Currency

Mitt Romney thinks so:

China has an interest in trade. China wants to, as they have 20 million people coming out of the farms and coming into the cities every year, they want to be able to put them to work. They want to have access to global markets. And so we have right now something they need very badly, which is access to our market and our friends around the world, have that same– power over China. To make sure that we let them understand that in order for them to continue to have free and open access to the thing they want so badly, our markets, they have to play by the rules.

They’re a currency manipulator. And on that basis, we go before the W.T.O. and bring an action against them as a currency manipulator. And that allows us to apply tariffs where we believe they are stealing our intellectual property, hacking into our computers, or artificially lowering their prices and killing American jobs. We can’t just sit back and let China run all over us. People say, “Well, you’ll start a trade war.” There’s one going on right now, folks. They’re stealing our jobs. And we’re gonna stand up to China.”

The theory goes that by buying U.S. currency (so far they have accumulated around $3 trillion) and treasuries (around $1 trillion) on the open market, China keeps demand for the US dollar high. They can afford to buy and hold so much US currency due to their huge trade surplus with America, and they buy US currency roughly equal to this surplus. To keep this pile of dollars from increasing the Chinese money supply, China sterilises the dollar purchases by selling a proportionate amount of bonds to Chinese investors. Supposedly by boosting the dollar, yuan-denominated Chinese goods look cheap to the American (and global) consumer.

First, I don’t really think we can conclusively say that the yuan is necessarily undervalued. That is like assuming that there is some natural rate of exchange beyond prices in the real world. For every dollar that China takes out of the open market, America could print one more — something which, lest we forget — Bernanke has been very busily doing; the American monetary base has tripled since 2008. Actions have consequences; if China’s currency peg was so unsustainable, the status quo would have collapsed long ago. Until it does, we cannot conclusively say to what extent the yuan is undervalued.

To Read More CLICK HERE

John Taylor, the founder of the world’s largest currency hedge fund FX Concepts, spoke with Bloomberg TV’s Erik Schatzker and Sara Eisen and said that Greece will leave the euro this year. He went on to say that, “this summer I think is very likely…the Europeans aren’t going to give them money, the IMF’s not going to give them an OK. They will be out of money in June.”

Courtesy of Bloomberg Television

CLICK HERE to watch the video

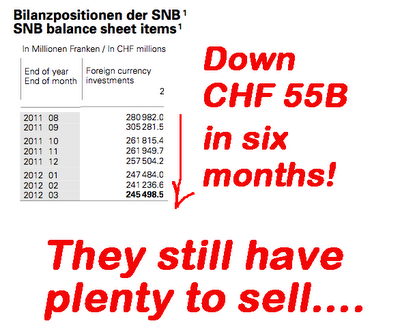

The 1st Q reserve numbers for the Swiss National Bank tell an interesting story. For a second quarter in a row, the foreign reserves have declined.

There is only one way that this could have happened; the SNB offloaded a portion of the EURCHF position it took on back in September of 2011 when it was forced to intervene.

A significant portion of the CHF 60B ($67B) “reverse intervention” was the result of the unwinding of large speculative short EURCHF positions by market players. (This demonstrates how big the speculative capital flows were.)

Some additional EURCHF sales by the SNB were, no doubt, accomplished when the market was betting that the SNB would raise the Peg from 1.20 to 1.30 or higher.

Officials at the SNB did everything they could to encourage speculation that the Peg might be raised. I find it amusing that while those officials were talking the EURCHF higher, they were actually selling on the side. Basically they lied. For an interesting perspective on this: Link

Just a few weeks ago a big shot at Goldman was selling the idea that the SNB would raise the Peg to 1.35. Maybe some of the SNB’s“chatter” rubbed off on O’Neill.

To Read More CLICK HERE

“On the threshold of a crisis,” we observed in our essay “Investing Ahead of the Curve” in the July 19, 2011 edition of The Daily Reckoning, “a fertile imagination can be an investor’s most valuable asset.”

“During normal times,” we continued, “investors can focus only on buying quality stocks one by one from the bottom up, without also trying to envision what tragedies might befall them from the top down… But it may be time to begin imagining the unimaginable.

“It may be time, in other words, to begin considering that the next phase of the global monetary system might not include the US dollar as its reserve currency…or that the next two decades of life in America might not look anything like the last two decades.”

Here in the US of A, life is still pretty good, even if the economy isn’t perfect. A true crisis seems unimaginable. After all, even the 2008 crisis wasn’t that bad. Today, the Apple store in the mall is always packed, most of the restaurants in town are full…and the dollar is still strong enough to buy a nice vacation almost anywhere in the world.

A currency crisis that triggers an economic crisis — or vice versa — just feels like a bunch of wacky doom-and-gloom stuff. And it may well be. In the context of America’s legendary resilience and economic might, a catastrophic currency crisis seems almost unimaginable… But the time has arrived to begin imagining it…not because it is certain, but because it has become less unimaginable.

The best way to defend against a currency crisis is as obvious as it is emotionally difficult: Don’t hold the currency that is hurtling toward a crisis.

There is nothing mechanically difficult about this remedy, but it can be very difficult emotionally…and tactically. An individual who trades dollars for some sort of “safer” currency, for example, risks looking like a fool for a long period of time. Not even gold is a sure bet over short-to-medium-term timeframes. This safe-haven asset tumbled about 40% against the dollar during the 2008 crisis.

In short, being “safe” can sometimes feel very dangerous…and foolish. And no one wants to look as foolish as Noah building his Ark…unless, of course, it starts raining.

When the rain started falling on Brazil in 1990…or Thailand in 1997…or Russia in 1998, investors who had traded their local currencies for US dollars or gold were able to sail through the crises relatively unscathed. As their economies tumbled into deep recessions and asset values collapsed, the folks who had parked their wealth in dollars or gold were able to preserve their wealth…and also to take advantage of the resulting bargains.

To Read More CLICK HERE

By Jack Crooks

“Beam me up Scotty.”

– Star Trek

Once again it seems the Fed Chairman Bernanke didn’t disappoint the stock bulls. I expected otherwise. Wrong again I was. I continue to be amazed by Ben’s logic here.

He says he wants to produce some inflation through monetary policy so the US economy doesn’t get caught up in a Japanese-like deflationary spiral. But in the process of creating inflation, which is in commodity prices primarily, thanks to the implicit weak dollar policy (driven by the Treasury and deftly executed by the Fed), he hurts consumers and businesses with many of these policies even though he tells us he is really saving them.

So, let me see if I get his right:

Pay those who save nothing on their deposits

Then further reduce their purchasing power by creating inflation

Continue to punish the interbank lending market (because of zero interest rates); therefore, banks have no incentive to lend to other banks that may actually have real economy lending opportunities.

Pretend the US labor market is healing, when it is now starting to weaken again, and unofficial unemployment and under-employed rate is off the charts, proving that something is very wrong with existing policy.

Then proceed to tell us how much this policy is working, and just in case there is a slowdown, tell us we will get more of this same policy that is working so well.

My head hurts after writing that.

But we do know who this policy helps—the financial economy; which consists of some very smart people who know where their bread is buttered and just so happen to have a lot of extra money lying around to make campaign contributions. Hmmm…

So Ben, you are telling us to forget about:

To Read More CLICK HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair