see more exciting setups in the commodities market…

That makes today the perfect opportunity to talk about some of the bigger trends shaping up so far this year in the commodities space…

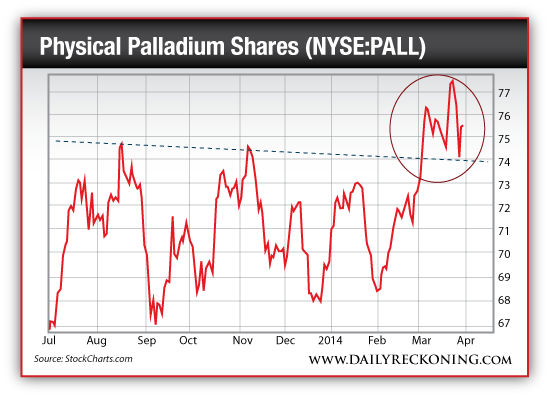

“The palladium trade is down so far,” writes an anxious reader. “What is the timing where we should see a move?”

Well, let’s see…

Palladium has been volatile since its breakout in early March. Take a look:

I’ve circled the post-breakout congestion in red. Despite the wild moves palladium has held above the breakout zone. That’s a bullish sign–and an opportunity to jump on this trade if you missed it a few weeks ago.

Ultimately, I think palladium will make a bigger move higher from here. Patience is key…

About Greg Guenthner

Greg Guenthner, CMT, is the editor of the Daily Reckoning’s Rude Awakening. Greg is a member of the Market Technicians Association and holds the Chartered Market Technician designation.

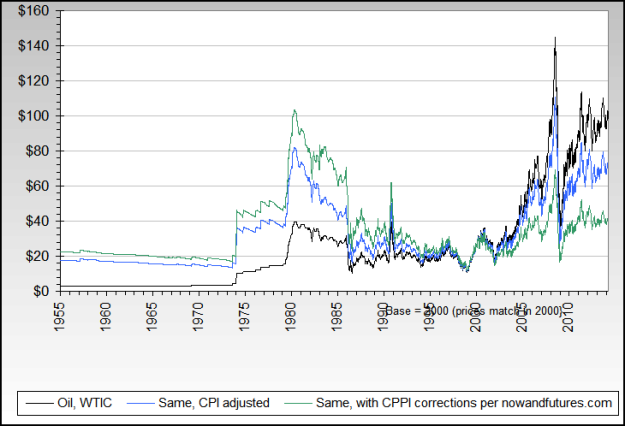

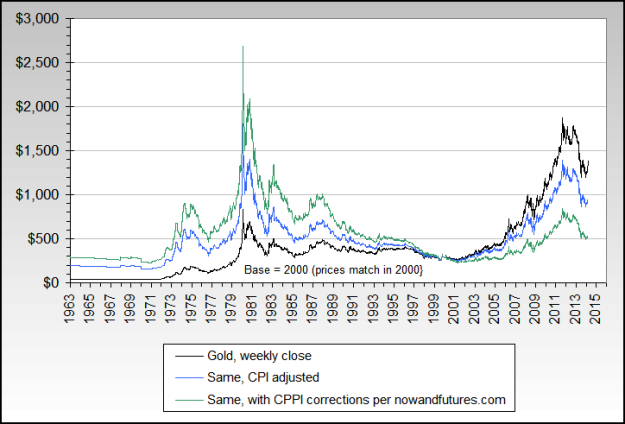

A 50 year look at commodities, their current prices & inflation adjusted prices. These 5 & 6 Decade charts provide a perspective that is not found easily. If nothing else, a quick scan is recommended – Editor Money Talks

get a lot of comments from various investors wondering why I am so bullish commodities, and in particular Agriculture. They claim that commodity prices are way too high and will collapse soon enough. Who knows… maybe these investors are right.

Having said that, today I thought I’d share with you some great long term charts from Now And Futures blog showing the nominal and inflation adjusted prices of various commodities. When I look at these charts, I wonder how on earth could some of these cheap commodities “collapse”? I mean, they are already so depressed… and so beaten down… relative to history… relative to inflation… relative to other asset classes.

I think a lot of investors are stuck with their annual charts, looking back only 365 days of the year. I think it is time to look back five to six decades of data to see where we truly are. Enjoy!

(2 examples of the 10 Commodities examined – Editor Money Talks)

….view all 10 Charts including the Agricultural Commodities HERE

Who will benefit from uranium’s revival?

Global fuel stocks are insufficient, and unmet demand for uranium is growing so it doesn’t take a Ouija board to predict a rebound in the price of uranium In this interview withThe Energy Report, David Sadowski, a mining research analyst at Raymond James, explains the forces that will push the price of uranium, and the companies that are likely to benefit. Being selective, he says, will provide the greatest rewards.

The Energy Report: David, the uranium price remains below the cost of production for many producers and the forecasts for uranium production are flat. Why are you optimistic about the uranium space?

David Sadowski: In the current price environment, supply won’t be able to keep up with demand growth. That’s really the core to the uranium investment thesis. The cost of uranium production spans a pretty wide range, from the mid- to high-teens per pound for the cheapest in-situ leach mines in Kazakhstan, to $50–60/pound ($50–60/lb) for some of the lower-grade, conventional assets in Africa, Australia and East Asia. So we’re looking at about $40 to produce your average pound of uranium. That number is climbing on cost inflation and depletion of the best mines.

The current spot price is under $36/lb, so many operations are underwater right now. That’s why we’ve seen numerous deferrals of projects and even shutdowns of existing mines, the most significant of which was Paladin Energy Ltd.’s (PDN:TSX; PDN:ASX) Kayelekera at the beginning of February. That’s on top of operations that are at risk for other reasons. In just the last few months, we’ve seen four of the world’s largest mines owned by Rio Tinto Plc (RIO:NYSE; RIO:ASX; RIO:LSE; RTPPF:OTCPK) and AREVA SA (AREVA:EPA) shut down on operational and political hiccups. Then you look at where the supposed growth is coming from over the next several years— Cameco Corp.’s (CCO:TSX; CCJ:NYSE) Cigar Lake and China’s Husab. Those are technically very challenging, too. All of this is occurring in a world no longer benefitting from a steady 24 million pounds per year (24 Mlb/year) supply of uranium from downblended Russian warheads. In short, the supply side is a basket case.

Yet demand growth keeps chugging along. European Union (EU) and North American growth perhaps isn’t what it was a couple of decades ago. Pressure from competing energy sources like liquefied natural gas (LNG) in the U.S. is causing some operators to switch off their older, smaller reactors. But reactor retirements are being more than offset by new reactor construction not only in the U.S. and EU, but much more important, in Asia and in Russia. China, India, Korea and Russia are collectively constructing 70 reactors right now.

TER: Japan and the United Arab Emirates (UAE) just announced a program to cooperate in developing nuclear technology. What’s the market significance of that?

DS: There is a push toward nuclear in many of these nations in the Middle East. Not only do they have pretty strong population growth and urbanization, thus electricity growth is strong, but some of those oil-rich nations have cited a preference to sell their petroleum into the international markets rather than domestically. The UAE is a very large potential source of demand growth. It is constructing two nuclear power plants at the moment and is imminently going to break ground on two more. There are an additional 41 new nuclear reactors on the drawing board in the Middle East. So in the context of 434 operable reactors today, that’s a very meaningful amount of growth potential.

Demand growth remains resilient, and supply is lagging behind. In just a few years, we think this will lead to a deficit that will quickly grow to crisis levels. That’s why we’re bullish. Uranium prices have to go higher to incentivize more supply to meet this looming supply gap.

TER: Why hasn’t that happened yet?

DS: There are just a few forces working against the price. Since the Fukushima accident in Japan, there has been a supply glut in the marketplace. There has been a decrease in demand, with a lower level of buying by some countries, like Germany, Switzerland and, of course, Japan. Additionally, some extra supply was coming out of the U.S. government. There is an extra amount coming from enrichment underfeeding. If you add all that up, there has been essentially more supply than is required, and that puts downward pressure on prices. It’s caused the utilities to take a step back from the market.

TER: So do you think conditions in the market itself will materially improve? What will that look like?

DS: For us, it comes down to when the utilities start getting involved again. While the utilities have been sitting on the sidelines over the last couple of years, high-fiving each other for not buying uranium in a declining price environment, their uncovered requirements in the future have actually risen quite dramatically. At some point, they have to resume long-term contracting to cover all those needs. Japan is a key catalyst.

Japan’s reactors were slowly shut down after the Fukushima accident. Right now, none of them are operating. The country’s inventories have piled up to probably around 100 Mlb. Many of these utilities have asked their suppliers to delay deliveries of fresh uranium. That material ends up in the marketplace one way or another, so it’s having a price-dampening effect. In late February, however, the Japanese government announced its final-draft energy plan. Japan will restart at least some of its reactors to stop spending a ludicrous amount of money on imported fossil fuels. There are other economic and environmental benefits, but it’s the country’s trade balance that is really driving the restart push.

It’s these restarts that we think will spur global utilities outside Japan to resume buying. The signal will be sent that Japan won’t be dumping its inventories, it won’t be deferring deliveries anymore and, by the way, there is not enough supply to go around in just a few years so you better start contracting again. That’s what we think is going to support prices.

TER: That basic energy plan in Japan is a draft, but there is a lot of public opinion against it. You do think its prospects are good?

DS: Consensus is that the plan is going to be approved by the cabinet by the end of March. The opposition is highly regionalized, and many pockets of the country are actually very pronuclear. Nuclear, obviously, provides a lot of jobs and generates a lot of tax revenue in these regions.

TER: Raymond James has revised its uranium supply-demand balance and anticipates a growing supply deficit beginning in 2017. What is the case for investing in the industry today with a payoff so far in the future?

DS: A shortfall beginning in 2017 doesn’t mean prices don’t move until 2017. In fact, in a healthy market, they should have moved already. But, again, it comes back to the utilities. They view the nuclear fuel market and their own fuel requirements as a game of risk management.

Today, many utilities are sitting on near-record piles of material, so there’s not a great deal of risk to the utilities with respect to supply availability over the next couple of years. However, as these groups start to look out beyond that period to 2017, 2018 and so on, they’ll realize that it could become more challenging to get the uranium they need. Given that the utilities typically contract three to four years in advance, we’re very close to that window where we expect buying to ramp up again and prices to move upward. Again, critically, we expect Japanese restarts to be an important catalyst in that resumption of buying. We expect first restarts in H2/14 with a half-dozen units online by Christmas. So from an investor’s point of view, we’re already seeing the benefit of this outlook. That’s been driving the uranium equities upward over the past couple of months.

TER: You’re forecasting spot uranium prices averaging $42/lb in 2014, but three months into the year, the price is still struggling to break $36. What will drive it over $42? When do you expect that to happen?

DS: We think the move this year is likely to happen toward the end of this year, as Japanese restarts spark a return of normal buying levels by utilities. The uranium price should really start moving in 2015.

TER: What indicators should investors look for in watching the uranium price trend?

DS: One of the best indicators is Uranium Participation Corp. (U:TSX). Since the fund’s inception, this stock has been a remarkably accurate predictor of where the uranium spot price is headed. When Uranium Participation’s share price is above its net asset value (NAV), the market is baking a higher uranium price into its valuation of the stock because the NAV is calculated at current uranium prices. For even more precision, you can divide the company’s enterprise value by its uranium holdings for a rough dollar/pound estimate on what the market is ascribing. So right now, we calculate the fund is implying $40/lb, and that’s over $4 above the current spot price. This is by no means a bulletproof measure, but absent a black swan event, history tells us that this could be the destination for the price in the near future.

TER: You have said you see $70/lb as the price that will incentivize new mining. What should investors do while they’re waiting for the price to reach that level?

DS: Buy uranium equities. It’s that simple. We think prices are going higher, so buy uranium stocks well ahead of the upswing.

TER: Do you have a target time that you expect the price to reach that level?

DS: We’re looking for the price to reach $70/lb in 2016. We forecast prices flat forward at $70 from that year onward.

TER: Which mining companies are the best investment prospects in this environment? Which are the weaker ones?

DS: They say a rising tide floats all boats. We think all the uranium stocks are probably going higher, or at least the vast majority of them. But we also believe being selective will provide the greatest rewards. Most investors should be looking at names with quality assets, management teams and capital structures.

Among producers, our preferred companies are focused on relatively high-grade projects with solid balance sheets and fixed-price contracts that can buffer them against near-term spot price weakness. After all, we think the spot price could remain weak for most of the balance of 2014.

On the explorer and developer side, the theme is the same—companies with cash and meaningful upcoming catalysts and, again, in good jurisdictions. But if you can tolerate an increased level of risk, I’d be looking at companies with lower-grade assets in Africa. Those are probably the highest-leveraged names out there.

TER: What other favorites can you suggest?

DS: Our top picks at the moment in the space are Fission Uranium Corp. (FCU:TSX.V) and Denison Mines Corp. (DML:TSX; DNN:NYSE.MKT).

Fission has been a top pick in the space for some time. We have a $2/share target and a Strong Buy rating. We view Patterson Lake South as the world’s last known, high-grade, open-pittable uranium asset. It has immense scarcity value. There are not very many projects in the world that can yield a drill intersection of 117 meters (117m) grading 8.5% uranium, as hole 129 did in February. There is only one project in the world where you would find an interval like that starting at 56m below surface, and that’s Fission’s Patterson Lake South. It’s in the best jurisdiction, has a management team that has executed very well and has huge growth potential. We think that property probably hosts over 150 Mlb uranium. We would be very surprised if the company was not taken out at some point in the next two years.

Denison is another story we like a lot. We have a $2/share target and Outperform rating on the stock. Denison has the most dominant land holding of all juniors in the world’s most prolific uranium jurisdiction, the Athabasca Basin in Canada, the same region as Fission Uranium’s Patterson Lake South. The company will run exploration programs at 20 projects in Canada this year, including an $8 million ($8M) campaign at Wheeler River, the world’s third-highest-grading deposit, which continues to grow in size, and with a new understanding of its high-grade potential uncovered last year.

Denison has a stake in the McClean Lake mill, which is also one of its crown jewels. It’s the world’s most advanced uranium processing facility, and it’s located a stone’s throw from hundreds of millions of pounds of high-grade Athabasca uranium deposits. It’s a big part of the reason why we think Denison will get bought out at some point, particularly given that to permit and construct a new mill in the basin would be a herculean task. Denison has a very strong management team and cash position and, once again, big-time scarcity value. It’s one of the only three North American uranium vehicles exceeding a $0.5B market cap. Denison has been and will continue to be a go-to name in the space.

TER: What is another interesting name in your coverage universe?

DS: UEX Corp. (UEX:TSX) owns 49% of the world’s second-largest undeveloped, high-grade uranium asset in Shea Creek and 96 Mlb in NI-43-101-compliant resources. It’s the biggest deposit with that kind of junior ownership in the Athabasca Basin. It’s a strategic asset and the company’s main value driver. But with the uranium price where it is, the company is also focusing on shallower assets near what is now the southern boundary of the Athabasca Basin, closer to Fission’s Patterson Lake South. We’re really interested to see what comes of the Laurie and Mirror projects this year.

We have a $0.60 target price on shares of UEX.

TER: Is any of that influenced by the fact that it has a new CEO?

DS: The target price is not heavily influenced by the recent change in CEO. I think the outgoing CEO, Graham Thody, did an excellent job. I’m very hopeful that Roger Lemaitre will continue that trend. Under the new CEO, I would anticipate that the company may ramp back up the level of work intensity at Shea Creek, to build on the achievements of AREVA and the UEX team as well as Thody. But given Lemaitre ‘s background, including his experience as head of Cameco’s global exploration, I wouldn’t be surprised to see UEX extend its view beyond the Athabasca Basin as a potential consolidator in some other jurisdictions that may be lagging behind a bit on valuation.

TER: You raised your target for Cameco from $25/share to $26/share. Are you expecting the rise to continue there?

