Currency

When there is a crisis of confidence in a currency then it is the precious metals that gain. Visit any city in Germany or Austria this summer and there is a gold shop in a prominent location.

They have not quite replaced the banks yet. But the message is there for anybody with eyes to see. It is noticeable too that this is not just a phenomenon in the peripheral eurozone but in its teutonic heart.

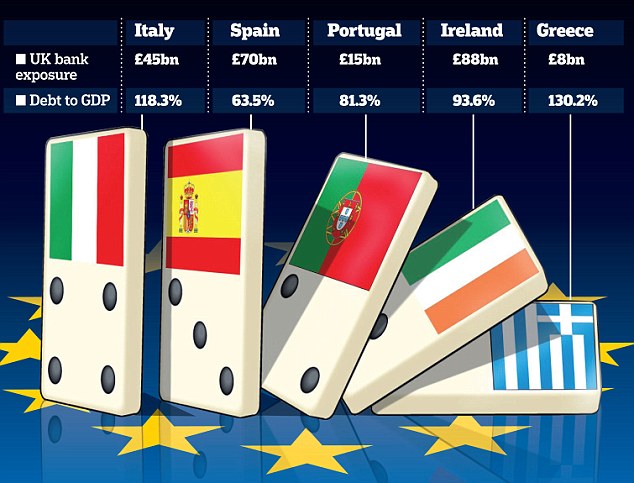

Spanish interest rates

Then again you certainly are getting good rates on your money in Spain and Italy these days, let alone Greece. Spanish bond yields have passed the danger point of seven per cent.

This is what happens when debtors become scarred about not getting repaid. Interest rates go up. No matter than the ECB has set official rates at a record low.

You can only wonder how much further this trend will go before it ends. The trend is always the investor’s best friend but so often missed for the surrounding noise.

Can anybody really see a solution in sight to the eurozone sovereign debt crisis? Does one exist? The requirement is for a federal Europe that is still a planner’s dream and even then this is no magic solution.

Besides US observers who think Europe has it all wrong and that they have the debt problem cracked are among the most deluded of our time. The US also has a temporary solution based on continuing to borrow money and that is also coming to the end of the road.

For what is happening in Spain will also hit the US in the future. The central banks can only hold interest rates low as an emergency measure, eventually market forces will take over, crush the bond market and raise interest rates.

Historical precedent

You would almost think this is stating something controversial. It is simple stating the blindingly obvious.

History also tells us that when confidence in paper money fails, that is to say bank notes and bonds, it is to precious metals that the population turns. This process happens very gradually and then there is a crunch, a crash and a reset of valuations.

…more articles at Arabianmoney

Gold is back in the news, big time, and not just because the price may be on the verge of another upswing or that Peter Munk is turning Barrick, the world’s biggest gold company, into a CEO meat grinder. It’s because Germany, it appears, wants to make gold the effective currency of the euro zone before the region plunges to the bottom of the seas like a concrete U-boat.

MORE RELATED TO THIS STORY

- IMF says Spanish banks need at least $50-billion in aid

- Stumbling economies have central banks girding for more intervention

- Greek economy continues to crumble

The weakest euro zone countries are tapped out financially and economically. But a few of them are brimming with gold reserves. Take Italy…

…..read more HERE

“The European Central Bank has reached the limit of its mandate, especially in the use of non-conventional measures… In the end, these [efforts] are risks for the taxpayers.

“It’s like morphine, the LTROs provide relief from the pain, but are not a cure for the illness.”

–ECB Governing Council member Jens Weidman, May 25.

We have often thought that interventionism is the opiate of the intellectuals.

“Investors pulled $3.05 billion from junk-bond funds globally in the week ended May 23, the most since August.”

–Bloomberg, May 25.

“Home prices drop 2% to post-crisis lows.”

–Case Shiller, May 29.

“Consumer Confidence Plunges in May”

–Yahoo! News, May 29.

The Conference Board number for May is 64.9, down from 68.7 in April, which is the biggest hit since October. The consensus was for 70. February’s 71.6 was the highest in a year.

Note that junk-bond withdrawals and consumer confidence have quickly moved to numbers seen at the culmination of the last crisis–away back last fall.

Does this suggest that current distress is culminating?

Not likely, but it is poised for some relief.

Last year’s problems began to be revealed last May and culminated in late September.

CURRENCIES

The dollar has progressed to new highs for the move, as the sovereign debt crisis resumes. The short squeeze on the DX, which is one of the features of a post-bubble contraction, continues. We had thought that the action would briefly pause at the 81 level reached in January. It only spent a few days there and with some drama has popped to almost 83.

And this is the story–drama as the world discovers that last year’s “stimulus” is not working. Well, the global economy has been rolling over.

And yet, the establishment continues in its fanaticism that intervention will make a normal post-bubble contraction go away. Unfortunately, the rise in the dollar as well as yields in Euroland insist that it is not going away. Chart on Spanish bond yields follows.

However, last week we noted that the daily RSI had reached 77.7, which was a level that could limit the move. This is now at RSI 80 and that ended the last big rally, which was to 88.7 (for the index) in 2010.

This fits with the Euro now registering a daily Downside Capitulation.

Stability in the Euro would make most everyone think that the pressures are over and Ross’s model has been reliable in signaling a rally.

This would fit with our outlook for choppy financial markets through the summer.

As instructive as it is, let’s call it a mini-crisis that is close to ending with the dollar at a daily RSI of 80. A major crisis, as in 2008, could culminate with a weekly RSI out at the 80 level. Possibly later in the year.

COMMODITIES

Last week we noted that the CRB was getting as oversold, with an RSI at 22, as at the double bottom last fall. That was at the 281 level and it has dropped to 275 with an RSI at 21. Mainly, this seems to be due to this week’s extension of weakness in crude oil and the fresh hit to natural gas. Cotton and sugar have seriously extended their 52-week lows. Cotton has plunged from 115 a year ago to 71 now. Sugar has dropped from 27 to 19.5.

This really confirms that a cyclical bear started from our “Forecaster” signal in 1Q2011.

However, base metal prices (GYX) at 363 have yet to take out last fall’s low of 356. At an RSI of just under 30 it is getting oversold enough to limit the move.

The grain’s index (GKX) has dropped to 397 and is testing last December’s low of 397. Who cares if it takes out the low, but where are the inflation bulls when you really need them?

It seems that most commodities are beat down enough to expect choppy action through the summer.

Stock Markets

Last week, the S&P got down to an RSI of 23 which could be the momentum low for the move. With this week’s pressures the index has slumped to 1311, which we take as testing last week’s low of 1292.

This will likely hold and general stock markets could be choppy through the summer. Perhaps another new paradigm is developing – – the “All-One-Chop” model?

Other than that, we are looking for a “Typical” summer. Pundits will describe each rise as a “Typical Summer Rally” and each set back will be a “Typical Summer Doldrum”.

GOLD STOCKS RELATIVE TO BULLION

- Gold’s have generally underperformed since the economy and orthodox investments arose out of the crash in mid 2009.

- Base metal mining stocks outperformed the rise in base metal prices. That ended in 1Q2011.

- The gold sector is preparing to outperform most every sector—on the planet.

SPANISH BONDS

BOB HOYE, INSTITUTIONAL ADVISORS

E-MAIL bobhoye@institutionaladvisors.com

WEBSITE: www.institutionaladvisors.com

Germany finalizing face-saving aid deal for Spain

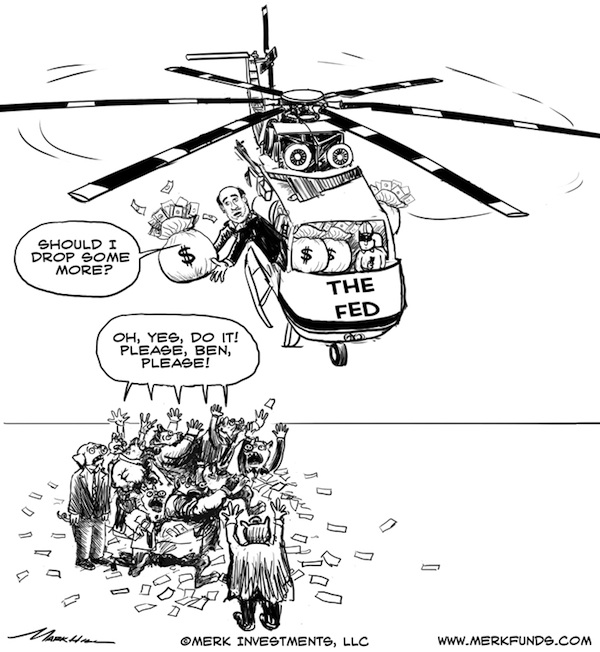

The dismal U.S. jobs report for May, released last Friday, caused the price of gold to soar as the market appears to be pricing in an ever-greater chance of “QE3” – another round of quantitative easing by the Federal Reserve (Fed). But given that 10-year government debt is already down at 1.5%, the Fed may dive deeper into its toolbox in an effort to jumpstart the economy. Investors may want to consider taking advantage of the recent U.S. dollar rally to diversify out of the greenback ahead of QE3.

o a modern central banker, it may be very simple: if the economy does not steam ahead, sprinkle some money on the problem. The Fed has done its sprinkling; indeed, the Fed has employed what one may consider a fire hose. But after QE1 and QE2, we continue to have lackluster economic growth, unable to substantially boost employment. Never mind that the real problem the global monetary system is facing is that the free market has been taken out of the pricing of risk:

…..read more HERE

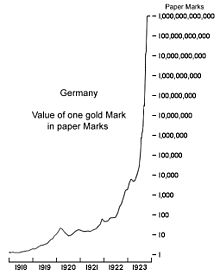

All of the hyperinflation calls have been missed by a mile. The dollar is strengthening, consumer credit is once again sinking, and treasury yields just made 60-year lows.

- This is what happens when you fail to take into consideration:

- Credit conditions Global economic conditions

- Printing by other central banks especially China

- Currency instability in Europe

- Untenable situation in Japan

Every time the US dollar ticks lower, commodity prices tick higher, or the CPI rises two tenths of a percent, hyperinflationists come out of the woodwork with nonsensical predictions and silly comparisons to Zimbabwe or Weimar Germany.

Given that the US dollar recently fell to the lower end of its trading range, hyperinflationists once again came forth with their message of impending doom.

….read why calls for Hyperinflation are so far off HERE and

(Ed Note: You can scroll down to the Headline “Alternate Nonsense” to get right to the Hyperinflation/Deflation argument). Mish’s Global Economic Analysis has an even deeper study HERE

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair