Currency

In our most recent article on gold, USD and Euro Indices we wrote that the outlook for the yellow metal was bearish just as the outlook for the Euro Index and just as it was bullish for the USD Index. At this time – since all of the above-mentioned markets moved in the opposite way – you might be wondering if we are sticking to the above analysis. In the medium-term, we do, but not in the short run. In fact, earlier this week we told our subscribers to cash in the profits from the short positions as the bullish correction was quite likely to be seen.

So, have metals bottomed? Not necessarily. Let’s take a look at the following charts and discuss them. After we describe them, you’ll see, why it’s not a sure bet (charts courtesy of http://stockcharts.com.) We’ll start with the USD Index.

The situation in the long-term chart hasn’t changed much recently and what we wrote in our last article is still up-to-date today.

(…) the long-term breakout above the declining long-term support line was not invalidated. Additionally, the USD Index reversed right in the middle of our target area. Therefore, from this perspective, it seems that the downward move – if it’s not already over – will be quite limited because the long-term support line will likely stop any further declines.

Now, let’s examine the weekly chart.

Looking at the above chart we see that after a sharp rally, which invalidated the move below the lower support line and the breakdown below the medium-term support line (a bold black line), the USD Index almost reached the previously-broken rising medium-term support line created by the August 2011 and January 2013 lows.

The invalidation of the breakdown is itself a bullish signal and it seems that we will still see more of its impact in the coming weeks.

Although we saw a correction in recent days, it is still shallow, which is a bullish signal for the short term – every now and then markets need to take a break from rallying – none of them can move in one direction all the time.

Let’s check the short-term outlook.

Quoting our previous article:

(…) the USD Index rallied in the previous week and moved above the previously-broken resistance line based on the June low. Additionally, (…) the U.S. dollar broke above the short-term resistance line based on the July and September highs. Looking at the above chart we see that both breakouts were confirmed.

On the above chart we clearly see that after the sharp late-October-November rally, the USD Index gave up some of the gains and corrected earlier growth in recent days. Despite this drop, the U.S. dollar still remains above the previously-broken resistance lines. Please note that as long as it stays above the short-term resistance line (marked with red), the situation will remain bullish.

Let’s now take a look at the Euro Index.

Larger view HERE or click on chart

Looking at the above chart we see that the October – November decline pushed the European currency to its lowest level since mid-September. At the beginning of the week the Euro Index bounced off the last week’s low and continued its upward move in the following days. In this way, the European currency almost reached the previously-broken 135 level. In spite of this fact, this week’s upswing didn’t change anything, because it didn’t even erase half of the recent decline. Taking this fact into account, it seems that further deterioration is quite likely in the coming week.

To see the current situation more clearly, let’s zoom in on our picture and move on to the medium-term chart.

From the medium-term point of view, the situation is a mirror image of what we saw on the short-term USD Index chart. After the Euro Index dropped below its rising support line and erased 50% of its entire July – October rally, we saw a relatively small move back up, which took the European currency to the 38.2% Fibonacci retracement level based on the October – November decline.

As mentioned earlier, although we’ve seen some improvement in the recent days, the Euro Index still remains below the level of 135. Additionally, the breakdown below the rising support line hasn’t been invalidated.

Please note that the current correction is still shallow, which means that the decline can continue. Even, if we see a move higher, to the 61.8% retracement level, the euro will still remain in a downtrend. From this point of view, the situation is bearish. But if we see a move below 131.56 the bearish implications will be even stronger. On a very short-term basis, though, we can’t rule out more strength in the European currency.

All in all, we could see further improvement in the Euro Index and weakness in the USD Index on a short-term basis. However, it seems that the bearish trend will remain in place as long as the euro remains below its short-term resistance line and the dollar stays above its short-term support line. Therefore, currently, the implications for the precious metal market are bullish but are likely to become bearish shortly. Please take a look at our Correlation Matrix for the confirmation of the above.

Correlations seem to have moved back to their default values in the case of the USD Index and the precious metals sector. This means that it’s no wonder that metals and miners are correcting – the reason could simply be the correction in the USD Index. The latter had quite a volatile run up in the recent weeks and – as mentioned earlier in today’s update – was something that one could have expected. Just as the trend remains up in case of the USD Index, the trend remains down in case of the precious metals sector.

Meanwhile, the correlation coefficients between PMs and the general stock market are rather insignificant on a short-term basis (with the exception of the mining stocks sector, which seems to be waiting for a decline in stocks in order to decline itself), so we can’t tell much about the possible impact of the current outlook for stocks for the prices of gold and silver.

Overall, with bullish implications from the currency sector (despite a very short-term correction that was likely triggered by the correction in currencies) and the unclear impact of the stock market, the precious metals sector seems to be set to decline once again after a quick move up.

What about gold itself? Let’s take a look.

HERE or Click on Chart for Larger View

Quoting our previous Premium Update:

Looking at the above chart we see that the situation hasn’t changed much from the long-term perspective. The medium-term outlook was bearish as gold had already broken below the long-term rising support line and the recent decline naturally hasn’t made the situation look bullish.

The medium-term trend remains down and from this perspective it seems that another local top has formed. Therefore, further deterioration is quite likely, if not immediately, then at least soon.

Gold is trading very close to the 38.2% Fibonacci retracement level ($1,285) based on the entire bull market, and just a bit more weakness might trigger a significant sell-off if the breakdown is confirmed.

Summing up, while gold could move higher in the following days – triggered by strength in the Euro Index and weakness in the USD Index – it will likely be just a counter trend move that will be followed by further declines.

Thank you for reading. Have a great and profitable week!

Przemyslaw Radomski, CFA

Founder, Editor-in-chief

Gold Price Prediction Website – SunshineProfits.com

* * * * *

Disclaimer

All essays, research and information found above represent analyses and opinions of Przemyslaw Radomski, CFA and Sunshine Profits’ associates only. As such, it may prove wrong and be a subject to change without notice. Opinions and analyses were based on data available to authors of respective essays at the time of writing. Although the information provided above is based on careful research and sources that are believed to be accurate, Przemyslaw Radomski, CFA and his associates do not guarantee the accuracy or thoroughness of the data or information reported. The opinions published above are neither an offer nor a recommendation to purchase or sell any securities. Mr. Radomski is not a Registered Securities Advisor. By reading Przemyslaw Radomski’s, CFA reports you fully agree that he will not be held responsible or liable for any decisions you make regarding any information provided in these reports. Investing, trading and speculation in any financial markets may involve high risk of loss. Przemyslaw Radomski, CFA, Sunshine Profits’ employees and affiliates as well as members of their families may have a short or long position in any securities, including those mentioned in any of the reports or essays, and may make additional purchases and/or sales of those securities without notice.

The U.S. Dollar has made a sharp move since October against a basket of currencies

Who wants a strong currency? If that question was for an opinion poll of finance ministers and central bankers, the response would be a firm no one. But in reality, no poll is needed. The last couple of weeks’ action has spoken louder than words.

Forex traders were once again reminded that when a currency makes strong gains the chances of verbal or monetary intervention are probably not far off. Losses on long positions can swiftly follow. Those long the U.S. dollar (USD) should be cautious.

Talk of currency wars has made the headlines regularly since the outbreak of the financial crisis in late-2007. A lack of economic growth prompts countries to try and grab a slice of someone else’s demand. The quickest way to do that is to devalue the national currency giving goods and services of that country a short-term competitive advantage.

The yield advantage made AUD and NZD attractive to investors engaged in carry trades – that’s borrowing in a low interest rate currency to buy a higher interest rate one. However, policy makers in those two countries decided recently that enough is enough.

Last week, the European Central Banks cut interest rates ostensibly to avoid deflation. But many observers interpreted it as a move to also weaken the EUR. It worked. On the same day of the ECB announcement the Czech Central Bank intervened sending the CZK plummeting.

A currency war victory for the ECB

How strong of a U.S. dollar is the Fed prepared to stomach?

With EUR/USD (FOREX:EURUSD) down, GBP/USD (FOREX:GBPUSD) stalled and the USD/JPY (FOREX:USDJPY) weakening, that leaves the (USD) as a potential stand-out among the majors. Since late October, the U.S. Dollar Index (NYBOT:DXZ13) has moved from around 79 to just over 81 against a basket of currencies – a fairly sharp move — although USD is still sitting below a high of 84.58 reached in September.

The question is, “Will the U.S. Federal Reserve allow USD to make continuing substantial gains against other major currencies?” After all, the U.S. economy, although not quite firing on all cylinders, is still doing better than most European counterparts. And Japan has yet to prove it can sustain its recent growth.

But the answer is that the Fed probably does not want a strong USD. That will certainly be one dilemma it faces if it ever manages to taper its quantitative easing program. Another often overlooked factor is that U.S. debt is substantially held by foreigners. This gives the U.S. authorities a strong motive to devalue – a form of default by stealth.

If USD does start making sustained gains – particularly sharp ones – dollar bulls should be cautious.

About the Author Justin Pugsley

Plus what’s next for Gold?

Plus what’s next for Gold?

When the euro arrived on the scene, it took over around 32% of global foreign exchange reserves from the USD, with the tacit approval of the U.S. This dropped the USD’s percentage of global reserves from 95% to around 63%. Since then [2000] its percentage of reserves dropped from 63% to 53% and now has risen back to 56%.

Arrival of the Euro

When the Euro arrived on the scene, gold continued to be held –with the exception of the amounts sold under the Washington Agreement and the Central Bank Gold Agreements—alongside the Yen, Sterling and the Swiss Franc.

The monetary system from the end of the World War has been firmly under the control of the U.S., with all other nations and their currencies dependent on the dollar’s proper functioning as the monetary system’s global foundation. The system functioned properly so long as the USD was managed as money measuring values across the world. Yes, the world had to accept the “exorbitant privilege” of the constant Trade Deficit, which worked well so long as the world’s economies, on balance, continued to grow, but the USD provided global liquidity and facilitated a globalization of world trade.

Unfortunately, the dollar and the Fed were beset by a major conflict of interests. On the one hand, the dollar had to be the stable base for the world’s monetary system; on the other hand, it had the task of coping with a U.S. economy and assist in maintaining stable prices and do all possible to assist in U.S. growth and low unemployment. These two tasks have become incompatible.

As this became clearer from the credit crunch in 2007 until now, confidence in the USD has declined.

Relationship of Currencies to the USD

The loss of confidence in the dollar is palpable, but as each attempt to find alternative currencies to the dollar was made, so the central banks of those currencies balked at the damage the ‘safe-haven’ treatment of their currencies caused to the int’l competitiveness. One by one, the exchange rates of ‘safe haven’ currencies was undermined by their central banks. First the Japanese Yen, then the Swiss Franc, were undermined as fleeing wealth sent their exchange rates through the roof. The net result was that other currencies showed themselves to be no more than branches on the ‘dollar tree’.

The net result has been that the entire currency system now shares in the loss of confidence in the dollar and carefully follows the course of cheapening the value of currencies alongside the dollar. This has left the dollar the sole global reserve currency once again, despite its increasingly threatening structural faults.

Loss of Confidence in the USD, then other Currencies

The fall in the percentages of the USD held as reserve assets from 63% in 1999 to 53% in 2012 precisely measured the loss of confidence in the dollar, as a currency, as attempts were made to flee to currency alternatives.

Short-term flights to other currencies still happen and will still happen as interest rate differentials remain tempting sources of profits. But the concept of ‘safe-haven’ currencies has gone. Once U.S. interest rates start to rise, we may well see a decimation of the liquidity levels. Nations with other currencies will suffer; nations with current account deficits will be the first victims of interest rate rises.

So why did the percentage of reserve portfolios move back to 56% in the second quarter of 2013?

This was an important change in the global monetary system.

Looking around after this change, it became clear that all currencies would follow the same course as the ‘Swissy’ and the Yen who are continually weakened by their central banks. With the bulk of the globe’s trade still transacted in the USD, no nation canafford to undermine its exports by allowing their currency to strengthen too much.

The same holds true of the Chinese Yuan at the moment and will do so until it can assist in carrying the mantle now being carried by the U.S. as the sole global reserve currency. The Yuan is close to becoming an alternative global reserve currency, a destination that the U.S. cannot change.

Confidence in the USD-based on Oil

Only oil producers whose balance of payments rests entirely on oil revenues, or nations who are self-sufficient in oil, can afford to allow their currencies to strengthen. This is because confidence in the dollar relies on being the currency in which oil is sold. If oil were prices in the globe’s main currencies, the exchange rate of the dollar would reflect it Balance of Payments. This would lead to a persistently declining exchange rate.

But even where an economy relies heavily on oil exports, if they have an export sector outside oil, they will force their exchange rates down or held steady against the dollar to protect those exports.

This emphasizes that the fundamental purpose of a currency is to assist in the int’l promotion of a nation. This implies that a currency is no longer a real store or measurer of value either locally of internationally.

So the dollar has returned, at the moment, to the foundation of currencies and the one that central banks will prefer to hold because it is the best of a bad bunch and the one on which the others rely.

Arrival of the Yuan

When we look forward we see the Yuan rising in importance as it becomes more and more convertible globally. Over time, expect more and more of China’s int’l transactions to be conducted in the Yuan and not via the dollar. This is a critical change as now the bulk of China’s transactions are done in the USD and then converted –by the People’s Bank of China—into Yuan. There is a date that only the gov’t of China knows, when it will make a change to that pattern.

There is a date somewhere in the near future, when China’s trade invoices are expressed in Yuan. This will necessitate the selling of local currencies directly for the Yuan to pay for imports. It is also likely that exporting countries to China are paid in Yuan and no longer in dollars. Expect the change will come about not precipitously but gradually so as to cause the least disruption to world trade. Once started, this process will not stop. The investor’s skill will be in knowing when that process impacts global trade overall.

To get this in perspective, China has well over $3 trillion in its reserves from trade as it grew steadily over the last 16 years. It’s now a vastly bigger economy and its int’l exposure on both the import and export fronts has grown alongside the expansion of reserves. If this need is changed into Yuan from the dollar, then the drop in the demand for the dollar globally will be precipitous! So it is not only the potential fall in the percentages of reserves in dollars, but the drop in the ongoing use of the dollar as a reserve currency. No nation will want a brutal change, and China will work with other nations to soften the blow much as it can.

Such a change is a pivotal change, particularly as there will be no interdependence between the Yuan and the dollar as we see between the euro and the dollar. China will not seek the interests of the U.S., and the U.S. has little concern for China’s interests.

You may think that at least China will continue to pay for its oil in dollars. Not so! Most of the oil deals China has organized can be switched into the Ruble or euro without strain, and some have already been agreed on that basis. Where there may be difficulty in doing so China will still have its vast $3+ trillion in dollars to use up so as to make the transition as smooth as possible. But eventually, China will have sufficient strength to dictate terms to all oil producers. They too may prefer to diversify out of the dollar then.

Not Gold vs. the USD, but Gold vs. all Currencies

We repeat that the overriding change that occurred since 2012 in asset allocation in reserves is that there has been a return to the dollar because that is the best of the worst among currencies, not because confidence has been restored back into the U.S. dollar. No currency is a safe-haven now.

How does that translate into an impact on gold?

What’s very clear is that if central banks feared for the prospects for the dollar up to 2012 they continue to do so now, because the situation has worsened for the dollar not improved. So where to go now?

Central banks and the entire banking system have disliked gold since the end of the Gold Standard because it prevented the devaluation of currencies without consequences. By removing gold from the monetary scene (except as a disjointed reserve asset) the consequences of devaluation have been removed, for a time. Eventually they will come back to haunt the monetary system, but so far, so good.Nevertheless, consequences are still on the way!

The first impact will hit when China forces a separation of U.S. fortunes from their own. The arrival of the Yuan as a reserve currency (almost on us) will mark the arrival of the first major consequence.

Once this happens, you will see the allocation of dollars in reserve portfolios drop again as the Yuan takes their place. The replacement of the dollar by the Yuan in reserve portfolios will go as fast as the use of the Yuan in global trade grows.

This makes sense of the World Gold Council’s statement we gave you last week,

“As more currencies are included in the reserve system, gold’s relationship with other currencies will likely evolve. It is likely that gold will retain its generally negative relationship with the US dollar, but it will also serve as a hedge againstall fiat currencies. As the monetary system evolves to make room for alternative reserve currencies, gold will have a growing prominence as a balancing mechanism against the risks inherent in fiat currencies.”

The global banking system will continue to fight against gold because of the limits it places on them, but a day is coming when confidence in fiat currencies will have fallen so low that they will reach out to gold for their very survival. As efforts to retain confidence and credibility in the current currency system start to sag, so gold will return to the global monetary system to ensure ongoing liquidity and facilitate the functioning of the current monetary system.

We emphasize that gold will not be brought back as alternative money, but in support of current paper, national money. We may be closer than we think to that point!

At that point, do not expect to see gold measuring by currencies. Gold will measure currencies.

Hold your gold in such a way that governments and banks can’t seize it!

Visit: www.stockbridgeMgMt.com And Enquire @ admin@StockbridgeMgMt.com

Get it First. Subscribe @

Legal Notice / Disclaimer

This document is not and should not be construed as an offer to sell or the solicitation of an offer to purchase or subscribe for any investment. Gold Forecaster – Global Watch / Julian D. W. Phillips / Peter Spina, have based this document on information obtained from sources it believes to be reliable but which it has not independently verified; Gold Forecaster – Global Watch / Julian D. W. Phillips / Peter Spina make no guarantee, representation or warranty and accepts no responsibility or liability as to its accuracy or completeness. Expressions of opinion are those of Gold Forecaster – Global Watch / Julian D. W. Phillips / Peter Spina only and are subject to change without notice. Gold Forecaster – Global Watch / Julian D. W. Phillips / Peter Spina assume no warranty, liability or guarantee for the current relevance, correctness or completeness of any information provided within this Report and will not be held liable for the consequence of reliance upon any opinion or statement contained herein or any omission. Furthermore, we assume no liability for any direct or indirect loss or damage or, in particular, for lost profit, which you may incur as a result of the use and existence of the information, provided within this Report.

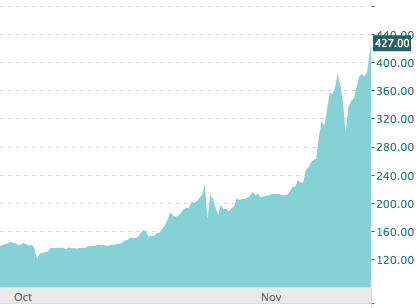

No longer wonder “why bitcoin has value?”. Bitcoin has traded in a range of 144.20 to a new high last night of 429.89. It sits at 428 this morning.

No longer wonder “why bitcoin has value?”. Bitcoin has traded in a range of 144.20 to a new high last night of 429.89. It sits at 428 this morning.

I Finally Figured Out Bitcoin

Economists,

Lieutenants,

Agents in the Field,

lend me your ears!

For I have finally figured out bitcoin! And truthfully, this is one of my best mental achievements. And hopefully, through my ability to write clearly and explain things, I may be able to explain bitcoin to us all.

I had listened to this podcast of Stefan Molyneux on bitcoin. It was very good, but did not fully answer my question, “why does a bitcoin have any value?” However, what the podcast did do is bring my perception or “observation” up high enough that I could finally see and conclude how bitcoin does actually have value.

To understand why bitcoin has value, you first need to think about why currencies exist in the first place.

The answer from an economics 202 class is “to avoid barter.”

Barter is horribly inefficient. If you are a cow herder and want a pint of ale, well, you’re out of luck. Because you can’t trade a whole cow for a measly pint of ale. Nor can you slice off pieces of beef from the live cow to make the trade more fair. Therefore, if any kind of economic trade and progress is to be made, you need a currency.

Historically, this has meant anything from gold and silver to salt and sea shells. But regardless of what item inevitably becomes an local economy’s currency, they all have some key traits and qualities in common.

Divisibility – You can divide gold, silver or salt into measurable quantities. Pounds, ounces, grams, etc. This allows you to scale the currency to the value of the item you wish to purchase.

Durability – The currency cannot rot or decay over time. Milk is a bad currency because in 3 years time it will be quite gross. Gold in 3 years time will still be gold.

Store of Value – The currency must also maintain its value and purchasing power over time. If you’re like Venezuela and constantly printing off more commie paper money, it will lose its value. But with a limited supply (gold, silver, diamonds, etc.) you can assume that currency will still have roughly the same amount of purchasing power as it did.

Finally,

Intrinsic Value – The currency must have some kind of real value. Gold can be used for jewelry. Silver can be used in electronics. Copper can be used in plumbing. Salt can be used in cooking. In other words, people will take it as a currency, because even if they don’t use it themselves, they know somebody who will. It does have an intrinsic value unto itself.

And it is here (intrinsic value) where most people get lost on bitcoin.

Bitcoin meets all the OTHER characteristics and traits of a good currency. It’s divisible. It’s durable (infinitely as it is digital). And it will not decay (again, binary doesn’t decay).

But precisely what practical, real world application does it have? You can’t use it in electronics. You can’t make jewelry (aka – buying sex) with it. So why does it have any intrinsic value at all?

The answer lies in comparing a currency’s “intrinsic value” versus its value as a currency.

For example look at what has served as the primary currency throughout most of human history – gold.

Why does gold have intrinsic value?

Economists will answer, “because you can use it in jewelry” which is the polite person’s way of saying, “men can buy sex with it.”

But does that make any sense? That ONE thing you can do with gold, “make jewelry” is why it served as the standard currency for thousands of years across the planet? What you’ll soon realize is that, yes, while gold can be used to make jewelry it serves a much more important function to society as a currency. In other words, an item’s value as a currency is really not dependent on its intrinsic value. It just needs SOME intrinsic value to get people to have faith in it and start trading it.

Salt can be used to flavor and store food. Was that grounds enough to make it the Mali Empire’s default currency?

Silver can be used to make jewelry and some industrial items. Was that grounds enough to make it the currency of the wild west?

Large clam shells could make some funky and uncomfortable bras in ancient Polynesia. Was that grounds enough to make it the default currency in the south Pacific?

Apparently so, because it DID HAPPEN. But not because of jewelry making potential or food storage potential. That was just “enough” intrinsic value to suffice. It was because those items provided more value to the economy as a currency than it did some as jewelry making materials or food flavoring. And to prove it an interesting comparison would be to compare the amount of gold (or silver) actually being used as jewelry versus that of currency, bullion or investment. I’d surmise over time, 90% of silver and gold has been used as a currency and NOT tiaras.

Understanding that a currency derives most of its value from its NON-intrinsic value traits, and only needs a “little” intrinsic value, this then puts the focus on how bitcoin derives it’s “little” but necessary intrinsic value.

The answer is simple – scarcity.

Consider diamonds.

Why do they have value?

Taking the jewelry and industrial drilling uses of it away, why do they have value?

The answer is, they don’t. They serve no purpose. At least from a PRACTICAL or PURPOSEFUL perspective.

But because they are so rare people will scramble for them. But understand what we’re talking about when we talk about “scarcity” or “rarity.” It is in relation to other things.

On this planet there is 9 quadrillion megatons of dirt and maybe 100,000 pounds of diamonds. Both dirt and diamonds have no real practical use or value, but diamonds are considered infinitely more valuable. Ergo, when we talk about scarcity, is merely a RATIO between two items that determine whether it is valuable or not. It is simply the ratio of the supply of one thing on the planet (copper) versus that of another (platinum).

And this is why bitcoin has that wee bit of necessary intrinsic value. It is very much like diamonds in that is has no practical use, but it is scarce. Matter of fact, diamonds, gold, silver, rare earth, etc., are constantly being dug up out of the ground. The makers of bitcoin have limited their supply to 21 million units forever, making it even more scarce.

In the end, bitcoin is really nothing more than a private sector currency akin to digital diamonds. And it is my opinion, you have a currency that is better than any official government fiat currency out there as it cannot be hyper-inflated away by a central bank. However, there are some drawbacks to bitcoin.

One, it is completely dependent upon the internet working. Any post apocalyptic event that shuts it down or turns off the electricity, and it’s about as valuable as those gold ETF’s you have. Two, it is not yet universally accepted by people. This may change over time, but it is a distinct (though growing) minority who use bitcoin. Three, it is such a threat to other established currencies I have no doubt in my mind governments will do everything they can to put the kibosh on it. Fourth, it can be undermined by another digital and more preferable currency.

Regardless, whether bitcoin ends up becoming a universally accepted currency is another matter. the key economic lesson to take from this is what drives the value of a currency is not so much its intrinsic value as much as it is the amount of value society puts on it as a tool for exchange.

(if you liked this post and it finally explained that NAGGING question, “how does Bitcoin have any value” please consider buying some of my books- Worthless, Enjoy the Decline, How to Privatize Governments, and Boris the Shitting Buffalo)

Perhaps you saw my comments last week BEFORE the European Central Bank surprised the markets with an interest rate cut. After seeing the inflation data come in weak, I asked:

Does that mean another LTRO (Long-Term Refinancing Operation) is right around the corner, the same corner around which the eurozone economy will supposedly turn?

Doubtful, at this stage. But don’t abandon the idea completely. If things get nasty, the European Central Bank will need to do something to help re-recapitalize a financial system built on crummy collateral.

The ECB is now moving to counteract, according to Mario Draghi’s post-meeting press conference, a “prolonged period of low inflation.”

And another ECB guy, Ewald Nowotny, is singing the same tune. Nowotny sees low inflation for some time. He also thinks stagflation is a greater risk than inflation. And another ECB guy, Jorg Asmussen, is so cautious he wouldn’t rule out negative interest rates.

Does any of this really surprise us?

If it does, it shouldn’t.

Let me offer you part of an idea we shared with our Global Investor members two weeks ago, titled:Neuroscience warns of financial market risks

Let us refer you to this Wired.co.uk article that summarizes a something else that neuroscientists are working on – it could explain, and even help anticipate, what would generate a coming collapse in risk appetite and risk markets.

“According to Lionel Barnett, lead author on the paper, they found the fact that all the elements “causally influence each other” to be of most importance. It means we must first identify all the parts of a system, then assess the relationship between individual nodes and then their causal effect on the whole. In doing so, we can find out when the fate of a node is dependant on its own behaviour because it behaves so differently from the others, and when its fate is dependant on all other nodes.

“”The dynamics of complex systems — like the brain and the economy — depend on how their elements causally influence each other; in other words, how information flows between them,” said Barnett.”

Now let us try our best to make this relevant …

Based on our shallow, yet appreciative, understanding of behavioral finance, financial markets are driven largely by sentiment. Herd mentality, for example, is one way of categorizing such sentiment.

Hence, if there is something to trigger an abrupt change in sentiment, a feedback loop, a chain reaction, can occur.

…

Back to the Wired article again:

“Using supercomputers at the Charles Sturt University in Australia, the team found that one measure called “global transfer entropy flow” reached a peak, repeatedly, “on the disordered side of the transition — just before the tipping point”.

“It’s the density of the information flow that anticipates the tipping point — “all other measures peak strictly at the tipping point itself” explained Seth.”

Now based on where our discussion is pointing, it seems counterintuitive to suggest the information flow right now is in a state of disorder and, after the tipping point is reached will converge into a state of order. After all, if the tipping point is to unleash a period of market turmoil, does that not imply disorder and chaos?

Actually, it does not if you’re thinking like a neuroscientist or Nassim Taleb. You might remember our recent review of Mr. Taleb’s new must-read book Antifragile: Things that Gain from Disorder.

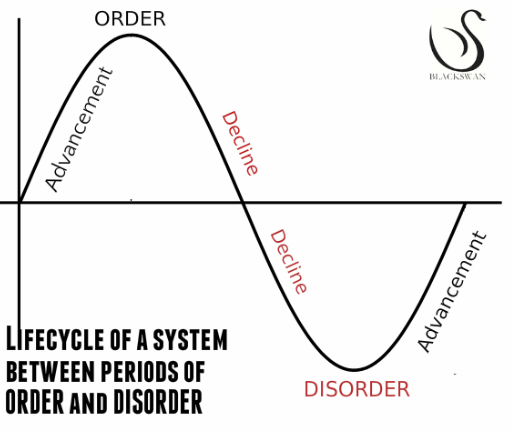

So what we should do is try to visualize the life cycle of a system’s advancement and decline between states of order and disorder. Here’s a diagram we’ve produced that we think generally applies:

I think the diagram is relatively clear. Now let’s assume the system in question is financial markets.

The financial crisis brought disorder. And that disorder bred advancement in financial markets. But amidst this advancement grew up initiatives aimed at producing order, e.g. extraordinary monetary policy.

Our central banks have built a highly-ordered financial system. And because of how the elements in such a complex financial system causally influence one another, our central banks cannot extract a vital element of the system — QE — without causing financial market instability.

It is why we’re constantly suffering through people like Larry Summers, confounded in their smug intellectualism (at best), bumbling on about keeping the lights on during a power outage. He of course equates power outage with economic/financial crisis andlights with fiscal/monetary stimulus.

It’s his analogy to why it’s so important to “contain the financial system.”

And though he did throw out a token criticism of monetary policy at the end — low rates are an inhibitor of economic growth — his overall implication is one that requires a fiscal policy to more closely manage the economy so the lights don’t go off.

But monetary policy, in an effort to enable a dysfunctional fiscal policy, has effectively commandeered control of the light-switch. But because they’ve sought stability in the financial system first and foremost. They sought merely, albeit actively, to restore sentiment instead of letting the economy clear out excesses and malinvestment.

These problems linger. And these problems continue to push down on the light-switch. The only thing holding up the light-switch is indeed extraordinary accommodation.

The million dollar question: can more accommodation, whether monetary or fiscal, in an effort to contain the financial system, eliminate the pressures pushing down on the light-switch?

As Mr. Summers mentioned, we’re four to five years down the road now. I ask: why hasn’t accommodation worked yet? And no, Paul Krugman, I’m not asking you because I already know your answer.

Are we closer to financial system decline — the collapse of the highly-ordered system — than most are willing to believe? If so, maybe we should look at the good that could come from disorder in our financial system …

After all, we’d see the deterioration of “a chronic inhibitor of economic growth”, that which is “holding our economies back from achieving their true potential.”

-JR Crooks

-

I know Mike is a very solid investor and respect his opinions very much. So if he says pay attention to this or that - I will.

~ Dale G.

-

I've started managing my own investments so view Michael's site as a one-stop shop from which to get information and perspectives.

~ Dave E.

-

Michael offers easy reading, honest, common sense information that anyone can use in a practical manner.

~ der_al.

-

A sane voice in a scrambled investment world.

~ Ed R.

Inside Edge Pro Contributors

Greg Weldon

Josef Schachter

Tyler Bollhorn

Ryan Irvine

Paul Beattie

Martin Straith

Patrick Ceresna

Mark Leibovit

James Thorne

Victor Adair