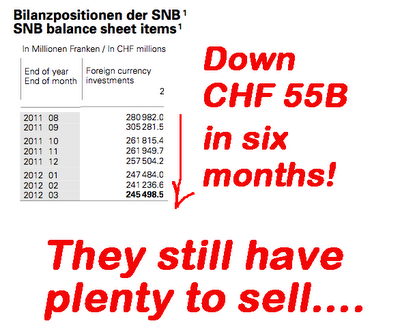

The 1st Q reserve numbers for the Swiss National Bank tell an interesting story. For a second quarter in a row, the foreign reserves have declined.

There is only one way that this could have happened; the SNB offloaded a portion of the EURCHF position it took on back in September of 2011 when it was forced to intervene.

A significant portion of the CHF 60B ($67B) “reverse intervention” was the result of the unwinding of large speculative short EURCHF positions by market players. (This demonstrates how big the speculative capital flows were.)

Some additional EURCHF sales by the SNB were, no doubt, accomplished when the market was betting that the SNB would raise the Peg from 1.20 to 1.30 or higher.

Officials at the SNB did everything they could to encourage speculation that the Peg might be raised. I find it amusing that while those officials were talking the EURCHF higher, they were actually selling on the side. Basically they lied. For an interesting perspective on this: Link

Just a few weeks ago a big shot at Goldman was selling the idea that the SNB would raise the Peg to 1.35. Maybe some of the SNB’s“chatter” rubbed off on O’Neill.

To Read More CLICK HERE