DS: Despite the recent run-up in shares, we think there’s a good chance of further strength. Cameco is the industry’s blue-chip stock. It’s the one everyone thinks of when they think of uranium. Given its size and liquidity, it is the only stock many of the big institutional fund managers can invest in. With that backdrop, we think it’s going to be the first stock for fund flows as the space continues to rerate, especially as we get more confirmatory news about Japanese restarts and as Cigar Lake passes through the riskiest part of its ramp-up. We think it should be a very good 24 months for the company.

TER: What other companies do you like in the uranium space?

DS: We recently upgraded Kivalliq Energy Corp. (KIV:TSX.V) to an Outperform rating. Our target price there is $0.50/share. The company has been a laggard in the last few months, but it has Angilak, a solid asset in Nunavut with established high-grade pounds and huge growth potential. Current resources stand at 43 Mlb, but we think there is well over 100 Mlb of district-scale potential. The company is derisking the asset by moving forward with engineering work, like metallurgy and beneficiation, ahead of a preliminary economic assessment potentially later this year. We’re also excited to see what comes with the newly acquired Genesis claims that sit on the same structural corridor that hosts all the mines of the East Athabasca Basin.

We also like Ur-Energy Inc. (URE:TSX; URG:NYSE.MKT), on which we have an Outperform rating and $2.20/share target price. This stock has been on a major tear. We continue to expect great things from Lost Creek in Wyoming. Early numbers from the mine, which just started up in August, have been hugely impressive to us, a testament to the ore body and execution by management. And the financial results should be equally strong, given the company’s high fixed-price contracts. In all, it’s a solid, low-cost miner in a safe jurisdiction, which we think should be in a good position to grow production organically or, using cash flow, buy up cheap assets in the western U.S., a region ripe for consolidation of in-situ leach uranium assets.

TER: Do you have any parting words for investors in the uranium space?

DS: I would just say we think the uranium price is going higher over the next 12–24 months. So in anticipation of that upswing, we recommend investors take a hard look at high-quality uranium stocks today.

TER: You’ve given us a lot to chew on. I appreciate your time.

DS: It’s my pleasure, as always.

David Sadowski is a mining equity research analyst at Raymond James, and has been covering the uranium and junior precious metals spaces for the past seven years. Prior to joining the firm, David worked as a geologist in western Canada with multiple Vancouver-based junior exploration companies, focused on base and precious metals. David holds a Bachelor of Science in Geological Sciences from the University of British Columbia.

Want to read more Energy Report interviews like this? Sign up for our free e-newsletter, and you’ll learn when new articles have been published. To see a list of recent interviews with industry analysts and commentators, visit our Streetwise Interviews page.

DISCLOSURE:

1) Tom Armistead conducted this interview for Streetwise Reports LLC, publisher of The Gold Report, The Energy Report, The Life Sciences Report and The Mining Report, and provides services to Streetwise Reports as an independent contractor.

2) Streetwise Reports does not accept stock in exchange for its services.

3) David Sadowski: I was not paid by Streetwise Reports for participating in this interview. Comments and opinions expressed are my own comments and opinions. I had the opportunity to review the interview for accuracy as of the date of the interview and am responsible for the content of the interview. This interview took place on February 28, 2014. All ratings, facts and figures are reflective of the date of the interview.

4) Interviews are edited for clarity. Streetwise Reports does not make editorial comments or change experts’ statements without their consent.

5) The interview does not constitute investment advice. Each reader is encouraged to consult with his or her individual financial professional and any action a reader takes as a result of information presented here is his or her own responsibility. By opening this page, each reader accepts and agrees to Streetwise Reports’ terms of use and full legal disclaimer.

6) From time to time, Streetwise Reports LLC and its directors, officers, employees or members of their families, as well as persons interviewed for articles and interviews on the site, may have a long or short position in securities mentioned. Directors, officers, employees or members of their families are prohibited from making purchases and/or sales of those securities in the open market or otherwise during the up-to-four-week interval from the time of the interview until after it publishes.

Streetwise – The Energy Report is Copyright © 2014 by Streetwise Reports LLC. All rights are reserved. Streetwise Reports LLC hereby grants an unrestricted license to use or disseminate this copyrighted material (i) only in whole (and always including this disclaimer), but (ii) never in part.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair