Currency

The US dollar has been rallying strongly for several months. That’s what we call a “gift horse.” And just as the saying goes, “Don’t look a gift horse in the mouth.” Instead, look for ways to exchange your strong dollars for other currencies and investable assets that don’t fly out of Federal Reserve Chairman Ben Bernanke’s printing press.

For many Americans, foreign investments are more of an accident than an objective. They might own a few foreign stocks through a global mutual fund. Or they might have some exposure to foreign economies and currencies through the shares of an American multinational corporation like Johnson & Johnson or GE.

But American stocks and bonds remain the steak and potatoes of traditional American investment portfolios. Foreign stocks and bonds are merely the spices and sauces. This provincialism — epitomized by the spectacular success of Warren Buffett’s Berkshire Hathaway — has served American investors very well for several decades. But a reassessment may be in order.

Simply stated, the America of the future may not reward investors as handsomely as the America of the past. For example, despite doubling from its lows of March 2009, the S&P 500 index has produced a negative total return during the last five years… and only a miniscule return during the last 10 years.

The US dollar’s role as the ultimate “safe haven” currency is also due for a reassessment. While the dollar may be safer than the euro, for example, the dollar is hardly safe in any absolute sense. The dollar is safer than the euro… just as a rabid squirrel is safer than a rabid wolf. But you don’t really want to cuddle up at night with either one.

America’s federal debt has exploded to more than 100% of GDP — an astonishingly large Greek-like debt load. Yet none of America’s political or financial leaders seem to have any plan for reducing the nation’s debt… except maybe to add a graveyard shift to the dollar-printing production line at the Philadelphia Mint.

Our advice: Spend your strong dollars while you can. Reallocate them into other currencies and asset classes.

Throughout the eurozone crisis of the last few months, the US dollar has been attracting widespread “flight to safety” demand. But the dollar is not merely rallying against the euro; it is rallying against almost every investable asset on the planet. For example, a dollar buys 36% more silver today than it did six months ago. A dollar also buys 20% more wheat, 13% more corn… and even 2% more “American house.”

If we broaden out our analysis to include stocks and currencies, the results are similar. A dollar buys 32% more French stocks today than it did six months ago… as well as 34% more Indian stocks and 18% more Japanese stocks. Among world currencies, a dollar buys 11% more Norwegian kroner today than six months ago… as well as 15% more Swiss francs and 8% more Canadian dollars.

It is that last financial asset — the Canadian dollar — that we find particularly compelling as an alternative to holding US dollars. The Canadian dollar, known affectionately as the “loonie,” possesses many virtues.

In no particular order:

- Canadian government finances are fairly solid; US government finances are spiraling out of control. Canada stands out as being one of the few countries that is not only rated AAA by the major credit agencies, but actually possesses a AAA balance sheet… or at least something close to AAA.

- Canada’s GDP growth is outpacing US GDP growth.

Canadian employment growth is booming; U.S employment growth is moribund. The Canadian economy has created nearly 800,000 jobs during the last five years, while the US economy has lost more than 5 million! In other words, the Canadian labor force has expanded by 4%, while the US labor force has contracted by 4%!

As a result of these trends, Canada is becoming an increasingly attractive investment destination, relative to the US The Canadian dollar, in particular, is increasingly attractive. The Canadian dollar’s appeal is hardly a new story, but it remains a very relevant story.

As the nearby chart illustrates, the Canadian dollar has been trending higher against the US dollar for several years. We expect this trend to continue — more or less — over the next several years. But investors should expect some bumps along the way. Currencies can sometimes bounce around even more than stocks. The Canadian dollar plummeted more than 25% during the depths of the 2008 credit crisis, for example, as terrified investors piled into the US dollar. Once the crisis eased, the Canadian dollar recovered. But the lesson is clear: Currencies can be volatile.

If you have a mind to Fed Reserve-proof a strong dollar, we like the Canadian dollar.

Regards,

Addison Wiggin

for The Daily Reckoning

Joel’s Note: It’s hard to put one’s finger on the exact date it began, but harder still to deny that the American Empire is in gradual, inexorable decline. It’s nothing personal. All things come to an end…even world dominance.

Some say the beginning of the end ticked over in 1913, with the passing of the Federal Reserve Act and the introduction of the Income Tax. Others argue all was well until Richard “Tricky Dick” Nixon cut the dollar’s last, tenuous ties with gold in 1971. Or maybe it was when the military industrial complex found the excuse it needed to kick into overdrive at the beginning of this millennium. Who knows?

In any case, the writing has been on the wall for some time. What we do know is that, as the managed economy attracts more and more meddlesome parasites, each with a nosier fix than the last, the boom-bust cycle increases in both frequency and magnitude. This general trend has led Addison to forecast the “Mother of All Bubbles.”

Find out what he’s talking about…and discover the safe haven investments you can employ to help protect yourself, right here.

“Where there is a crisis, there may be opportunities – but not necessarily in the places one might expect.”

“the course Europe is on may avoid chaos now, but may lead to disintegration down the road. These are serious matters, as the odds of anarchy, followed by military control of Greece have increased substantially. When we suggest that the road to hell is paved with the best of intentions, we are serious.

What does it mean for the euro? Massive short positions previously built-up need to be unwound. As central bankers around the world hope for the best, but plan for the worst, lots of money is being printed: by the Fed, the ECB, the Bank of England (BoE) and Bank of Japan (BoJ), to name the prime instigators. Commodity currencies, i.e. the Australian Dollar (AUD), New Zealand Dollar (NZD) and Canadian Dollar (CAD) should be the main beneficiaries. While these currencies have performed well, Australia is undergoing some domestic political turmoil and Canada’s fate is closely linked to that of the U.S.; as a result, the NZD would be our favorite in that group. Having said that, geopolitical tensions and monetary easing have boosted oil prices in particular, causing headwinds to global economic growth and, with it, also to commodity currencies. If those headwinds play out further, we would make the Norwegian Krone (NOK) our preferred choice, as Norway benefits from rising oil prices, as well as providing investors with relative safety in Europe. It’s not surprising that gold, the one currency with intrinsic value, continues to appreciate in this environment.”

….read the whole article HERE

One of the ways I look at the market is in terms of a giant teeter-totter…I see the market swinging up and down as psychology changes from bullish to bearish. I try to judge what the prevailing mood is, relative to whatever time frame I’m using, and then either establish a position in line with the trend or look for signs that the trend is about to change. I use hard data such as the COT reports, gut instincts such as how a bull market takes bad news, and chart patterns to gauge whether a trend is likely to continue or reverse. I’m mindful that market trends often go far beyond what I think is reasonable so I’ve developed a risk management technique I call, “Anticipate…but wait for confirmation,” to restrain myself from trying to pick tops and bottoms.

We had the biggest credit blow-out in history in 2007-08 (after 30 years of boom times) and asset markets collapsed in anticipation of a depression. Authorities around the world countered the deflationary forces with massive fiscal and monetary stimulus (again and again and again.)

In teeter-totter terms the market will rally when it thinks that the authorities are prevailing (like now) and will fall (like August/September of last year) when it thinks that the authorities are losing the battle against deflation. So we have risk-on, risk-off, as public confidence in central planning waxes and wanes.

…..read more of Victor’s analysis HERE

It is said that markets discount the stuff we do know and run on the stuff we don’t. Let’s take a look at what we do know, might know, and some best guesses about the future (called forecasts by “serious” analysts), as it relates to the rally in EUR/USD:

1. Euro short rates relative to the US have turned higher again, i.e. the yield differential in favor of euro is improving.

Question: Will this continue?

Best Guess: I don’t think so because euro supply may begin to overwhelm demand (see #2 below). And if US growth is for real, and a the 10 nation Eurozone recession is for real, one would expect US 3-month benchmark rates to drift higher relative to the euro.

2. European Central Bank expected to flood banks with more credit next week; euro seemed to rally sharply on the last round of Long-term Refinancing Operations (LTRO) by the European Central Bank, i.e. three-year term loans to the European banking system.

Question: Will we see the same type of rally in the periphery debt this time around?

Best Guess: Unlikely, in fact it might be a good time for those who bought last time to sell into the next round of ECB Long-term Refinancing Operations. If so, if the EUR/USD rally shows signs of stalling next week, it could be time to start looking the other way.

3. There is a lot of Fed jawboning about the potential for QE3.

Question: Is QE3 baked in the cake?

Best Guess: I don’t think so. Two points here: 1) If the US recovery is for real, it doesn’t make sense that Fed Governors are so boisterous about the potential for QE3; and 2) Even Ben Bernanke (going out on limb here) has to understand that monetary policy stimulus has limits that become counterproductive at some stage and many, including me, think we are into the counterproductive territory. Plus, how will QE3 that sits on US banks’ balance sheets help any more than the pledge to hold Fed Funds rates low into 2014, in and of itself an incredible act by a central bank chief? It is what a rational person, assuming Ben is rationale, may ask himself.

Bottom line: Though the recent move in EUR/USD is powerful, I think it is a relatively near-term event. Here’s why: 1) If the US is really growing, the dollar at some point wins on growth and yield relative to euro. Growth and yield are the intermediate-term drivers for currencies, and 2) if the US goes back into recession, a case we made in our latest Global Investor monthly issue; Europe goes into an even deeper one and China is in trouble too. This means the US dollar, for all its warts, gets a big risk bid.

We watch and see how reality plays out against our best guesses …

Captain of our fairy band,

Helena is here at hand,

And the youth, mistook by me,

Pleading for a lover’s fee.

Shall we their fond pageant see?

Lord, what fools these mortals be!

– A Midsummer Nights Dream Act 3, scene 2

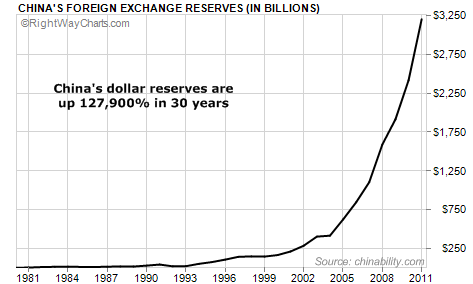

Since 1978, China has been exporting more goods than it has imported. That’s allowed the nation to stockpile trillions of Dollars. What to do with so much money?

The way it works is simple to understand. When a Chinese business earns Dollars by selling overseas, the law requires the company to hand those Dollars over to the country’s central bank, the People’s Bank of China (PBOC). In return, the business gets Chinese currency (called either the “Yuan” or the “Renminbi”) at a fixed rate.

There’s nothing fair about this. The Chinese people do all the work, and the Chinese government keeps all of the money. But that’s the way it goes.

At first, the Dollar inflow was small because trade between the two countries was tiny. In 1980, for example, China’s foreign currency reserves stood at approximately $2.5 billion. But since then, the amount of foreign currency reserves held by the Chinese government has gone up nearly every year…and now stands at $3.2 TRILLION. That’s a 127,900% increase. It’s simply astonishing to look at the chart of the increase in currency reserves…

As I mentioned yesterday, the group in China that manages these foreign reserves is called the State Administration of Foreign Exchange (SAFE). This group is engaged in a full-fledged currency war with the United States. The ultimate goal – as the Chinese have publicly stated – is to create a new dominant world currency and dislodge the US Dollar from its current reserve role.

And for the past few years, SAFE has had one big problem, where to put the money.

SAFE decided to use most of these reserves to buy US government securities. As a result, the Chinese have now accumulated a massive pile of US government debt. In fact, about two-thirds of China’s reserves remain invested in US Treasury bills, notes, and bonds. The next biggest chunk is in Euro. Of course, all this money is basically earning nothing to speak of in terms of interest…because interest rates around the world are close to zero.

And while the Chinese would love to diversify and ditch a significant portion of their US Dollar holdings, they are essentially stuck. You see, if the Chinese start selling large amounts of their US government bonds, it would push the value of those bonds (and their remaining holdings) way down. It would be like owning 10 houses on the same block in your neighborhood…and deciding to put five of them up for sale at the same time. Imagine how much that would depress the value of all the properties with so much for sale at one time.

One thing China tried to do in recent years was speculate in the US stock market. But that did not go well…The Chinese government bought large amounts of US equities just before the market began to crash in late 2007. It purchased a nearly 10% stake in the Blackstone Group (an investment firm)…and a similar stake in Morgan Stanley. Blackstone’s shares are down about 46% since the middle of 2007, and Morgan Stanley is down about 70% since the Chinese purchase.

The Chinese authorities got burned big time by the US equities markets and received a lot of heat back home. They are not eager to return to the US stock market in a meaningful way. So China’s US Dollar reserves just keep piling up in various forms of fixed income – US Treasury bonds, Fannie and Freddie mortgage bonds, and other forms of debt backed by the US government. These investments are considered totally safe – except that they’re subject to the risk of inflation.

According to a statement by the government: “SAFE will never be a speculator. It mainly seeks to protect the safety of China’s foreign exchange reserves and ensure a stable investment return.”

If the Chinese won’t buy stocks and the only real risk to their existing portfolio is inflation, what do you think they will do to hedge that risk?

They will Buy Gold…lots and lots of gold.

The Chinese are now clearly on a path to accumulate so much gold that one day soon, they will be able to restore the convertibility of their currency into a precious metal…just as they were able to do a century ago when the country was on the silver standard.

The West wasn’t kind to China back then. The country was repeatedly looted and humiliated by Russia, Japan, Britain, and the United States. But today, it is a different story…

Now, China is the fastest-growing country on Earth, with the largest cash reserves on the planet. And as befits a first-rate power, China’s currency is on the path to being backed by gold.

China desperately wants to return to its status as one of the world’s great powers…with one of the world’s great currencies. And China knows that in this day and age – when nearly all governments around the globe are printing massive amounts of currency backed by nothing but an empty promise – it can gain a huge advantage by backing its currency with a precious metal.

As the great financial historian Richard Russell wrote recently: “China wants the Renminbi to be backed with a huge percentage of gold, thereby making the Renminbi the world’s best and most trusted currency.”

I know this will all sound crazy to most folks. But most folks don’t understand gold, or why it represents real, timeless wealth. The Chinese do.

About the Bullion Vault

The BullionVault gives private investors around the world access to the professional bullion markets. You can benefit from the lowest costs for buying, selling and storing gold and silver.

We currently take care of some $2 billion for more than 34,500 users, making us the world’s largest online investment gold service.

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair